summary

- Costly Legacy of COVID-19: Government Debt

- Lingering Liability

- She-Cession

Latin writer Publilius Syrus once said: “A small debt produces a debtor; a large one, an enemy.” In macroeconomic parlance, investors and financial markets have often proven to be the enemies of heavily indebted nations. Debt at small or moderate levels can lubricate the wheels of economic activity, but in excess, it does more harm than good.

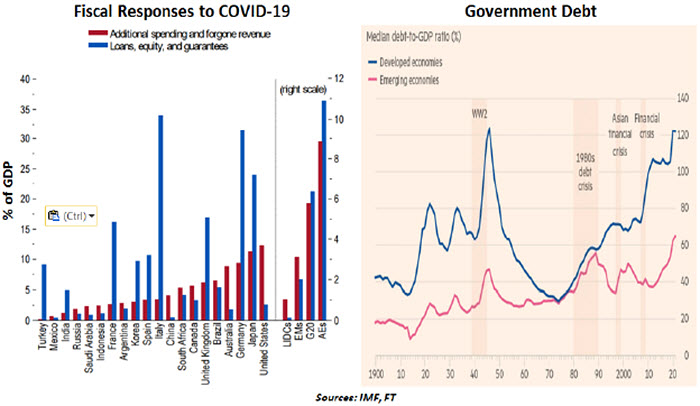

COVID-19 has throttled global economic activity. In response to its repercussions, governments and central banks around the world have announced support measures to prevent household and business insolvencies. Given the nature of the crisis, fiscal policy has played a prominent role. Nearly all countries have deployed fiscal measures since the onset of the pandemic. Two-thirds of them have scaled up their fiscal spending since April to ease the economic jolt. This has revived the debate around looming debt problems.

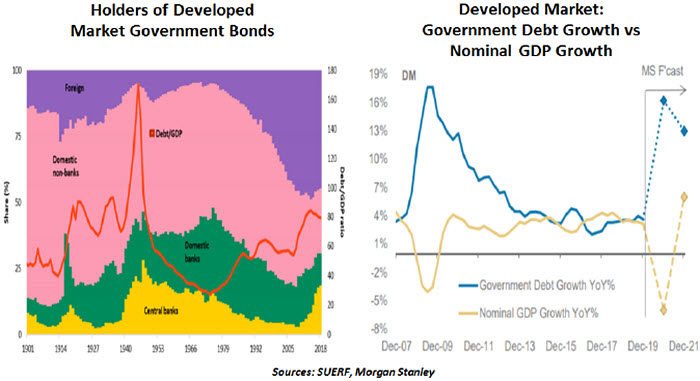

When the pandemic began, the world was already heavily indebted. We typically compare debt across countries by examining the ratio of government debt to gross domestic product (GDP); both parts of that ratio are moving targets. As the COVID-19 crisis took hold, automatic stabilizers cushioned the impact while governments cumulatively committed over $11 trillion in fiscal stimulus, increasing debt. At the same time, GDP contracted sharply. A growing numerator and shrinking denominator are making ratios surge.

The International Monetary Fund expects global average gross government debt to climb to 101.5% of GDP this year, up from 82.8% in 2019. In advanced economies, it is expected to surge to more than 130% of GDP, above even the levels seen during the 2008-2009 financial crisis. In emerging markets (EMs), it is predicted to rise to 63% of GDP.

Advanced economies are accruing large sums of debt, but emerging and low-income economies face bigger struggles in servicing their debt obligations. More than 100 low- and middle-income nations have to pay a combined $130 billion in debt service this year, half of which is owed to private creditors. Many of these countries have fragile economies with weak fiscal buffers and plummeting export revenues. While debt troubles are compounded for some nations by past economic or financial shocks, others are simply struggling because of their addiction to debt and mismanagement of their economies.

External support and strong multilateral cooperation are needed to help financially vulnerable nations combat the crisis. Elevated debt levels will constrain the scope and effectiveness of government support during these unprecedented times, but a full-blown debt crisis will also drive cuts in government spending on social sectors, causing long-term economic disruptions. While the G20’s call for a moratorium on debt servicing for low- and middle-income countries was a welcome move, it is not enough. A few members of the G20 are also among those struggling with high debt. Restructuring of debt, particularly for some African and Latin American countries, appears to be the only way out from the current malaise.

“A debt crisis in even a small economy has the potential to send shockwaves to other parts of the world.”

