Yellow Flag Jobs Data

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLoss Exposure

Stiff Drink Time

Crowding Out

The Absurd, Totally Misleading Unemployment Report

Puerto Rico, Montana, Missing Maine, and Changing Life Habits

As I file this letter Friday morning, people are reacting to the July jobs report. My own reaction: The headline report is absurd. I will explain further at the end of this letter. But first, I have another topic.

Regular readers know I worry about debt, mainly that the world has too much of it. But it’s a little more nuanced. Whether debt is excessive depends largely on what it buys.

Debt is problematic when it underwrites unnecessary consumption. Going on vacation, for instance, is generally a bad idea if it saddles you with years of credit card payments. But debt helps when used to finance productive assets. This kind of debt should, if all goes well, generate enough new wealth to pay for itself and more.

In fact, the economy needs the second kind of debt to grow. Access to credit helps entrepreneurs start businesses that create jobs and offer innovative products. The challenge is to keep it under control. Lenders and borrowers both get overextended in good times and then overcompensate. The resulting cycle is one reason we have recessions.

And that’s where we are now: in a deep recession, and facing a depression. We’ve already seen the savings rate climb to historic highs (with help from government stimulus). Now the second part is here as economically-critical credit begins drying up, sometimes even for stable, well-capitalized borrowers.

We don’t want banks getting into trouble that would require public bailouts. But lower access to capital is a growing problem that will extend our economic agony, above and beyond the coronavirus and everything else.

Loss Exposure

Loan delinquencies and defaults rise when the economy weakens. That’s obvious—so obvious that, in theory, it shouldn’t happen. Everyone knows good times don’t last forever. The rational course is to borrow only if you are confident in your ability to repay when normal events (like recessions) happen.

That applies to lenders, too, and maybe even more so. They are in the business of taking credit risk. That’s why they can charge more than the risk-free interest rate. Their loan books should be prudently diversified and every borrower subject to strict credit analysis. Interest rates should be high enough to keep the lender stable even when normal events (like recessions) occur.

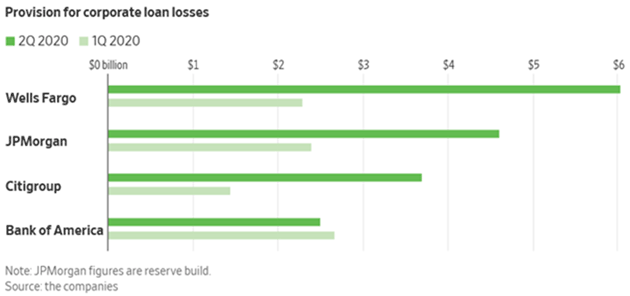

Last month’s bank earnings reports revealed the big lenders are sharply raising their loan-loss reserves. It is also happening in smaller banks.

Source: The Wall Street Journal

These numbers still seem low to me, so I expect them to grow. Nevertheless, they are already trickling through the economy at a noticeable pace.

Anecdote: I have a business associate (who asked not to be named) who has excellent credit. He monitors his FICO score and it’s always north of 800. He has several high-limit credit cards he rarely uses. In the last month, seemingly out of nowhere, three card issuers cut his limit to a paltry few thousand dollars. That’s no loss to my friend, who wasn’t going to use the cards anyway. But what made the banks do this? It makes perfect sense from their perspective.

What the customer sees as “available credit” the bank sees as “loss exposure.” At any moment, my friend could have spent to his limit and then stopped making payments, maybe even going bankrupt and leaving the bank in a bad spot. The bank normally accepts that possibility because it sees potential revenue, too. But now the risk outweighs the benefit so better to eliminate the possibility.

Actually, it makes sense. My friend is a lousy “customer.” Even though his credit is over-the-top, he is not making the bank any money. Without knowing, I can guarantee you the cards in question have low or no fees. Yet the bank has to reserve cash in case he decides to use them. Their actual reserves are being challenged, so he is an easy target.

I, on the other hand, don’t have his pristine credit. But I only have a few credit cards, which I used to charge everything possible, and then pay them off every month. It feeds my secret fetish: airline miles. So far, bank algorithms see me as a good customer who generates fees, and have not cut my credit line.

But he illustrates a point. If even highly rated, stable borrowers are seeing their limits cut, imagine what is happening to marginal borrowers.

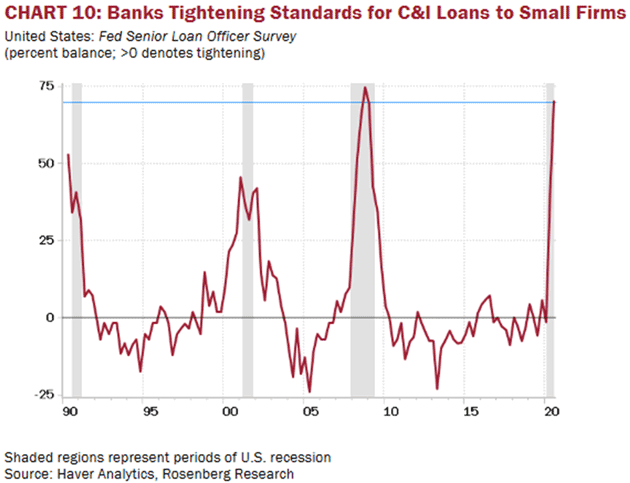

We don’t have to imagine. We have actual data from the Federal Reserve’s quarterly Senior Loan Officer Opinion Survey. US banks, and particularly the US branches of foreign banks, are tightening credit in most categories. It’s worse for small firms. In fact, banks are tightening business loan standards at the fastest pace since 2008.

Source: Rosenberg Research

The Fed survey also found lower demand for all kinds of lending except residential real estate. I don’t know of any other business where it makes sense to raise the price of your product as demand for it drops. That banks are doing so speaks to how nervous they must be. Worse, it’s happening despite massive Federal Reserve efforts to encourage and subsidize bank lending.

Stiff Drink Time

Whether it’s a bond or a bank loan, recovery potential is part of credit analysis. Defaults usually aren’t a 100% loss. What can we expect to get back if the borrower can’t repay? If you have collateral worth, say, 70% of the loan value, then you are taking less risk as the lender and can loan more freely.

Even better is to have the federal government standing behind a portion of the loan. That’s how Small Business Administration loans work. The SBA typically guarantees 50% to 85% of a loan amount, which lets banks offer more flexible terms than many small business owners could get on their own.

Keep in mind, many small businesses are struggling now but not all. Some have new opportunities in this environment. With capital, they could expand and maybe create jobs for the millions who need them. But they need the capital first.

Last week I read and reposted a Twitter thread (you should follow me, by the way) by someone describing himself as a consultant who helps franchisees get loans, often via SBA guarantees. I asked him to contact me and was able to verify his identity, though I can’t reveal it here. He described a terribly frustrating credit environment in his space. Below is a portion of his thread. (You can read the full version here.)

The banks I work with are SBA, conventional lenders who service smaller loans under 2mm and generally smaller operators of these franchise systems, and then larger banks who provide loans to larger operators from 2-50mm. I’m short—20+ banks across ALL spectrum of SME lending.

I fund 400-500mm in loans per year through these banks. In February we were on pace to fund well over 500mm and potentially 750mm — growing exponentially year over year. STIFF DRINK TIME. Since April 1st we have funded 5mm total through only 2 banks. Let’s dive in as to why.

SBA banks—they have lending limits to 5mm. Congress has authorized them to go to 10mm in the CARES Act but they have ignored it. This will become important later. They currently have guarantees from the govt at 80%—pretty good right? DOESNT MATTER THEY STILL WON’T LEND.

In fact, they are pushing the government to guarantee 90% of the loans (and likely on their way to 100%—see my prior posts on the de facto nationalization of the banking system). In short SBA has SHUT OFF BORROWERS waiting for more from Uncle Sam.

Current excuses ARE PLAYING BOTH SIDES (and this applies to all banking segments). A chain with increased sales since pandemic—no loan. “We want to wait to see if sales increases are sustainable.” Doesn’t matter that sales are up. They may not be “sustainable.”

On the other side for businesses with sales down—“well we just aren’t comfortable sales will rebound and we have concerns over COVID.” So, sales up = no loan. Sales down or flat = no loan. Operator size IRRELEVANT. Are some banks lending? Yes. This is 75–80% of SBA banks.

They are also being EXTREMELY selective on industries they will do. If you are an industry with “large public gatherings” you better pray to Santa Claus for money.

So, businesses with solid revenue still can’t get capital even when the government will guarantee 80% of the risk. Economic recovery will be very hard if this persists. All those loans not being made represent business activity that won’t happen, buildings not constructed, jobs not created.

It doesn’t mean the situation is hopeless. But it probably means we will be stumbling through this morass even longer.

Crowding Out

While others reach for credit, one borrower is having no trouble at all. People are clamoring to lend even more money to the US Treasury, which is why yields are so low. Adjusted for inflation, they are paying to lend money to the government. Enormous amounts of it, too.

In the April-June quarter, Treasury borrowed $2.753 trillion in marketable debt. This week officials estimated they will issue another $947 billion in Q3 and $1.2 trillion in Q4. Q1 was $477 billion. So, for this calendar year, Treasury will have borrowed almost $5.4 trillion. Or maybe I should say “at least” since there is a very good chance these estimates will prove low.

Everyone (including me) expects Congress to pass another “stimulus” package. My best guess is it will be between $1.5 to $2 trillion. The bulk of that will be spent in 2020. That means US federal debt will be $29 trillion and perhaps $30 trillion as we ring in the new year, or shortly thereafter. Not to mention $3 trillion in state and local debt.

It gets worse. From my friend Mark Grant (quoting Bloomberg):

Money managers just can’t get enough corporate bonds as the Federal Reserve supports the securities, and that demand is igniting the markets for issuing and trading company debt.

When Activision Blizzard, Inc. sold $1.25 billion of notes on Wednesday, the video game maker got orders for almost 10 times as many bonds. When Alphabet Inc., Google’s parent, sold $10 billion of debt securities on Monday, it garnered nearly four times as many orders. Last year that ratio averaged closer to three times. Junk bond issuance this week is at its fastest clip since mid-June.

Just last week, many dealers thought that companies were going to cut back on selling high-grade bonds, after most corporations had raised the money they needed to tide them over for the rest of the year. They expected as little as $50 billion of issuance in August, after volumes in July were down about a third from the year before.

Now the forecasts for August are increasing to as much as $75 billion, on the theory that companies might borrow more to lock in ultra-cheap borrowing costs. Yields in the $6.8 trillion high-grade bond market averaged just 1.83% on Wednesday, according to Bloomberg Barclays index data.

The Federal Reserve has basically said we are going to backstop high-grade corporate debt while doing little for small business. At least that is how lenders perceive the Fed’s action.

That’s the problem. Small businesses are the US economy’s engine and we’re starving them for fuel. People like me who worry about government debt often talk of a “crowding out” effect in which high governmental credit demand sucks limited capital away from smaller private-sector loans. Is that what’s happening now? Maybe. In theory, lenders seek the best risk-adjusted returns. They will risk loaning to unstable borrowers if they can set rates high enough. The high-yield bond market is one such segment.

So what counts is not so much the level of rates, but the spread between what a lender can make in Treasury paper vs. lending to businesses and individuals. It must be enough to match lenders who are willing to take more risk with borrowers who can pay higher rates. But other things count, too. Loan covenants, collateral, assorted other arcane details.

When Treasury yields are below zero in real terms, it shouldn’t be hard for a lender to sharply increase their income by making loans to reasonably stable borrowers at 5%, or to riskier ones at 10%. Yet it appears they aren’t eager to do that. Why?

