U.S.-China Outlook, Fed’s Programs Ending, Presidential Authority

SUMMARY

- China Should Not Celebrate The Election Results

- The Fed Is Losing Some Key Tools

- Power of the Presidency

In 2016, when President Trump was running for his first term, he promised to “stand up to trade cheating,” a reference to America’s trade agreements (or lack thereof) with other nations. On his very first day in office, he withdrew the United States from the Trans-Pacific Partnership and set out on a course marked by escalations in economic tensions with almost every American trading partner.

China has been a particular source of the president’s ire. While Beijing has thus far treaded with caution about the election results, one could certainly imagine Chinese officials being pleased with the outcome. But they’re unlikely to get a better deal from Biden.

President Trump is certainly not leaving quietly, and this applies to his posture on China. Chinese companies have often downplayed their links to the government, but a rising number of companies writing Communist Party into their charters and paying homage to its leader has been a concern for Washington. Last week, the White House issued an executive order banning U.S. investors from holding shares in 31 Chinese firms identified as “Communist Chinese military companies.”

As discussed in the final segment of this week’s commentary, the use of executive authority is not new to U.S. politics. But it is the first time that an executive order has been issued blocking American investors from purchasing Chinese securities, inclusive of exchange-traded or mutual funds that include those securities.

Beijing hasn’t retaliated yet and is unlikely to do so in the near term, preferring to await the transition to a new administration. An aggressive reciprocal retaliation would only hurt confidence in China’s own financial sector.

The order has not delivered an immediate shock to markets, given its phased-in implementation. The ban will come into effect on January 11 and gives investors until November 2021 to divest their stakes. That said, it will likely deter investments into Chinese entities, wiping off billions of dollars in market value. In an earlier example, U.S. blacklisting of Huawei led to a significant loss of business for the company, and led other countries like the U.K. to follow suit. The company reported a $12 billion revenue shortfall in 2019.

This week’s action could create compliance problems for investors, particularly considering the significant presence of Chinese entities in U.S. markets (see above chart). According to Treasury data, U.S. residents currently hold about $238 billion of Chinese corporate stocks.

The ban sends a clear message that the president is now less concerned about upsetting the stock markets, an indicator that he has often relied upon to gauge his economic policies, and he will continue to target Beijing’s interests before leaving office. Further measures could include export controls involving key technology sectors like semiconductors, drones and companies on the Department of Defense list, which will cause further pain to Chinese corporations.

“Chinese corporations have a significant presence in the U.S. markets.”

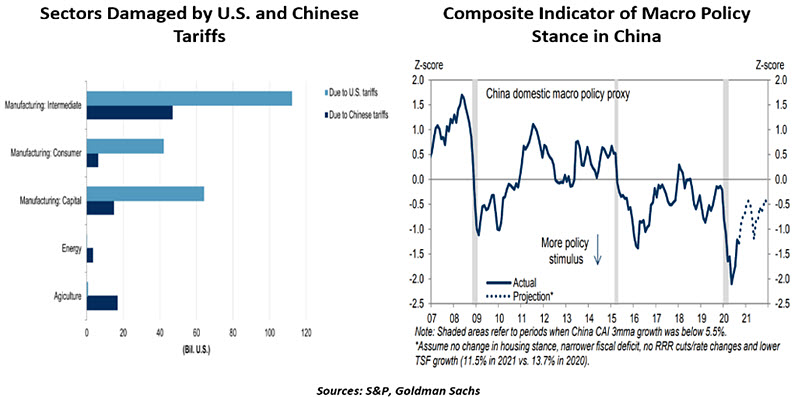

Studies show that the trade war has cost the U.S. economy nearly 300,000 jobs, up to 0.7% of gross domestic product and over $45 billion in tariffs paid by American corporations. Uncertainty has pushed businesses to postpone or cancel their investment plans. Research shows that U.S. firms lost at least $1.7 trillion in market capitalization due to increased U.S. tariffs on Chinese imports. China, too, has suffered significantly. According to Goldman Sachs, the initial rounds of tariffs (implemented before August 2019) reduced Chinese gross domestic product by 0.4%, leading to more policy interventions. Manufacturing has been the biggest casualty on both sides.

The trade war hasn’t caused a structural shift in Chinese policies or supply chains yet; reconfiguring value chains is a slow and expensive process. But it has pressured China to give in to some U.S. demands. Chinese exporters have lost business to alternative suppliers like Taiwan, Vietnam and India, and their exports fell by about $25 billion in the first half of 2019. In the “Phase One” deal, China committed to buying $200 billion more in goods from the U.S. across sectors including politically sensitive agriculture, services, manufacturing and energy.

According to White House estimates, intellectual property theft costs the United States between $200 to $600 billion a year. In the Phase One deal, China also gave concessions on the treatment of foreign interests in the country. China promised not to force U.S. corporations to hand over technology as a condition of doing business and will refrain from directing its firms to obtain sensitive foreign technology through acquisitions.

The incoming president will have the executive power to repeal some of his predecessor’s orders. However, it will be difficult to undo measures targeting China’s economic and strategic might without appearing to be soft. Conventional wisdom about free trade has quickly grown hawkish, and any action that helps China may face strong opposition, even within the new administration.

“U.S.-China decoupling will accelerate before slowing under the Biden administration.”

During the election campaign, both candidates shared a protectionist bent. President-elect Biden pledged to put American goods and workers first and take a strong stance against China’s trade practices. Biden’s “Buy American” agenda talks of allocating $400 billion for federal government purchases of American-made goods and has indicated his unwillingness to negotiate any trade agreements until significant investments are committed to U.S. manufacturing. The new administration would also seek to bring supply chains back to America.

On the other hand, Biden has pledged to re-embrace traditional allies and adopt a less isolationist approach to trade. Indications (like recommitment to the U.S.-Japan security alliance) are that he will focus on working more closely with America’s allies to apply further pressure on China.

Biden is unlikely to roll back tariffs without any major concessions from China on contentious issues covering intellectual property and state aid for businesses. We would regard it as progress if trade negotiations were to become more deliberate, repealing steel and aluminum tariffs placed on U.S. allies and allowing the world to focus on China’s trade practices.

This all means that the majority of tariffs against China appear likely to stay in place. U.S.-China decoupling will likely continue until both countries feel compelled to return to the negotiating table. Costs will continue to accrue on both sides.

While Biden likely wouldn’t be referred to as the “tariff man”, he certainly wouldn’t be named a “Davos man” either. Fair trade over free trade will remain the central theme in Washington.

Separation Anxiety

The pandemic has certainly tested the strength of some relationships. Family lawyers report a surge in business, as too much togetherness takes its toll.

In Washington, a relationship that seemed strong has apparently ruptured. Throughout the year, The Treasury Department and the Federal Reserve worked closely to engineer stable markets and a durable economic recovery. The Fed has been purchasing copious amounts of government debt to support relief programs, while the Treasury provided more than $200 billion of capital for a series of Fed programs that made over $1 trillion in credit available.

This week, however, Treasury Secretary Steven Mnuchin announced that the Treasury would be taking its money back at the end of the year. The programs it supported are scheduled to sunset on December 31. Fed officials have expressed disappointment at the decision.

To be sure, only a fraction of capacity in the Fed’s special lending programs has been used. As an example, the Municipal Lending Facility (MLF) was designed to provide credit to state and local governments unable to access the capital markets on reasonable terms. At the end of October, only two obligors had taken advantage of the program, borrowing a total of $1.65 billion. The MLF has a ceiling of $500 billion.

The design of these programs bears some responsibility for the paucity of demand. The Fed is restricted by its charter to lend only when a loss is not expected. To meet this standard, the rates charged by the Fed have been high, and banks originating loans for some programs are required to bear the risk of loss up to a certain point. The Fed has adjusted terms on a number of occasions this year, but has not been successful in generating additional activity.

The small take-up on Fed facilities has led to questions about whether the money invested by the Treasury might be otherwise deployed. This tactic is not without precedent: during the 2008 financial crisis, Congress passed the Troubled Asset Relief Program (TARP), which was originally intended to purchase distressed securities. When that effort proved slow to launch, policymakers pivoted to use TARP funds to recapitalize banks.

This is not a step to be taken lightly. While the value of loans made and bonds purchased under the Fed’s facilities is modest, the signaling value of the programs has been substantial. Credit market function began to improve immediately after the Fed’s backstops were announced, allowing a number of corporations and public sector borrowers to raise money in the capital markets. (2020 will be a record year for corporate debt issuance.)

Further, the ability to purchase corporate debt and exchange-traded funds has provided the Fed an avenue it did not have before, and which it could conceivably employ to stimulate economic activity if needed. At a time when liquidity traps are limiting the effectiveness of many monetary policy tools, this program represents an interesting alternative.

“Usage is an incomplete measure of how effective Fed programs have been.”

As with most other things in Washington, politics are playing a hand in this process. Current leaders are concerned about how new leaders might reallocate the money; the current cast apparently does not want to give the incoming administration any latitude. The Fed would need Congressional action to re-establish the programs next year, cooperation which is not assured.

Sustaining financial stability is a goal that should attract bipartisan support. With some potentially difficult months ahead, that goal could be tested again. If that happens, the Fed may not have the tools it needs to respond.

Judge, Jury, and Executive Order

The absence of a “blue wave” election outcome has led to a reassessment of the potential of a Biden presidency. With the two parties sharing few legislative priorities, a divided government is likely to lead to gridlock. While the prospects for substantial legislation have dimmed, we cannot ignore the power of the president to pursue policies directly, including by executive order (EO).

Article II of the U.S. Constitution charges the president to “take care that the laws be faithfully executed,” granting wide discretion over the operation of the federal government. Presidents have used this authority to take action when Congress has not advanced presidential agendas or has shied away from divisive issues. Every president has issued EOs: Franklin Roosevelt holds the record at 3,721 orders, an average of 307 executive orders per year of his presidency.

“Presidential power has gradually expanded.”

Subsequent presidents have issued fewer orders, but they were often of greater consequence. President Eisenhower desegregated schools and President Kennedy codified “affirmative action” by executive order. President Obama came under fire for using EOs to change immigration and environmental policies.

Most of President Trump’s contentious policies came through EOs and other presidential authority. Implementing tariffs, leaving the Paris climate accords, withdrawing from the World Health Organization, and restricting immigration were all unilateral executive actions. As these were not acts of Congress, the incoming president can rescind them with the stroke of a pen.

In many cases, president-elect Biden is likely to quickly change course; we see only the China tariffs as likely to persist. The new administration may seek to execute orders on other fronts: proposals to forgive some portion of student loans, heighten environmental regulations and encourage immigration have already sparked debate over how much the next president will be willing to do on his own.

Though a Biden administration will have little in common with the Trump agenda, reliance on EOs is likely to continue. The blue wave did not appear, but the blue ink will still flow.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.