A debt crisis can lead to losses for financial institutions and, in turn, compromise the stability of financial systems, at home and abroad. Market turmoil and tighter financial conditions are some of the ways other countries can feel the effects of a debt crisis in a debtor nation. In major economies, a debt crisis that results in a sharp domestic economic slowdown can have adverse spillover effects on growth elsewhere.

Debt crises led to Latin America’s La Década Perdida (the lost decade) of the 1980s and Greece’s recent half-decade-long recession. In Japan too, excessive government debt has weighed on the economy, although there are a few other structural factors at play. A crisis in a small market economy can spiral into a significant event around the world, as shown by the 1997 Asian financial crisis. Thailand’s inability to pay its creditors due to surging debt and devaluation of its currency spread to other Asian countries like Indonesia and South Korea. Borrowers of foreign capital in those countries struggled to service their debt as currencies weakened and interest rates surged to contain capital outflows.

Of course, debt is not intrinsically bad for an economy, especially when bonds are issued for productive purposes like scaling up infrastructure. According to a World Bank study of 101 developed and developing economies, a debt-to-GDP ratio of 77% is the threshold at which debt starts to weigh on economic growth over time. Every percentage point of debt above the threshold costs 0.017% of annual real growth. In EMs, the threshold is 64%. This drag may sound small, but it can have a sizeable impact. The 130% debt-to-GDP ratio forecasted for advanced countries would weigh on their GDP growth by 0.9%, impairing an already-fragile recovery.

“Falling into debt traps is easy; climbing out is difficult.”

Problems also emerge when countries enter a debt trap, when a country’s debt grows at a faster pace than its economy. Government intervention in the economy increases along with taxes. Re-borrowing or debt rollover becomes the norm. Populist schemes, generally, expand public expenditure. Once a country grows accustomed to a certain level of government spending, disciplined debt repayment and austere policy become difficult political propositions.

Protracted weak aggregate demand makes debt servicing difficult too. Policymakers, particularly in advanced economies, appear to have learned the lessons from the 2008 financial crisis and are proactively relying on fiscal policy to boost demand and keep deflationary forces at bay. Fiscal stimulus is the most potent tool to fight the immediate economic crisis. Efforts to bring debt under control will be more important when the economy returns to growth. Debt is a potent medicine: safe when consumed wisely, but an overdose can cause unwelcome side effects.

Only the Lawyers Win

Business leaders are juggling many questions as they ponder when and how to reopen. What do local laws allow? Are suppliers ready to sell raw materials? Are employees ready to return, and will they be safe at work? Are customers back in the market? And a scary thought hangs over each of those questions: Will I get sued?

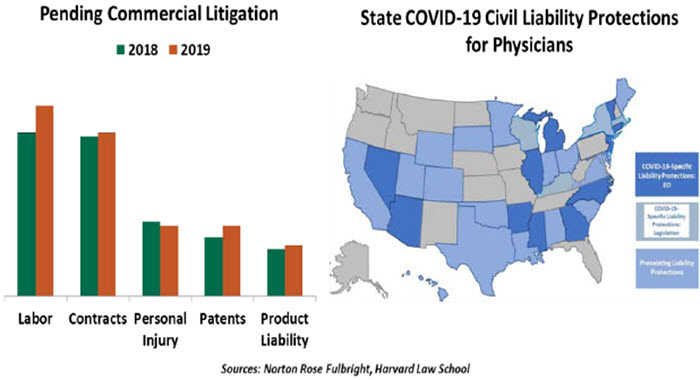

Litigation serves an expensive but necessary role in business. Lawsuits follow when contracts are broken, when people are mistreated or when injuries happen. The cost of fighting and settling lawsuits motivates businesses to create and enforce rules that promote safety.

But the novel coronavirus is also a novel legal challenge. When a person contracts COVID-19, is anyone at fault? The idea sounds implausible if the virus spreads in a passing encounter. The allegation gains more merit, however, if an employee falls sick after working in close quarters with infected coworkers.

Litigation is already taking shape. Examples are accruing of now-deceased workers who were unknowingly sent to work in viral hotspots, were not provided personal protective equipment (PPE), and were discouraged from wearing masks. In many cases, their families are filing lawsuits against the employers. While managers can cite the evolving health guidance and general uncertainty in the early days of the outbreak, these will be difficult arguments to defend before a jury.

Debating liability has contributed to the stalemate of the next round of U.S. fiscal stimulus. Businesses want legal protection in case COVID-19 cases are traced back to their premises. Insurers who backstop litigation would find their capital stretched by these unexpected claims.

The question of liability becomes even more difficult in other congregate settings. Schools at all levels are struggling to find the right balance of safety, instructional content and social interaction as they plan for the school year ahead. Could an elementary school teacher who tests positive sue a school district? If a dormitory has a COVID-19 breakout, is the university at fault? Beyond education, what about infections transmitted in a doctor’s waiting room or government office? These questions have no ready answers. If every death resulted in a lawsuit, legal systems would be overwhelmed. Pre-emptively restricting lawsuits would make some decisions easier.

“Fear of lawsuits can lead to well-considered business practices.”

Lawsuits are not the only costs of COVID-19. Breakouts cause downtime as facilities close for cleaning, forfeit productivity as employees fall sick, and can lead to negative media coverage that scares away customers.

In law, as in much of life, the best offense is a good defense. Employers should actively monitor employees for symptoms, distribute PPE, require distancing and clean regularly. Offering generous amounts of paid sick time would encourage employees to stay home if they might be contagious. Each of these measures is an added cost, but all are minor compared to the cost of hosting a super-spreader event.

As the reopening began, a National Federation of Independent Business survey found 70% of business owners were concerned about liability protections. However, these fears do not appear to have stopped their decision to reopen. The risk of liability will take shape later, if deaths occur and lawsuits follow. For now, many have decided that getting back to business has been worth the risk.

Congress has proposed a liability shield, but this would not give employers carte blanche to reopen without precautions. Employers would still need to abide by government guidelines, and employees endangered by gross negligence could still seek recourse. Though negligence is difficult to prove in court, fear of lawsuits may prompt more cautious and beneficial decisions.

Ultimately, stopping the spread of COVID-19 is everyone’s responsibility. Masks, hygiene and distance are the best remedies available thus far. Lawsuits won’t bring about a cure or bring back a worker who was lost to the disease. But as an incentive to stay vigilant against the virus, it’s not all bad for liability to remain on managers’ minds.

Women and Children First

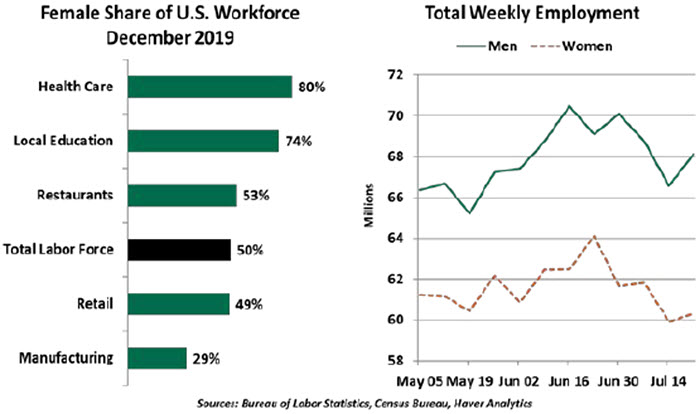

The consequences of economic downturns are felt by particular demographics. Technology workers faced mass layoffs in the dot-com recession. The housing crash sidelined builders and real estate agents. In the COVID-19 recession, an unfortunate trend is emerging: The slowdown is disproportionately affecting women.

A rise in female unemployment is evident in both the monthly Employment Situation and the Census Bureau’s new weekly Household Pulse Survey. As lockdowns took effect, several sectors that employ more women slowed more than others. Education systems were shocked as students moved to online learning; teachers kept working from home, but many school support staff were left without work. The healthcare industry also slowed as elective and non-emergency medical appointments were deferred, causing doctors, nurses and social workers to lose shifts.

“Women are still the primary caregivers in most households.”

Meanwhile, at home, childcare needs only grew. Parents of younger children lost access to daycare, while school-aged children were left at home, struggling to find their way through a new online curriculum. Daily life in households required more planning, more meals and more interaction with children. Much of this added work fell upon women.

Despite a trend toward equality in the labor force, household work may not be split evenly. In many two-parent families, mothers continue to shoulder the brunt of this labor. The effort was aptly summarized in the title of a U.S. Census Bureau working paper: “Why Is Mommy So Stressed?” The research found that women in states with early lockdown measures were 20% more likely to stop working than those that had more warning of what was to come. As quarantines were enacted, women were bifurcated into those who stopped working to tend to their families and those who worked more to compensate for lost household income. Both paths induce greater stress.

Mother’s Day in May 2020 was atypical, with celebrations limited by lockdowns. As we keep working through the pandemic, let’s not forget to recognize the women who are sacrificing so much to make it all possible.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust