The U.S. stock market hit pause in early September, as investors took a harder look at market overconcentration and frothy sentiment. Meanwhile, global economies may be entering a new phase, and the Federal Reserve’s newly announced inflation policy is likely to keep U.S. rates lower for longer.

U.S. stocks and economy

With the recovery showing some signs of stalling in certain areas of the economy, the U.S. stock market’s rally took a breather. Pushed by momentum chasing and excessive froth in measures of sentiment and the options market, U.S. stocks’ climb to new highs reversed course at the beginning of the month. The Information Technology sector was hit hard as investors rotated into more traditional cyclical sectors, as well as into some defensive areas like utility stocks.

Much of the risk leading up to the recent selling pressure was related to overconcentration. As you can see in the chart below, the largest five stocks in the S&P 500® Index recently accounted for nearly 25% of market capitalization, while for the Nasdaq Composite (note the data is limited and the series starts later), it was a more staggering 38%.

The top 5 stocks continue to dominate as a percentage of market cap

Source: Charles Schwab, Bloomberg, as of 9/9/2020.

Compared to the tech bubble that formed in the late 1990s, the largest companies now have more solid fundamentals. However, the risk associated with their dominance is that any rotation out of them—like we saw earlier this month—could lead to a more amplified downturn in the broader market.

August saw the S&P 500 and Nasdaq 100 (which is a basket of the 100 largest, most actively traded non-financial stocks in the overall Nasdaq) hit a number of new all-time highs, while volatility was simultaneously rising. As you can see in the next chart, both volatility measures that track each index remain elevated relative to pre-pandemic levels and were increasing alongside stocks. It was a head-scratching feature of the most recent bull market, but partly explained by coming election risk, which elevated the cost of October volatility contracts relative to the spot price.

Volatility rose along with stocks

Source: Charles Schwab, Bloomberg, as of 9/9/2020. Past performance is no guarantee of future results.

Internals within the market—like the previously mentioned concentration risk—were flashing warning signs. As fewer names made new 52-week highs and/or were trading above their 50- and 200-day moving averages, the market’s backdrop grew weaker as participation narrowed. This again highlighted the strength of just a few of the largest names.

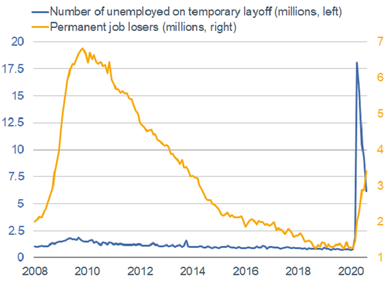

A bifurcated picture has more or less been the same in the economy, as some areas like housing and retail sales have already bounced back above pre-pandemic levels, while restaurants and other small businesses struggle to navigate reopening and hiring back employees. As we saw in the August U.S. jobs report, the pace of job growth has slowed. You can see in the chart below that permanent job losses have increased to 3.4 million, while those on temporary layoff have fallen to 6.16 million (down from their peak of 18 million in April).

Permanent job losses pick up as temporary layoffs fall

Source: Charles Schwab, Bureau of Labor Statistics, as of 8/31/2020.

Despite a falling unemployment rate, the increase in permanent job losses doesn’t bode well for the labor market—especially if continuing jobless claims remain elevated and the pace of economic growth moderates as we emerge from the immediate aftermath of the shutdown.

Global stocks and economy: Stage 1 complete

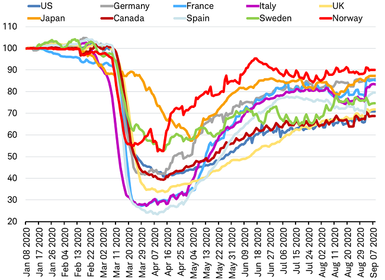

The global recovery appears to have reached the end of stage 1. The initial, sharp economic rebounds coming out of the global COVID-19 lockdowns are now largely complete across most of the world, as you can see in the chart below.

Countries have rebounded from pandemic shutdowns

Source: Charles Schwab, Bloomberg data as of 9/8/2020. Chart uses high-frequency activity indexes to reflect activity in each country. The activity indexes are estimated using a dynamic factor model with a methodology that extracts an unobservable latent common factor of the underlying high-frequency data—where a reading of 100 means activity has returned to pre-pandemic levels, and thus indicates strength. The axis’ scale indicates the percentage of activity that is back to normal. The sources of the underlying data used in the model are: Bloomberg Economics, Google, Moovitapp.com, German Statistical Office, BNEF.com, Indeed.com, Shoppertrak.com, Opportunity Insight.

After recovering about halfway from April through July of this year, the global economy likely transitioned in August to the next stage. This second stage may proceed at a more gradual pace now that inventories have been restocked, pent-up demand has largely been exhausted, and major parts of the service sector of the economy remain constrained (i.e. travel and entertainment). Economic progress may be uneven, interrupted by a return to localized lockdowns due to virus outbreaks, as seen recently in Spain, France, and Japan. The stock market may face further volatility during this period, but not enough to elicit major new stimulus from policymakers.

Will volatility rise in stage 2?

Source: Charles Schwab, Bloomberg data as of 9/4/2020. Past performance is no guarantee of future results.

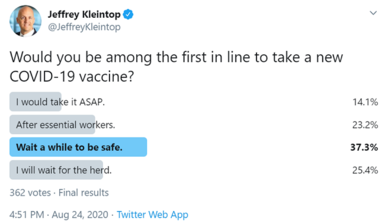

How long the second stage of recovery lasts largely depends on widespread availability of a COVID-19 vaccine, which would mark the beginning of the third and final stage of the recovery, when all sectors of the economy can return to normal. This offers some explanation for the market’s recent daily obsession with vaccine headlines.

However, it’s important to realize that a vaccine doesn’t flip the switch to stage 3 overnight. Initially, supplies may be limited and would likely go to first responders in countries that have preemptively secured supplies ahead of availability. Many surveys—including the informal poll we took on Twitter —show many people would be hesitant to take a new vaccine. As a result, it is likely that pandemic risk would continue to circulate in the population well after a vaccine is available—resulting in physical distancing and limits on economic activity for many months even after a vaccine is developed.

Most respondents in our informal poll would wait to take a vaccine

The good news? The global economy remains on the road to recovery, though at this stage of the journey, there may be some potholes.

Fixed income: Bond yields likely to stay low

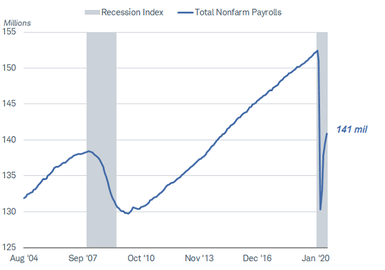

Amid signs of improvement in the labor market, rising inflation expectations, and record issuance of Treasury securities, bonds yields have remained low. Can these trends continue? We believe they can—for a while. There is still enough weakness in the economy and inflation to keep bond yields low this year and into 2021. With the Federal Reserve indicating it intends to keep short-term interest rates low for the next few years, the upside potential in bond yields is likely to be limited. However, with yields below the inflation rate, we believe investors may want to consider strategies to mitigate the risk of rising yields longer-term. The economy is improving from the spring’s steep decline. Recent job gains (on average) in the millions per month, along with fiscal relief, have helped prevent a deeper contraction in the economy. However, there is still a long way to go to recover what has been lost. Only about half of the jobs lost since the onset of the pandemic have been recovered and about a third of those who were laid off are now permanently unemployed. Moreover, the duration of unemployment is rising. In the past, long spells of unemployment have made it harder for workers to retain skills and re-enter the job market.

Payrolls climbing back, but still far below the February peak

Source: Bloomberg. US Employees on Nonfarm Payrolls Total SA and the Monthly Recession Index (NFP T Index, USRINDEX Index). Monthly data as of 8/31/2020.

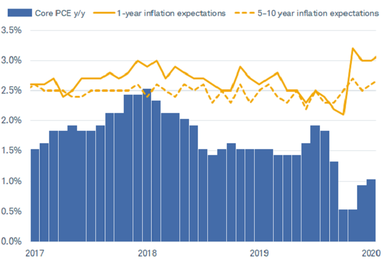

High unemployment tends to keep wages down. The excess supply of labor means employers can generally find workers at lower wage rates, keeping a lid on inflation. Despite some bottlenecks driving up costs of a handful of goods, most inflation readings indicate that overall price increases remain tame. The indicator commonly watched by investors—the Consumer Price Index—is rising at about 1% annual rate. However, inflation expectations have been picking up, likely due to the belief that the Federal Reserve’s easy monetary policy will lift prices longer term. It’s the same pattern we saw in the aftermath of the financial crisis. Every time the Fed announced a new round of bond buying (quantitative easing), inflation expectations and bond yields moved up.

Inflation expectations have been picking up

Source: Bloomberg. U.S. Personal Consumption Expenditures Chain Type Price Index YoY SA (PCE DEFY Index). Monthly data as of 7/31/2020. University of Michigan 1-year inflation expectations (CONSEXP Index) and 5-10 year inflation expectations (CONSP5MD Index). Monthly data as of 8/28/2020.

However, inflation remained tame despite the Fed’s expansive policies. It’s apparent that the drivers of inflation have changed over the years. It would not be surprising to see the pattern repeated in this cycle. Investors may anticipate more inflation than occurs and drive long-term bond yields higher for a while.

The prospects of ever rising budget deficits may put upward pressure on bond yields longer-term. Issuance of treasury securities continue to increase to keep pace with record high deficits. For the near term, the impact on the bond market appears to be modest. Low or negative yields in other major countries have meant global investors continue to find U.S. treasuries relatively attractive. Also, financing the deficit at record-low yields has meant high levels of debt are having limited impact on the economy or the bond market. Longer-term however, we are concerned that rising deficits could lead to higher yields.

As long as the economy is showing signs of gradual improvement, we expect long-term bond yields trend moderately higher, with 10-year Treasury yields potentially moving up to near 1%. The yield curve should continue to steepen, in line with the rebound in real economic growth and employment. For the near term, we suggesting limiting average portfolio duration to mitigate the risk of rising rates. For investors, looking for more income, one strategy to consider is a bond ladder. Regular reinvestment of principal in a rising rate environment can lead to higher income over time.

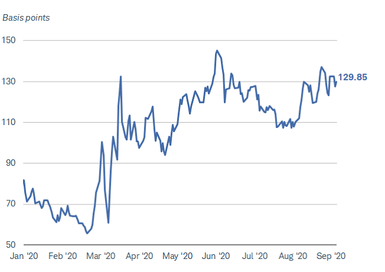

The Fed’s new inflation stance is steepening the yield curve

Note: The rates are comprised of Market Matrix U.S. Generic spread rates (USYC2Y30). This spread is a calculated Bloomberg yield spread that replicates selling the current 2 year U.S. Treasury Note and buying the current 30 year U.S. Treasury Note, then factoring the differences by 100. Source: Bloomberg. Daily data as of 9/9/2020.