Templeton Global Macro CIO Michael Hasenstab offers the team’s 2021 outlook.

At first glance, nothing ahead in 2021 could be as bad as 2020. We have been enduring the worst economic crisis in 80 years and the worst global health crisis in 100 years—events that have profoundly damaged lives and livelihoods around the world. The International Monetary Fund (IMF) projects that when we finally close the books on 2020, the world economy will have contracted 4.4%.1 Fortunately, as we flip the calendar to 2021, we are getting closer to a point at which the economic shocks of the past year become prologue for the economic stories ahead. Global growth is projected by the IMF to expand 5.2% in 2021, as economies improve from the lows of the prior year.2 Promising vaccine trials have presented scenarios for mass distribution by the spring of 2021, with the potential to drive the COVID-19 pandemic into remission by the second half of the year. Optimism for a return to better days abounds as 2020 draws to a close.

Yet the current state of the pandemic paints a starkly harsher reality. Second waves of COVID-19 infections have surged exponentially in areas of Europe and the US in the waning months of 2020, compelling several regions to reinstate restrictions and lockdowns. Some of the roughest conditions of the entire pandemic are likely to be faced in the final months of 2020 and the first quarter of 2021. In the absence of a widespread remedy, economic hardship will continue to deepen with each month of restricted mobility and stifled economic activity. Time is the key factor for many people and businesses teetering on the brink of insolvency—each day of income destruction threatens lasting damage. Unfortunately, near-term conditions are likely to worsen before they ultimately improve.

Investment Opportunities Are Emerging

From an investment standpoint, optimism for the second half of 2021 should be counterbalanced with caution over acute near-term risks, in our view. The pandemic continues to destroy areas of economic activity, resulting in substantial risks for a number of financial assets. Broad disinflationary effects are likely to persist until economies return to full mobility. We have been maintaining a cautious approach on risk assets in anticipation of second waves of COVID-19 in the fall and winter months.

However, several longer-term investment opportunities are beginning to emerge. We expect staggered timelines for when certain investments may become suitable given the wide variance in macro fundamentals and the divergent levels of control over the spread of the virus in specific countries. COVID-19 cases appear likely to reach a zenith during the winter months before vaccine treatments may cause the pandemic to ebb in the late spring and summer of 2021. The timing and effectiveness of vaccine treatments will be the key determinant for economic activity and financial asset valuations in the upcoming year.

Fiscal Deficits and High Levels of Debt Present Longer-Term Risks

It is also crucial to map economic trajectories beyond the impulses of 2021. The rate of growth during the rebound is unlikely to sustain its magnitude in 2022 and the years that follow. World GDP (gross domestic product) growth will moderate to around 3.8% in the 2022–2025 period, according to IMF projections, with advanced economies averaging 2.2% and emerging/developing economies averaging 4.9%.3 Stimulus programs will eventually wane as governments that were already burdened with high debt levels before the pandemic are forced to contend with limited fiscal space and deepening fiscal deficits.

Debt-to-GDP ratios have risen significantly in just about every country. Unorthodox policies such as modern monetary theory and debt monetization are likely to see greater political interest in upcoming years, increasing the risks for structural damage by imprudent governments. The upcoming decade will be increasingly defined by quality of governance factors, in our view, both at the domestic level as well as geopolitically.

In the US, debt levels are projected to exceed 100% of GDP over the next decade with a fiscal deficit heading toward more than 5% of GDP by 2030.4 Monetary policy is projected to remain loose for the foreseeable future, with the US Federal Reserve (Fed) anticipating near-zero-percent rates through 2023, while it continues to provide unlimited balance sheet support to financial markets. The Fed has also indicated a willingness to let the economy run hot in upcoming years to make up for several quarters of below-target inflation. Short-term US Treasury yields are likely to remain anchored by monetary accommodation in the near term, but surging fiscal deficits, massive debt levels and rising reflation expectations should eventually drive term premiums higher.

Geopolitical Risks Remain Elevated

Adding to the complexity of the current crisis is the precarious state of the world that existed before the pandemic. Heightened geopolitical tensions, rising nationalism and political polarizations have made it difficult for countries to find the collective goodwill needed to design collaborative solutions for shared problems, both domestically and internationally. COVID-19 has also enabled a number of governments to enact over-reaching policies that would otherwise be objectionable. Some regimes have drifted further toward authoritarian rule, using the pandemic for political cover.

Additionally, the deglobalization trends that existed before the pandemic have accelerated, as countries have increasingly turned inward to prioritize domestic concerns. Trade relations have been decaying among major economies in recent years. Structural shifts toward domestic production and regional supply chains would have substantial implications for the global economy and financial markets in the years ahead.

ESG Factors Will Shape the Post-COVID World

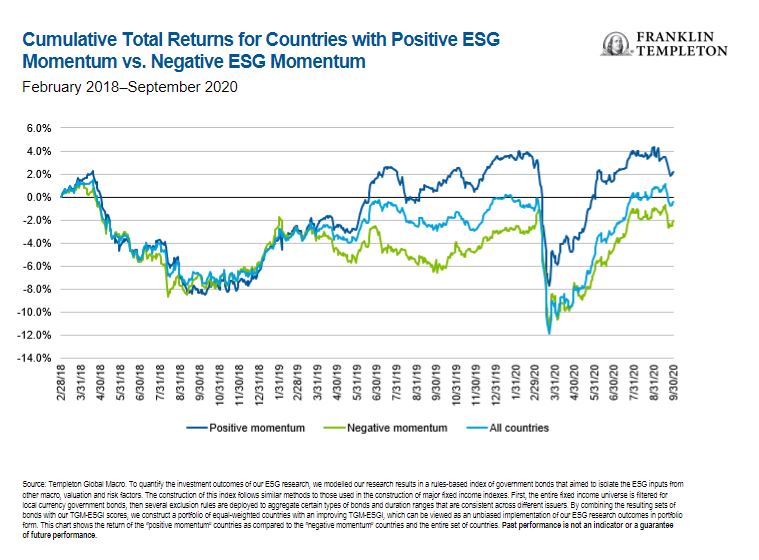

Environmental, social and governance (ESG) factors will play a major role in rebuilding the post-COVID world. Social cohesion and good governance have the power to accelerate a country’s post-crisis recovery, or the lack thereof can stymie it. Tragically we have seen the consequences of weak ESG factors in specific emerging markets during the pandemic. Countries that were less prepared for a health crisis due to weaker health care systems and less developed infrastructure, and/or less prepared for an economic crisis due to fiscal imbalances, high levels of debt and external dependencies, have suffered greater damage. By contrast, countries that were in stronger fundamental shape before the crisis, with stronger institutions, lower levels of debt and more diversified economies, have generally fared better.

Widening income inequality in many countries also remains a critical issue that threatens to undermine economic stability and intensify social discord. Damaged economies and elevated unemployment from the pandemic have only worsened several pre-existing structural problems. Countries that effectively address these challenges in the years ahead can strengthen the underpinnings of their economies, while those that neglect these factors risk further instability. We expect ESG to be a defining attribute for global fixed income markets in years ahead. Countries that are projected to improve on ESG factors often present the strongest investment opportunities.

Tactically Opportunistic for the Year Ahead

Overall, we anticipate being constructive in a number of regions as the world transitions toward a post-COVID era. However, near-term risks remain substantial. Regional lockdowns and restrictions will likely continue to be needed in upcoming monthsto counter exponential spread of the disease. Mobility restrictions will continue to be the most effective tool of virus suppression until a vaccine becomes broadly available. Until that point, lost incomes and damaged aggregate demand will continue to have a detrimental impact on macroeconomic conditions. We expect perceived safe-haven assets to remain relevant during the extant months of a worsening pandemic, but to eventually diminish in importance as medical advances incrementally beat back the disease. Looking ahead, we remain tactically opportunistic in specific local-currency markets while continuing to manage near-term risks. We remain optimistic for the new year, and the potential eradication of COVID-19.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies. Sovereign debt securities are subject to various risks in addition to those relating to debt securities and foreign securities generally, including, but not limited to, the risk that a governmental entity may be unwilling or unable to pay interest and repay principal on its sovereign debt. Investments in emerging market countries are subject to all of the risks of foreign investing generally and have additional heightened risks due to a lack of established legal, political, business and social frameworks to support securities markets.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

1. Source: International Monetary Fund, World Economic Outlook, October 2020.There is no assurance that any forecast, estimate or projection will be realized.

2. Ibid.

3. Ibid.

4. Source: Congressional Budget Office, An Update to the Budget Outlook: 2020 to 2030, September 2, 2020.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments