Our Fixed Income CIO Sonal Desai unveils the first insights from the new Franklin Templeton–Gallup research project on the behavioral response to the COVID-19 pandemic and implications for the recovery: we find a gross misperception of COVID-19 risk, driven by partisanship and misinformation, and a willingness to pay a significant “safety premium” that could affect future inflation.

The first round of our Franklin Templeton–Gallup Economics of Recovery Study has already yielded three powerful and surprising insights:

- Americans still misperceive the risks of death from COVID-19 for different age cohorts—to a shocking extent;

- The misperception is greater for those who identify as Democrats, and for those who rely more on social media for information; partisanship and misinformation, to misquote Thomas Dolby, are blinding us from science; and

- We find a sizable “safety premium” that could become a significant driver of inflation as the recovery gets underway.

Misperceptions of risk

Six months into this pandemic, Americans still dramatically misunderstand the risk of dying from COVID-19:

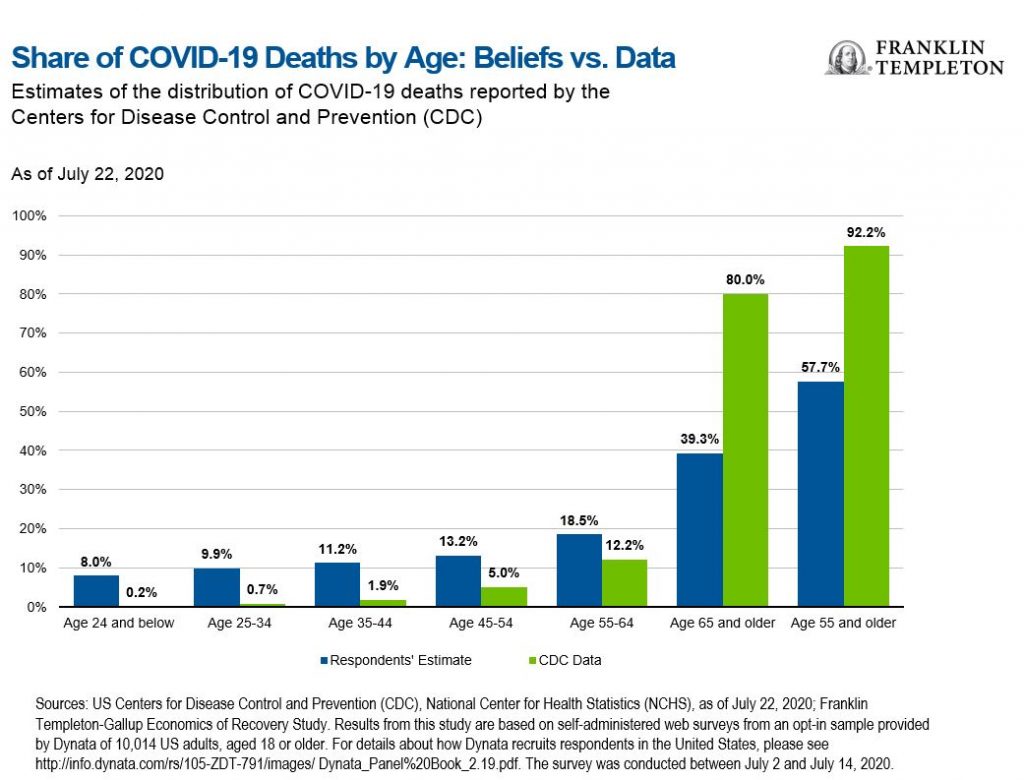

- On average, Americans believe that people aged 55 and older account for just over half of total COVID-19 deaths; the actual figure is 92%.

- Americans believe that people aged 44 and younger account for about 30% of total deaths; the actual figure is 2.7%.

- Americans overestimate the risk of death from COVID-19 for people aged 24 and younger by a factor of 50; and they think the risk for people aged 65 and older is half of what it actually is (40% vs 80%).

These results are nothing short of stunning. Mortality data have shown from the very beginning that the COVID-19 virus age-discriminates, with deaths overwhelmingly concentrated in people who are older and suffer comorbidities. This is perhaps the only uncontroversial piece of evidence we have about this virus. Nearly all US fatalities have been among people older than 55; and yet a large number of Americans are still convinced that the risk to those younger than 55 is almost the same as to those who are older.

