summary

- Europe and the U.S. Consider State Aid

- Is China’s Rebound Sustainable?

- Mortgage Rates Hit Bottom

With movie theaters, concert venues and sports arenas closed, streaming services have enjoyed immense popularity during the pandemic. One offering our family agreed to stream together was “Hamilton,” the hit Broadway show that has been made into a movie.

But while we watched the performance in the same room, members of my household were attracted to different aspects of the production. Some were engaged by the historical narrative; some were inspired by the choreography; and some were mostly into the music.

Not surprisingly, I was most interested in the economics. Hamilton’s gambit to consolidate debts at the federal level was controversial, depicted by some as a bailout of weak states by richer ones. In the present day, both Europe and the United States are confronting difficult questions about the relationship between federal and state finances. The gambits under discussion this summer could bear critically on the prosperity of each union.

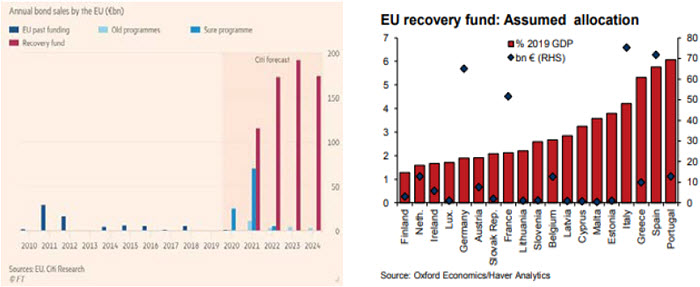

After months of difficult negotiations, leaders of the European Union (EU) emerged this week with a landmark fiscal proposal. A stimulus program of €750 billion, financed by common debt, will be presented to members for approval. The money will augment the automatic stabilizers that have kept Europe’s economy afloat over the past few months.

Europe has a less-than-perfect union. After the U.K.’s departure, the EU now has 27 members, but only 19 of them use the euro as a common currency. For those 19, the European Central Bank (ECB) sets a common monetary policy, but fiscal policy is largely the province of member states. Some countries have been more frugal, while others have been less so. When the pandemic arrived, the former were in much better positions to react; those on the periphery (financially and geographically) have struggled.

EU members have historically been reluctant to issue common financing, fearing it would dull incentives for fiscal discipline among its members. The Netherlands led a group of more frugal nations who wanted strict terms and conditions for those receiving aid under the proposed accord. Dutch taxpayers wondered, reasonably, why their hard work should subsidize citizens in other countries where the benefits paid to those not working are more generous.

“Europe takes a step toward commingling its finances.”

Ultimately, EU leaders realized that if some of its members struggle, everyone will struggle. Angela Merkel, the German Chancellor, came to this conclusion earlier this year; her conversion from skeptic to supporter was critical to the deal. While conditions will be attached to some of the forthcoming aid (a complex governance structure will oversee disbursements), a significant portion will be considered grants. The money should be viewed as an investment in the economic and political future of the continent.

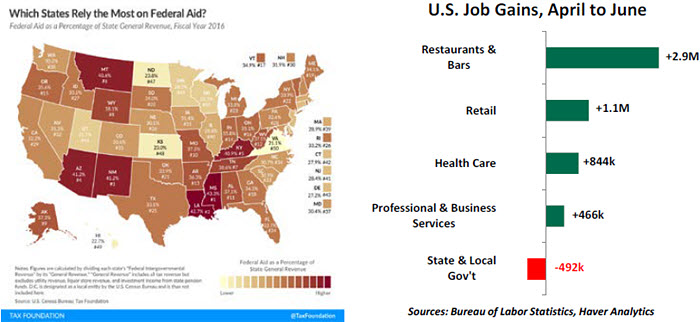

On the other side of the Atlantic, the pandemic has done substantial damage to U.S. state finances, which are heavily dependent on sales taxes. States are on the front lines of providing medical and social services, which are at risk for cutbacks. Further, state and local governments account for one in eight jobs in the United States; substantial layoffs in the public sector could seriously hinder the recovery.

The U.S. federal government appropriated $150 billion of aid to the states earlier this year as part of the CARES Act, but that amount will not be nearly enough to balance local budgets. Earlier this summer, the House of Representatives passed a bill that called for $1 trillion of additional aid to states, but the Senate and the White House have balked at the amount and the design.

As is the case in Europe, some U.S. states have not handled their finances very well, and some federal legislators are therefore reluctant to make them whole. In particular, the massive pension deficits that exist in many states are attributable to very bad management. Those states that have been more responsible are understandably reluctant to subsidize poor policy elsewhere.

This kind of fiscal friction between states is a constant in Europe, but is much less common in the United States. Some U.S. states contribute more to the federal government than they receive in return, and they are taking notice. The pandemic seems to be pitting states against one another, medically and financially.

Negotiations on state aid are coming down to the wire: Congress has not yet agreed on a new round of economic support, and the traditional summer recess begins early next month. States and households are facing a “fiscal cliff”; the sunset of government support would take a bite out of demand, which is critical to the nation’s growth. The overriding principle today is the same as it was 230 years ago: unions cannot be strong if members are not strong.

As in Europe, the fewer strings attached to aid, the better. But Congress might consider requiring the first steps towards state pension reform as a condition for receiving help. If not restructured, public retirement systems will become even more of an economic headwind in the years ahead.

“If some states falter, all states will be impaired.”

The U.S. colonies were in financial disrepair after the revolution of the 1700s; they owed the sum of $80m, immense for the time. Some states were teetering on the edge of insolvency. The nationalization of debts championed by Hamilton put the colonies on a firmer financial footing. From that base, the United States grew more prosperous and powerful.

Hamilton understood that unions will not be durable unless finances are commingled. If I were in the Room Where It Happens today, I would urge policy makers not to miss their shot to support the states.

All That Glitters Is Not Growth

Like “fool’s gold,” some things that seem valuable on the surface can prove to be illusory. Such is the case with China’s “real” gross domestic product (GDP) growth.

As other major economies were still struggling with the pandemic, China was able to begin easing its COVID-19 lockdown. Aggressive steps taken by the Chinese to contain the infection appear to have paid off. So, China’s earlier start towards economic recovery is not perplexing: It is the pace of recovery that has surprised many.

Reported figures from China have shown a rapid, V-shaped rebound. In particular, readings on manufacturing appear to have picked up where they left off in January. But observers were still surprised when full results for the second quarter were tallied: China recorded growth in real GDP of 3.2% year-over-year, a strong rebound from a 6.8% contraction in the first quarter. Annualized real growth for the second quarter exceeded 11%.

A closer look inside the headline numbers reveals that the recovery has been uneven, and driven by factors that may be unsustainable. China seems to have leaned once again on debt- and state-financed investments to prop up the economy. Investments in infrastructure and real estate have driven the recent rebound. Investments by state-owned enterprises rose 2.1% in the first half of the year, while those by private enterprise declined 7.3%.

China’s Banking and Insurance Regulatory Commission has already warned of a surge in bad loans and renewed risks in the shadow banking sector. This is the danger of adding leverage to a system that may already have too much of it.

Household spending in China has improved considerably, underpinned by government stimulus. But it is still down from where it was a year ago. Online retail sales (largely essentials) have boomed, but offline retail sales and discretionary purchases are still well down. Lingering worries about the virus, poor job prospects and weak income growth are weighing on consumer sentiment. Job creation, though improving, remains below last year’s levels. (China’s official unemployment rate, which has been falling, is not an accurate depiction.) As is the case in other countries, saving rates are on the rise as households prepare for an uncertain future.

The resilience of Chinese exports has been the most salient feature of the country’s recovery. China’s share of global exports has risen by over four percentage points since March, to about 18%. Chinese exporters filled the supply gap as other exporting nations grappled with COVID-19. As importers like the U.S. and Europe started to reopen their economies, demand for Chinese exports grew. Exports of pandemic prevention supplies like protective gear, drugs and medical equipment have surged. Exports of household appliances, audio and video equipment and high-tech products have also increased.

“Demand from China’s consumers and its export clients is likely to be subdued.”

The path forward for Chinese exporters will likely be full of hurdles. Recovery in many nations is threatened by a resurgence of the virus. A prolonged recession or slower recovery anywhere in the world will hurt demand for Chinese goods. Countries like the U.S., Europe, Japan and India are increasingly calling for reduced reliance on Chinese imports, and not just for COVID-19-related reasons.

China is at loggerheads with several nations over its initial handling of the virus, recent movements in Hong Kong, territorial disputes, cyber security and trade practices. Multinational corporations are reconsidering their dependence on China, with several either considering or being induced to move at least some of their export-oriented manufacturing out of the country. Chinese businesses with international presences are concerned over the pushback from abroad and are unlikely to make any capital commitments.

China appears to be a bright spot in a gloomy world distressed by the pandemic. But there are several dark clouds on its domestic and international horizons. After smooth sailing through the second quarter, China will face increasing headwinds in the months ahead.

Broken Record

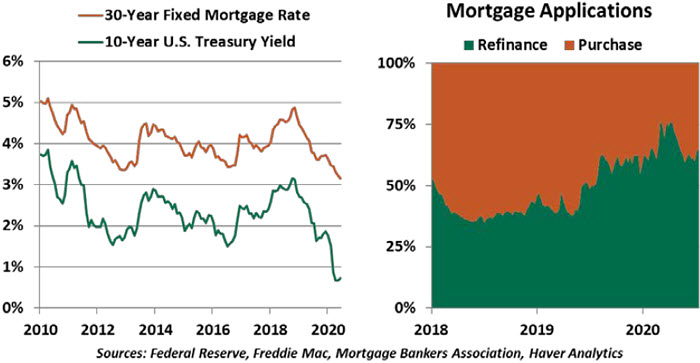

Mortgage rates are reaching record lows. Today, offered rates on U.S. fixed-rate 30-year loans are near 3.0%. But it has been accurate to say we’ve been approaching a record low for decades: the 30-year rate has steadily fallen since it peaked at over 18% in 1981.

At risk of sounding greedy, we are left wondering: Why aren’t rates lower? Mortgage rates typically track the yield on 10-year U.S. Treasuries, which have also been on a long downward trajectory. From 2010 to 2019, mortgage rates averaged a 1.7% premium to 10-year bond yields. But that spread has widened considerably over the last several months, as Treasury yields fell but mortgage rates did not. Borrowers could have had even better opportunities.

Mortgage rates may have found a natural floor. The efforts required to underwrite and administer a mortgage loan are substantial: Originators need a certain spread to cover their costs. Mortgage servicers (companies that collect payments on home loans and forward them to bondholders) are facing a pinch from forbearance: While consumers can request a reprieve from payments, servicers must sustain cash flow to mortgage-backed securities owners while they await relief from mortgage guarantors. This has squeezed some of the leading servicers in the industry.

“If historical conditions held today, 30-year mortgage rates should be well below 3%.”

Protecting margins will be vital to keeping players in the mortgage industry afloat. And for this reason, we think loan rates are unlikely to fall much further.

That said, rates are still incredibly low, serving as a boon to home buyers and sellers. Consumer interest in refinancing grew once again this year as rates fell, and originators are struggling to keep up with applications. As these are processed, household budgets will gain some space to hopefully bolster consumption.

Low mortgage rates have also supported housing prices during the pandemic: growth in the Federal Housing Finance Agency home price index cooled in June but remains up 4.9% year-over-year. Demand for housing has held up thus far, as buyers contemplate a new lifestyle of working from home. After quarantines stalled the market, the volume of both new and existing home sales showed strong growth in June.

The mortgage industry was at the center of the last crisis. It is nice to see it contributing importantly to the recovery from the current one.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust