Stock Market Party

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFundamental Madness

Market Psychology

More on Where We Are Now

There’s Always a Bull Market Somewhere

It’s Actually a FANG (and Now Tesla) Market

Holiday Wishes and Some Schedule Changes

"History repeats itself, that's one of the things that's wrong with history.”

—Clarence Darrow (1857-1938), American lawyer

The end of 2020 has me looking back. I started writing the letters that later became Thoughts from the Frontline back in the late 1990s. Similar to COVID-19 today, we had a giant macro issue then, too: Y2K. It’s hard to believe now how frightened some people were. But as I expected, the big day came and the world didn’t end.

Another similarity is the stock market was rising like a rocket. This newfangled “Internet” thing had people super-excited, and rightly so. It was a world-changing paradigm shift. Unfortunately, some of the stocks born in that incredible boom weren’t world-changing paradigms at all. The market party ended, just as this one will, but went on far longer than almost anyone (including me) expected.

Had you bought the Nasdaq at the March 2000 peak, and held on, you would have got back to breakeven about 15 years later. And now, 20+ years later, your annualized return for those two decades would be around 4%. That’s not terrible. You beat CPI inflation by a couple of points. But people back then expected far more—15% annualized returns were thought to be easy.

The moral of the story is simple: Starting valuation matters. In the example above, waiting a couple of years to start lower would have drastically changed the outcome. But again, almost no one thought that at the time.

And while we’re talking about valuable things, please let me remind you that the window of opportunity to become an Alpha Society member this year is closing soon.

The Alpha Society is our most exclusive membership service—and the one that is nearest and dearest to my heart.

It was born out of my desire to create an “inner circle” of serious investors. I have watched it grow over the years like a proud father watches his kid’s first steps, first day of school, first football game... all the way to graduation.

We’ve upgraded many of the features this year—for example, you’ll find a brand-new version of the Alpha Council, our members-only social media platform, which now looks a lot like Facebook. You can meet your fellow Alpha Society members there, as well as our editors. I sometimes stop in to chat as well.

New members also receive a hand-selected bonus package I’m sure you will enjoy. It gives you free access to three of Mauldin Economics’ most popular events and specialty products.

As an Alpha Society member you’ll receive lifetime access to all of our premium subscription services, including those we’ll launch in the future. You can even bequeath your membership to your kids or grandkids.

The savings over time are enormous, so if you are serious about investing (and our research), I highly recommend you join my “inner circle” before time runs out. The membership offer closes at midnight, December 21.

And now, we’ll take a closer look at the stock market and where it may be going.

Fundamental Madness

We last dove into the equity pool back in July in Valuation Inflation. Rereading that letter, I could easily say it all again and just update the numbers. All the valuation metrics I described look even more overvalued now.

That makes sense when you consider the prime factor—central bank liquidity—hasn’t changed. The Fed has continued pumping so asset prices have kept rising. It’s not just stocks, either. Their bubble is just more obvious because they change hands more often than houses and land do.

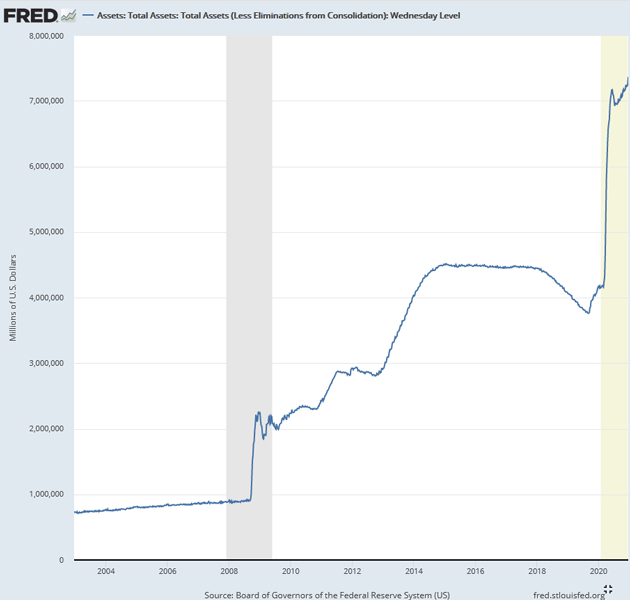

Here are Federal Reserve assets, via the FRED database:

Source: St. Louis Fed

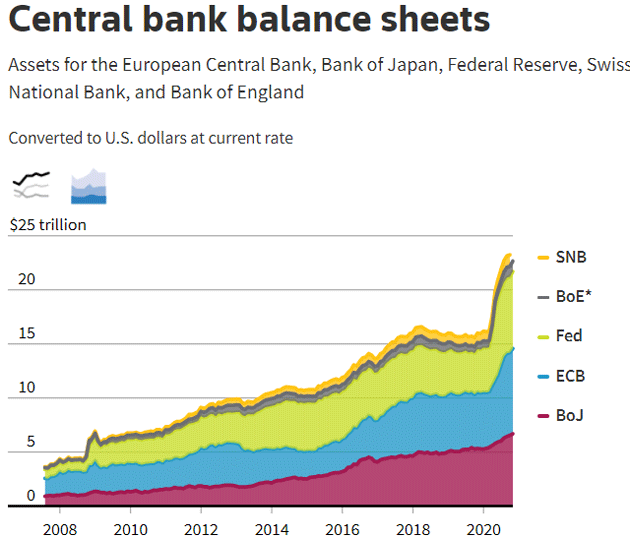

It’s not just the US Federal Reserve. The world’s other central banks are all doing the same thing.

Source: Thomson Reuters

The passage of time also indicates monetary stimulus may be more important to markets than fiscal aid. The stimulus checks, extra unemployment benefits, and PPP loans mostly ended over the summer and fall, but stocks kept climbing. This suggests that government spending, while it was a lot, had a smaller impact on the stock market.

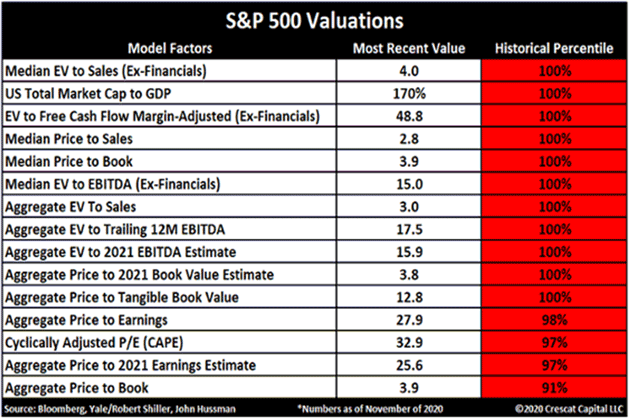

But regardless of the cause, this market is certainly at the upper end of fair value, if not overvalued, no matter what fundamental or historical comparison you want to make. It’s clear in this Doug Kass table I showed you last week.

Source: Doug Kass

To buy now, you must either convince yourself this is wrong, or find some reason to argue “it’s different this time.” That is rarely the case. To see why, we are going to look at some of the above data in detail, starting with some charts from Dave Rosenberg’s magnificent monthly chartbook.

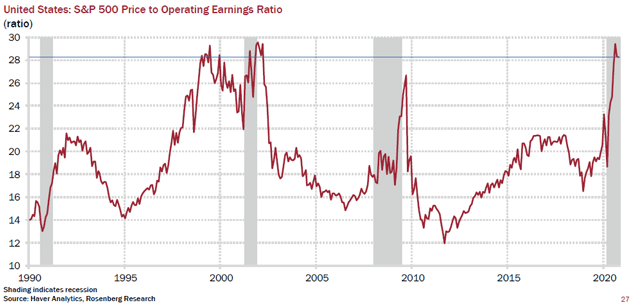

The S&P 500 price-to-operating earnings ratio is back where it was in the early 2000s bull market and well above its peak in the financial crisis.

Source: Rosenberg Research

Worse, notice how fast it climbed. That’s not normal. Nothing fundamentally changed enough to make US public company earnings 50% more valuable than they were in March. What changed was the cost of debt capital, and it changed for purely artificial reasons. That means the valuation is now artificial, too.

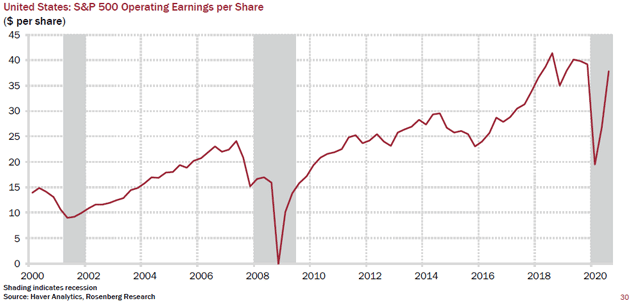

Looking at it in dollar terms, we see S&P 500 operating earnings per share are now back where they were in 2018–2019, when the market was much lower. There is a whole lot of optimism going on (channeling my inner Jerry Lee Lewis).

Source: Rosenberg Research

That’s partly good news. It means companies collectively (though not every company) are making as much as they did before the pandemic and recession. As I noted last week in Survival of the Biggest, some of this is at the expense of struggling and dying small businesses (especially in the restaurant and hotel/travel sector). But it’s not imaginary.

The bad part? While S&P 500 companies are making the same profits, their share prices are something like 35% higher. Investors are willingly paying much more for each dollar of earnings. What are they thinking?

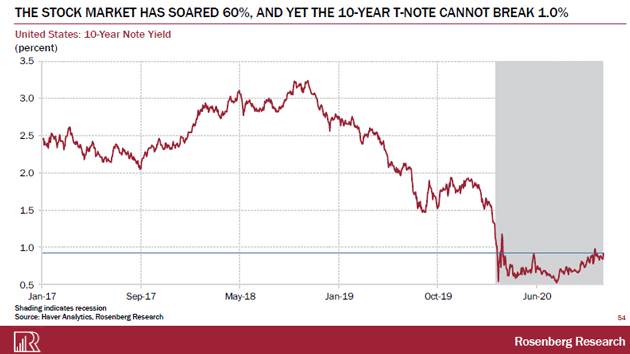

That being said, the traditional difference between the bond and stock market is striking:

Source: Rosenberg Research

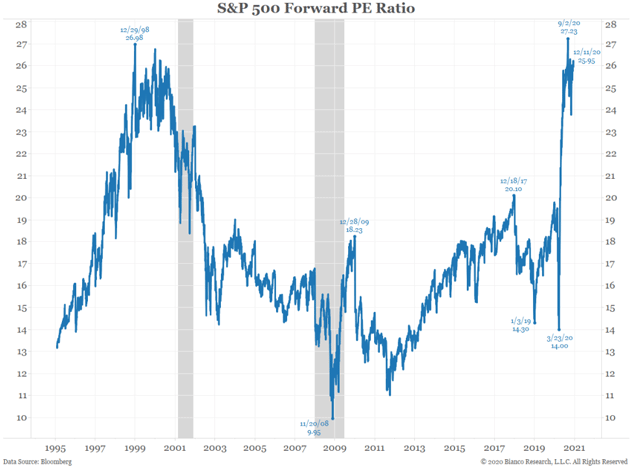

Well, maybe they are thinking earnings will rise a lot more. This next chart, courtesy of Jim Bianco, shows the forward P/E ratio, which means it looks at Wall Street’s consensus expectation rather than what has actually happened.

Source: Bianco Research

Here again, we see the same pattern. This means buyers are not simply paying fair price for expected future earnings. They are paying more even if earnings grow to match Wall Street’s rosy scenarios. That’s a market we can no longer call “rational.” It is trading based on something other than reality.

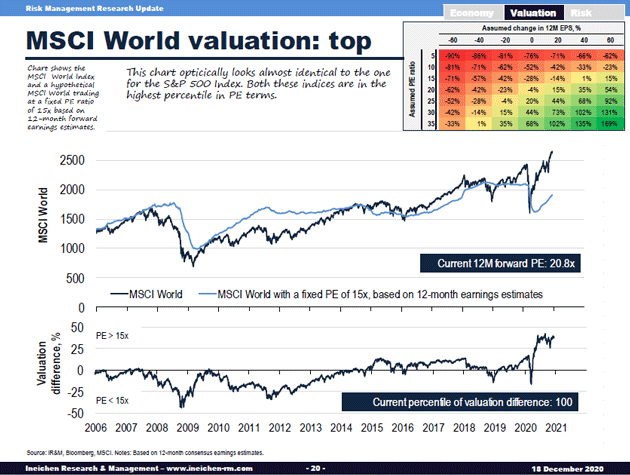

By the way, it’s not just the US market. The whole world is being revalued. My friend Alexander Einechen since this out Friday morning:

Source: Alexander Einechen

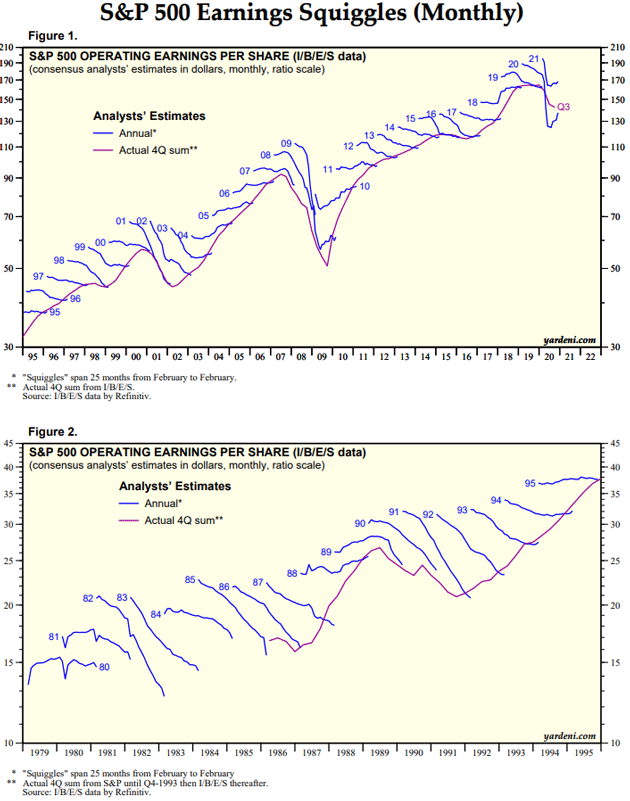

Further, the chart from Jim shows forward “projections.” How often do those projections turn out to be correct? The answer is, almost never. Jim shows our friend Ed Yardeni’s reviews of analyst estimates for the last 35 years. The little blue squiggles show where estimates begin and you can see where they end. Most of the time they end up going down, especially when valuations are high. Analysts are human, and they make the human mistake of projecting current reality into the future.

Source: Bianco Research

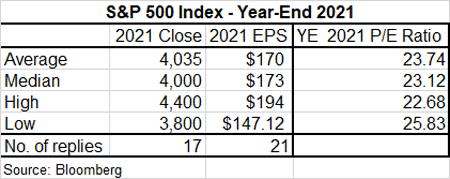

So what are analysts actually projecting? It turns out that they are a remarkably bullish group. Again from Jim Bianco:

Just for the record, here are the individual estimates…

Source: Bianco Research

This is a very optimistic group. Maybe I should ask them to share their drug of choice so it would make me happier, too.

As I write, the S&P is around 3,700. Citigroup, the most bearish, estimates 3,800 by the end of 2021. J.P. Morgan and Cantor Fitzgerald see an almost 20% further gain on top of what we have seen this year.

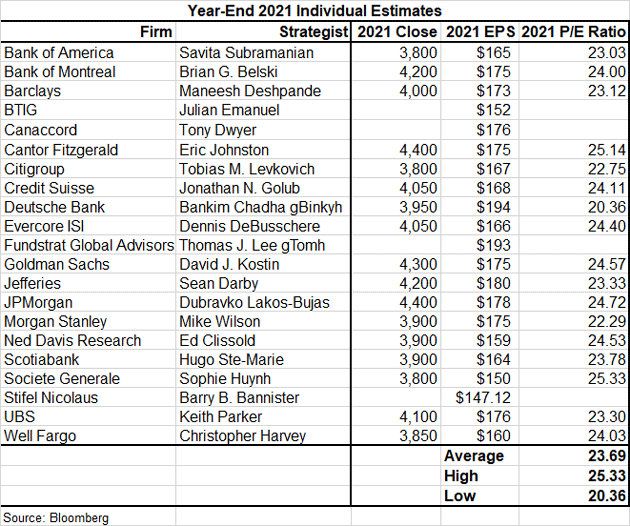

Not everyone is so bullish. John Hussman projects a -1.7% 12-year total return for a 60/30/10 portfolio. Please note the tight correlation of the red line with actual 12-year returns. That should worry current “long-term” investors:

Source: John Hussman

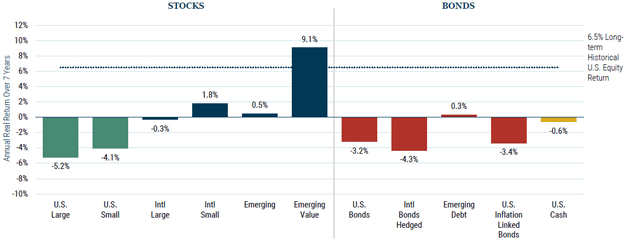

And there is Jeremy Grantham’s seven year projection from GMO (note his projections on emerging market value -we will come back to that again shortly):

Source: GMO

Market Psychology

Wrapping up that valuation letter last July, I said…

History also shows manias can persist much longer than most people think. Back in 1999, I and many others thought there was no way the bull market could go on. Yet it did, with the Nasdaq actually doubling in 1999.

Since then the Nasdaq Composite rose another 28%. Not quite doubling in a year but it’s certainly been a furious pace. And it’s entirely possible the pace could continue, just as it did in the 1990s. But it will end at some point.

Back in June, my friend Anatole Kaletsky of Gavekal wrote a fascinating analysis on “Five Features of Market Madness.” (Alpha Society and Over My Shoulder members can read it here.) At the time, the Nasdaq Composite was trying to break over the 10,000 level. Anatole said a breakout would mean a resumed bull market, with questionable companies again soaring to new highs. That’s exactly what happened.

But more important, Anatole explained how market psychology was in charge, just as it was in the 1998–2002 period, and he listed five reasons why. I’ll repeat them for you with some comments.

- While monetary easing usually starts a bubble, a reversal in monetary policy is unlikely to deflate the bubble once the speculative momentum builds.

This is what happened 20 years ago. The Fed was actually raising rates in 1999 and 2000, but stocks continued merrily higher with only short interruptions. This week’s FOMC meeting confirmed yet again they will keep pumping a long time. I think they may pause the QE activity next year if the vaccines go well and the economy picks up steam, but I see no chance they will try to withdraw the new liquidity. They’ll just let it gradually roll off as time passes.

- Valuations do not matter while a bubble is inflating, but they become very important after it bursts.

The charts above show this pretty clearly. Anyone who is buying stocks now obviously doesn’t care about valuations. But a time will come when they do care, and they will care a lot.

- Bubbles typically end with some huge corporate collapse, often tainted with fraud.

In past bubbles we saw scandals and failures like Enron, Lehman and Bear Stearns. This bubble will probably bring similar collapses from similarly well-regarded companies. Who? Your guess is as good as mine. I feel sure a lot of accounting games are being played. As cracks begin to form, these will be harder to sustain.

- Bubble dynamics need not bear any relation to the strength, or weakness, of the economic cycle.

This is certainly the case. We are not just in recession but a deep recession, with millions unemployed and millions more having lost income. Yet the stock market doesn’t care. It just goes up, for its own entirely different reasons.

- Speculation increases dramatically when prices break through major highs.

This year has been a long string of “____ hits new all-time high” headlines. That’s both a sign of speculation and a cause of it. A new all-time high in a stock means every shareholder has an open gain. That both gives them confidence and makes them less interested in selling, which sends prices higher still.

This party will end. They always do—but they also defy the naysayers longer than anyone expects. We have clearly reached a point where investor psychology is far more important than any kind of corporate or economic data. Stocks will go up as long as people want to buy them.

But whenever they stop, look out below.

More on Where We Are Now

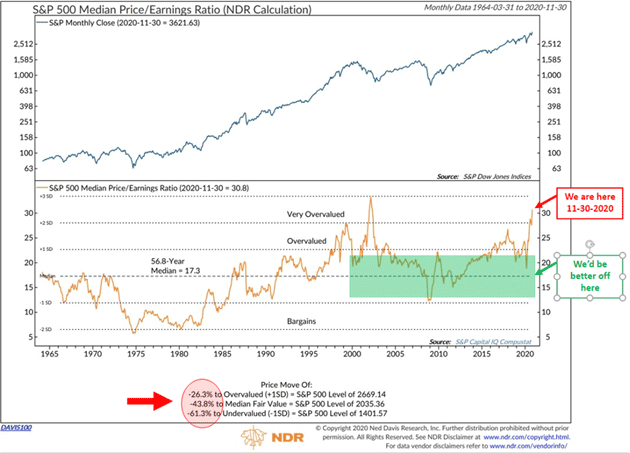

My friend and partner Steve Blumenthal sent me these two charts along with some explanatory data. We’ll start with median P/E, remembering Bob Farrell’s investment rule #3: There are no new eras—excesses are never permanent.

In the following chart, note the red “we are here” arrow. We sit in the “very overvalued” zone. Note also the green highlighted area and the “we’d be better off here” arrow. The dotted line shows the long-term median P/E is 17.3. The latest reading is 30.8. That’s higher than almost all other bull market peaks.

Lastly, take a look at the red circle toward the lower left. I think this is a pretty good way to estimate where you may want to buy equities more aggressively. Target one: 2,669.14 (though still overvalued, that is likely where the Fed steps back in should the market correct that much. Likely sooner in my view but just a guess). Target two: fair value at 2,035.36.

Source: Steve Blumenthal

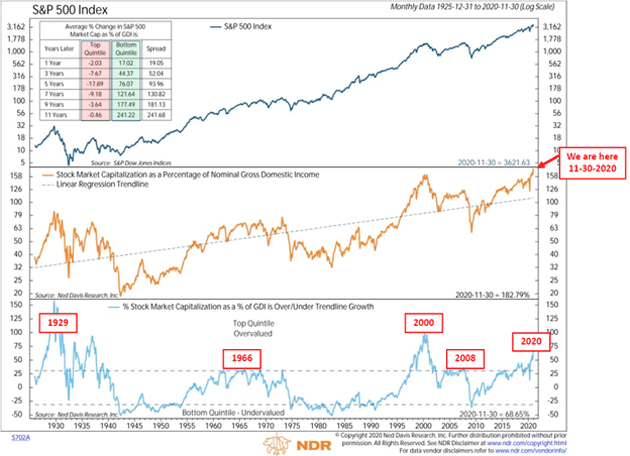

This next chart shows stock market capitalization as a percent of gross domestic income. I feel it is informative in terms of coming returns.

Note the red “we are here” arrow. This shows the stock market’s current value as a percent of GDI. The lower section plots the amount over and under the blue dotted long-term trendline that appears in the middle section of the chart.

The data box in the upper left shows the 1, 3, 5, 7, 9, and 11-year subsequent returns achieved when the market was in the top quintile—overvalued zone (red highlight in the data box) and when the market was in the bottom quintile—undervalued zone (green highlight in the data box).

We currently sit in the red zone, so expect negative annualized returns over the coming 11 years.

Source: Steve Blumenthal

There’s Always a Bull Market Somewhere

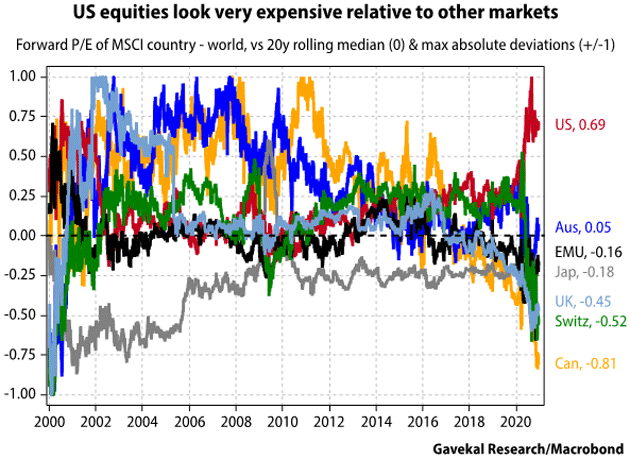

From Gavekal’s Will Denyer.

For various reasons, some countries tend to trade at higher multiples than others. So the spread must be normalized. In the chart below, a reading of zero indicates a normal spread vs. the world MSCI (based on the median of the past 20 years). A reading of 1 indicates that the spread is as positive as it has ever been in the past 20 years and is a strong warning signal. The US, currently at about 0.7, looks very expensive compared to other markets.

Source: Gavekal

As Jeremy Grantham noted, there are some significant relative valuation opportunities outside of the US.

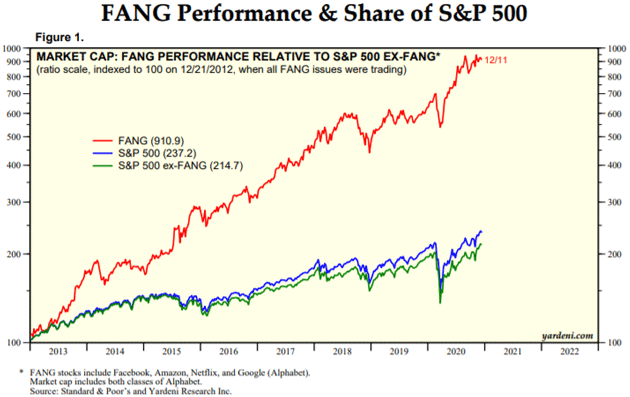

It’s Actually a FANG (and Now Tesla) Market

This chart is from Ed Yardeni.

Source: Yardeni Research

Note that almost all of this year’s outperformance has been from just four stocks. The “S&P 496” has been relatively flat. Those top four names now represent over 12% of the market and Tesla will soon add another 1.5%.

I have no idea where the top is, but history tells us there is a top somewhere out there prior to another steep drop. I will speculate about that in my forecast issue in January. But as a reminder, friends don’t let friends buy-and-hold index funds. Index funds make excellent trading vehicles. Use them appropriately. And tighten your hedges.

I will leave you with this bit of wisdom from my friend Doug Kass:

The Dunning-Kruger effect is a cognitive bias in which people with low ability at a task overestimate their ability. It is related to the cognitive bias of illusory superiority and comes from people's inability to recognize their lack of ability. Stated simply, the Dunning-Kruger effect observes that people who are the most ignorant about something will be the least aware of their own ignorance; they have the highest sense of false confidence.

With the benefit of a zero-commission trading app it is now easy and costless to trade, and the COVID-induced "stay-at-home" factor coupled with the desire of many to reclaim agency has contributed mightily to 2020's trading fever. As I have mentioned previously, the big marketing push of Robinhood's platform is taking advantage (selling orders) of those who don't understand and are likely to wind up losing plenty of money.

Perhaps, with so much out of their control this year, some have seen trading as a way of reclaiming the wheel and making risky bets on their own terms (or so they think).

Holiday Wishes and Some Schedule Changes

We will all be glad to see 2020 over. Like market valuations, the calendar is artificial but it has a psychological effect. The new year makes us pause and reassess. That’s certainly what I will do. This year both Christmas and New Year’s Day fall on Fridays so I am going to take a little writing break. My editorial and production teams could use some time off, too. I’ll be back on January 9 with my 2021 forecast issue.

Shane and I will spend the holiday season at home, using Zoom to connect with our children. It’s not the same, and I am really looking forward to when I can get my vaccine and get back on the road every now and then. I think it will take longer for the vaccines to roll out that most people anticipate, but I hope I am wrong. In any event, it will happen.

I think we will look back in five years and realize that the primary economic effect of COVID-19 was how it accelerated change faster than any of us had anticipated. It’s as if the world went on fast-forward. Not a bad thing, just a lot to adjust to. But periods of rapid change also bring lots of opportunities.

With that, let me wish you the best of holiday seasons, and sincerely thank you for the gift of your time and attention. I really do write these letters thinking of one reader, and for all practical purposes, that one reader is you. I hope you enjoy our weekly time together. We will resume our weekly chats in January. All the best!

Your finding opportunities in change everywhere analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All