I suspect it is because this is no ordinary recession. Its outcome doesn’t depend on normal economic forces or cycles we have seen unfold before. The economic weakness comes from a virus we can’t presently control whose presence stifles economic activity. The recession can’t end until something changes. There are three possibilities.

- A working vaccine, deployed on a large scale worldwide,

- Effective treatments that sharply reduce hospitalization and fatality rates, or

- A large part of the population having been infected and survived with immunity.

When will any of those happen? We all hope it’s soon but we can’t know. This uncertainty renders normal credit analysis impossible. The restaurant industry will take years to recover. Ditto for travel and hospitality. If you’re a loan officer, lending to a restaurant or hotel right now is a pure gamble. Banks aren’t (and shouldn’t be) gamblers.

But this means the businesses which are the actual engine of growth for the economy can’t get credit. Scarce credit means scarce capital investment, and therefore little growth, if any.

Remember when we complained about GDP growing “only” 1% a year? Or, as some called it, secular stagnation? We may long for those days. They were better than we knew at the time.

The Absurd, Totally Misleading Unemployment Report

I cannot end this letter without commenting on the sheer insanity that passes for the

headline unemployment report this morning. Here’s the lead.

In July, the unemployment rate declined by 0.9 percentage point to 10.2 percent, and the number of unemployed persons fell by 1.4 million to 16.3 million.

This number will be breathlessly reported in all the media but let’s look at reality on the ground.

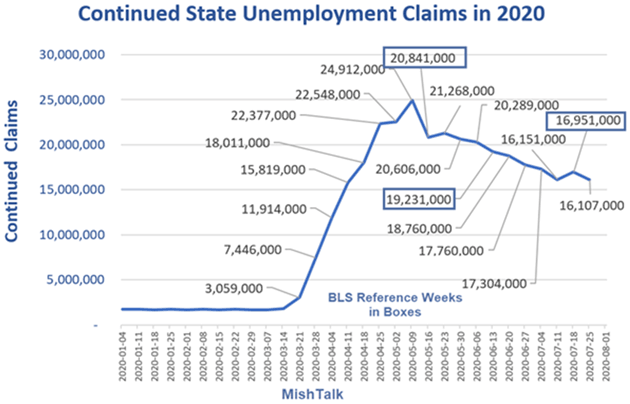

First, Mike Shedlock offers this chart from yesterday’s continued unemployment claims.

Source: MishTalk

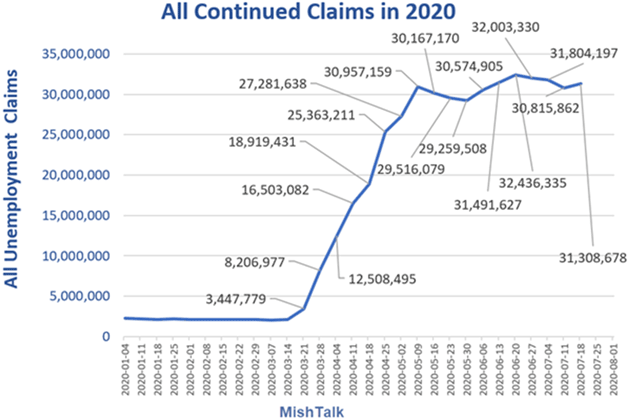

It certainly shows improvement over last week but this doesn’t reflect those on federal unemployment programs (again, I assume they will continue in some way). If you add those in, you get 31.3 million workers receiving some kind of unemployment benefit.

Source: MishTalk

That is roughly double the number of unemployed that BLS reports. The US workforce is about 160 million people so 16 million unemployed gives you the 10% unemployment number. If 31.3 million are unemployed (assuming those receiving benefits are actually unemployed, a reasonable assumption) then the unemployment rate is 19.6%.

Then add an unquantifiable number of those who don’t qualify for unemployment insurance of any kind, as in those who worked “off the books” for cash or otherwise fell through the cracks. It’s a significant number. This brings you to an unemployment rate easily 20% or more.

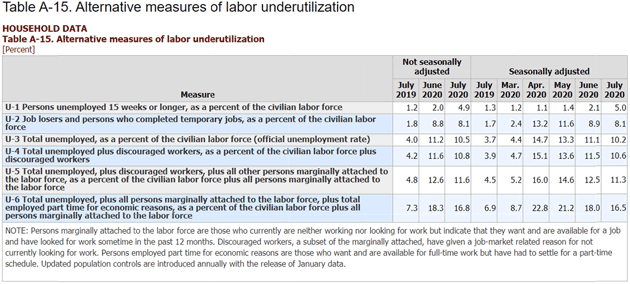

The BLS isn’t hiding this unemployment. They have systems developed over decades to track unemployment, and the current crisis/recession doesn’t fit neatly into that system. They do, however, track several items called “Alternative Measures of Labor Underutilization.” One of those numbers is the U-6 category, which shows 16.5% unemployment.

Source: Bureau of Labor Statistics (Click to enlarge)

Let me leave you with a final and somewhat depressing thought. Private investment fell roughly equal to federal spending last quarter. As much as it pains me to say, even acknowledging some of the stimulus money was wasted, without it the US and therefore the world would be in a deep depression.

The numbers above show we are nowhere close to “recovery.” Whatever stimulus package comes out of DC will be smaller and hopefully better targeted. But it will be absolutely necessary to keep the economy from truly collapsing.

(Just writing that forces a deep and audible sigh from me. Never once in my life did I think I would write those words. And that they would be true.)

To talk about a V-shaped or any other shaped recovery based on past history is sheer absurdity. The future recovery, and there will be one, will be unlike anything we have ever experienced, including even our (great?) grandparents (and for some of us our parents) in the Great Depression. This is a completely different economic animal.

Perhaps by understanding it, we can figure out how to get out of it for everyone’s sake, as well as determine our own individual paths forward. It will be the Stumble-Through Economy indeed.

Puerto Rico, Montana, Missing Maine, and Changing Life Habits

Week after next I will meet Shane in Missoula, Montana. I will be flying from Puerto Rico and Shane will be coming from Oregon after attending a spiritual retreat. I will be “batching” it this next week. We will then spend five delightful days with old friend Darrell Cain and some of his family at his home on Flathead Lake. The closest thing I will have to a vacation, as opposed to my permanent staycation, this year.

For the last 14 years, the first Friday of August found me at Leen’s Lodge in Grand Lake Stream, Maine. I find that I am truly emotionally missing it. Sadly, it was a major economic stimulus for that area and is now just another financial dent in what are truly small, mostly family businesses.

I have noted before how I miss my gym. It is once again closed, and in the two weeks it was open I noticed a significant drop off in attendance. It became quite easy to social distance. Then I read this note this morning from Neil Howe:

As gym owners reopen their doors, their worst fears are coming true: People aren’t coming back. Recent polls show that Americans are in no hurry to return to fitness centers. Morning Consult tracks weekly comfort levels for different activities during the pandemic. On the week of July 13, only 20% of Americans felt comfortable going to the gym. One week later, that share dropped to 18%. A different poll from TD Ameritrade found that 59% of Americans don’t plan to renew their gym memberships even once the pandemic is over.

This will play out in multiple service industries. On the flip side, I can’t get simple weights and other home workout equipment anywhere. All sold out here. Amazon won’t deliver. The barbell business must be booming. Big equipment workout iron? Not so much. I expect a lot of used gym equipment will go on the market in a few months as one gym after another goes bankrupt. Ditto restaurant kitchen equipment, hotels, planes, etc.

I hate being a Gloomy Gus, because I actually see fabulous opportunities all around me. When the world gets repriced, opportunities appear even as some doors close. Our job is to find the open doors. And with that, you have a great week!

Your home alone for the week analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All