Back in high school, I ran hurdles. I wasn’t very good, but got a spot on the track team because no one else wanted to do hurdles. I quickly discovered why: It’s hard, and a small mistake makes a huge difference in your time. Plus, the practices were brutal. The better you got, the higher the hurdles. Sprinters got to run their hearts out, and the distance runners got to experience the “runner’s high.” Hurdlers were lucky to avoid falling down. There were a lot of bruises.

There’s a good chance that the Federal Reserve is in for a few bruises in the months and years ahead as it raises the acceptable hurdle rate for inflation. After a long review of its policy framework, the Fed announced it is shifting to an “average inflation target” of 2% rather than a precise target. Rather than tighten policy pre-emptively when it sees inflation moving above 2%, it plans to hold interest rates steady for some time, allowing the economy to run a little “hot” at times, after being “cool” for a long time.

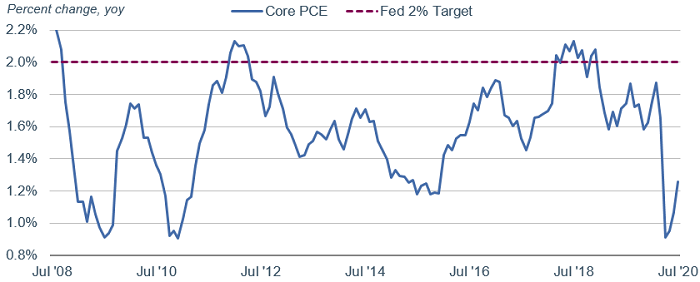

The immediate question that comes to mind is, “How will the Fed raise inflation?” After all, what good does it do to raise the target if you’ve been undershooting it for years? Core Personal Consumption Expenditures (PCE), which the Fed uses as its benchmark inflation measure, has spent most of the past 12 years below the 2% target.

Inflation has fallen short of 2% for most of the past decade

Source: Bloomberg. Personal Consumption Expenditures: All Items Less Food & Energy (Core PCE) (PCE CYOY Index), percent change, year over year. Monthly data as of 7/31/2020.

We believe the Fed will have a difficult time pushing up inflation, but inflation expectations are likely to continue to rise due to the change in the way the Fed will react to potential inflation. In fact, the Fed’s new stance is actually more focused on jobs than inflation. In his policy speech, Fed Chair Jerome Powell talked extensively about employment and the importance of the Fed doing all it can to support job growth. A part of the Fed’s review of its policy was a “listening tour” during which it engaged in discussions about the economy with communities across the country. The overwhelming message was that a strong labor market is important for improving the lives of individuals and the overall economy.

With that message and years of overestimating inflation based on the “natural rate” of unemployment, the Fed has abandoned its old framework and will not pre-emptively raise interest rates just because the unemployment rate falls below a predetermined level.

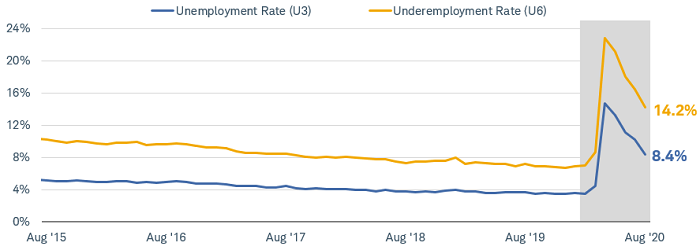

High unemployment is one of the Fed's biggest concerns

Source: Bureau of Labor Statistics. Civilian Unemployment Rate and Underemployment Rate, Total unemployed, plus all marginally attached workers plus total employed part time for economic reasons (U6 Rate), Percent, Monthly, Seasonally Adjusted. Shaded area indicates recession. Monthly data as of August 2020.

With the unemployment rate in double digits, pre-emptive rate hikes wouldn’t have been on the agenda anytime soon, anyway. However, the change is important. The Fed has thrown the Phillips curve (which describes the relationship between employment and inflation) into the dumpster. Whether it’s due to the effects of globalization, the decline in unionization, or the rise of service sector jobs over manufacturing jobs, wage growth has slowed relative to productivity growth over the past few decades. This has resulted in a decline in labor’s share of gross domestic product (GDP). Consequently, economic growth doesn’t necessarily translate into money in the pockets of those most likely to spend it—lower- and middle-income workers. Without a pocket full of money to drive up demand for goods and services relative to supply, a low unemployment rate doesn’t necessarily lead to inflation.

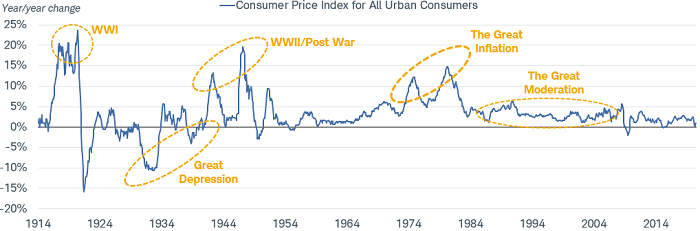

Inflation is not what it used to be

The Phillips curve is only one of the inflation metrics to get tossed. The truth is, the Fed and most economists are struggling with the breakdown in the relationship between inflation and the factors that were historically believed to drive it. The demographics of an aging population is a long-term, structural issue that appears to be keeping inflation low. Moreover, inflation expectations have moderated considerably since the 1980s. Once the back of inflation was broken in 1980s, things changed. The 1990s ushered in the “great moderation,” followed by recession and the crisis-packed 2000s.

Inflation volatility has moderated since the 1980s

Source: Bloomberg, using monthly data as of 7/31/2020. US CPI Urban Consumers year-over-year (YoY) NSA (CPI YOY Index).

All of these structural economic changes led to changes in the old economic relationships. Money supply growth, nominal GDP growth, employment growth, and even commodity prices are not nearly as useful in forecasting inflation as they were in the past. Here’s a quick look at each one:

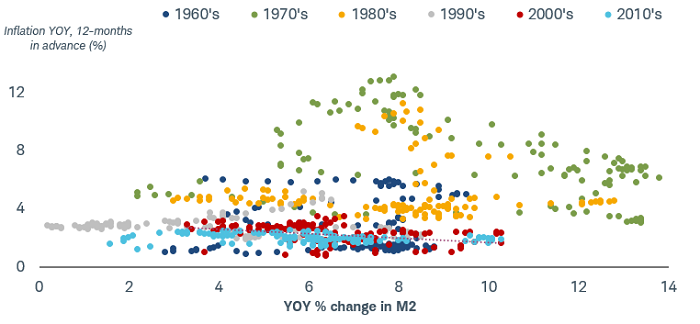

1. Money supply growth: Not enough

Economist Milton Friedman famously said that inflation is “always and everywhere a monetary phenomenon.” It was gospel for years, but now money supply growth doesn’t correlate well with inflation. It is a prerequisite for inflation, but isn’t sufficient by itself. The money has to circulate in the economy—and that isn’t happening. Much of the money created since the onset of the COVID-19 crisis is sitting in checking and savings accounts, as wary consumers build savings.

Money supply growth is less likely to correspond with inflation than in the past

Source: Bloomberg. Inflation Composite Indicator and year-over-year (YoY) change in M2. M2 is a measure of the money supply that includes cash, checking deposits and easily convertible “near money,” such as savings deposits, money market securities, mutual funds and other time deposits. Monthly data as of 7/31/2020.

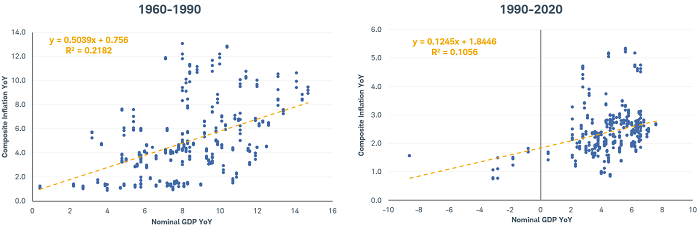

2. GDP growth has become a weaker driver of inflation

It’s a similar story with GDP growth. It’s often assumed that stronger growth will boost inflation, but in recent years that hasn’t been the case. Not only are nominal growth rates much lower now, but the sensitivity to inflation has also fallen.

During the past 30 years, GDP growth and inflation have become less correlated

Source: Bloomberg. Nominal GDP YoY and a Composite Inflation Indicator (GDPCURY Index). Monthly data as of 7/31/2020.

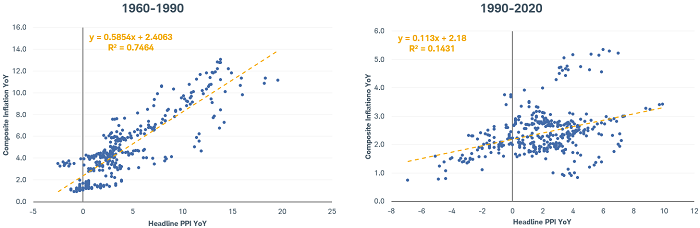

3. Commodity prices are a diminishing factor.Commodity prices show a similar trend toward diminished correlation with inflation. In the 1960s-1980s wholesale prices were a major driver of finished goods prices and therefore inflation. In the past 30 years, that relationship has weakened. Raw materials prices are a diminishing factor. Value-added costs are a more important factor in pricing.

“Inflation in the pipeline” doesn’t necessarily result in consumer inflation

Source: Bloomberg. US PPI Finished Goods NSA YoY% and Inflation Composite (PPI YOY Index). Monthly data as of 7/31/2020.

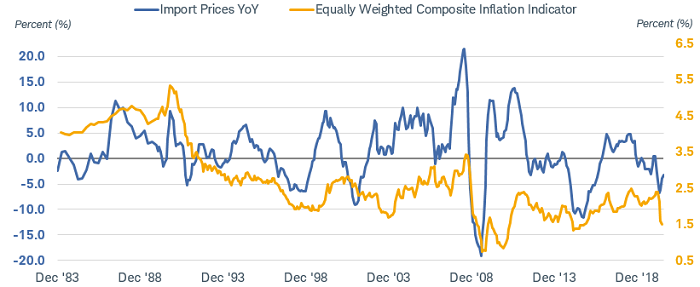

4. Currency has a weaker impact than in the past.Currency changes are another example of how inflation dynamics have changed. Throughout much of the period from 1960 to 1990, a 10% move in the dollar would lead to a change in the inflation rate of about 0.4%. In recent years, the impact has fallen by half. A weaker currency should raise inflation by boosting domestic growth as exports become more competitive, and raising the cost of imports. Even though trade is a relatively small proportion of GDP for the U.S., there was a strong correlation in years past. However, with increased domestic production of oil, globalization, and more widespread use of the dollar in financing global transaction, currency movements have had less impact. In other words, a weaker dollar may help lift inflation on the margin, but it’s not the solution to the Fed’s problems.

The dollar has less influence on import prices than in the past

Source: Bloomberg. Import Prices YoY and Inflation Composite (IMP1YOY% Index). Monthly data as of 7/31/2020.

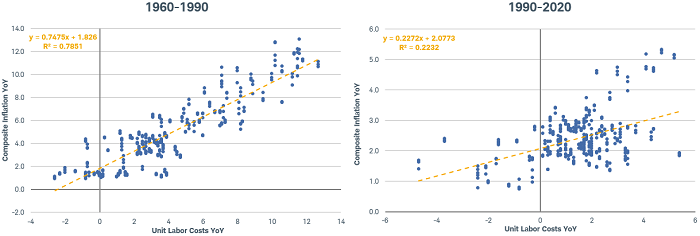

5. Labor costs are still important, but their impact has declined.Labor costs still show a statistically significant correlation with inflation, but the relationship has declined over the years, as well. Still, using all of its tools to boost the labor market is probably the best shot the Fed has to achieve its goals.

The relationship between labor costs and inflation has declined in the past 30 years—but is still statistically significant

Source: Bloomberg. Unit Labor Costs YoY and a Composite Inflation Indicator (COSYNFRM Index). Monthly data as of 7/31/2020.

In sum, the Fed’s new framework is a concession to reality. It has relied on the Phillips curve and old relationships to try to forecast inflation, only to find out that it has overestimated inflation risks for decades. It will now take a patient approach and wait for inflation to show up before taking action in hopes of getting more people into jobs and supporting economic growth. The hurdles are very high. As a result, we expect the Fed to keep short-term rates near zero for several more years.

