The ongoing COVID-19 pandemic has led to the closure or partial closure of many on-campus dormitories and privately run, offsite facilities. Against this backdrop of weakening demand and uncertainty around when college life may return to normalcy, our municipal bond team’s Vander Shanholt gives his take on the long-term challenges for student housing projects. He also explains why state budget cuts due to the pandemic could lead to opportunities for public-private partnerships to finance campus infrastructure projects.

For many years, colleges and universities across the United States have faced challenges arising from aging facilities. While some schools are able to borrow directly or leverage a large alumni base to fund capital improvements, a number of both public and private schools have utilized tax-exempt financing to fund the construction of privatized student housing projects.

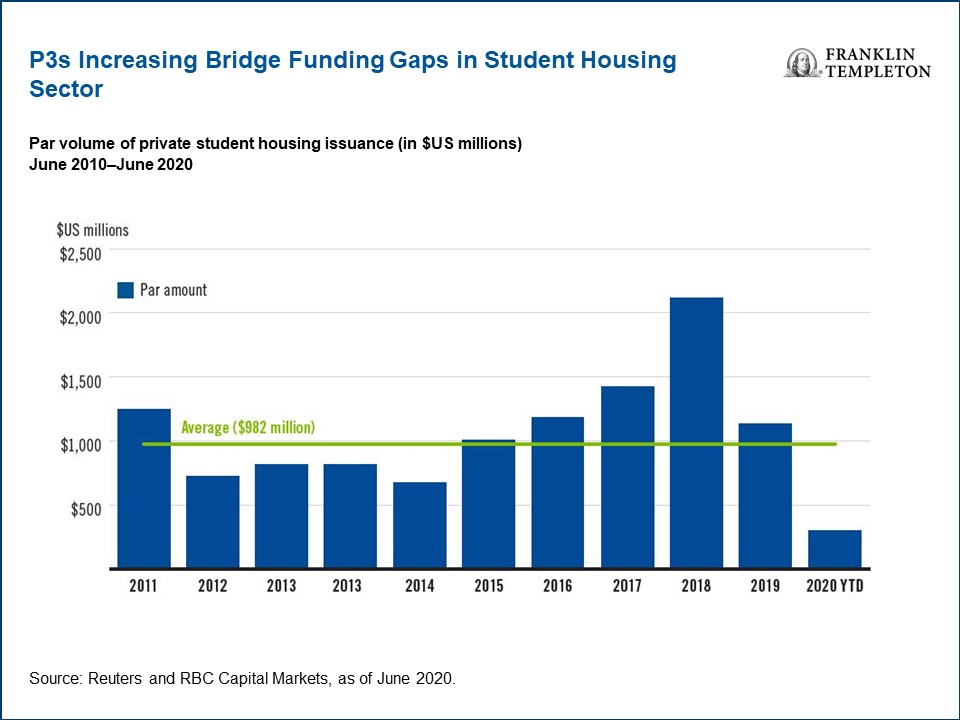

These public-private partnerships, otherwise known as P3s, have increasingly become the workaround for chronic gaps in public funding. Between 2010 and 2019, there was approximately $11.1 billion of tax-exempt debt issued to finance P3 projects, including $6.7 billion over the last five years, as shown below.

It is important to note that 2018 saw an abnormally high number of P3 issuance in terms of par amount due to a couple of large transactions, including an over $500 million issuance for a project at the University of California-Davis. In 2019, we saw issuance return closer to what we have seen in previous years.

There is no question the COVID-19 pandemic has materially impacted the student housing sector. As cases increased in March, nearly every college and university closed its campus for the remainder of the spring semester and ordered students to depart on-campus housing facilities.

Schools have provided various levels of support for impacted projects. In some cases, as with University of California-Irvine, the university stepped into existing leases to ensure privatized student housing projects would receive their full year of revenues. Our analysis shows other institutions were less supportive, requiring the P3 projects to refund students their pro-rata portion of rent, reducing annual revenues between 15% and 30%. These projects have little flexibility to mitigate revenue reduction through expense management, given the majority of fixed costs are derived from principal and interest requirements.

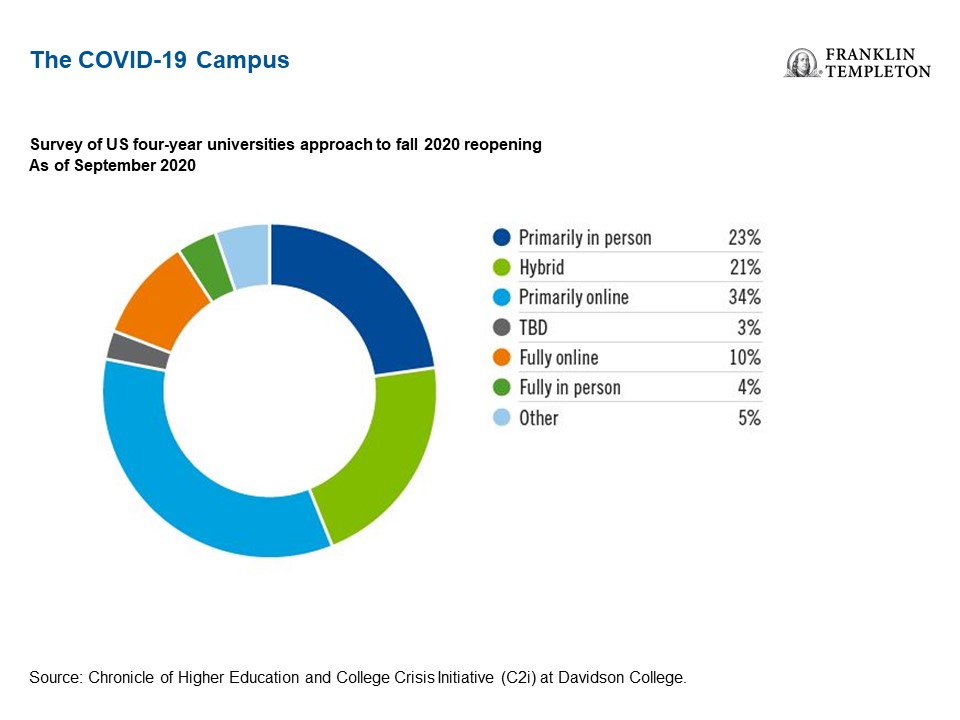

The coronavirus pandemic has left schools with difficult decisions as to how to reopen campuses for the 2020/2021 academic year. The Chronicle of Higher Education has been tracking the reopening models for nearly 3,000 institutions as we enter the fall semester. As of September 14, 2020, the majority of schools were offering at least a portion of the curriculum through online courses and very few institutions were providing fully in-person classes, as the chart below shows.1

The schools that will at least partially reopen have implemented initiatives to reduce the spread of the virus. Plans include requiring masks in public spaces, disinfecting and cleaning areas more frequently and de-densifying student housing. Housing de-densification refers to the practice of limiting the number of students that may live in each room. Certain student housing projects will be required to reduce occupancy to comply with university requirements.

As we enter the fall semester, the COVID-19 pandemic has negatively impacted occupancy across almost all privatized projects. American Campus Communities, one of the largest developers and managers of student housing, reported an 8% drop in occupancy in September as a result of both campus closures and reduced college attendance.2 The decline was twice as high among first-year students,3 reducing average occupancy just over 15%, from 95.7% in September 2019 to 79.5% in September 2020.

Finding Value Around Campus

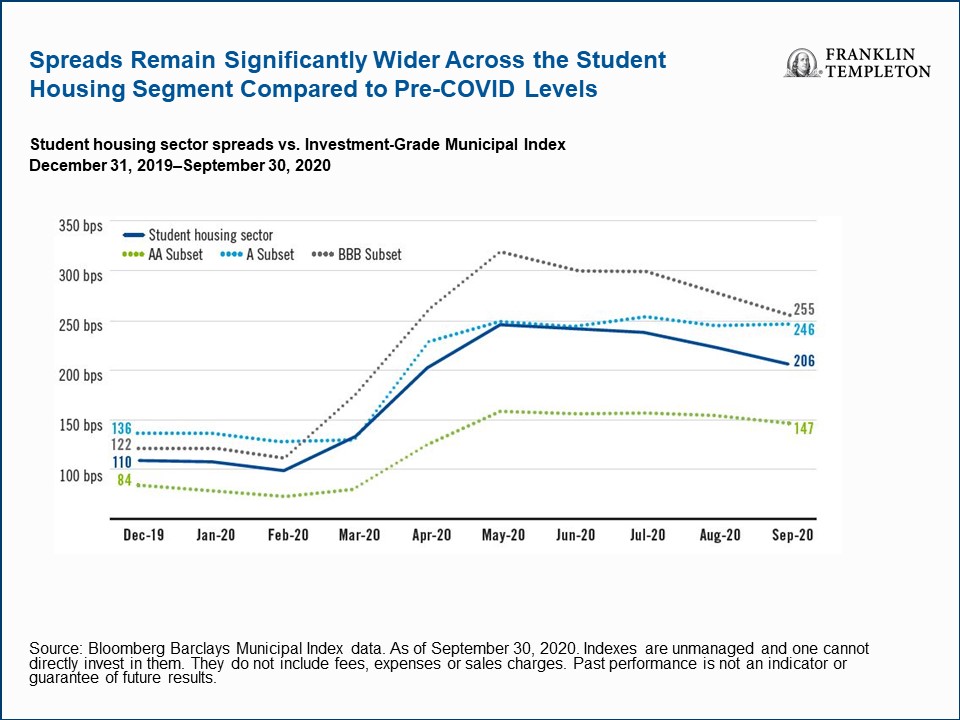

Against the backdrop of weakening demand and uncertainty around when college life may return to normalcy, it begs the question: how many of these projects will survive the pandemic? At the outset of the pandemic, bonds secured by student housing project revenues were almost unilaterally punished relative to the broader municipal market and spreads remain notably elevated compared to pre-COVID levels, as illustrated below.

While we recognize the fact that a number of privatized student housing projects will be challenged in both the short and long term, our bottom-up credit research has also helped to uncover many investment opportunities in projects that, in our opinion, have adequate liquidity reserves and strong long-term, credit fundamentals. Leveraging our own proprietary scenario analysis, we quickly identified projects we felt had the requisite funds to weather the disruption in operations.

Additionally, we identified certain unit configurations we felt were best suited in a COVID-19-impacted environment. As an example, we believe apartment-style housing will fare better than traditional residence halls. Apartments generally include private bedrooms with in-unit bathrooms and kitchens, minimizing the use of shared spaces and making them preferred candidates for social distancing.

We also prefer facilities that market primarily to upperclassmen and graduate students, anticipating a decline in first-year enrollment given uncertainty around campus reopening. Weaker occupancy rates at housing projects for first-year college students support our view.

In addition to COVID-19-related analysis, it remains critical to consider any project’s fundamental long-term economics as we look to life beyond the pandemic. We continue to place significant emphasis on the size of any facility’s target market as well as the level of both on- and off-campus competition.

We also identify projects that receive strong support from the affiliated college or university. Some schools have provided liquidity support to privatized facilities during the pandemic, either directly or through the deferral of ground rent. These actions demonstrate a strong commitment to the success of the project, in addition to providing a longer liquidity runway for the facility. A number of institutions have also reduced the number of beds of their own student housing facilities, improving demand for privatized projects.

Disruption Creates Potential Opportunities

The pandemic created immense disruption across the municipal market, particularly in the student housing sector. But with volatility comes opportunity. We feel it is too early to tell how COVID-19 will impact higher education in the longer term. Our general view is the on-campus college experience is not going away and it is possible that state budget cuts may lead to a greater reliance on P3s to finance campus infrastructure projects.

We continue to leverage the size and experience of our municipal research team to identify holdings that we believe were unfairly penalized amid the broader uncertainty, illustrating our efforts to create long-term value for our tax-sensitive clients by adeptly navigating the municipal market’s short-term challenges.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own investment professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

What Are the Risks?

All investments involve risk, including possible loss of principal. Because municipal bonds are sensitive to interest-rate movements, a municipal bond portfolio’s yield and value will fluctuate with market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the portfolio’s value may decline. Investments in lower-rated bonds include higher risk of default and loss of principal. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

______________________________________

1. Source: RBC Capital Markets, P3 Higher Education Market Overview, August 2020.

2. Source: The Bond Buyer, “P3 College Housing Down 8% in September, Developer Says,” September 2020.

3. Ibid.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments