The Times Are a Changing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSome changes unfold over time and it’s possible to see them coming. There are demographic changes coming in the next decade that will change the direction of the U.S., since the Silent generation and the Baby Boomers hold a different view of government than Gen Z’s and Millennials. According to a poll by Pew Research two years ago, those in the Gen Z and Millennial generation believe by a wide margin that government should do more in addressing societal problems, when compared to Baby Boomers and especially members of the Silent generation. In the 2024 election the number of eligible Gen Z and Millennial voters will equal the number of Baby Boomer and older voters, and in the 2028 election outnumber them handily. As more Millennials are voted into power in local, state, and national elections, they will shape the legislative agenda, direction, and role government will play in managing the economy and solving many of the problems that have become so divisive.

The financial crisis disrupted the lives of Millennials significantly as many found it difficult to get a good job after graduating from college burdened with more student loans ($497 billion in 2019) than any prior generation. The impact is that Millennials have purchased their first car, gotten married, and welcomed their first child later than previous generations. They question the value of capitalism since it hasn’t helped them as much as their parents. They are too young to grasp the Fall of the Berlin Wall in 1989’s meaning, or the short comings of socialism. When they tune into the news on social media all they see is dysfunction and disorder, with many accepting the narrative that too many working people are receiving too little of the economic pie, since that has been their experience. The influence of the progressive movement within the Democratic Party was small in the 2020 election, but it will gain traction in coming years and exert a greater influence. Demographics suggest that the U.S. will move to the left politically in the next decade. Some may not like that outcome, but it’s better to see this shift coming since it will have an impact on the economy and financial markets. Some of the coming changes will be good and some of the changes will have negative unintended consequences, just like every demographic shift that has developed since 1776.

Millennials and GEN Z’s will vote for candidates in coming elections that promise to do more to address many of the problems that have built up in recent decades. The solutions will require more federal spending and ongoing deficits, and Congress is likely to turn to the Federal Reserve to use its balance sheet to fund initiatives as discussed in the October Macro Tides. “The concept of Modern Monetary Theory (MMT) is discussed as if it is something that may happen in the future. The evolution of monetary policy since 2002 and how the Fed has used its balance sheet during the Pandemic indicates that MMT is already in place. The Federal government can run huge deficits knowing the Federal Reserve will be the buyer of first resort. And after remitting the interest income the Fed has received back to the Treasury, keep the government’s borrowing costs extremely low. Politicians won’t be able to resist spending more to address all of the U.S.’s special needs. So funding $1 trillion for an infrastructure program or funding a modest $3 trillion Universal Basic Income program to narrow the income inequality gap could easily be on the table. According to the Congressional Budget Office (CBO), funding for the Highway Trust Fund will be depleted in 2021, the Medicare Hospital Insurance Trust Fund Part A will run out of money in fiscal 2024, the Social Security Disability Trust fund in fiscal 2026, and Social Security could run dry in 2032 or sooner. It is unlikely politicians will vote to lower disbursements for these trust funds, especially for Medicare and Social Security, nor will tax increases prove sufficient since they would be too steep for the economy to bear. Politicians are likely to turn to the Federal Reserve to keep funding these programs. The Fed will learn that sometime around 2002 the Fed checked into the Hotel California of extreme monetary accommodation will never be able to leave.” Congress will need the Feds assistance since no matter how high Congress increases taxes for the top 1% or even the top 5%, it won’t generate enough revenue to equal the coming increases in government spending.

In 2021 there will be Republican members in the Senate and House who will express their deep concerns about budget deficits and the rising tide of debt that promises to be an albatross around the neck of coming generations. If Republicans manage to hold onto the Senate, after gaining 12 seats in the House in the 2020 election, they may have enough leverage to shave a few billion off spending bills. The Republican leadership will have their eyes focused on the midterm elections in 2022 and fiscal austerity is not likely to be a winning message, if Republicans realistically expect to regain a majority in the House and Senate. Republicans will run on how they reined in spendthrift Democrats from spending too much, and then agree to smaller increases in spending. Republican spending discipline will look like a 1 foot wall of sandbags protecting us from the coming mandatory spending tsunami.

Anticipated and Unanticipated Changes

While some changes can be anticipated, others can’t as they unfold more quickly and often as a result of a major event. World War I and World War II each altered the course of history and spurred changes that couldn’t have been foreseen. COVID-19 has forced societal changes that will persist long after the Pandemic ceases to make headlines. Some of the changes simply accelerated changes that were already unfolding. An increasing number of consumers were shopping online before COVID-19, as E-Commerce sales rose from less than 0.8% in 2000 to 10.8% at the end of 2019. In the second quarter of 2020 E-Commerce sales soared to 16.1% of total sales, an increase of almost 40% virtually overnight. The trend in E-Commerce sales will continue to rise from a higher plateau. Shopping online for everyday goods like groceries has become entrenched for not just Millennials but for every generation. A recent survey by consulting firm McKinsey & Co. found that about three out of four people have tried a new shopping method due to the Pandemic and that more than half intend to continue using curbside pickup and grocery-delivery services after the pandemic is over. Many businesses have stepped up their digital services to make it easier for consumers to access products and services. In order to survive restaurants have expanded curbside pickup and deliveries as more consumers have grown to like eating at home without having to cook. When COVID-19 has become a memory, people will return to the Mall and shop a bit less online, but never at the levels that existed BC (Before Covid-19).

The percent of employees working from home climbed from 3.3% in 2000 to 5.3% in 2018. As states enacted lockdowns in mid March, the percent of employees working from home soared to 51% in April, according to Gallup. In a September 24-27 poll the percent of workers always working from home had fallen to 33%, with 25% saying they sometimes did, and 42% reporting they never worked from home. Many technology firms have announced they will keep the majority of their workers at home until next summer. The percent of employees working from home will fall after the vaccines have been widely distributed in the second half of 2021. The percent of hours worked at home will remain far higher than before the Pandemic made it possible for companies and employees to learn what was possible.

The shift to working at home accelerated an existing trend but created other changes that were difficult to foresee. The first wave of COVID-19 was concentrated in the northeast and predominantly in New York, while the second wave hit cities in Arizona, Texas, and Florida hard. Densely populated areas in these and other states led those who could move out of cities and into the suburbs to do so. The ability to work from home made this change possible. For many workers not having to go into an office meant they didn’t have to live in or near downtown. The high cost of living in most major metropolitan areas forced many renters to live in a smaller apartment. If one was commuting to work every day, there wasn’t a need for an extra bedroom or space for a home office. The prospect of spending much more time working from home in a cramped apartment caused an exodus out of cities to the suburbs. The extra money provided by the federal government ($1,200 per person) covered the cost of the move and allowed many to get more space for the same amount of monthly rent or less. As more apartments became available in cities during the summer, rents began to fall. Rents in many cities are now down by -5%, with more declines likely. In high priced cities like San Francisco rents are falling sharply. In August the asking rent for an apartment fell -6% from the prior month to a still mind boggling $3,400, and is now down over -20% from August 2019. The story is much the same in New York where the median rent in Manhattan in September was -7.1% less than a year ago. The number of empty apartments has soared from 5,600 in August 2019 to 15,923 leaving the vacancy rate at a record high of 5.5%. The average rent for a one bedroom apartment is now down to just $3,445. In Chicago the average rent for an apartment is down -7.98%, while the rent for a one bedroom apartment is down -9.6%. Apartment values in major cities will fall as the cash flow from rents lower their valuation. This could become a problem in the next year or so for overextended landlords and lenders. Rents in suburban areas have rebounded after dipping in the spring, as the rising demand from those moving out of cities allowed suburban landlords to increase rents.

For the majority of workers in major cities who are unable to work from home, can’t afford to move, or whose family ties are simply too strong, riding mass transit is how many get to and from work. Owning a car in a major city is expensive so many have no choice but to rely on mass transit for transportation. The prospect of riding on the subway or on a bus during a pandemic caused a lot of people to decide they needed to buy a car. Those who moved to the suburbs suddenly found they needed a car or a second car for errands in the suburbs. After peaking in 2014 used car and truck prices fell sharply in 2016 and 2017, as a torrent of cars came off three year leases, before stabilizing in 2018 and 2019. The net result is that COVID-19 caused the demand for used cars to sky rocket in the last four months lifting used car and truck prices by more than at any time since 1969.

Mass Transit in Crisis

COVID-19 has caused a huge decline in the use of mass transit across the country and especially in New York, which was devastated last spring. Ridership on subways and buses hasn’t recovered and the current surge in cases isn’t helping. As of November 12 the number of people using the subway is down more than -65% with a greater than -50% decline in bus riders.

The decline in revenue from mass transit in New York and across the country is contributing to large losses for many cities. An independent analysis commissioned by the American Public Transportation Association (APTA), a non-profit advocacy group, found that, even after the $25 billion included in the CARES Act for public transportation relief, public transit agencies nationwide still face a $23.8 billion shortfall through the end of 2021. The budget shortfalls many cities are facing are likely to result in cutbacks in public transportation. The rebound in ridership will be stunted by lingering concerns about COVID-19 until the vaccines eradicate COVID-19. Those who can now work from home or have a used car are not likely to return en masse to riding the bus or subway. According to the APTA non-white Americans make up less than 40% of the U.S. population, but comprise 60% of transit riders. During the height of the COVID-19 crisis in New York, 67% of essential non-white workers - doctors, nurses, and kitchen staff - relied on mass transit to get to the hospital and home. The coming budget cutbacks will disproportionately hurt those who depend on mass transit to commute to work and around many major cities.

Another Housing Boom

The exodus out of major cities wasn’t restricted to former apartment dwellers finding a larger apartment in the suburbs, but also included a wave of people who wanted to buy their first house, and existing home owners who found they required a larger home, if they were going to work from home far more than in the past. The U.S. Census Bureau reported that in October New Home sales were 1,179,000 up 29.4% from 726,000 in 2019. (Chart compliments of Doug Short Advisor Perspectives.com) Despite the surge, New Home sales are still -9.3% below the July 2005 peak of 1.3 million. According to the National Association of Realtors, Existing Home sales were up +26.6% from September 2019 and totaled a seasonally adjusted rate of 6.86 million. Existing home sales are -5.5% below the peak in 2005.

Housing has been a major source of strength since April and has contributed to the rebound. New home construction represented about 22% of housing activity in October and adds 3% to 5% to GDP. New home owners will often purchase new furniture, fixtures, and appliances, especially if they have moved into a larger space. The range of 3% to 5% also includes the remodeling of existing homes. With time on their hands and extra money from the government in their pockets, home owners have made many trips to Home Depot and Lowes since April, as they embarked on major upgrades to their home. Rent payments and utility payments, which are fairly stable adds another 10% to GDP. Even though unemployment remains high, record low mortgage rates have made housing affordable, but that is changing.

The surge in demand for existing homes has collided with a record low level of homes for sale. There were 1.42 million existing homes on the market at the end of October, down -19.8% compared to October 2019. At the current sales pace, that represents a 2.5-month supply, the lowest on record. When sales were last at this level in February 2006, the supply of homes for sale was twice what it is now. The mismatch between the supply of homes for sale and demand has led to a big jump in home prices. According to the National Association of Realtors (NAR), the median price of an existing home sold in October was up +15.5% from October 2019 at $313,000. The increase in home prices was broad based as the median price for existing homes in each of the 181 metro areas tracked by the National Association of Realtors was higher in the third quarter from a year earlier. This is the first time since 1980 that every metro area tracked by NAR posted an annual price increase in the same quarter, with more than 60% of the areas posting a double-digit gain.

Home price appreciation has far outstripped the increase in wages during the last decade. The average annual increase in wages was less than 2.5% in the years following the financial crisis, although wage growth picked up in 2018 and 2019. In comparison home prices consistently rose at a faster clip than wages. The gap between home prices and Hourly Earnings has widened significantly since 2012 and is approaching the levels that last developed in 2006.

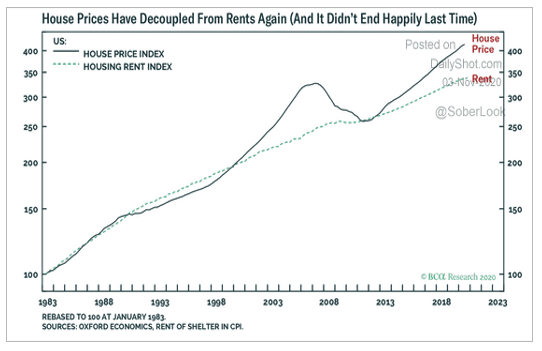

There has been a good correlation between the cost of renting and home prices. This makes sense since changes in rents supports the amount of money a home buyer would allocate to a mortgage. From January 1983 until 2002 home prices and rents moved higher in lock step until they began to diverge. The spread between home prices and rents continued to widen as the Federal Reserve kept the federal funds rate low, innovative mortgage products took full advantage of lax lending, and a wave of home speculation fueled the housing bubble. The gap between rents and homes prices was closed after home prices fell -34.4% based on the S&P/Case-Shiller home index in 20 major cities. Home prices have been rising faster than rents since 2012 causing the gap between home prices and rents to become stretched. The gap widened more in 2020 as home prices soared and rents fell in major cities.

The significant increase in home prices since April 2020 has lowered the Housing Affordability Index (HAI) by more than -7.0%, so fewer Americans can afford to buy a home. The HAI ticked up to 159.6 in September from 158.9 in August as mortgage rates edged lower. Mortgage rates are likely to remain low until the vaccines allow for a more complete return to normal and a broad based improvement in economic growth. Although the Federal Reserve has indicated it will keep the federal funds rate low for years, the Treasury market may not have the same level of patience. There is a 4-year cycle in the 30-year Treasury bond that timed trend changes in 2000, 2004, 2008, 2012, and 2016. As discussed in the August 10 WTR and the September Macro Tides, this cycle suggested a trend change was likely in 2020. “The 30-year Treasury yield has established a high or low every four years since 2000. In 2000 and 2004 a high in yield was recorded while an important low was reached in 2008, 2012, and 2016. This suggests it is wise to be on the lookout for a potential low in the 30-year Treasury sometime in 2020. Even if a low develops, the initial uptick may be modest.” Since September the yields for 10-year and 30-year Treasury bonds have drifted upward by 0.15%. Not enough to cause mortgage rates to move up, but the four year cycle may become more apparent in 2021 as economic growth improves and inflationary pressures build. There is a high level of complacency in the Treasury bond market since investors are comforted by the Fed’s commitment to keep buying Treasury bonds. But the bond market has been known to throw a tantrum and 2021 may provide the right ingredients for another outburst.

An indication of how strong the move to buy an Existing home has been is evident in how sales are bucking what is normally a weaker seasonal period. In the last seven years seasonally adjusted home sales peaked in June and then fell by 15% to 20% in September and October likely due to the beginning of the new school year. In 2020 home sales topped in July but have held up remarkably well in September and October. As long as mortgage rates behave in coming months the surge in housing can weather the decline in affordability due to price appreciation. The test may come in the second or third quarter of 2021 (or sooner), after the distribution of the vaccines allows consumers to unleash a wave of pent up spending.

The imbalance between supply and demand driven by COVID-19 will moderate in 2021. In 2020 the supply of homes for sale dropped to a record low as home owners didn’t want prospective buyers who might be infected walking through their home. As a vaccine becomes widely available by mid 2021, more home owners will be comfortable in putting their home up for sale which will increase supply. The fear of living in a densely populated city prompted a surge in demand for homes and apartments in the suburbs. This fear will fade as people become confident that the vaccine will control the spread of COVID-19 in cities. The dramatic increase in employees working from home will moderate by the middle of 2021. More employees will spend less time working from home and more time in the office, so the need for more home space for work will diminish. The number of people moving out of cities will slow, which will also dampen demand for larger homes in the suburbs. When prospective city dweller movers compare the cost of renting to buying, the decline in rents and higher home prices will persuade many to stay put. All of these factors will contribute to a slowing in the appreciation in home prices by mid-2021, and by the end of 2021 there will be some areas that will experience small declines.

Housing Bust Not Likely

It would be easy to compare how detached home prices have become to wages and rents in 2020 with the housing bubble in 2006 and conclude that another broad decline in housing prices was coming. For a number of reasons that would overlook meaningful differences between now and in 2006. Record low mortgage rates have enabled existing home owners the opportunity to refinance their mortgage and lower their monthly payment. The Household Debt Service and Financial Obligation ratio includes mortgages, Home Equity Loans, auto loan payments, and credit card interest. The ratio is calculated as the percent of aggregate required debt payments (interest and principal) to aggregate after-tax disposable income.

This broad measure of the consumer’s balance sheet provides key information on whether the consumer is over extended and carrying too much debt. After the Federal Reserve increased the federal funds rate from 1.0% in June 2004 to 5.25% in July 2006, the Household Debt Service and Financial Obligation ratio rose from 16.8% in June 2004 to 18.1% in the fourth quarter of 2007. To determine whether consumers have too much costly mortgage debt, the Federal Reserve monitors Mortgage Debt Service Payments as percent of disposable income. Mortgage debt service payments rose from 5.8% in the second quarter of 2004 to 7.2% by the end of 2007. As of June 30, 2020 it was down to 3.7% almost half of what it was in 2007. Homeowners are in a much stronger financial position now than in 2007.

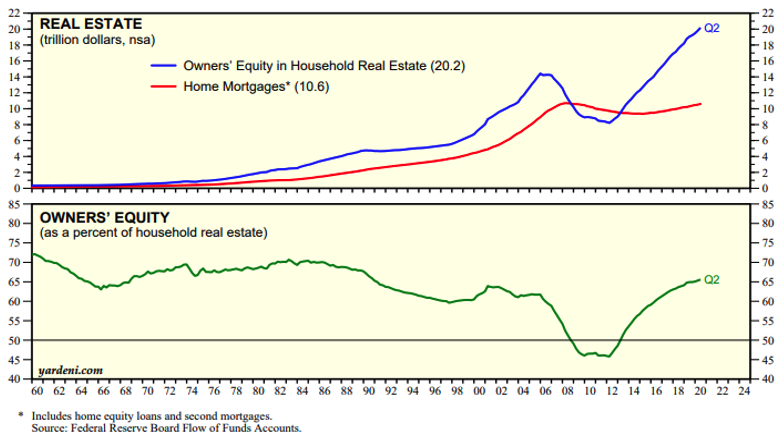

Although soaring home prices have become disconnected from incomes, they are a boon to existing home owners, since it boosts their home equity. Home equity rose by $620 billion from June 2019 through June 2020 according to Core Logic. Home owners equity as a percent of home prices has improved from 45.5% in 2012 to 65.5% in 2020.

Home owners equity bottomed in 2012 at $8 trillion after home prices had fallen by -25% to -50% in the cities that had experienced the most extreme appreciation during the housing bubble. Since that low home owners equity has soared to $20 trillion as of June 2020 compared to $10 trillion of mortgage debt. The vast majority of home owners have a larger equity cushion than in 2007. Before the Housing Bubble popped, Homeowners equity fell from 61.8% in the first quarter of 2005 to 54.2% at the end of 2007. Some of the decline in homeowners equity was due to a drop in home prices, as prices fell to $173,300 and by the end of 2007, after topping in June 2006 at $184,500, based on the Case/Shiller national home price index.

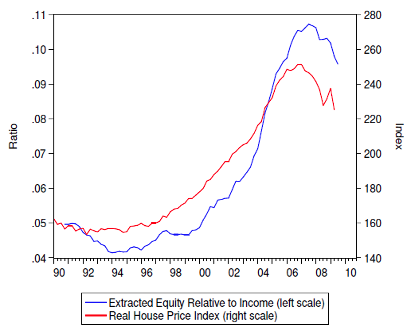

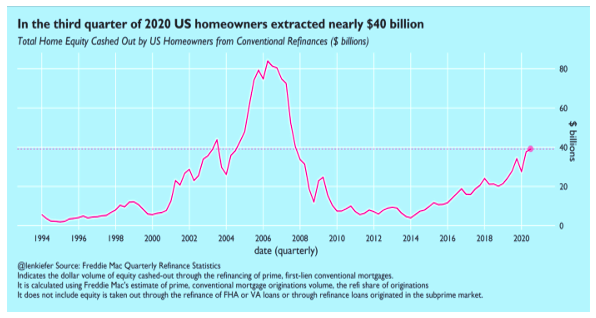

The other factor that caused home equity values to fall was mortgage equity withdrawals as home owners pulled equity out of their home value in the form of home equity loans as the Housing Bubble was inflating. Beginning in 2005 homeowners extracted more equity than their homes appreciated. This continued even after home prices topped in 2006 and was made possible by extremely lax lending standards. Between 2002 and through 2005 homeowners pulled out more than $1 trillion of their home’s equity through home equity loans. Consumers used those finds to buy cars, go on vacations, and purchase second homes. The Federal Reserve estimated that home equity extraction funded 75% of GDP growth from 2003 to 2006. From the beginning of 2005 through the end of 2007 homeowners routinely pulled out $40 billion to $80 billion of equity every quarter. For the first time since 2007 homeowners took more than $40 billion from their home’s equity in the third quarter of 2020. Undoubtedly many homeowners spent this money at Home Depot and Lowes and to purchase new and used cars and trucks. If homeowners increase the amount of money they pull out of their home equity in coming quarters, this could become a concern but for now it’s providing the economy a lift.

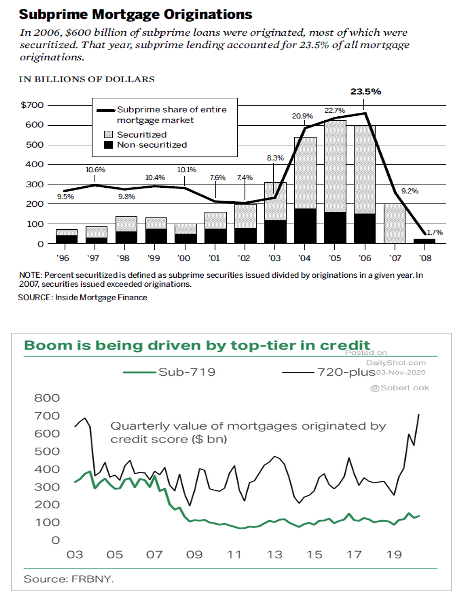

Another major difference with the housing bubble is that lending standards are much higher now. During the peak years of the housing bubble lending standards were lowered so much that many mortgage loans earned the nickname Liar Loans. As lending standards fell the amount of sub-prime mortgages became an ever larger portion of the mortgage market. The percent of sub-prime mortgages rose from 7.4% in 2002 to 23.5% in 2005 more than tripling in the process. The vast majority of the increase in sub-prime loans were then securitized and sold to investors, pensions, or held by the banks that securitized the pool of mortgages. Almost without exception these pools of sub-prime mortgages were given a triple AAA rating by the rating agencies, after being paid by the firm that securitized the loans. According to the Federal Reserve of New York the current boom in housing is being funded by mortgages made to borrowers who have a much higher credit rating than during the Housing Bubble.

Lasting Changes Reshape Society

If COVID-19 had been COVID-04 it would have been far more disruptive for daily life and the economy. In 2004 we didn’t have the technological capability to almost seamlessly shift from working every day in an office to working at home. The ability to readily communicate with customers via ZOOM didn’t exist. Restaurants wouldn’t have been able to take orders and have customers pick up their meals or use a delivery company to bring food to people at home. The accessibility to order just about everything we need online and have it delivered within 48 hours was barely a dream in Jeff Bezos mind. As difficult as 2020 has been, it would have been far worse in 2004.

Vaccines will make it possible for many of those working from home to resume working in an office at some point in 2021, but the majority of employees will never spend as much time in an office as they were before the Pandemic. Employees have learned that they don’t need to go into an office to get their work done, are happier spending less time in meetings, and don’t miss the time wasted every day commuting. Companies have learned that productivity is higher, which translates into lower costs, employee retention is higher, and office space costs can be reduced. There have been numerous studies that have attempted to quantify how the work from home shift benefits employees and companies.

-According to the U.S. Census Bureau, the average worker spends nearly an hour traveling to and from their home and office every day–more than 300 hours in a year. Dell estimates that employees who worked remotely ten days a month saved about $350 a year in commuting costs.

-Global Workplace Analytics likewise suggested that on-site workers spent around 11 days in traffic per year as well as $2,500 to $6,000 on various expenses related to showing up at an office.

-Remote worker respondents to a CoSo Cloud survey said they saved as much as $5,240 per year by working from home.

-83% of employees feel they don’t need an office to be productive, according to Workforce Futures.

-In a survey by Polycom Inc, two out of three respondents said they were more productive working remotely than when they worked at an on-site office. Additionally, three out of four respondents mentioned working remotely helps them with work-life balance.

-A Cisco-sponsored study performed and results concluded that partially working from home resulted in a 12% increase in productivity. After AT&T’s telework initiative, the company reported saving $150 million in extra hours of productive work from these employees.

-Cisco’s Internet Business Services Group also reported an annual savings of $277 million in productivity due to remote work.

Downside of Disruptive Changes

While the wave of people working from home and moving out of cities has given the housing market a big boost, it is creating some negative ripples. With fewer employees working in an office, companies will need less office space which will hurt commercial landlords and the valuation of office building properties. The full impact of the shift to working from home hasn’t been fully realized but the vacancy rate for Offices is already the highest since 2014. As more companies solidify how much time their employees will spend in the office, the vacancy rate will rise during 2021. According to Kastle Systems, a security firm that monitors access-card swipes in more than 2,500 office buildings in 10 of the largest U.S. cities, the return rate has climbed from a low of less than 15% in April to 25% on November 18. The return rate in San Francisco is 13.4% which means 86.6% of offices have no workers, with New York’s return rate of 15.9% not much better. According to data firm Trepp LLC the percent of office mortgage backed securities that were more than 30 days delinquent has increased from 1.7% in February to 2.3% in early November. This will likely lead to consolidations, bankruptcies, and bad loans for banks in the second half of 2021 or 2022. The surge in consumers ordering more online is going to result in more retail bankruptcies and store closures in 2021, even as retailers improve their online presence and service. The vacancy rates for Shopping Centers and indoors malls will continue to climb and cause more financial pressure for large real estate firms.

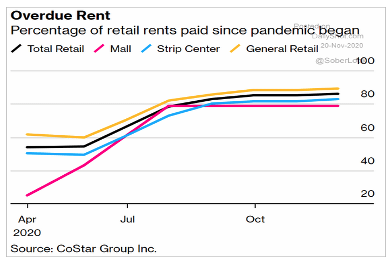

With fewer workers working in downtown office buildings, there will be less demand for quick lunches, business lunches, and especially business dinners for clients and employees. This will make any recovery for restaurants and bars far more difficult, even after vaccines have done their job of containing or eliminating COVID-19. The migration out of cities will only make a bad situation worse for many small businesses. According to Bloomberg, retailers, restaurants, gyms, and other service businesses have accumulated $52 billion in back rent with no real possibility of catching up. Even with viable vaccines on the horizon, the amount of time it will take to vaccinate the U.S. population won’t happen quickly, which means it will be too late for many small businesses. A surge in voluntary and involuntary small bankruptcies is coming as owners throw in the towel or their landlord presses them for payment. Unless Congress acts soon landlords may demand repayment and push many of these businesses over the edge and into bankruptcy.

The clock is ticking for millions of unemployed workers with many nearing the end of their unemployment benefits. As of November 7 there were 20.45 million people receiving some form of unemployment benefit. According to the Census Bureau there are 17.8 million adults living in a household that is behind on rent or their mortgage payment. Most of the eviction protections enacted by Congress are due to expire on December 31, 2020. In the most recent Household Pulse Survey by the Census Bureau, 5.8 million Americans said they may be facing eviction in the next two months. In addition to the unemployed, there are millions more who are working, but getting far fewer hours than before the Pandemic. With less income many are forced to decide whether to pay the mortgage or rent or buy food. Images of cars as far as the eye can see waiting hours to receive a bag of food from a food bank is a stark reminder that millions of people are facing a reality every day that few of us can comprehend. It is unconscionable that Congress has been unable to address the hardships faced by millions of people for political reasons.

Will Politics Change?

I understand the political calculations of the Republicans. They want to wait until December 14 for the electors to cast their votes and finalize the election. The electors will vote on a winner takes all basis, which means whichever candidate won the state receives all the electoral votes from that state. The only exceptions are Nebraska and Maine. By waiting until the election is finalized, Republicans hope they won’t lose the ardent supporters of President Trump especially in Georgia. If the Republicans are to retain control of the Senate, they need them to vote in Georgia’s Senate election on January 5. The Republicans will have no excuse after December 14 not to negotiate and agree to a new stimulus bill. The Democrats had the opportunity to agree to a $1.8 trillion deal before the election. Nancy Pelosi chose not to take it to avoid angering the progressives in her party since the Democrats needed progressive votes for Joe Biden to win, pickup seats in the House, and in a perfect election win the Senate. With the election over the Democrats don’t have a reason not to come to the negotiating table, if the Republicans reengage after December 14.

The size of the stimulus bill before the election was an issue for both parties. Some Republicans think the economy doesn’t need additional stimulus since we’re in the middle of V-shaped recovery and they are worried about deficit spending. They were willing to support $600 billion and possibly up to $1 trillion in additional spending before the election. The Republicans who oppose more support should go to Main Street and talk to small business owners, consumers facing eviction, and distribute food at a food bank for a day. The Democrats in the House pushed through a spending bill in May that totaled $3.0 trillion that included items that had little to do with helping those who most need the assistance.

- Nearly $1 trillion for cash-strapped state and local governments

- A second round of $1,200 direct paymentsto individuals, with up to $6,000 per household

- $200 billion for hazard pay for essential workers

- $75 billion for Covid-19 testing efforts

- An extension of the $600 per week federal unemployment insurance benefit through January (it is currently set to go through July)

- $175 billion in rent, mortgage and utility assistance

- A 15% increase in the maximum Supplemental Nutrition Assistance Program benefit

- Repeal of the $10,000 cap on state and local tax deductions for two years, which would help certain states’ budget crunch but benefit higher-income taxpayers most

- Expanded mail-in ballot access

- Relief funds for the U.S. Postal Service

- $10 billion in emergency small business disaster assistance grants

- Subsidies and a special Affordable Care Act enrollment period for people who lose employer-sponsored health coverage

In addition to the items highlighted in green I would include funds for states to cover the cost of distribution and vaccinations, and costs for contact tracing and testing. I would lower the $600 a week in federal unemployment assistance to $350. The Democrats who won’t support a smaller stimulus bill should go to Main Street and talk to small business owners, consumers facing eviction, and distribute food at a food bank for a day.

On November 19 Treasury Secretary Mnuchin requested that the Federal Reserve return $455 billion to the Treasury that was part of the $500 billion included in the CARES Act for emergency lending facilities through the Fed. These funds have already been appropriated by Congress, so they could be redirected to additional loans for small businesses and extending unemployment benefits. This would make it easier for Republicans reluctant to pass another $1.2 trillion stimulus bill in accepting a bill that would authorize an additional $600 -$700 billion in spending. Combined with the $455 billion already sitting at the Treasury, an additional $600 would bring the total amount to near $1.0 trillion. Hopefully Democrats would accept a $1.0 trillion bill, if Senate Majority leader McConnell brings it up for a vote after December 14. Time is of the essence and both parties need to put politics aside and provide small businesses and unemployed workers a lifeline, which is far different than ‘stimulus’. A lifeline is for those who are drowning, while stimulus is adrenalin for those who are OK. Congress also needs to extend the eviction deadline through June 30, 2021, and provide funds for landlords who are under pressure from banks. Providing landlords funds so they agree not to evict tenants (families and businesses) is not much different than providing funds to companies that were then required to keep their employees on the payroll so job losses would be lower.

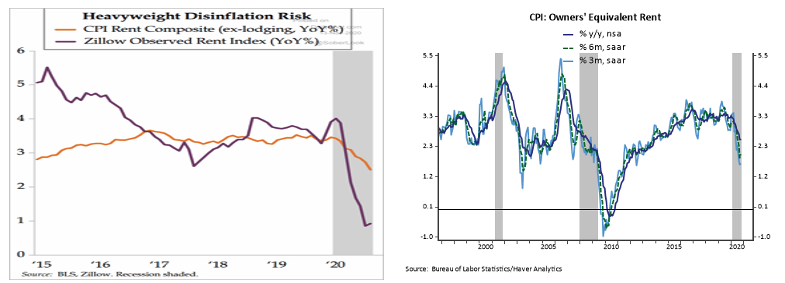

Consumer Price Index and Rents

In October the Consumer Price Index (CPI) was unchanged from September as was the Core CPI, which was up just 1.6% from a year ago. The benign headline numbers belie what’s going on under the surface. One has to look at the composition of the CPI to better understand why the CPI and Core CPI are likely to remain tame in coming months. Housing represents 42.1% of the CPI and the decline in apartment rents in major cities has weighed on the CPI. In order to calculate the costs associated with Housing (Shelter), the Labor Department uses owners’ equivalent rent (OER) of primary residences. Most households in the United States own the home in which they live so OER represents the rent that homeowners implicitly pay to themselves or the amount they could obtain by renting their home to someone else. The second largest component is the rent that tenants pay to landlords, whether it is for a home or apartment.

The CPI Rent Composite held steady during 2017 until the Pandemic hit in 2020. The Zillow Observed Rent Index (ORI) dipped below the CPI Rent Composite in 2017 and 2018 and then spent the last half of 2018 and 2019 modestly above it. The migration out of major cities has caused the ORI to drop well below the CPI Rent Composite, which should continue to pull it down as it has since last spring. The downward pull from OER in the CPI will keep the Core CPI from rising and may cause it to fall in coming months.

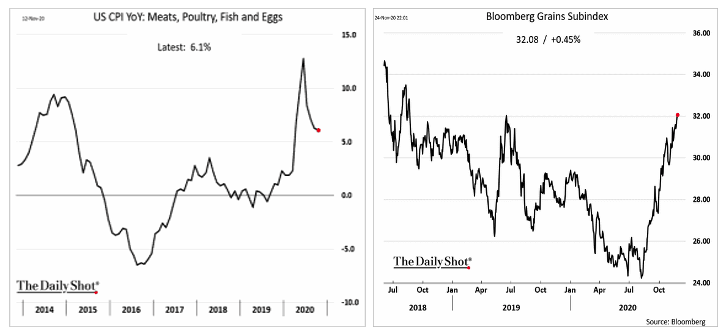

With more people working from home and restaurants closed or only available for pickup or delivery, the number of meals prepared at home has increased since last February. Meat prices spiked higher after meat packing plants were closed due to the Pandemic and have come down since those plants reopened.

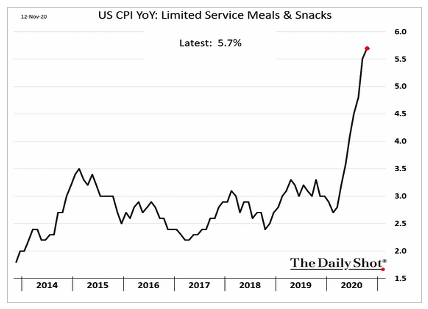

The cost of preparing a meal has increased as the cost of fish and eggs have gone up. In coming months food costs are set to rise again as the 33% increase in grain prices pass through the food chain and result in higher meat, poultry, and cereal prices. The Core CPI excludes food and energy, so higher food prices won’t show up in the Core CPI. Fast food restaurants have adapted quickly by allowing customers to order a lunch or dinner online and then pick up the food at the store. Fast food restaurants (Limited Service) have been able to pass along the additional costs they have incurred to expedite ordering by almost doubling the average price increase in recent years to 5.7%.

The increase in new and existing home sales typically results in higher demand for washing machines, dryers, refrigerators, and dish washers. For most of the past seven years the prices of major appliances actually deflated by more than -5.0% annually. After President Trump levied a 20% tariff on washing machine imports from China in 2018, a brief bout of inflation ensued. After that price surge ran its course, the prices for major appliances reverted by falling -8.0% Y-O-Y in January 2020. The dramatic increase in home sales has caused prices for major appliances to jump by +11.5%, which is leading to sticker shock for many new home owners. Of course this shock came after they moved out of the city and shocked by how much a used car cost.

Since the Pandemic began the cost of living for many CPI components has changed dramatically. The cost of a men’s suit has plunged by almost -25.0% as demand for suits and sports coats have collapsed with so few men going into an office or meeting with clients or prospects. People are using household cleaning products like never before so the change in the cost of cleaning products has jumped from 0% at the onset of 2020 to +5.0%, and up from the normal annual increase of +1.0%. Gasoline prices have dropped by -18.0% from a year ago as most people are driving far fewer miles, so this is like a double savings. Gauging the true rate of inflation is going to be tougher in 2021, especially if one relies on the Core CPI as it will likely understate the true level of inflation due to the drop in rents. On the surface it may make it look like inflation is holding steady, but what most consumers pay for the goods and services they buy could easily exceed Core CPI. If this proves correct, inflation expectations may be a better indicator of inflation, as expectations are likely to more accurately reflect the real world inflation experience of most consumers.

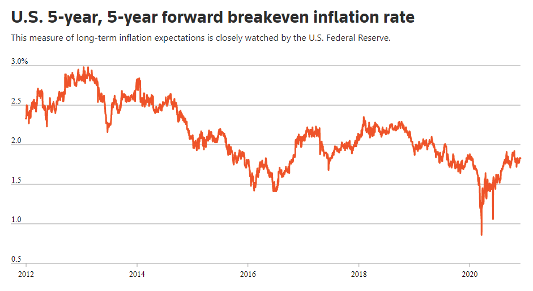

Since topping at 2.9% in February 2013 the 5-year forward breakeven inflation rate has trended lower, and set a lower peak of 2.3% in October 2018. A trend line connecting the February 2013 high with the lower high in October 2018 looks like it would now be near 2.1%. This is where it was in April 2019 after it ticked up to 2.1%. If the 5-year forward breakeven inflation rate climbs above 2.1% in 2021, it would represent a breakout worth paying attention to irrespective of what message the Core CPI is providing.

Jim Welsh

@JimWelshMacro

MacroTides.com

[email protected]

Related Links:

https://news.gallup.com/poll/321800/covid-remote-work-update.aspx

https://www.zerohedge.com/personal-finance/used-vehicle-market-wild-ride-weirdest-economy-ever

https://www.wsj.com/articles/home-sales-rise-to-14-year-high-in-october-11605798326

https://www.epi.org/nominal-wage-tracker/

https://www.federalreserve.gov/releases/housedebt/default.htm

https://fred.stlouisfed.org/series/HOEREPHRE

https://www.wsj.com/articles/factories-hum-to-keep-up-with-auto-housing-demand-11603816320

https://www.census.gov/construction/c30/pdf/release.pdf

https://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales

https://www.economy.com/united-states/house-price-value-for-new-homes

https://www.zerohedge.com/markets/struggling-retailers-owe-52-billion-overdue-rents

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr425.pdf

https://graphics.reuters.com/USA-ECONOMY/010040W01WS/index.html

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All