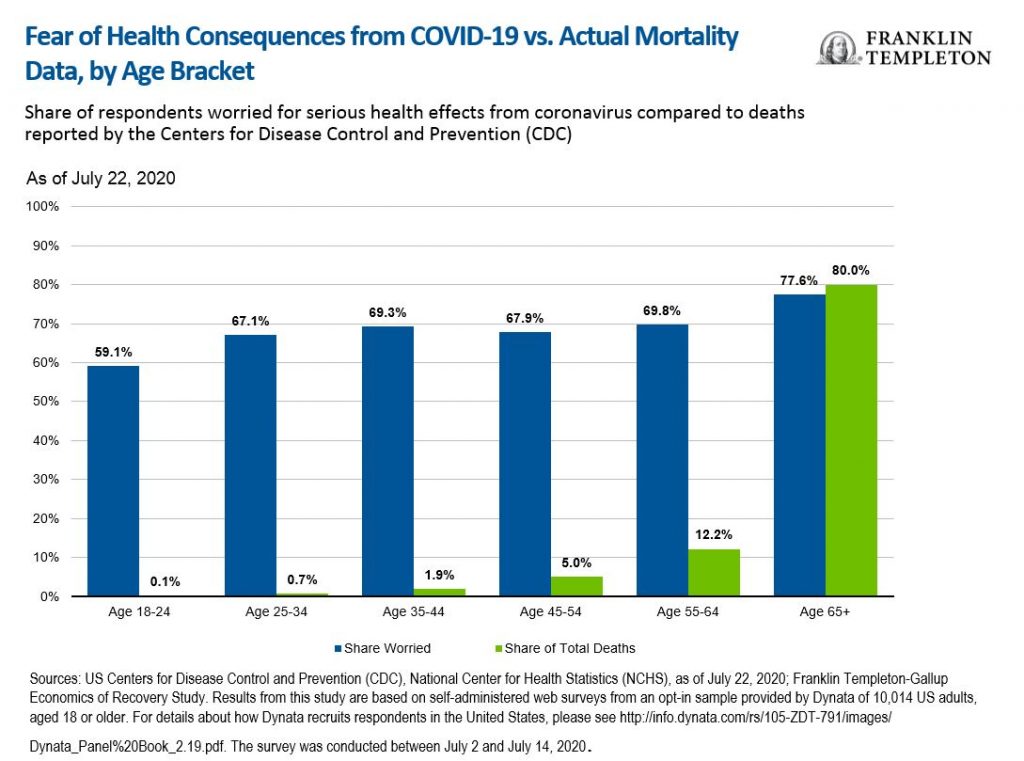

This misperception translates directly into a degree of fear for one’s health that for most people vastly exceeds the actual risk: we find that the share of people who are very worried or somewhat worried of suffering serious health consequences should they contract COVID-19 is almost identical across all age brackets between 25 and 64 years old, and it’s not far below the share for people 65 and older.

The discrepancy with the actual mortality data is staggering: for people aged 18-24, the share of those worried about serious health consequences is 400 times higher than the share of total COVID deaths; for those age 25-34 it is 90 times higher. The chart below truly is worth a thousand words:

Our question asks about fear of serious health consequences, not fear of death, but the evidence to-date indicates that the two follow a very similar age distribution; indeed the CDC has clearly stated on its website that “Among adults, the risk of severe illness from COVID-19 increases with age, with older adults at the highest risk.” Recent concerns of possible adverse long-term consequences are by necessity speculative, since we obviously do not have long-term data yet.

Partisanship and social media

For the last six months, we have all read and talked about nothing but COVID-19; how can there be still such a widespread, fundamental misunderstanding of the basic facts?

Our poll results identify two major culprits: the quality of information and the extreme politicization of the COVID-19 debate:

- People who get their information predominantly from social media have the most erroneous and distorted perception of risk.

- Those who identify as Democrats tend to mistakenly overstate the risk of death from COVID-19 for younger people much more than Republicans.

This, sadly, comes as no surprise. Fear and anger are the most reliable drivers of engagement; scary tales of young victims of the pandemic, intimating that we are all at risk of dying, quickly go viral; so do stories that blame everything on your political adversaries. Both social and traditional media have been churning out both types of narratives in order to generate more clicks and increase their audience.

The fact that the United States is in an election year has exacerbated the problem. Stories that emphasize the dangers of the pandemic to all age cohorts and tie the risk to the Administration’s handling of the crisis likely tend to resonate much more with Democrats than Republicans. This might be a contributing factor to why, in our survey results, Democrats tend to overestimate the risk of dying from COVID-19 for different age cohorts to a greater extent than Republicans do.

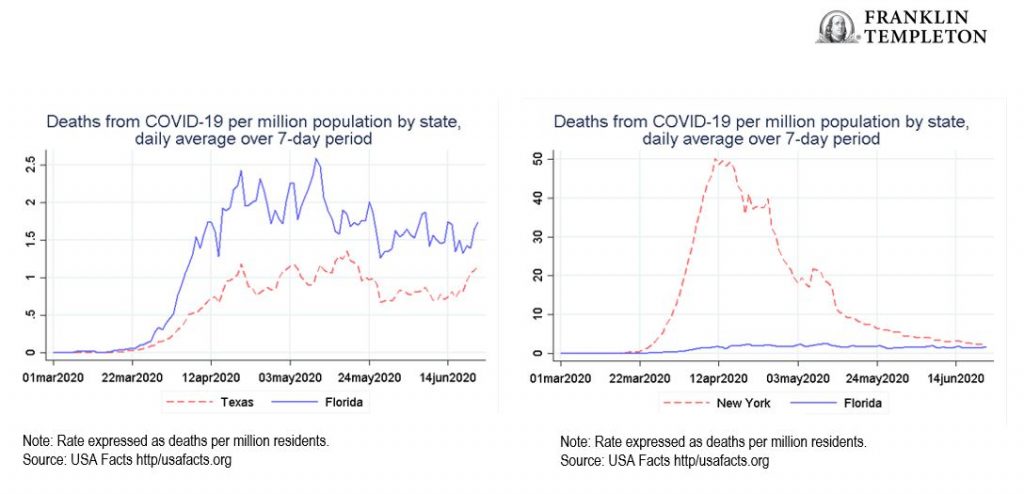

Our susceptibility to how the information is presented also plays a role. The same data can be portrayed in different forms on a graph—some reassuring and some alarming. Our study finds that how the data are presented has a very strong impact on people’s attitudes. For example, respondents who were shown COVID-19 case trends for Texas and Florida in isolation were much less willing to reopen schools and businesses than those who were shown the same trends compared to New York. And more alarming graphics tend to be used more frequently, as they generate greater engagement.

This misinformation has a very concrete adverse impact. Our study results show that those who overstate deaths among young people are more cautious about making purchases, more reluctant to travel, and favor keeping businesses and schools shut.

Here again, we find a significant difference across partisan lines. According to our study, political affiliation is as powerful as age in predicting whether someone would be likely to eat at a restaurant indoors; Democrats have roughly the same willingness to eat in a restaurant at 25% capacity as Republicans do in a restaurant at full capacity. Individual risk from COVID-19 depends on age and health, but perceived risk depends on one’s politics—and it’s perceived risk that drives behavior. Conversely, previous Gallup research has found that Republicans have been less likely to accept public health guidelines like wearing a mask, regardless of the local rate of infection—again evidence that partisanship plays an important role.

This misinformation also causes another fundamental problem. The policy decision of what activities to keep shut and for how long is a very difficult and consequential one. It requires balancing two opposite effects of uncertain scale: on the one hand the benefits in terms of slowing COVID-19 contagion, on the other hand the harm to the economy and to people’s long-term health and livelihoods. This decision is strongly influenced by public perceptions of dangers, not only because politicians are sensitive to the public’s concerns but also because politicians are people too, subject to some of the same biases. Our poll results suggest fundamental misperceptions of the risk of death or serious adverse health consequences from COVID-19 could be distorting these decisions.

The “safety premium” and inflation prospects

Everything has a price. In several industries, resuming activity while limiting contagion risk implies extra costs or reducing the number of customers. The extent to which these costs will be passed on to consumers in higher prices will depend—among other things—on the extent to which people are willing to pay for the extra safety.

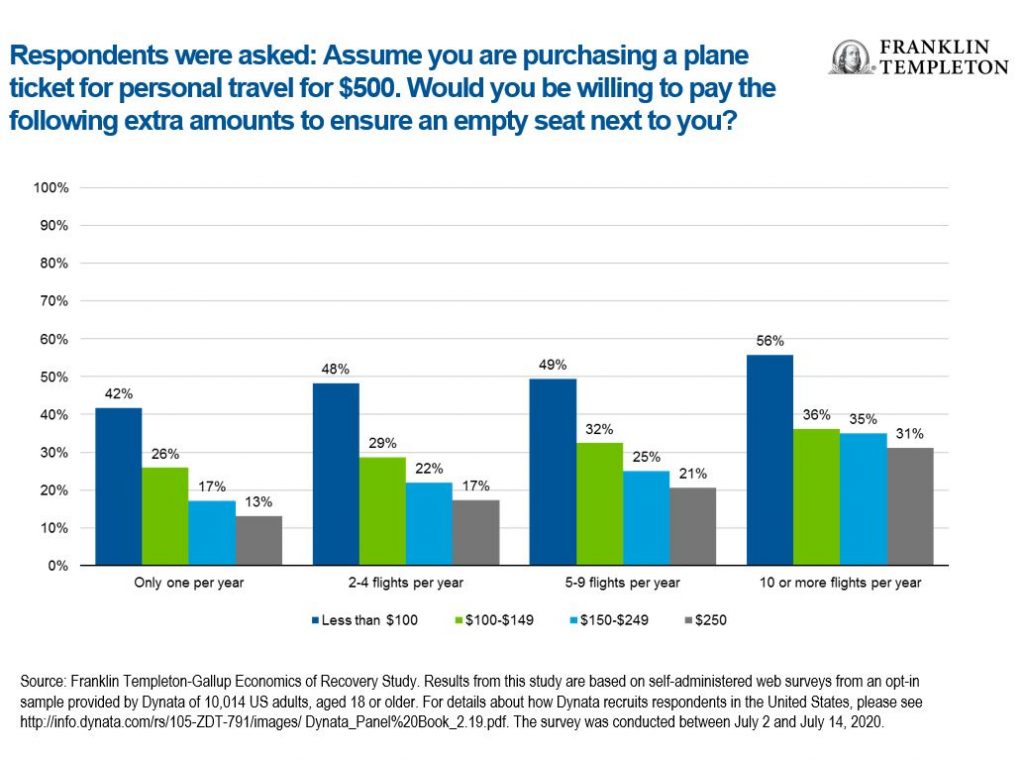

To test this, in our poll we asked people “Assume you are purchasing a plane ticket for personal travel for $500. Would you be willing to pay the following extra amounts to ensure an empty seat next to you?” The results are striking:

- About half of our respondents would be willing to pay up to $100 more, a 20% price increase;

- Between a quarter and a third of respondents would be willing to pay up to an additional $150, a 30% price increase;

- Between one in ten and one in three of our respondents would be willing to pay an additional $250, a full 50% price increase; and

- The more often people fly, the more willing they are to pay extra.

A prolonged recession would depress incomes and demand, but a combination of bankruptcies and safety requirements might cause a corresponding cut in supply. If those who can afford it are willing to pay significantly more for extra perceived safety, we might see a significant rise in inflation down the line. And, higher inflation would further exacerbate the rise in inequality caused by the recession.

Implications

We launched this joint project to gain a deeper insight into people’s behavioral response to the pandemic, because we believe it will play a crucial role in shaping the economic recovery. Our first round of polls has already yielded surprising insights that raise some concern for the outlook, but also highlight important calls to action.

From a public interest perspective, we believe the top priority should be better information and a less partisan, more fact-based public debate. It is shocking that six months into the pandemic so many people still ignore the basic mortality statistics, with perceived risk driven by political leanings rather than individual age and health. Misperceptions of risk distort both individual behavior and policy decisions.

The fact that a large share of the population overestimates the COVID-19 danger to the young will make a targeted public health response more difficult to agree on. We think it is also likely to delay the recovery, causing a deeper and prolonged recession.

Our first results also reveal that people will be willing to pay a significant premium for safety. Combined with a likely hit to supply from the pandemic, this might give an unexpected boost to inflation somewhere down the line. Policymakers should be mindful of this for several reasons, one being that it might exacerbate the rise of inequality from a pandemic that already discriminates against the most vulnerable workers (concentrated in the hardest-hit service sectors) and disadvantaged children (through prolonged school closures). In our view, investors should also start thinking about the impact of inflation reawakening from a decades-long slumber.

Stay tuned for our next round of results and insights.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments