The renewed global resurgence of COVID-19 demonstrates that the virus remains the largest risk to every economy’s outlook. The widespread nature of the viral surge shows that many nations that had appeared to have mitigated the virus remain at risk for great economic and physical harm. Lockdown measures are likely to push most European economies back into contraction and put a dent in the recovery around the world, even in places with no new restrictions.

Vaccine developments have cheered markets, but the many months required for approval, production and dissemination of vaccines will prevent a rapid recovery. In the near term, the global economy will continue to live with the virus as best as it can.

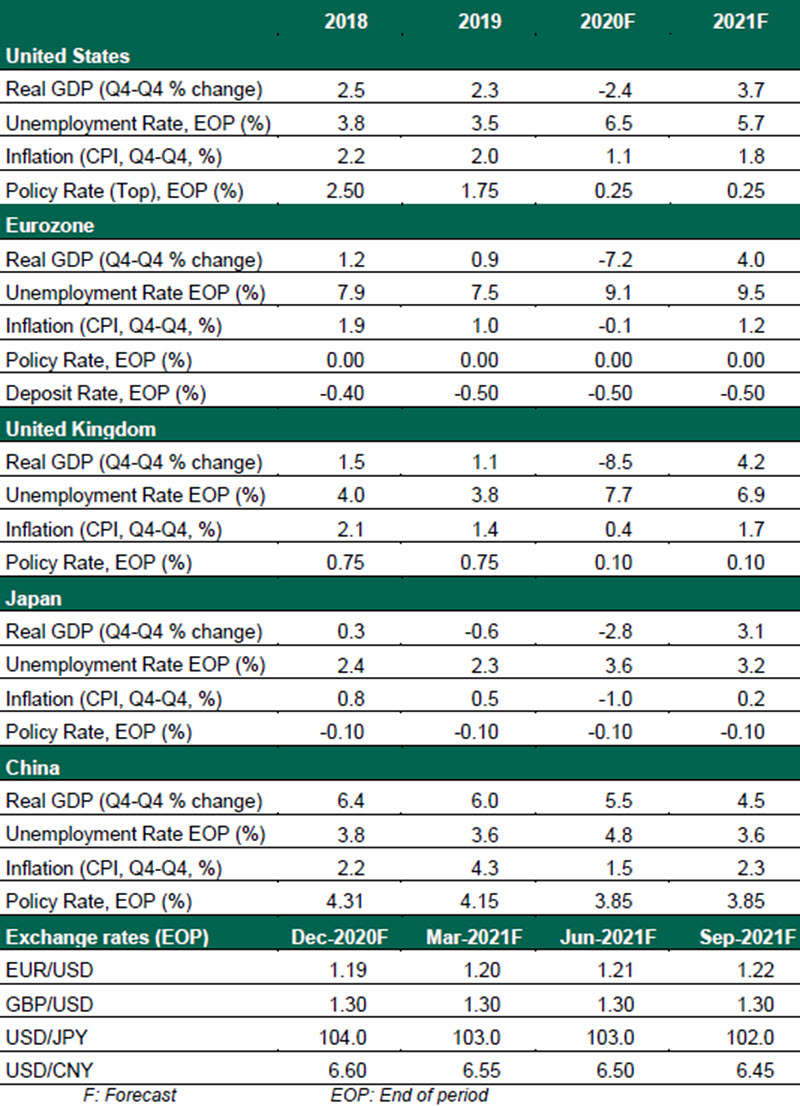

The following are our views on how major world markets will fare during the balance of this year and next.

United States

- With former Vice President Joe Biden the winner in the race for the White House, focus has now shifted to how the president-elect will approach the pandemic alongside other domestic and foreign policy matters. While the prospect of gridlock between the Senate and the House on important legislation has cheered markets, it may not be the best outcome for the economy.

- America is witnessing a renewed outbreak in COVID-19, prompting localized restrictions on activity. After record economic activity recorded in the third quarter, there are growing signs that the economy has again started losing momentum. In our base case, the surge in fresh COVID-19 cases along with fading fiscal support will slow the economic recovery, but not derail it. A stimulus package will likely be passed in the first quarter of 2021 that should soften the hit to the economy.

Eurozone

- As we recently discussed, the eurozone is at risk for a double-dip recession. The region has long been in an economically unsteady state, starting the year on the cusp of recession even before facing COVID-19. New widespread and strict lockdown measures across many nations will keep consumers home, likely driving growth negative for a brief interval. But this lockdown should be less severe in its consequences than the dramatic downturn seen in spring, and 2021 is poised for a return to growth.

- At its October meeting, the European Central Bank (ECB) stated that it would “recalibrate its instruments,” previewing an expansion to the asset purchase program likely to be announced at its December meeting. While quantitative easing is helping to maintain financial stability, each additional dose of this medicine depletes the ECB’s ability to provide stimulus to a liquidity-flooded market.

United Kingdom

- In response to its own viral surge, the U.K. government implemented a four-week national lockdown, which may be extended beyond the December 2 expiration. The renewed restrictions come as a particular disappointment to a nation that imposed a delayed but long-lasting set of controls in the initial wave, and we expect Britain to track the eurozone into a brief near-term recession. However, the government is responding: Chancellor Rishi Sunak announced an extension to the furlough scheme through March 2021 with expanded eligibility. The Bank of England has committed to a greater volume of bond purchases to support fiscal conditions, a tool that should prove more effective than the proposal to take its policy rate negative.

- Brexit negotiations with the European Union continue. We expect COVID-19 will force negotiators to find a way forward; governments will not create a second, self-imposed crisis under these circumstances. However, the deal will likely come late in the game, still creating a risk of border disruptions and fueling more uncertainty.

Japan

- Japan is managing COVID-19 better than most developed markets, but its economy has yet to show a similar state of improving health. Over the past month, key indicators like industrial production and the manufacturing purchasing managers’ index have improved, but remain in contraction.

- The transfer of power from Abe Shinzo to Suga Yoshihide has thus far been smooth. The new prime minister has committed to maintaining Abenomics, especially fiscal stimulus: employment subsidies have been extended, as have support measures for businesses and the health care system. The fate of the delayed 2020 Summer Olympics remains a substantial uncertainty surrounding the outlook for the new year.

China

- China’s recovery from COVID-19 continues at a strong pace, with viral outbreaks limited and manufacturing surging. The country logged its highest single month of exports to the world in October, making up for pent-up demand as supply chains worked through their past disruption. However, with the rest of the world at growing risk of a renewed recession, the potential for more export-driven growth is limited. Household consumption continues to recover slowly, which drove a lower-than-expected reading of third quarter output.

- At its fifth plenum, the Chinese Communist Party released a five-year plan that called for “more sustainable,” “higher-quality” growth, focusing on innovation rather than raw production. China recognizes it may face ongoing export headwinds. The election of Joe Biden has raised the risk of a more unified global front against China’s trade practices.

Global Economic Forecast – November 2020

© Northern Trust

Read more commentaries by Northern Trust