Investment Grade Credit Update: An Exceptionally Eventful Year That Has Created Opportunities

The investment grade fixed income market has been unusually active in 2020. Initial concerns about Covid-19 triggered a sharp selloff, but sentiment abruptly reversed when the Fed announced plans to purchase corporate bonds. Spreads have nearly returned to their pre-pandemic levels, but not all sectors have recovered equally, creating interesting opportunities for savvy investors.

“There are decades where nothing happens; and there are weeks where decades happen” - Vladimir Lenin

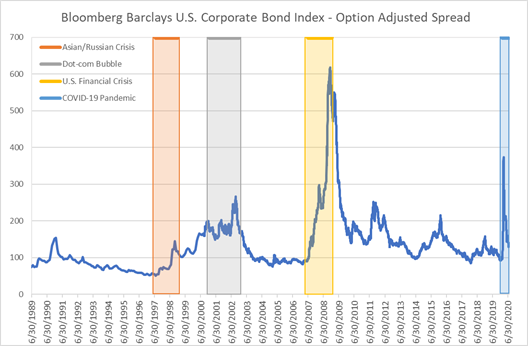

2020 has been a wild year in the investment grade (IG) fixed income markets. At the height of the Covid-19 crisis, IG corporate bonds were upended by dual fears of widespread insolvencies and inadequate market liquidity, which caused spreads to triple from their pre-pandemic levels. But thanks to a rapid and monumental response from the Federal government – in the form of both monetary and fiscal stimulus – the market recovered unexpectedly quickly. As of July 31st, the option adjusted spread (OAS) of the Bloomberg Barclays U.S. Corporate Index was just 31 basis points wider than it was on January 31, 2020, before the pandemic began.

The speed of the current recovery is highly unusual. As you can see from the chart below, each of the other major downturns during the past three decades unfolded much more slowly.

Source: Bloomberg

Although it’s atypical, we think the pace of the recovery makes sense. Obviously, support from the Federal Reserve (the Fed) has been critical, but in our view there is another important reason the market has been treating the pandemic as a temporary setback rather than a long-term situation. Specifically, it was triggered by a sudden public health crisis rather than a structural imbalance resulting from years of excesses and bad financial practices – both of which were hallmarks of the previous crises. Thus, improved safety precautions and the development of an effective vaccine – which may be available as soon as early next year – could end the current slowdown in short order, which was never an option with the others. On the contrary, it took years to repair the damage caused by each of them.

Fed Support Turned the Tide

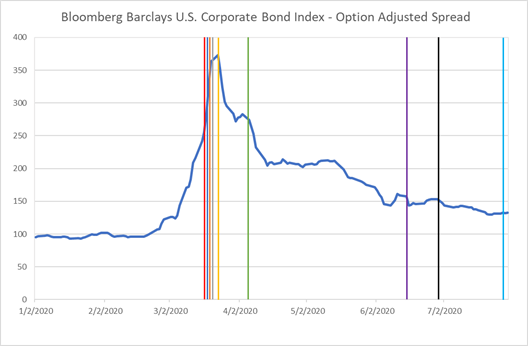

There is little doubt that the recovery began in earnest when the Fed stepped in to backstop the markets. The first big announcement came on March 15, when they cut the fed funds rate to 0-0.25% and began a $500 billion Treasury and $200 billion mortgage backed security quantitative easing (QE) program. This was significant, but sentiment didn’t change materially until March 23rd, when they unveiled the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF). These two facilities were effectively an open-ended commitment by the Fed to purchase IG corporate bonds, asset backed securities, and commercial paper. This unprecedented level of support reversed the trajectory of the corporate market almost immediately, as you can see from the chart below (which shows the timeline of Fed announcements and the corresponding changes in corporate bond spreads).

Source: Bloomberg

The Fed effectively liquified the bond market by stepping in as the buyer of last resort, which set the stage for companies to borrow at substantially lower costs. This was the beginning of the rally in corporate bonds, and the effective end of the dramatic spread widening resulting from the pandemic.

2020 Issuance Breaks Records

Investment grade companies, not surprisingly, were delighted by the Fed’s response. Prior to the Fed intervention, corporations were limited to drawing on bank lines for emergency funding, which they were doing aggressively. This spike in borrowing activity motivated the Fed to step in, as they wanted to protect the banks.

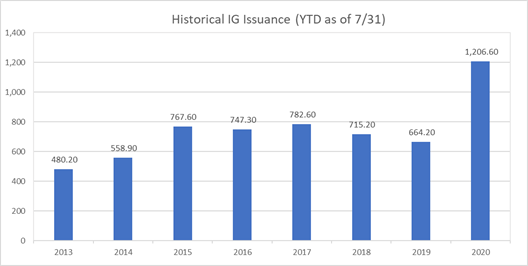

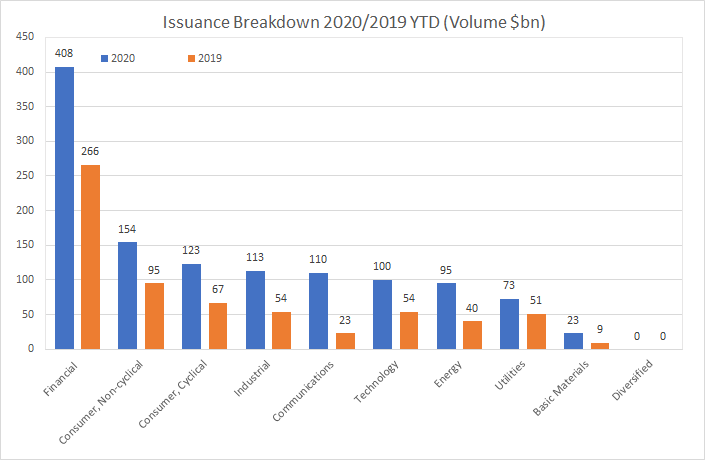

Once they announced their QE plans, access to the term markets reopened for investment grade borrowers, who took advantage by issuing record quantities of debt. According to JP Morgan, through the end of July, gross issuance in the Investment Grade credit market reached $1.2 trillion, which was 85% higher than the YTD volume of 2019. In fact, 2020 YTD volume on July 31 was already higher than full year 2019 volume of $1.05 trillion. Net issuance (gross issuance less maturities) increased even more on a relative basis. The IG market had maturities of $450 billion YTD, resulting in a net supply of $789 billion, which is up 195% year over year.

Source: Citibank

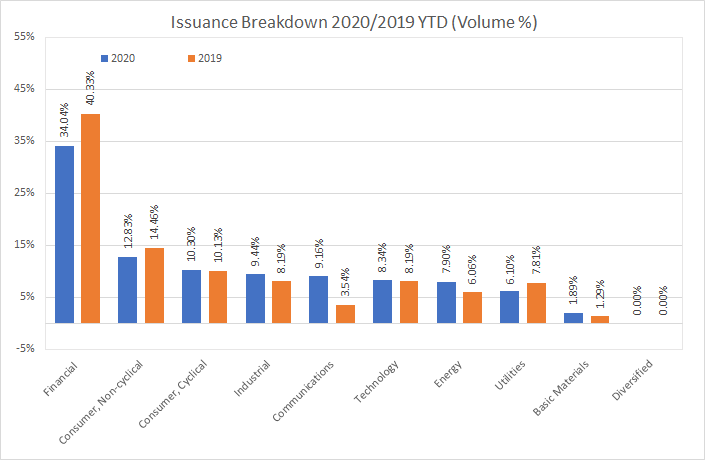

In addition to the stunning uptick in volume, the composition of the issuance also changed substantially. Specifically, corporations issued further out the curve in 2020 compared to 2019, as they sought to lock in historically low rates for a longer period of time.

Demand has kept pace with the surge in issuance, as fixed income investors have been looking for alternatives to the minuscule yields on U.S. Treasuries. Investment grade corporates currently offer materially higher returns, and although they are not risk-free, they are generally considered among the safer asset classes.

Interestingly, investors have expressed a preference for longer dated bonds, presumably because they feel yields are not likely to increase anytime soon. This is further supported by the fact that demand for products that take advantage of rising rates (e.g., floating rate notes and shorter maturity bonds) has been substantially lower than in 2019.

Although 2020 issuance is up across the board, some sectors have been more active than others. The largest percentage increase in issuance came from communications companies, which needed funding for large capital expenditures, mergers and acquisitions, and substantial refinancing needs. Financial institutions, on the other hand, accounted for the largest increase by dollar amount, but they decreased as a percentage of the overall market as they are heavily regulated, which limited their flexibility.

Source: Citibank

Lastly, YTD issuance has continued the trend of lowering of credit quality in the investment grade market, with 46.6% of 2020 issuance being BBB rated vs. 39.4% in 2019. In addition, according to JP Morgan, as a result of 2020’s record issuance, IG leverage will increase materially this year from 2.9x to 3.7x. We are watching this increase in leverage closely, but we do take some solace in the fact that the early use of proceeds was largely to warehouse liquidity (many companies still have the cash on their balance sheets). Moreover, dividends plus share buybacks as a share of EBITDA fell to six-year lows, which suggests that management teams have generally been bondholder-friendly so far during the pandemic.

Fallen Angels on the Rise

Another consequence of the pandemic has been a significant increase in fallen angels – investment grade companies that lose their BBB rating and become high yield borrowers. As we have discussed in the past, the growth of the BBB sector has been a focus of the market, and investors have been monitoring their de-leveraging measures in hopes of seeing a favorable trend. Unfortunately, the pandemic has made it very difficult for borrowers of any category to reduce debt loads, and according to CreditSights, through July 2020, ~$200 billion of investment grade debt was downgraded versus ~$19 billion for all of 2019. Not surprisingly, two of the largest three names to fall out of the IG index were energy companies.

Prior to the pandemic, the rating agencies had been giving BBB rated companies a substantial amount of leeway regarding their leverage ratios, which led to a historically low frequency of downgrades (despite deteriorating fundamentals). Unfortunately, the depth of the economic slowdown forced the hands of the rating agencies, leading to the sharpest spike in the volume of downgrades since the period following the financial crisis.

Looking forward, we feel that sectors that have been most adversely impacted by the pandemic (such as airlines, lodging, gaming, restaurants, etc.) will be vulnerable to further downgrades. However, we still believe that the downgrade cycle will be limited and will not reach the levels of the period following the 2008 Financial Crisis.

It is also important to note that as companies fall out of the investment grade index, it helps the supply/demand technical as there are fewer eligible credits for investment grade buyers to choose from. This dynamic coupled with reduced new issue supply should be a positive support for credit spreads for the balance of the year.

Spreads Near Pre-pandemic Levels, but Recovery Not Uniform

Although the weighted average spread of the BC Agg has nearly returned to its pre-pandemic levels, a closer look at the index shows that not all segments have recovered equally. The dispersion in performance makes sense, as the virus has impacted each sub-sector a bit differently, but our analysis revealed that some of the most notable performance anomalies had little to do with the economics of the pandemic and were instead a function of index construction.

Sector Analysis: Some Surprises, but Mostly by the Book

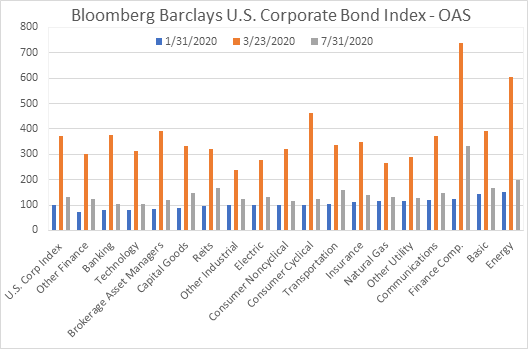

The chart below shows a breakdown of how each sub-sector of the index performed during the crisis and how it has recovered since the Fed announced its stimulus programs. Each sub-sector has three bars – the first represents the spread as of 1/31 – before the crisis began; the next is the spread as of 3/23 – the peak of the crisis; and the third is the spread as of 7/31. The data is sorted in ascending order of the pre-pandemic spread level. You can see that there was comparatively very little dispersion of spread levels in January versus the peak of the crisis and the recovery. Note that the spread of the index is the first set of bars in the chart.

Source: Bloomberg

In our view, the most surprising sector is Consumer Cyclicals, which actually outperformed the broader index – as of 7/31 it was only 24 bps wide of pre-crisis levels (vs. 31 bps for the index). This performance is highly unexpected because many of its subcomponents have been hit quite hard due to massive declines in consumer spending in areas such as travel and leisure. In our view, one of the biggest reasons this sector has outperformed is that it benefitted from the fallen angels mentioned above. In particular, two very large issuers – Ford Motor Company and Royal Caribbean Cruises – were both downgraded and removed from the index, eliminating two sizable sources of underperformance. Moreover, the sector includes big box retailers like Target and Walmart, both of which benefitted from the pandemic (unlike most smaller retailers, who suffered significant damage during the crisis) and helped the sector recover quickly.

The best performing sector during the period, Other Industrials, was also a little unexpected. Industrials were hit hard during the pandemic as factories were shut to protect workers, yet spreads in this category were only 25 bps wide of January as of 7/31. A deeper analysis revealed that despite its name, the vast majority of the category has nothing to do with industry or manufacturing. In fact, 77% of the sector is comprised of bonds issued by educational institutions such as Harvard, Yale, Stanford, and Georgetown – schools with sufficiently large endowments to ride out any short-term market disruption.

On the other hand, the group that was impacted most by the pandemic and has been the slowest to recover is the Finance Companies sector, which aligned with our expectations. This group includes firms that lease aircraft to airlines as well as the troubled company General Electric, which made up 28.1% of the sector going into the pandemic. This sector’s OAS widened 617 bps from January 31 to March 23, and is still 209 bps above its level from January. This makes sense given that the sector is exposed to credit risk from airlines, one of the industries that has struggled the most since the virus outbreak began.

The other leaders and laggards during the period generally fell in line with what we would have predicted based on how they were impacted by the pandemic.

BBBs Are A Growing Concern

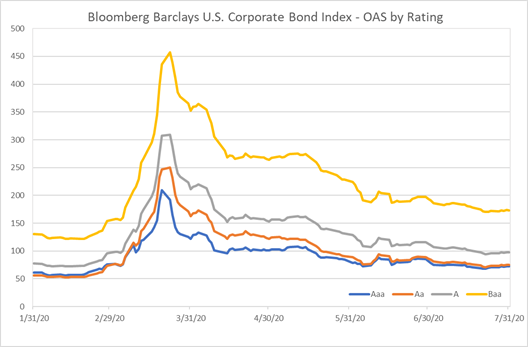

As noted above, BBB bonds increased as a percentage of the total investment grade market during 2020, which is a continuation of a longer trend. Based on the spreads of BBBs during the period, it appears the market is concerned. The chart below shows spreads as a function of ratings. As you can see, BBBs are substantially wider now than they were before the pandemic, and they are also substantially wider than any other rating category.

Source: Bloomberg

BBBs generally carry higher leverage and are more vulnerable to downturns in the economy, so not surprisingly they underperformed during the worst of the crisis and during the recovery. As expected, corporates with stronger balance sheets and higher ratings experienced less spread widening and recovered closer to pre-crisis levels.

Looking Ahead: Opportunities Exist

The investment grade credit market experienced a roller coaster ride in 2020, along with most risk assets. The dramatic widening of credit spreads highlighted the vulnerability of a $7 trillion market that has very few built-in shock absorbers and limited capacity to handle substantial selling pressure during periods of stress. Thanks to monumental support from the Fed, the market recovered quickly, and we believe that as long as Fed support remains in place until the pandemic passes, the IG market should remain stable for the foreseeable future. The key to successful investing in the current environment is avoiding weak credits and fallen angels, as Fed support cannot provide protection against losses from individual securities.

Looking forward, we remain constructive on corporate credit even though the vast majority of the recovery in spreads has likely already occurred. We are expecting spreads to tighten a bit further, primarily due to technical performance drivers. Specifically, the combination of (1) anticipated slower pace of issuance for the balance of the year, (2) supply leaving the market through downgrades and tenders, and (3) ongoing strong investor demand will likely create tighter spreads. We expect to maintain our exposure to investment grade credit with a bent towards higher quality credits that we expect will perform well going forward.

In addition, we feel that the dispersion of returns in the index indicates that there are still many compelling opportunities within the IG universe. Although the specific constituents of the Agg sectors may be misleading or unexpected, the index can still be used as an effective guide to help find investment opportunities. We have always believed careful security selection and rigorous fundamental credit analysis are the foundation of performance, and that is especially true in a world upended by Covid-19. With so many sectors still wider to the index than their pre-pandemic levels, we believe there is a rich opportunity set to pursue.

John Sheehan

Vice President & Portfolio Manager

Daniel Oh

Vice President & Portfolio Manager

Learn More about the Total Return Fund

The Morningstar Rating™ for funds, or “star rating,” is calculated for mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product’s monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period has the greatest impact because it is included in all three rating periods.

© 2020 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance does not guarantee future results.

Opinions expressed are those of the author, are subject to change at any time, are not guaranteed and should not be considered investment advice. Past performance does not guarantee future results. Fund holdings and sector allocations are subject to change and are not recommendations to buy or sell any security. Current and future portfolio holdings are subject to risk.

Mutual fund investing involves risk. Principal loss is possible. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities.

Past performance is not a guarantee of future results. Index performance is not illustrative of fund performance. One cannot invest directly in an index. Please call (866) 236-0050 for fund performance.

The Fund’s holdings may be viewed by clicking here.

The Bloomberg Barclays U.S. Corporate Index includes publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. The index includes exclusively corporate sectors, including Industrial, Utility, and Finance, which include both U.S. and non-U.S. corporations.

The Bloomberg Barclays U.S. Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded.

Investment grade bonds are bonds with high and medium credit quality assigned by a rating agency. For Standard and Poor’s, investment grade bonds include BBB ratings or higher. For Moody’s, the cutoff is Baa.

High-yield, or “below investment grade” bonds, include bonds with a lower credit rating than investment-grade. These bonds typically pay higher coupons as they are riskier.

A basis point is a unit that is equal to 1/100th of 1%.

A mortgage-backed security (MBS) is a type of asset-backed security that is secured by a mortgage or collection of mortgages.

EBITDA is an acronym for Earnings Before Interest, Taxes, Depreciation and Amortization.

Leverage ratio is a financial measurement that looks at how much capital comes in the form of debt (loans), or assesses the ability of a company to meet its financial obligations.

Spread is the difference in yield between a risk-free asset such as a U.S. Treasury bond and another security with the same maturity but of lesser quality. Option-Adjusted Spread is a spread calculation for securities with embedded options and takes into account that expected cash flows will fluctuate as interest rates change.

Interest coverage ratio is a measure of a company’s ability to service its debt and meet its financial obligations. The higher the coverage ratio, the easier it should be to make interest payments on its debt or pay dividends. The trend of coverage ratios over time is also studied by analysts and investors to ascertain the change in a company’s financial position.

The debt-to-equity (D/E) ratio is calculated by dividing a company’s total liabilities by its shareholder equity.

Credit Quality weights by rating were derived from the most recent data available as determined by Standard and Poor’s. Grades are assigned to bonds by private independent rating services such as Standard & Poor’s and these grades represent their credit quality. The issues are evaluated based on such factors as the bond issuer’s financial strength, or its ability to pay a bond’s principal and interest in a timely fashion. Ratings are expressed as letters ranging from ‘AAA’, which is the highest grade, to ‘D’, which is the lowest grade. In situations where Standard & Poor’s has not issued a formal rating, the security is classified as not rated (NR). Additionally, common stocks, if any, are classified as NR.

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [47026]

© Osterweis Capital Management