Franklin Small Cap Value Fund Assistant Portfolio Manager and Research Analyst Nick Karzon gives five reasons why we continue to see attractive long-term opportunities for select small-capitalization (small-cap) P&C insurers.

Following relatively strong performance over a trailing five-year period (2015-2019) during which P&C insurance companies in the Russell 2000 Value Index outperformed both the broader index and the financial services sector, the group has been a relative laggard year-to-date.1

In our view, recent underperformance is attributable to lower interest rates as well as multiple risk factors, which have generated elevated loss claim activity across the United States. These factors include the COVID-19 pandemic and related business interruption claims in addition to hurricanes, floods and wildfires.

Here, we outline five reasons why we think the long-term investment opportunities outweigh near-term risks for select small-capitalization (cap) P&C insurers, which remain attractive investments for our strategy.

Reason #1: Alignment in Focus on Risk-Adjusted Returns

The Franklin Small Cap Value Fund’s process is built on investing in businesses that we view as having a track record of success, low leverage and attractive risk-adjusted returns, which we discussed in greater detail in a prior post. Consequently, while we look for potential upside in investments, we also spend considerable time evaluating downside risk.

We have found that P&C insurers typically take a similar approach to capital management with conservative asset allocation strategies, while managing outsized underwriting or liability risk through reinsurance. Our research shows typical asset leverage is only 3-5x tangible equity, which is well below banks or life insurers, and investment portfolios are primarily comprised of investment-grade fixed income securities. On the liability side, insurers mitigate the risk of large losses through reinsurance contracts designed to redistribute exposure to catastrophic loss events.

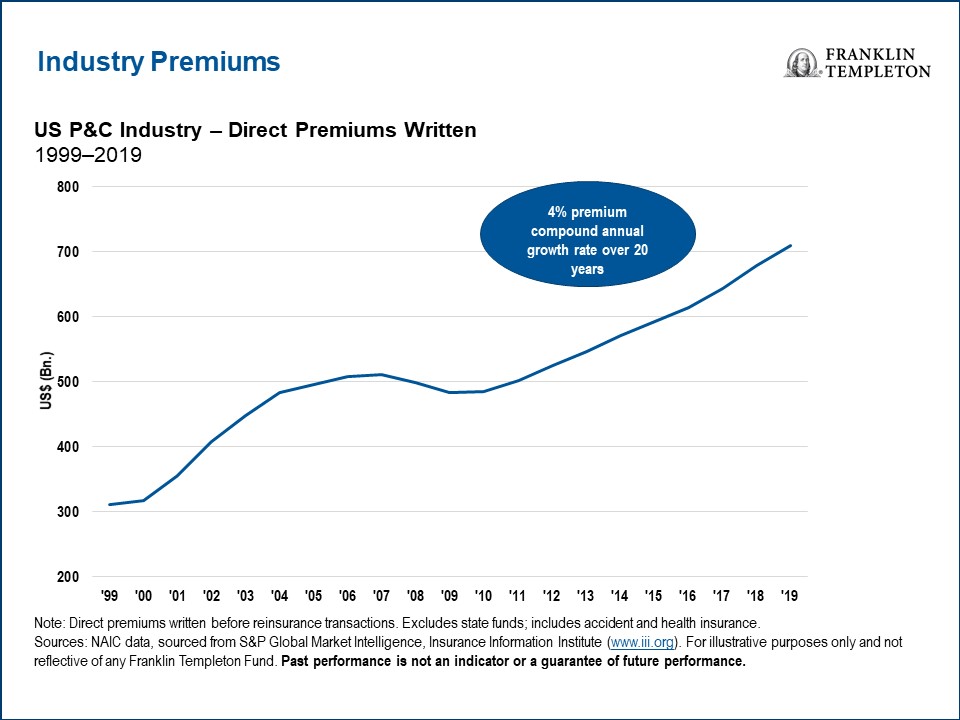

Reason #2: P&C Insurance Is a Growing Essential Industry

The P&C insurance industry’s function is to protect against risks to property, people and businesses with coverage often mandated—making it an essential industry. As the US economy and population grow, demand for protection also rises.

As the chart below shows, premiums in the US P&C industry have grown at a mid-single-digit pace over the past 20 years.2 While exposure can shrink during a recession as unemployment rises and activity declines (e.g., fewer commercial auto miles driven), the greatest annual reduction in premiums during this period was just 3% in 2009.3 Current pricing trends suggest to us that even with a moderate decrease in exposure in the near term, industry premiums are likely to grow over the medium term.4

Reason #3: Disciplined Approach to Pricing

According to our analysis, the P&C insurance industry focuses on return on equity, and companies have taken a disciplined approach to product pricing. If an insurer’s return outlook is challenged (e.g., rising loss cost trends or lower investment returns), it can raise pricing to return profitability to its targeted level.

In the last few years, we have observed commercial insurers respond with accelerating rate increases to address rising loss severity trends, elevated levels of catastrophe losses, and now lower interest rates. While these factors may manifest themselves in lower near-term earnings, we believe insurers will utilize price increases to offset these potential headwinds over the medium term.

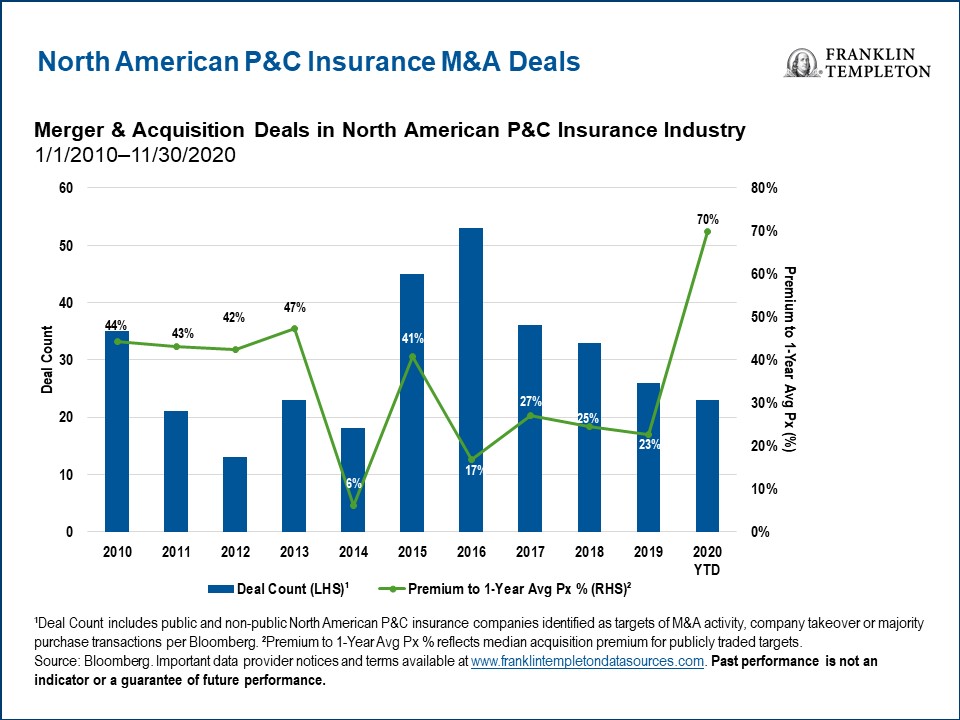

Reason #4: Industry Consolidation

Merger-and-acquisition activity has been an ongoing industry theme and is likely to continue in our view, with strategic rationales including geographic expansion, enhancing distribution, increasing scale and growing product level expertise. While we do not embed merger-related upside into our base-case analysis, our research shows recent acquisitions of publicly traded insurers have occurred at healthy premiums.

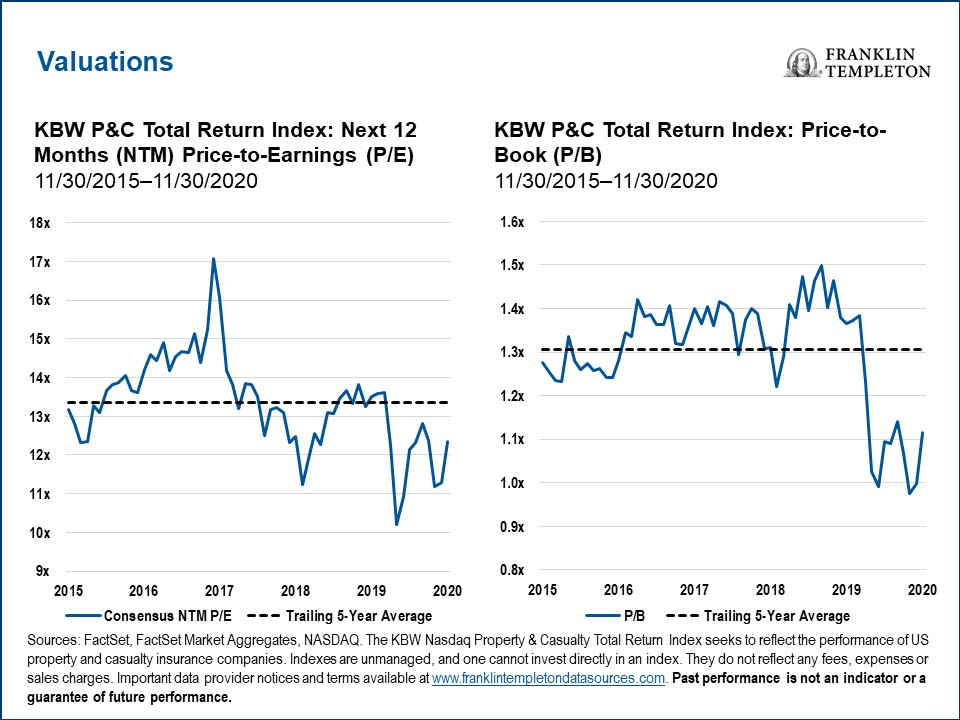

Reason #5: Valuations

Over the course of 2020, valuations for P&C insurers as a group have dropped below five-year averages on both a price-to-earnings and price-to-book basis. While this may be attributable to some of the risk factors identified above, we find the risk-return profile attractive at these levels, given our favorable outlook on industry fundamentals.

Investment Implications

We view a select group of small-cap P&C insurers as compelling investment opportunities despite recent underperformance given strengthening fundamentals and our outlook for attractive risk-adjusted returns at the stock level. We see these companies as well-positioned due to disciplined underwriting, especially with regard to weather-related catastrophe exposure and the utilization of standardized viral exclusions (a key mitigating factor for business interruption claims) within most property policies.

The COVID-19 pandemic, macroeconomic fallout and coincidental decline in interest rates have created significant near-term uncertainty within the financial services sector, and the P&C insurance industry is no exception. While our current outlook on P&C insurance is favorable, we remain observant of both industry and stock-specific factors that could alter this view.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Sources: Bloomberg, Russell Indices. Frank Russell Company is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. Important data provider notices and terms available at www.franklintempletondatasources.com. Past performance is not an indicator or a guarantee of future performance.

2. Source: S&P Global Market Intelligence. Important data provider notices and terms available at www.franklintempletondatasources.com.

3. Ibid.

4. There is no assurance any forecast, projection or estimate will be realized.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments