Spreading Setbacks, The Paradox of Thrift, and Sports Interrupted

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- Spreading Setbacks

- The Paradox of Thrift

- Sports Interrupted

This year’s Fourth of July celebrations featured a new twist. In lieu of in-person festivals, many municipalities offered live-streamed fireworks shows. There was a lot to like about watching the pyrotechnics online: No crowds, no mosquito bites, no tired children struggling to get home at the end of the show. (The dazzling bursts from the top of the Empire State Building were spectacular.) But in the end, the night served as a reminder that we are still a long way from normalcy, and we are adapting as best we can.

As Independence Day dawned, several parts of the United States were experiencing bursts of coronavirus cases. As of this week, only half of U.S. states remain on their intended reopening paths. Twenty states have paused, while five are retreating. Arizona, California, Colorado, Florida and Texas have closed businesses including bars, movie theaters and indoor restaurants.

Economic progress will only occur at the mercy of COVID-19; growth will be held back by fear of the spreading virus. It will be important to watch the impact of the renewed outbreaks on consumers and policy makers. Lessons may be learned from the affected areas that will be useful elsewhere.

Many new metrics are helping us to gauge the recovery. In a recession characterized by a nearly complete halt to consumer activity, gauges of consumer spending are most helpful. JPMorgan Chase has answered the call by publishing spending patterns of its 30 million active credit and debit card holders. The information is rich, as it contains spending categories and locations as well as whether the cardholder was present in the store for the transaction. The report highlights some interesting correlations: States that experienced more in-person restaurant spending tended to see greater growth in viral spread. And across states, older consumers, who are at greater risk of succumbing to COVID-19, were more likely to have reduced their spending during the lockdown.

Mobile location data is also helping to provide greater insight into consumers’ actions. We have previously written about the smartphone location trends available from Apple and Google. These datasets are helpful but highly aggregated, showing resolution only by counties and for a broad set of categories of destinations. Building on this concept, location data aggregator SafeGraph is publishing more precise data, showing exact locations of users who have opted in to location sharing. Its live dashboard is showing a plateau in foot traffic, particularly to bars, restaurants and movie theaters, suggesting a local retraction and nationwide stall in the recovery.

“The consequences of failed reopenings are visible in the economic data.”

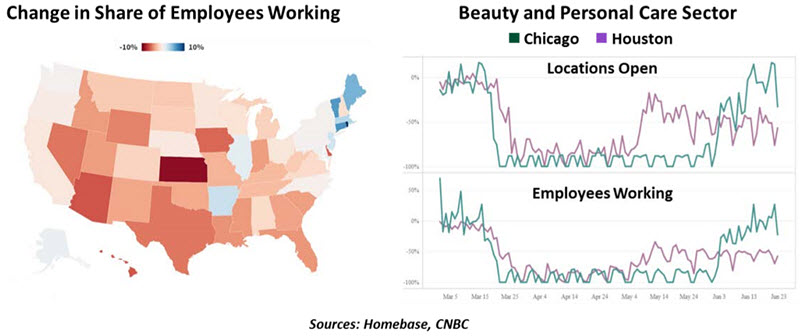

The online staff management platform Homebase is also stepping up with rich data. Over 60,000 small businesses employing a total of more than one million workers use Homebase for scheduling workers and tracking their time. The company’s latest publications reinforce the overall trend that the reopening is slowing. Workers in most states and all sectors are seeing their shifts reduced. A distillation of Homebase’s trend dashboard allows some sector and city comparisons: In the example shown below for the beauty sector, Chicago’s businesses stayed closed for longer than Houston’s did. Today, Houston is retrenching while Chicago grows. At present, this looks like Chicago’s more stringent restrictions were well-considered, but it is far too soon for celebration. In the future, will we look back on this chart as a foreshadowing of a surge in Chicago cases?

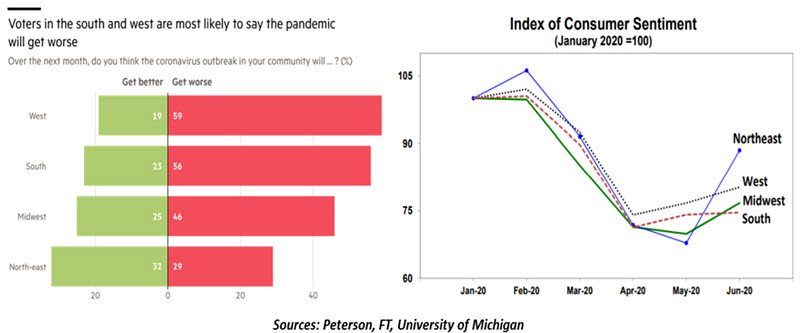

The evolving behavior has been reflected in a noticeable decline in consumer confidence. A recent FT-Peterson poll showed voters in the U.S. southern and western regions were the most pessimistic about the near-term path of the virus, with majorities expecting conditions to worsen in the month ahead. But we are all realists; even in the relatively cautious and optimistic northeast, only 32% of respondents expected the virus to become less threatening. The monthly University of Michigan Survey of Consumer Sentiment showed a similar dispersion: All regions are more pessimistic than they were at the start of the year, the south most of all.

Having survived one lockdown, we have learned that policy responses are less significant than public perceptions of safety. A close study of SafeGraph data by researchers at the University of Chicago found that while overall consumer traffic fell by 60 percentage points as lockdowns took hold, legal restrictions explain only 7% of that loss.

The study also investigated regions with locally varied lockdown policies. For instance, the Quad Cities region straddles Illinois (which had a strict statewide quarantine) and Iowa (which was more permissive). Retail traffic in areas like these fell on both sides of the border, regardless of formal local policies. When people are concerned about infection, they stay home. And conversely, if fear remains in local communities, lifting lockdowns has limited upside.

Every jurisdiction worldwide must vigilantly monitor the spread of COVID-19; not just in its own backyard, but in other yards as well. The natural experiment offered by areas dealing with renewed outbreaks offers an important lesson: ongoing social distancing restrictions are inconvenient, but effective in the long term. If closures have to be reinstated, the cost—to businesses, to workers and to society—will be substantial.

“Even if officials press ahead with reopening, consumers may remain hesitant.”

States witnessing a resurgence of COVID-19 generally had lighter lockdown restrictions and were quicker to lift them. As nations and regions that successfully mitigated the virus contemplate reopening, they must prioritize maintaining hard-won public health gains over a rush to get back to business. With luck and vigilance, we can celebrate victory over the pandemic in a more conventional manner next year: with fireworks, in person.

Squirreled Away

Vaibhav examines the uptick in saving around the world.

There are many ways in which COVID-19 is changing our habits, including mine. Even though my finances are reasonably secure, I have found myself saving more. But the economist in me recognizes that I am part of a growing problem.

Many nations are pumping large amounts of money into their economies through direct cash payments and employment support. The measures are intended to sustain demand, providing a boost to consumer spending that will stop the recession and hasten the recovery.

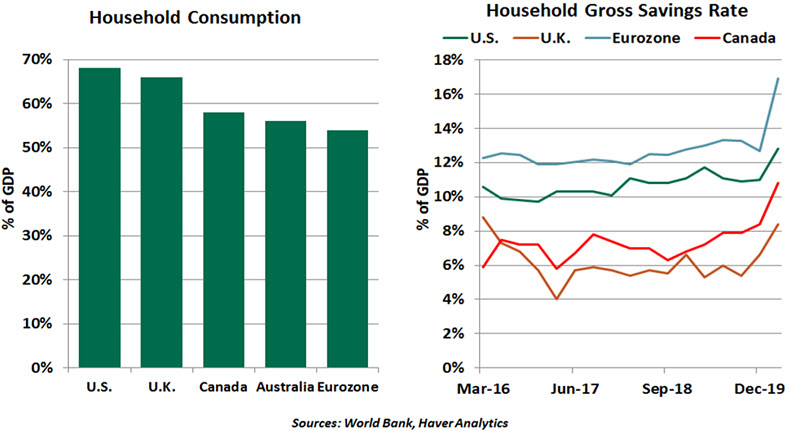

Instead, households have turned cautious: saving rates around the world are soaring, especially in countries where consumption normally accounts for a large share of economic output. Consumer spending accounts for more than two-thirds of the U.S. economy and more than half of the eurozone economy. Some of this renewed saving is involuntary, as consumers are unable to maintain their usual consumption patterns amid lockdowns. But much is also rational and deliberate: When job and income prospects are uncertain, building a safety net is a higher priority.

In the U.S., the gross personal saving rate (personal incomes less personal outlays and taxes) surged from 7.9% at the start of the year to about 33% in April. It remained at an elevated rate of 23.2% in May. Eurozone household saving, defined as the ratio of gross saving to gross disposable income, climbed from 12.7% in the fourth quarter of 2019 to about 17% in the first quarter of this year, the highest since the birth of common currency region in 1999. According to European Central Bank data, household savings have reached an all-time high of €7.3 trillion.

In Canada, the saving rate has surged to its highest level since early 2001. Asian economies like Taiwan are also witnessing a similar phenomenon, with Taiwan’s national saving rate estimated to reach 36% this year, its highest in over three decades.

The increase in saving suggests that stimulus measures have had a low multiplier effect thus far. This is a recipe for a liquidity trap, where a massive surge in the money supply is met with limited uses for it. Household bank deposits from the four largest eurozone economies surged over €100 billion in March and April, three times as much as the average pace of growth over the past decade. U.K. households too, made record deposits in March and April.

Several markets are facing the “paradox of thrift,” a central component of Keynesian economics. The paradox states that in a recession, individuals try to save more, which is sensible. However, if everyone decides to become thrifty at once, economic activity will contract further, leading to a more anemic economic recovery. The more households save, the less likely businesses are to hire more people, which in turn will weigh on tax revenue and government spending. What makes sense individually is bad for the collective.

Precautionary savings aren’t unusual in times of economic uncertainty, but this time it is different. As already seen in the U.S., some of those savings will likely be spent, but with the virus expected to stay with us much longer than initially thought, consumers are likely to remain thrifty for longer. Furlough schemes have kept unemployment rates in check, but those supports won’t remain in

place forever. As a result, households in those markets will continue to save.

“Elevated savings will alter the trajectory of economic recovery.”

The higher savings rate not only poses a threat to economic recovery, but is also a challenge for policymakers as they try to gauge the amount of stimulus that would fuel a return to growth without igniting inflation. Going forward, policies will have to shift from putting money into the hands of consumers to encouraging them to spend. These could be in the form of implementing consumption tax cuts or issuing spending coupons, as China has done.

Higher savings is one reason among many why the curve of economic recovery could look very different from what many observers had hoped just a few months ago. While my wife is pleased with my newfound frugality, her joy may not last for long. It is my sworn duty to support the economy, and I intend to go on a shopping spree. Online, of course.

Play Ball?

Sporting events were among the early casualties of the pandemic: social distancing is impossible in the seats and on the field. Most leagues shut down, at least temporarily. Major summer events like Wimbledon, the Tour de France, and the Olympic Games have all been canceled or postponed.

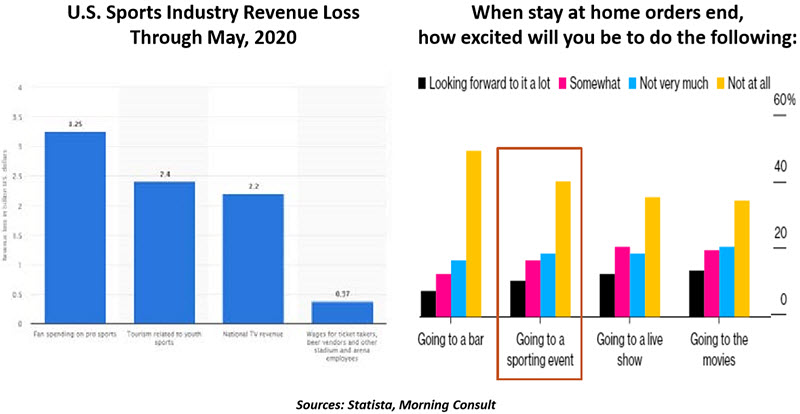

What is entertainment for most of us is big business for others. The global sports industry generates an estimated $800 billion in annual revenue. There may be little sympathy in some corners for losses endured by rich owners and rich players. (The struggle between the English Premier League and its players’ association was particularly bitter.) But global sport creates millions of jobs: 3 million Americans and 1.7 million Europeans work in the industry.

At the highest levels of international sport, television contracts and sponsorship provide the lion’s share of revenue. The longer the pandemic lasts, the more likely that broadcast and sponsorship income will come under pressure. Many clubs around the world have taken on significant amounts of debt to construct new stadiums, which may become difficult to service if the games don’t go on.

“Sports aren’t just entertainment…they’re big business.”

Below the top tiers, clubs are much more reliant on ticket sales and concessions to sustain their operations. As shown in the survey results below, spectators are not overly anxious to return to arenas. Minor leagues are therefore facing much more existential challenges; minor league baseball in the U.S. may never return to its former norm. And American college athletics are looking precarious; the likely loss of substantial football and basketball revenue has already forced schools to suspend dozens of sports programs.

Over the past two months, some leagues have taken steps to restart, without spectators present. Cynics suggest that playing games in the off season for sports like soccer and basketball is a naked attempt to salvage some marketing and media revenue. Yet there is a large community of fans around the world who crave entertainment during these challenging times.

For those who tune in: be forewarned. Without supporters present, the games are simply not the same. And the industry that depends on the games may never be the same.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All