For the first time in months, COVID-19 news took a back seat as the U.S. elections took center stage. With former Vice President Joe Biden having won the race to the White House, focus is now shifting to how the president-elect will approach the pandemic alongside the economic issues of the day. As we wrote here, with Republicans likely to retain control of the Senate, enacting substantial legislation will be a difficult task, and prospects for a large stimulus package have faded.

The U.S. economy rebounded strongly in the third quarter, fueled by a large fiscal stimulus. Incoming data shows that the economy remains in need of additional stimulus. Without it, the economy could be in for a rough winter.

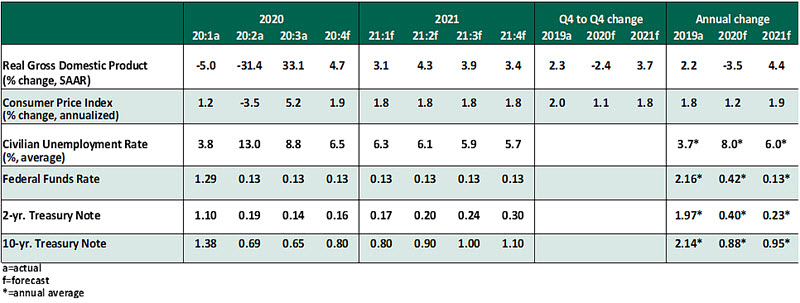

Key Economic Indicators

Influences on the Forecast

- Real gross domestic product grew by 33.1% on an annualized quarter-over-quarter basis in the third quarter as the economy reopened. Consumers and housing were powerful contributors to growth, indicating the significance of fiscal and monetary support measures in securing a rebound. That said, output remains 3.5% below pre-pandemic levels. With fiscal measures like enhanced jobless benefits concluded and infections soaring, attaining full recovery could be an uphill task.

- The escalation in new COVID-19 cases will slow the process of economic recovery. (Promising news on the vaccine front is encouraging, but full development and administration will take many months.) Income growth has slowed, and high-frequency indicators like small business credit card sales and restaurant reservations have moderated, reflecting a rapidly deteriorating health situation. We have revised our fourth-quarter growth estimate down.

- Congress failed to agree on a renewed fiscal aid package before the election, and the path to the next one will be challenging. In October, Republicans in the Senate had put forward a $500 billion proposal primarily focused on aid to the unemployed and small businesses, compared to a $2.2 trillion package advanced in the House of Representatives. While the House will remain under Democratic control, the party’s working majority has diminished. Enacting legislation will be a tricky affair.

That said, we expect both sides to find a middle ground in the first quarter of 2021 that will result in a $1.25 trillion stimulus package, half of what we would have expected under a “blue wave.”

- The labor market continues to recover. The unemployment rate fell from 7.9% in September to 6.9% in October, a much larger improvement than expected. While the headline numbers were positive, all isn’t well underneath the surface. The economy has reclaimed 12 million jobs from the trough of the crisis in April, but total employment is still 10 million below pre-pandemic levels. The labor force participation rate increased slightly but remains near its lowest level since the 1970s. We expect the labor market to continue to recover, but only gradually; full employment is still quite a way off.

- Inflation should not be a major concern. Prices have firmed recently, led by virus-sensitive categories and base effects stemming from sharp declines in the early stages of the lockdown. But lingering economic and labor market slack will keep consumer prices below target this year and next.

- In line with expectations, the Federal Reserve maintained its monetary policy stance this month. The FOMC acknowledged slowing economic activity and reaffirmed its dovish forward guidance. Fed Chair Powell reiterated the need for more stimulus. We expect the Fed to keep interest rates at their effective lower bound well beyond next year but could be forced to increase asset purchases, particularly in the absence of sizeable fiscal support.

- The housing market is one of the few bright spots of the economy amid record low mortgage rates. Even though early signs of cooling off have emerged, in lower levels of pending home sales and mortgage purchase applications, there’s plenty of steam left in this engine of growth. Single-family housing starts are still above pre-COVID levels and existing home sales are running at their highest pace since 2006.