Recovery Changes Seasons

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe pandemic has made indoor activities and gatherings risky. During the summer, outdoor adventures and backyard socializing were effective workarounds. But as autumn takes hold, the cooling air will gradually limit those options.

This summer also brought a series of promising economic reports, with many sectors showing a warming trend. Growth during the third quarter will likely break records, albeit from a low starting point. But the change of seasons also seems to be bringing a cooling trend to economic momentum.

With COVID-19 cases rising again and policy support falling away, the recovery is facing rising risks just a few months after it began. The course of the virus and the policy response to ongoing economic dislocation will continue to determine the course of growth and create uncertainty around the outlook.

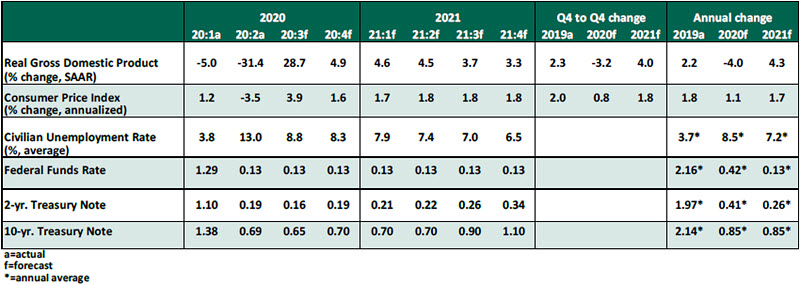

Key Economic Indicators

Influences on the Forecast

- The outbreak of COVID-19 in the White House has captured recent headlines, but the resumed rise in U.S. cases will be the more impactful development for the economy. Reopening will likely proceed more slowly than previously thought, and reversals may become more common as colder weather aids transmission.

- Congress has failed to agree on a renewed fiscal aid package. The House passed a more limited stimulus bill than its May effort, but it remained too large to find majority support in the Senate. The Treasury secretary had quietly kept negotiations going, but the president expressed significant misgivings about the outlines of a compromise. Action before Election Day now seems unlikely. Federal Reserve Chairman Jerome Powell said the economy could face “tragic” risks if fiscal support is not sustained.

- The costs of the stimulus failure will be diverse: personal income fell sharply last month, as supplemental unemployment benefits expired. The rate of small business failure appears to be accelerating now that benefits of the Paycheck Protection Program have worn off. Industries that had received aid in exchange for postponing layoffs announced substantial headcount reductions this month.

- In light of these factors, we have revised our growth outlook down somewhat. The third quarter was a quarter of historic advance, with sectors including housing and manufacturing witnessing a rebound after a halted second quarter. But broad high-frequency indicators are flattening out and industries dependent on interpersonal interaction, including travel, hotels, conventions and restaurants, will remain impaired until a COVID-19 vaccine is perfected and widely distributed. Medical professionals anticipate that this process will not be complete until the end of 2021.

- The unemployment rate fell to 7.9% in September, a much smaller improvement than the large monthly reductions seen since joblessness reached a peak of 14.7% in April. The slower improvement suggests the recovery is changing gears, and further gains will be more difficult. The labor force participation rate has fallen for two consecutive months, while the number of respondents reporting a permanent loss of employment grew to 3.7 million, triple its pre-crisis level. Discouraged workers are beginning to abandon efforts to return to work.

- Inflation is receiving a good deal of attention in light of the Fed’s change to its inflation targeting strategy, but uneven demand in the economy will leave us years away from worries about exceeding the Fed’s target of sustained 2% core inflation. The Consumer Price Index (CPI) grew by 1.3% year-over-year in July. The deflator on personal consumption expenditures (PCE) grew by 1.4%, and by 1.8% on a core basis (excluding food and energy).

- As government supplements expire, personal income growth is retreating from its high spring levels; income from employment compensation remains lower year-over-year. The rate of personal saving remains elevated at 14.1% of disposable personal income, but this is in decline, suggesting that consumers are using their savings to survive an income disruption.

- Interest rates remain well-contained, despite rapidly rising debt. Forecasts from the Congressional Budget Office indicate U.S. federal borrowing will exceed 100% of GDP in 2021 and 200% of GDP by 2050. Nonetheless, the country’s ability to service its debt is not currently in question. When COVID-19 is in the past, the high debt level will spark many debates about taxation and spending.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All