U.S. Economic Outlook: Brighter Days Will Return

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAfter a quarter of record-breaking gains, the U.S. economy has lost momentum. COVID-19 is resurgent and the weather has turned cold, keeping more consumers home and weighing on the recovery.

With promising developments surrounding vaccines and fiscal stimulus, there is reason to be optimistic for conditions improving in the near future. Consumers and businesses are eager to return to their prior lifestyles and levels of activity. Though it will bring its own surprises, we hold out hope that 2021 will be a better year than 2020. But at the moment, the economy is working through a slower interval.

The disruption from COVID-19 has endured longer than most of us initially anticipated. Recent news gives us hope that this disruption has an end point. Additional support to head off lasting financial damage will be a worthwhile investment. For now, we wait out this crisis during these darkest days of winter.

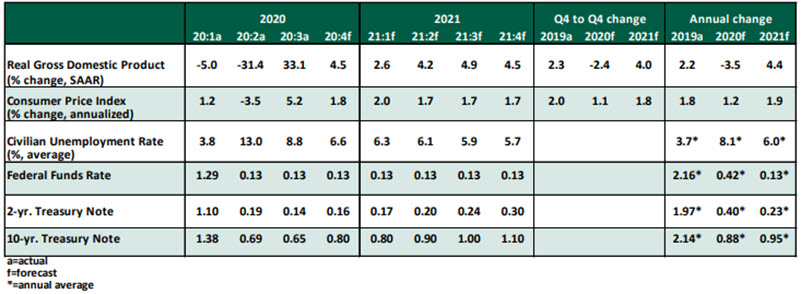

Key Economic Indicators

Influences on the Forecast

- The Bureau of Labor Statistics’ Employment Situation Summary for November revealed a labor market that has slowed. Job growth of 245,000 is more typical of a mature growth cycle, not the sharp recovery we had hoped to continue. Though the unemployment rate improved slightly to 6.7%, that fall was due to a decline in the labor force; the participation rate is hovering at levels last seen in 1976. Employment remains more than nine million workers below its peak in February 2020. Continued progress will depend on demand recovering across all sectors.

- COVID-19 remains the greatest impediment to economic progress. New diagnoses, hospitalizations and deaths are still ascending for the nation overall. Though some regions appeared to pass a peak of new infections, the effects of Thanksgiving travel are still becoming apparent. No leaders are eager to place new restrictions on businesses, but the constraint of hospital capacity has forced some selective business closures.

- The fourth quarter started with economic momentum. Indicators like capital goods investment and consumer spending held their strength, and purchasing managers’ indices show ongoing expansion in both manufacturing and services. Worrying signs have emerged later in the quarter and will cast a shadow on the new year. We expect the slowest interval for growth to be the first quarter of 2021. As vaccines are administered to more individuals, confidence and activity should rebound from the second quarter onward.

- Fiscal support will aid the economy through what we hope to be a final temporary slowdown. Members of Congress have renewed their negotiations. Proposals that have surfaced are all under $1 trillion; at this limited size, they will serve more as targeted relief for affected populations like the long-term unemployed, rather than broad stimulus. Discussions are ongoing as of the time of writing, and President Trump’s support for the final bill is uncertain, especially as Treasury Secretary Steven Mnuchin has offered a separate proposal. Our expectation has been for no further fiscal movement until after the next presidential inauguration, but we will welcome the upside if a bill comes together sooner.

- Funding for the federal government is the more pressing matter. The government is at risk of a shutdown if Congress does not approve funding by Friday, December 11. Funding by a series of brief continuing resolutions will keep this matter top of mind.

- Inflation risk remains muted. The October readings for both the consumer price index (CPI) and personal consumption expenditures (PCE) grew by only 1.2% year over year, with core PCE growing by 1.4%. Consumer price inflation will remain modest as long as demand is dislocated by the pandemic.

- Secretary Mnuchin’s call for the conclusion of the Federal Reserve’s special lending programs was a surprise. The programs in question were little utilized, but the Fed’s presence in markets is a stabilizing force. Absent any further stress in municipal and commercial lending markets, these programs can terminate at the end of the year without issue. However, if support is needed again in the future, the Fed’s ability to intervene will now depend on a Congressional renewal that may not be forthcoming.

- Single-family housing has held its strength, with housing starts elevated and house price indices showing continued appreciation through October. We will closely watch the multifamily sector, with millions of households at risk of eviction as moratoriums expire.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All