Some emerging markets have been coping with the COVID-19 crisis better than others, and their economies are in different stages of recovery. Our emerging markets equity team highlights a few—and offers thoughts on why the pandemic has accelerated some existing fundamental and technological trends.

Three Things We’re Thinking About Today

- A collapse in economic activity amid the COVID-19 pandemic and expectations of slowing loan growth, falling margins and rising bad debts have hurt near-term earnings forecasts for Brazilian financials. While the pandemic has weighed on their businesses in the short term, we see a low probability of a systemic banking crisis in Brazil. The pandemic could, in fact, have the unintended effect of boosting bank penetration in Brazil. The government’s disbursement of emergency handouts through banks has compelled scores of previously “unbanked” individuals to open accounts. This group of new customers could drive a fresh wave of demand for financial services in the future. When the outbreak eventually passes, we expect quality banks to resume secular growth. Credit penetration in Brazil is far below many other markets, signaling room to head higher in the coming years. Brazil’s central bank has also cut its policy interest rate to a record low, which reduces the cost of renegotiating or restructuring loans, and could be a catalyst for longer-term credit growth. Our longer-term conviction remains bullish for select Brazilian banks where we see strong fundamentals, improving competitive positions and potential to benefit from structural growth drivers.

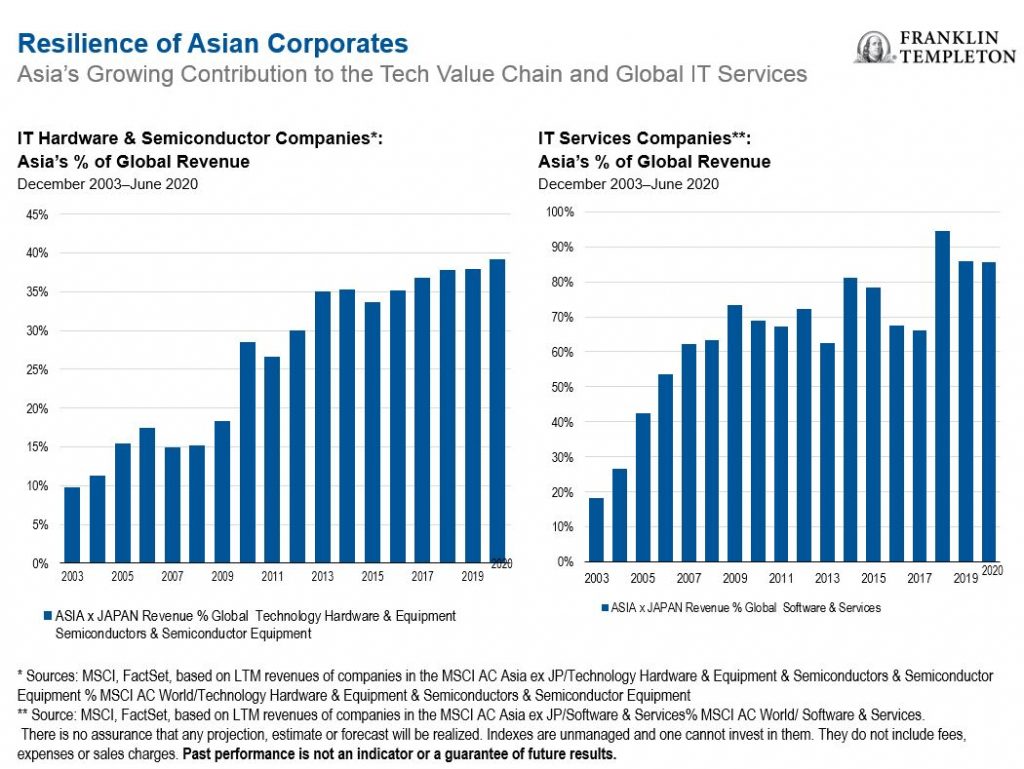

- A rally in technology stocks and effective control of COVID-19 in the country drove Taiwan’s equity benchmark to an all-time high in July. Known for its research and development strength, Taiwan’s semiconductor industry is a global leader, with the island home to one of the world’s largest independent integrated chip manufacturers. The industry has been benefiting from increased demand from cloud applications related to remote working and online education, trends which the pandemic has accelerated. We believe the global outlook for memory chips will remain strong, driven by demand for memory solutions from smartphones, high-performance computing, 5G (fifth-generation wireless technology), artificial intelligence, internet of things, data centers and cloud infrastructure. The announcement by a major American competitor of a delay in the production of its next-generation chips and the possibility of outsourcing further bodes well for Taiwan’s semiconductor industry. Taiwan’s manufacturers are also at the forefront of the global push to move supply chains out of China, as rising tensions between the United States and China fuel demand for servers and chips not made on the mainland. The coronavirus pandemic is only expected to accelerate the shift to Taiwan, as more companies domestically and globally begin to re-evaluate China-dependent supply chains.

-

South Korea embodies much of emerging markets’ new realities; namely institutional resilience, improved economic diversification and the emergence of world-leading emerging market (EM) companies. In addition to standing out as illustrative of the aforementioned factors, South Korea is also an example in terms of its handling of the COVID-19 pandemic. As a major oil importer, South Korea has disproportionately benefited from lower oil prices, while also seeing little economic impact from the collapse in international travel due to its lower dependency on tourism. An export powerhouse, a number of South Korean exporters are of global importance, supplying hardware that enables the modern economy to function. World-leading semiconductor and battery makers are benefiting from the secular trends of increased computing power and greener mobility—some of which are accelerating due to the pandemic. South Korea’s advantages in innovation and intellectual property are also evident in the health care sector—ranging from virus test kits to biologics—which have undoubtedly been supportive during this crisis. The country’s internet sector has also been thriving amid social distancing.

Outlook

While some countries are struggling with a second or even third wave of COVID-19 transmissions, others are seeing containment and the gradual reopening of economies. Consensus suggests that a potential vaccine is at least 12 to 18 months away and, in the interim, countries will need to start operating effectively again, whether from a health, social or governance perspective. The long-term and far-reaching economic consequences of lockdowns will also become clearer and need to be managed.

In addition to the health crisis, we have also seen increasing geopolitical risk, with the long-standing friction between China and the United States returning to the forefront. The nature of US-China relations has changed at both the political and economic levels. The US administration’s view of China as a rival superpower has brought about a different policy stance: the current administration is taking a sharper approach than before, which is likely to persist. The US presidential election ahead in November also has had a huge effect on the country’s rhetoric, which will likely remain heated as the election approaches. But once it has passed, and as a US economic recovery becomes clearer, we believe the tone should improve.

Geopolitical risks are par for the course for emerging market investors. While we continually factor these considerations into our investment decisions, of far greater importance are company fundamentals and earnings sustainability, as well as the irrefutable combination of demographics and long-term growth potential.

Emerging Markets Key Trends and Developments

EM equities climbed in July and outpaced their developed market counterparts. Progress in coronavirus vaccine trials, more policy stimulus, China’s economic recovery and a weaker US dollar boosted investors’ risk appetite despite a resurgence of COVID-19 outbreaks and worsening US-China relations. The MSCI Emerging Markets Index increased 9.0% during the month, while the MSCI World Index returned 4.8%, both in US dollars.1

The Most Important Moves in Emerging Markets in July 2020

Asian equities rallied in July, with Taiwan, India and China posting some of the strongest returns. Taiwan’s technology-heavy market rose on strong momentum in semiconductor stocks. India benefitted from an improving outlook for several large-capitalization companies, even as the country confronted rising COVID-19 cases. China’s economy returned to growth in the second quarter. A risk-on mood drove stocks higher at the start of the month, before government efforts to cool market exuberance and a US-China diplomatic row triggered some profit-taking. Bucking the regional uptrend, stocks in Thailand and the Philippines fell. Thai officials projected a deep contraction for the economy this year, while the resignation of key Cabinet members stoked political uncertainty. The Philippines recorded a spike in COVID-19 infections. A drop in remittances to the country also added to concerns for the economy.

Latin American markets were among the top global performers in July, as the lifting of social distancing measures and an uptrend in global equities continued to drive investor confidence. Stronger domestic currencies further supported gains in US dollar terms. Argentina, Brazil and Chile were at the forefront with double-digit gains, while Peru, Mexico and Colombia lagged their regional peers. Although Brazil reported mixed macroeconomic data during the month, efforts on the reform front continued, with the government sending a tax reform proposal to Congress for approval. In Chile, the government announced a series of measures to stimulate the economy, support the middle class and inject liquidity into small and medium enterprises. Strength in the Mexican peso was responsible for the modest returns in that market, which was down in peso terms. Mexico’s gross domestic product (GDP) declined 17.3% quarter-on-quarter in the second quarter, its steepest contraction on record, as the pandemic continued to weigh on the economy. Peru’s central bank maintained its benchmark interest rate at a historic low of 0.25% for the third consecutive month in July.

Markets in the Europe, Middle East and Africa region lagged their EM counterparts during the month with Turkey, Egypt and the United Arab Emirates recording declines. South Africa, Poland and Hungary, however, outperformed their regional peers. The South African Reserve Bank cut its key interest rate by 0.25% to a record low of 3.5% in July and signaled nearing the end of the easing cycle. The central bank also revised its 2020 GDP growth projection to -7.3% from -7.0%. Gains in Russia were held back by depreciation in the ruble, despite a 0.25% surprise interest rate cut. The central bank also announced additional regulatory changes to support mortgage and corporate lending. Sentiment in Central and Eastern European markets benefited from a European Union agreement on its COVID-19 recovery fund and the 2021-2027 budget.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

1. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments