The journey to a full recovery will be a long one, but at least we’ve taken some initial steps.

We had predicted that the worst economic news would accumulate in the second quarter, with recovery starting in the third quarter. Now, as we pass the halfway mark of 2020, we see that by many measures, the recovery is already underway. Many businesses have reopened, millions of workers have returned to their jobs, and many consumers are showing eagerness to shop and dine out. The journey to a full recovery will be a long one, but at least we’ve taken some initial steps.

Though encouraging, this recovery is young and fragile. Renewed rounds of infections in several regions have led to selective slowing of the reopening. Further progress will be more difficult against this challenging public health context. We do not expect a nationwide second wave of the virus, but the prospect remains a significant risk. Tradeoffs that prioritize safety today will pay dividends in economic activity in the future.

Key Economic Indicators

Influences on the Forecast

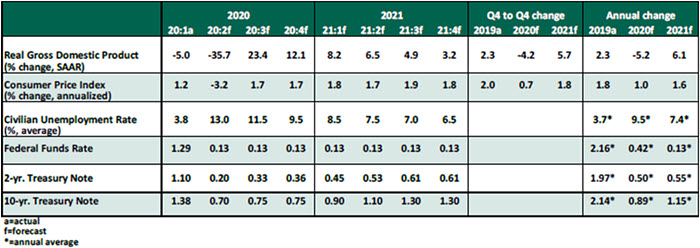

- The unemployment rate has positively surprised two months in a row, falling to 11.1% in June from 14.7% in April. Totaling May’s and June’s figures, 7.5 million jobs were recovered as lockdowns were eased. However, the crisis has left lasting damage. Total employment remains more than 14 million workers below its February figure, and more than 1.6 million workers believe their job losses are permanent. More than 31 million people are receiving some form of unemployment insurance (UI), either through conventional programs or the new Pandemic Unemployment Assistance program for self-employed workers and independent contractors.

- Fiscal policy supports were passed urgently as the crisis took hold, with a general premise of supporting the economy through a temporary disruption. Though the economy is not back to normal, many policy measures have end dates in sight. The Paycheck Protection Program reached its June 30 deadline with unspent funding and was extended into August. The supplemental UI of $600 per week will expire at the end of July, representing a dramatic loss of income for people who do not have jobs to return to. We anticipate another round of stimulus to prevent cliff-edge outcomes.

- Second-quarter economic growth, to be announced July 30, will almost certainly set a record for a single-quarter contraction. The near-total cessation of activity in April will not be offset by the gradual reopening that followed. But recent data already show the economy entering the third quarter with some momentum, with strikingly rapid month-over-month growth in indicators including retail sales, consumer spending and durable goods orders.

- After acting swiftly to ensure liquidity and stability in the financial system, the Federal Reserve is watching the progress of its policies and special purpose vehicles. The target overnight interest rate will stay at the zero lower bound for years to come, while quantitative easing will continue at a steady pace. Minor tweaks and expansions may follow, such as extending the Main Street Lending Program to nonprofit organizations.

- Inflation readings have fallen amid the severe demand shock of the lockdown. The consumer price index grew by only 0.1% year-over-year in May. The deflator on personal consumption expenditures fell to a five-year low of 0.5% in May, or 1.0% excluding food and energy. The producer price index has had two months of negative year-over-year readings in April and May. While fiscal and monetary interventions raised fears of an inflationary cycle, inflation is the least of our worries in the near term.

- The Institute for Supply Management’s Purchasing Managers Index has recovered above the 50 reading, which is considered neutral. We urge caution when using this metric, though, as large fractions of survey respondents indicate that conditions have not improved.

- Residential real estate activity is returning after slowing down amid lockdowns in the spring, which is normally the busy season for this market. Housing starts fell below normal levels in April and May, but lower inventories and low interest rates are helping to keep house price indices buoyant. Investors in commercial real estate markets, meanwhile, are reckoning with lower rent collections and potentially permanent shifts in location demand.

- The sudden onset of the pandemic and subsequent shutdown required many businesses to immediately downsize and adjust to accommodate the new reality. A reward for these rapid cost reductions may be a faster return to profitability than seen in past recessions.