What this could mean for markets

The Fed’s new stance should have implications for the markets, including:

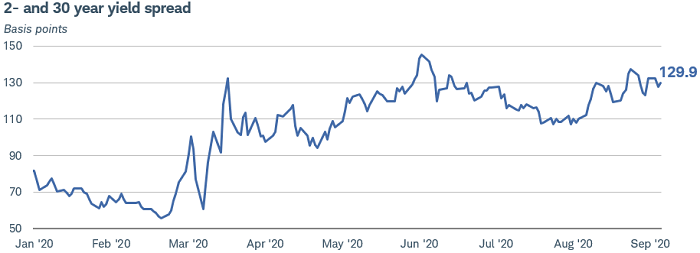

1. The yield curve likely will steepen.The initial reaction to the Fed’s policy announcement was a steepening in the yield curve. Long-term yields rose while short term yields remained pinned near zero. That’s a logical response to the signal from the Fed. However, within a few hours of Powell’s speech, bond yields gave back much of the gain, perhaps on the realization that it could be a long time before inflation actually shows up in a meaningful way. Nonetheless, we believe the curve will continue to steepen somewhat, as the market builds in a greater inflation risk premium and more concession for increased supply of Treasuries.

The Fed’s new inflation stance has steepened the curve

Note: The rates are comprised of Market Matrix U.S. Generic spread rates (USYC2Y30). This spread is a calculated Bloomberg yield spread that replicates selling the current 2 year U.S. Treasury Note and buying the current 30 year U.S. Treasury Note, then factoring the differences by 100. Source: Bloomberg. Daily data as of 9/9/2020. Past performance is no guarantee of future results.

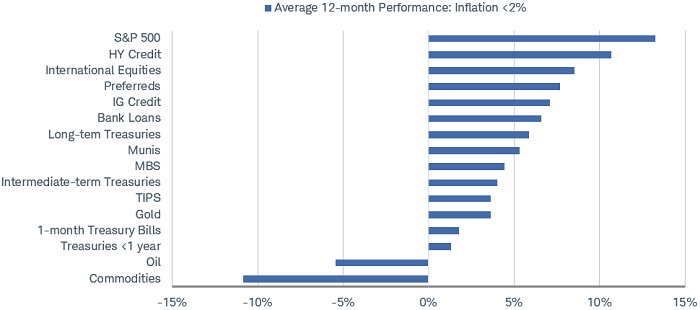

2. Moderate inflation may favor credit exposure, but high inflation would not.

While investors often worry about the bond market in times of inflation, historically moderate inflation has been good for returns in bonds with credit exposure (that is, the possibility the issuer will default on payments or at worst, fail to return principal). Given the Fed’s easy policy stance, ample liquidity and the potential for economic recovery, credit spreads should continue to decline. History tells us that the riskier segments of the markets do best in an environment of low to moderate inflation. However, we’re not inclined to overweight lower-rated corporate or municipal bonds, as we do see scope for spreads to narrow further.

Average performance when inflation is at 2% or lower

Source: Bloomberg & Morningstar. Monthly data as of 6/30/2020. Each return listed is for the full time period available for each of the asset class indices shown. HY Credit = Bloomberg Barclays High Yield Credit Index; International Equities = MSCI EAFE NR Index; Preferreds = ICE BofA Fixed Rate Preferred Securities; IG Credit = Bloomberg Barclays U.S. Aggregate Corporate Bond Index; Bank loans = S&P/LSTA U.S. Leveraged Loan 100 Index; Long-term Treasuries = IbbotsonAssociates SSBI U.S. Long-Term Government TR; Munis = ICE BofA U.S. Municipal Securities Index; MBS = ICE BofA U.S. Mortgage Backed Securities Index; Intermediate-term Treasuries = IbbotsonAssociates SBBI U.S. Intermediate-Term Government TR; TIPS = Bloomberg Barclays U.S. Treasury Inflation-Linked Bond Index; Gold = Gold Dollar Spot; 1-month Treasury Bills = IbbotsonAssociates SBBI U.S. 30 Day Treasury Bills TR; Treasuries <1 year = Bloomberg Barclays US Short Treasury Index; Oil = Crude Oil – WTI; Commodities = LF98TRUU Index, NDDUEAFE Index, P0P1 Index, LUACTRUU Index, SPBDLL Index, U0A0 Index, M0A0 Index, LBUTTRUU Index, XAU Curncy Index, LT12TRUU Index, CL1 Comdty Index, SPGSCITR Index. Past performance is no guarantee of future results.

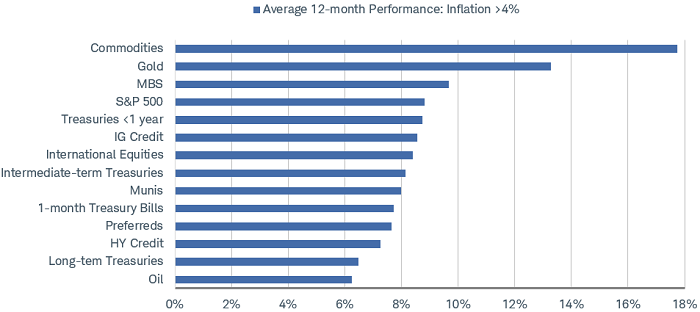

Historically, higher inflation has benefited “hard assets” such as gold and other commodities. However, it should be noted that periods of inflation above 4% were mostly seen in the “old regime” of 1960-1990.

Average performance when inflation above 4%

Note: Each return listed is for the full time period available for each of the asset class indices shown. For a description of the indexes used to represent each asset class, please see the Important Disclosures below. Source: Source: Bloomberg & Morningstar. IbbotsonAssociates SSBI U.S. Large Stock TR, Bloomberg Barclays High Yield Credit Index, MSCI EAFE NR Index, ICE BofA Fixed Rate Preferred Securities, Bloomberg Barclays U.S. Aggregate Corporate Bond Index, S&P/LSTA U.S. Leveraged Loan 100 Index, IbbotsonAssociates SSBI U.S. Long-Term Government TR, ICE BofA U.S. Municipal Securities Index, ICE BofA U.S. Mortgage Backed Securities Index, IbbotsonAssociates SBBI U.S. Intermediate-Term Government TR, Bloomberg Barlcays U.S. Treasury Inflation-Linked Bond Index, Gold Dollar Spot, IbbotsonAssociates SBBI U.S. 30 Day Treasury Bills TR, Bloomberg Barclays US Short Treasury Index, Crude Oil - WTI, Commodities (LF98TRUU Index, NDDUEAFE Index, P0P1 Index, LUACTRUU Index, SPBDLL Index, U0A0 Index, M0A0 Index, LBUTTRUU Index, XAU Curncy Index, LT12TRUU Index, CL1 Comdty Index, SPGSCITR Index). Monthly data as of 6/30/2020. Past performance is no guarantee of future results.

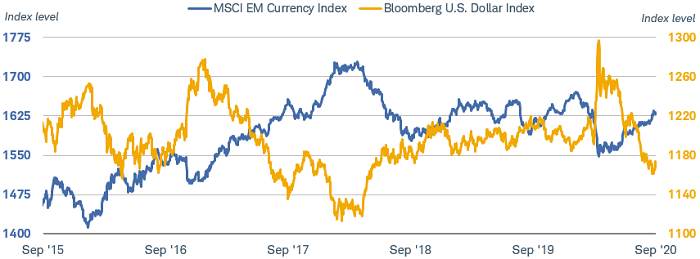

3. TIPS and emerging-market bonds may benefit.Treasury Inflation-Protected Securities (TIPS) and emerging-market (EM) bonds are not included in the charts above because of lack of data in the older era. However, these are two investments that could benefit now. The Fed’s dovish tilt should continue to put downward pressure on the dollar and support global growth—bothpositive factors for EM bonds. It’s a risky segment of the market, but one that has lagged in performance relative to other aggressive-income bonds.

Emerging market currencies have risen on the back of the Fed’s more dovish tilt

Source: Bloomberg. MSCI Emerging Markets Currency Index (MXEF0CX0 Index) and Bloomberg U.S. Dollar Spot Index (BBDXY Index). Daily data as of 9/9/2020. Past performance is no guarantee of future results.

TIPS also may benefit from the Fed’s shift in stance. Year-to-date performance has been strong, but breakeven rates are still below the 2% target, leaving room for a further rally. The downsides are low-to-negative yields, but for investors concerned about inflation rising above 2%, TIPS can provide a hedge.

TIPS breakeven rates are still below 2%

Source: Bloomberg. U.S. Breakeven 10 Year (USGGBE10 Index) and U.S. Breakeven 5 Year (USGGBE05 Index). Daily data as of 9/9/2020. Past performance is no guarantee of future results.

There are potential risks to our outlook. The first is the potential for a double-dip recession due to lack of fiscal relief. In general, we’re optimistic that the economy will continue to improve over the long run. However, the next six months are likely to be challenging if there’s no more fiscal relief from the federal government. Economic momentum is already ebbing and the virus is still active in many places. Until there is a vaccine or the virus has run its course, the potential for another contraction in growth near the end of the year is uncomfortably high. That could mean renewed flattening of the yield curve and wider credit spreads on the risk of rising defaults.

The second risk is around global growth. Markets are pricing in a global reflation, but there is room for concern. On the positive side, global trade is rebounding and a cessation of trade conflict with China is allowing for normalization of supply chains. However, the rise of COVID-19 cases in Europe, and ongoing spread in Latin America could hold back the economic recovery.

The third risk is the potential for the Fed to lose control of the yield curve. It seems unlikely, but if there were to be a bout of significant inflation pressure without a policy response from the Fed, it’s possible that long-term rates could rise more sharply than expected. With record amounts of deficit financing to be done and real yields in negative territory, it’s something to consider. We assume the Fed would use yield curve control to shift purchases to the long end of the curve to hold down rates, but it’s impossible to know for sure.

What investors should consider now

This is a good time to consider bond ladders or barbells. A bond ladder is a portfolio of individual bonds that mature at different dates. A steepening yield curve would allow you to reinvest maturing bonds at higher yields and earn more income over time. (If yields fall, it’s true that you’ll be reinvesting at lower interest rates, but you’ll already have some higher-yielding bonds in your portfolio from when you initially put the ladder together.)

Barbells are another potential strategy. With a bond barbell, you hold some short-term maturities and some longer-term maturities. This is another way to lock in yields, although investments at the long end can be volatile. We often suggest barbells as a way for investors who have been on the sidelines in cash to work into a ladder. They can add rungs on the ladder over time.

We don’t expect a big rise in 10-year Treasury yields from current levels, but we would consider adding some intermediate to longer-duration bonds if yields push up toward 1%. At current levels, the risk/reward on longer-duration bonds is not that attractive, although holding some long-term bonds can provide both added income and a hedge against a bout of volatility in risk assets. Overall, we prefer keeping average duration somewhat below that of the typical benchmark, given the low level of yields.

We suggest a neutral weighting to corporate bonds. The risk/reward balance looks reasonable, with yield spreads versus Treasuries still slightly above long-term averages. However, we continue to suggest staying up in credit quality due to the likelihood of rising defaults and downgrades.

We see value in highly rated municipal and corporate bonds for core bond holdings. For investors willing and able to take more risk, we favor preferred securities and emerging market bonds.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

ICE BofA U.S. Municipal Securities Index, (U0A0 Index), tracks the performance of US dollar denominated investment grade tax-exempt debt publicly issued by US states and territories, and their political subdivisions, in the US domestic market

ICE BofA U.S. Mortgage Backed Securities Index, (M0A0 Index), tracks the performance of US dollar denominated fixed rate and hybrid residential mortgage pass-through securities publicly issued by US agencies in the US domestic market.

IbbotsonAssociates SSBI U.S. Long-Term Government TR, Measures the performance of long-term maturity U.S. Treasury bonds. It is an unweighted (equal-weight) index.

S&P GSCI Total Return CME (SPGSCITR Index), The S&P GSCI Total Return Index in USD is widely recognized as the leading measure of general commodity price movements and inflation in the world economy. Index is calculated primarily on a world production weighted basis, comprised of the principal physical commodities futures contracts.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Commodity related products carry a high level of risk and are not suitable for all investors. Commodity related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Currencies are speculative, very volatile, and not suitable for all investors.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. You must perform your own evaluation of whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance and financial circumstances.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0920-0EXD)

© Charles Schwab & Co.

© Charles Schwab

More Global Markets Topics >