Emerging markets overall felt a dose of optimism in August amid hopes for a COVID-19 vaccine, continued easy monetary policy globally and improving economic data pointing toward recovery. Our emerging markets equity team breaks down the key trends, news and events it has an eye on, and shares its latest market outlook.

Three Things We’re Thinking About Today

- A trend witnessed in several countries globally, the daily number of COVID-19 cases in India started to increase in late-August as the country continued to ease quarantine restrictions and economic activity began to gradually normalize. A silver lining is that these countries—including India—have not seen a corresponding jump in mortalities, reflecting improved treatments and wider testing revealing asymptomatic cases. While this may raise uncertainty on the pace of economic recovery, government stimulus should filter into the real economy gradually, supporting a recovery in due course. Indian equity markets continue to trade at a discount to long-term averages, and we believe long-term reforms and expectations of faster earnings growth could support a re-rating. Importantly, while the government is working on reviving growth, the current challenging macro environment provides opportunities for stronger companies to gain market share at the expense of weaker ones. The macro picture can also fail to capture the disruption in business models, leading to shifts in the profit pool at the corporate level. For example, stronger private-sector banks have increased their lead at the expense of weaker public-sector banks or non-financial banking companies. We believe this factor, combined with our positive outlook on India in the long term (underpinned by several structural growth drivers), supports the case for investing in Indian equities.

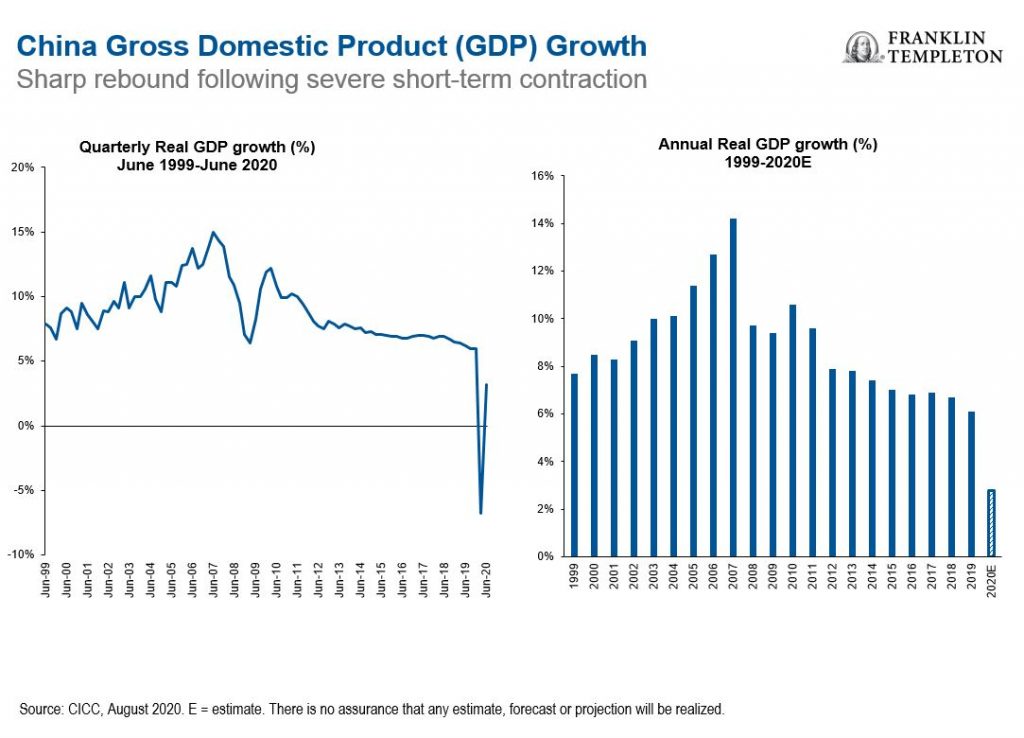

- Although US-China tensions heightened in August following US President Donald Trump’s decision to ban Chinese apps TikTok and WeChat in the United States, sanctions on Huawei, export controls and the South China dispute, commitment by American and Chinese officials to ensure the trade deal remains on track eased investor concerns that worsening relations could lead to the end of the agreement. While we expect US-China relations to remain volatile, we remain positive on China’s longer-term outlook as the country continues to emerge from the COVID-19 crisis with positive growth in gross domestic product (GDP) in the second quarter, raising expectations for positive growth for the year as a whole. Although domestic consumption continues to lag (although improving), other economic indicators such as industrial production and manufacturing have returned to pre-COVID-19 levels. Additional characteristics that favor China include continued domestic reforms, technological advancement, rapid digitalization, a huge consumer market and the availability of fiscal and monetary tools to help weather external shocks.

- In our view, Russia is in an enviable position when looking at a number of fundamental factors; it has little sovereign debt, a current-account surplus and considerable foreign exchange reserves. While oil—an old economy sector—is a major contributor to Russia’s economy, we have found that the new economy in Russia is also thriving. The country’s leading bank, for example, is so much more than a traditional bank. Its digital ecosystem incorporates artificial intelligence (AI), big data and robotization. Already it reports that 40% of client queries are solved by its chat box, and it has created its own private cloud and collaborated with others to offer services such as video streaming, e-education, restaurant bookings and ride sharing. Similarly, Russia’s leading search engine has built an impressive ecosystem. Already successfully competing with Google, it offers services such as e-commerce, ride sharing and online music in a similar fashion to Apple Music. Initiatives include a Russian version of Netflix with a plan to create its own content, and it is even developing autonomous cars. Thus, it would seem that in addition to its continued dominance in the old economy of oil, Russia appears to offer a compelling investment pool for those wanting to ride the structural tailwind of the new reality where consumption and technology underpin tomorrow’s drivers of growth.

Outlook

We continue to focus on three new realities in emerging markets (EMs). One is the institutional resilience of EMs. Many corporations across EMs entered the crisis with stronger balance sheets compared to those in developed countries—net cash levels once considered inefficient have proven to be prudent. Countries such as Brazil, India, China and South Korea have benefited from institutional reforms in years past, entering this crisis with stronger foundations and greater fiscal flexibility relative to history and Western peers—which also bodes well for recovery.

Second, the nature of EM economies has changed. We have seen a transformation in the last decade away from cyclical sectors and dependence on foreign demand, toward domestic consumption and technology. The contribution of trade to the Chinese economy has halved from its peak, ensuring that China is no longer beholden to a recovery in Western economies.

The third reality centers on innovation, and the notion of EMs “leapfrogging” the developed world in terms of infrastructure and business models. We have seen this unfold in areas such as mobile telecoms, broadband, e-commerce, and e-payments—and more recently in new areas such as education and health care amid lockdowns. Such business models are highly suited to the structures of EMs, and benefit from the availability of superior data coverage at substantially lower cost in countries such as China and India.

Emerging Markets Key Trends and Developments

EM equities notched a choppy advance in August, finishing behind developed market stocks. Investors welcomed improving economic data, encouraging news on potential coronavirus vaccines and treatments, as well as a new US monetary policy approach signaling an extended period of low interest rates. However, new clusters of COVID-19 infections and shaky US-China ties capped market sentiment. The MSCI Emerging Markets Index increased 2.2% during the month, while the MSCI World Index returned 6.7%, both in US dollars.1

The Most Important Moves in Emerging Markets in August 2020

Asian markets rose in August to seal the best regional performance in EMs. Stocks in China, India and Indonesia posted notable gains. Stronger service sector activity and other indicators in China pointed to the economy’s continued recovery. China and the United States also pledged commitment to their trade deal, even as the US administration ordered fresh restrictions on Chinese technology companies. In India, better-than-expected corporate earnings eclipsed an uptrend in COVID-19 cases. Meanwhile, stocks in Malaysia, Thailand and Taiwan fell. Thailand posted a sharp second-quarter economic contraction, while anti-government protests fueled political uncertainty. In Taiwan, investors tempered their outlook for certain suppliers to Huawei Technologies on tighter US sanctions.

Latin American equities bucked the global trend, with Chile and Brazil recording the largest declines, partly due to weaker domestic currencies. Uncertainty relating to the renewal of monthly emergency aid to support those impacted by lockdown measures pushed equities lower in Brazil, despite improving macroeconomic data and an interest-rate cut to a record low. However, Peru, Colombia and to a lesser extent, Mexico, ended the month with gains. Better-than-expected economic activity data and higher metal prices, driven by a pickup in economic activity, supported equity prices in Peru. In Mexico, improving manufacturing, industrial production and exports boded well for the economy. The central bank also cut its key interest rate by 0.5%, bringing the cost of borrowing to its lowest level in four years.

Markets in the Europe, Middle East and Africa region lagged their global peers in August. Equity prices in South Africa recorded a small decline despite a fall in the weekly number of new COVID-19 cases and the government’s continued easing of restrictions, opening the country for domestic travel. The Russian market edged up in August as investors balanced increasing political noise with progress on the development of a COVID-19 vaccine and better-than-expected second-quarter GDP data. In Central Europe, the Czech Republic and Poland outperformed Hungary, which ended the month in negative territory, as the government announced plans to close its border to non-residents to contain the spread of COVID-19 following an increase in new cases in neighboring countries.

© Franklin Templeton

https://emergingmarkets.blog.franklintempleton.com

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments