summary

- Room At The Inn

- Where Will Next Month’s Rent Come From?

- Analyzing Argentina’s Debt Settlement

Long ago, in a world far, far away, I was a frequent traveler. (Actually, it was only five months ago, but it seems like a different age.) Northern Trust has clients all over the world, and visiting with them has been my great pleasure. The quality of the conversations has always been more than ample compensation for the flight delays, missed meals and time away from family.

Among the variables associated with life on the road is lodging. In fact, the quality of hotels I have stayed in over the years has been highly variable. There have been occasional treats: getting upgraded to the presidential suite, swimming in a nice hotel pool and enjoying an amazing view. But there have been plenty of tricks, too: the eight-foot-by-eight-foot interior room with no closet, failed hot water heaters and mattresses well past their “best by” dates.

Whatever their quality, hotels are suffering amid the pandemic. Public health issues initiated their troubles, and economic issues have perpetuated them. The hospitality industry provides an instructive case study of commerce during, and after, COVID-19.

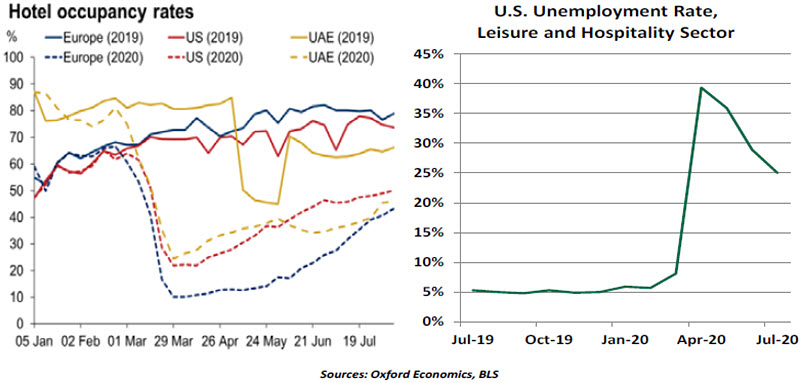

Until a vaccine is perfected, the only reliable way to prevent the spread of the coronavirus is to limit movement and increase spacing. Travel, therefore, has been deeply depressed. While there has been some modest recovery over the past few months, hotel occupancy around the world remains substantially below pre-pandemic levels.

This has presented a particular hardship for those who work in the hospitality industry. There are more than 700,000 hotels worldwide, which together employ 173 million people. Prior to the pandemic, more than 17 million Americans were employed in the leisure and hospitality sector. Many of these employees were at the lower end of the wage and education spectrum, which has made it difficult for them to cope with layoffs.

Even when allowed by public policy, reopening a hotel is difficult. Enhanced cleaning must be done throughout the property; temperature screening for guests is required; and hotel restaurants, often big moneymakers, may remain closed. High-rise properties have the added complication of managing crowding in elevators.

“The hotel industry is dealing with a panoply of pandemic problems.”

Consumer surveys routinely reveal that comfort with staying at a hotel will take a long time to fully recover. The risk of aerial transmission in crowded places and contact transmission from surfaces touched by carriers creates substantial trepidation. Hotels built around particular attractions like stadiums, theme parks, and casinos are struggling because attendance at those venues is either not allowed or severely limited.

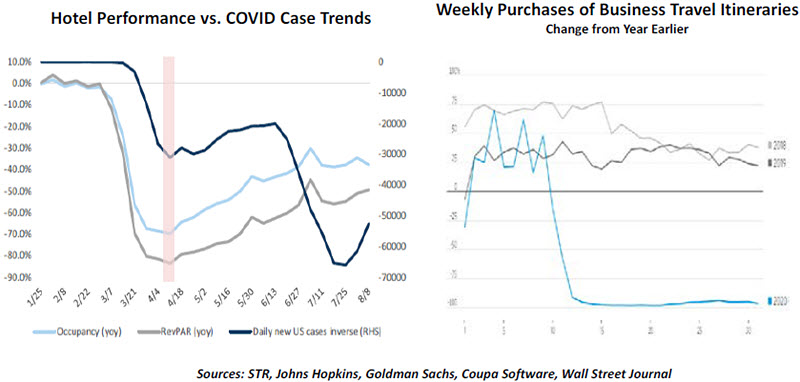

One of the hotel industry’s key metrics is revenue per available room, or RevPAR. It captures the influence of both occupancy and the rates charged. On this score, the industry’s performance is the worst in history. Analysts at Bank of America do not expect RevPAR to return to 2019 levels for five years.

This spells trouble for hotel owners and their creditors. Loans to finance lodging properties are often packaged into securities and sold to investors; the prices of these securities have struggled. Delinquencies on hotel mortgages that are traded in the financial markets have risen to 18% of outstanding loans.

The number of hotel bookings, like many economic variables, has started to recover from the depths seen earlier this year. Families weary of working and learning from home have started to venture out, although they are traveling more locally. (They also tend to stay at more modest properties.) It is also fair to say that there is growing pent-up demand for getting away, which could add energy to the industry as public health conditions settle.

Corporate travel, however, remains limited. Restrictions aimed at safety and saving are very much in force; almost all conventions and conferences are being held remotely. As communication platforms like Zoom, Webex and Microsoft Teams improve and become more widely used, some interactions that used to be in-person are moving to virtual channels. This development will likely be sustained even after a COVID-19 vaccine has been implemented.

The misery experienced by the lodging sector has some company. Cities rely on room taxes to help finance their activities. In aggregate, the American Hotel and Lodging Association estimates COVID-19 will cost local governments $17 billion in revenue this year. Given the poor state of public finances in the United States, this is money that will be missed.

“Leisure travel is working its way back, but business travel may never be the same.”

The struggles of the hospitality sector illustrate the influence of the four curves that will determine the pace and shape of the economic recovery. The path of the virus will influence the path that public health officials will take in relaxing restrictions. On the basis of these first two paths, businesses will determine when and how to reopen, and consumers will determine how willing they are to get out and about again.

COVID-19 is not going away quietly. In fact, the approach of colder weather in the Northern Hemisphere may give it renewed pathways. Persistent caution will therefore be required until a broad vaccination program is completed; medical professionals don’t expect that to be achieved until late next year.

And that means it may be a long time before I have the chance to stay in a hotel again. I certainly don’t miss the crackerbox rooms, stale muffins and overnight construction noise I’ve encountered at some properties. But when I can get back out onto the road, it will represent a step toward normalcy for me and for the economy. I can’t wait for my next check-in time.

Flat Out

An eviction is an ugly affair. Residents are removed from the dwelling and their belongings are piled onto the street. The newly homeless family has to find shelter in short order. It is a scene that should be avoided at all costs.

In the United States, fear of a wave of evictions is rising. Even though labor markets have been improving, there remain more than 30 million Americans who are collecting jobless benefits. Many of them were put out of work by the pandemic, which continues to limit the scale at which firms are operating. For some, what began as a short-term furlough has turned into longer separation.

Prior to COVID-19, the Federal Reserve’s survey of economic well-being revealed that 16% of families were unable to stay current with their bills, and another 12% would fall behind if confronted with an unexpected expense of $400. The survey was taken at a time when unemployment was at a 50-year low. Those in the bottom 50% of the U.S. income distribution have very little financial cushion. With supplemental unemployment insurance benefits lapsing on July 31, the position of many households has become much more precarious.

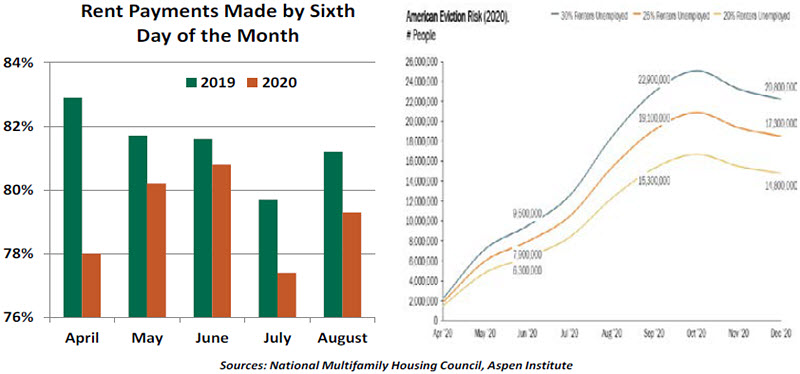

About 37% of Americans are renters, the highest level in 30 years. That percentage is even larger in most major cities, where population density has allowed COVID-19 to spread more readily and where economic disruption has therefore been more severe. In recent years, there have been about a million evictions annually; the Aspen Institute projects that between 15 and 20 million renters will be at high risk by the end of 2020.

The CARES Act, passed in March, placed a four-month moratorium on evictions from properties financed with federally-backed mortgages. This protected roughly 28% of tenants, but that provision expired on July 25. Residents who are behind on their rent are now in a 30-day notice period before evictions can commence. A patchwork of state and local bans provide additional protections, but many of these have also expired.

Practical constraints may limit the scale of an eviction crisis. Eviction requires a court order, and backlogged courts keeping limited hours will slow many eviction proceedings. Landlords may also hesitate to incur the expense of eviction, given the limited pipeline of more qualified tenants amid an economic crisis. Working out a repayment plan may be in many landlords’ best interest.

“Keeping families in their homes will be critical to sustaining the recovery.”

Extending eviction protections was the goal of one of the executive orders issued by the president earlier this month. However, the order did not extend the moratorium. It merely instructed the Department of Health and Human Services to “consider” whether an extension would be beneficial to prevent the spread of COVID-19. The memorandum further instructed the Department of the Treasury to identify funds that could be used for housing payment support, with no deadline. Any policy changes may come too late to help evicted renters.

The majority of tenants continue to pay their rent on time, according to the National Multifamily Housing Council. But relative to last year, there has been an increase in the fraction paying late. Signs of stress are emerging as more landlords report tenants paying rent with credit cards, often at additional cost, suggesting that cash is limited.

Residents won’t be the only ones harmed if evictions escalate. Many rental properties are leveraged, and the loans supporting them are held by banks or investors. Sustaining some level of cash flow is certainly preferable to losing it all. The makings of compromise are there, if all parties are willing to embrace it.

COVID-19 has thrown the economy for a loop. We shouldn’t compound the consequences by throwing people out of their homes.

Worth It

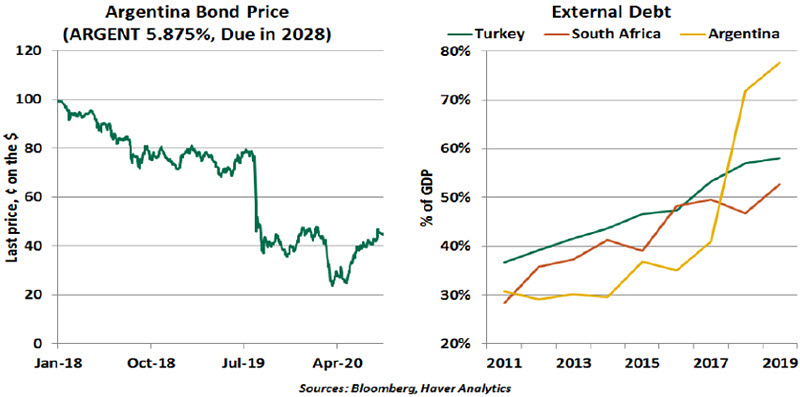

After months of deadlock, the Argentine government clinched a deal with three creditor groups to restructure $65 billion of debt and emerge from its ninth sovereign default in the last century. An open-ended default was not an attractive option. Creditors would have resorted to litigation that could have resulted in another lengthy and contentious battle that could have locked the government out of global credit markets for a long time.

Under terms of the agreement, Argentina’s creditors will exchange their old bonds for new ones, taking a 45% discount in the process. This implies a significant loss for investors, but is still better than the initial proposal offered by the Argentina government.

Argentine officials believe the deal will restore debt sustainability, but some in the markets are already betting on next default.

Nations like Argentina, Ecuador, Mexico and Colombia have a long history of defaults. Yet investors continue to pile into their securities. Full debt repudiations have been rare, but restructurings have not: in these latter situations, investors have conceded haircuts averaging 44%. But higher risk does equal higher returns. A National Bureau of Economic Research study shows that investors in emerging market debt have received average returns that are three times higher than bonds issued by the U.S., U.K. and Canada.

“Debt restructuring is the least-worse outcome.”

Though the deal marks an important step to stabilize Argentina’s economy, it will be in vain if Argentina fails to reduce imbalances. The World Economic Forum ranks the country 139th out of 141 countries for economic stability. Argentina is in talks with the International Monetary Fund (IMF) to update the $57 billion lending arrangement established two years ago.

Argentina isn’t the only country struggling to fulfill its external obligations. Economic damage from the pandemic has led more than 100 countries to approach the IMF for emergency financing. Turkey and South Africa, both with high external debt, are of particular concern. The South African rand and Turkish lira have depreciated notably (by over 20%) this year, raising the potential for runaway inflation and default on foreign debt payments.

While sovereign defaults are not common, COVID-19 is threatening to make them more frequent. An expensive but responsible resolution of Argentina’s debt restructuring should set a positive precedent for the global financial system. At the end of the day, having an option to retrieve pennies on the dollar is better than ending up with nothing.

© 2020 Northern Trust Corporation

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust