2021 IG Outlook: Despite Headwinds, a Path Forward Exists

Executive Summary

We enter 2021 with a set of circumstances and challenges completely unforeseen one year ago. The pandemic turned the world economy upside down, but a series of fiscal and monetary stimulus measures propelled markets to stunning returns that have created a difficult situation for fixed income investors. Below are the key issues that we believe will shape the IG market in 2021, as well as a preview of our portfolio positioning.

- Fed support will continue, but strength of economic recovery uncertain

- IG credit and mortgage backed securities (MBS) priced to perfection

- Fundamentals likely to improve in 2021

- IG credit supply expected to be lower, while MBS supply remains elevated

- Global demand likely to remain robust

- Significant spread dispersion within the index, creating pockets of opportunity

- We plan to remain overweight corporates and MBS, and underweight Treasuries

Economic Outlook: Strong Fed Support Amidst Uncertainty

Following a playbook devised in 2009, the Fed responded to the pandemic by launching a quantitative easing program that in nine months has matched the size of the three prior quantitative easing programs combined – and those were implemented over a period of six years. New wrinkles (including corporate bond and ETF purchases) have left yields low and spreads tight. Together, these combine to give us all-in-yields across the spectrum of investment grade assets near all-time lows.

The Fed support will certainly benefit the economy in the new year, but at the same time we will be grappling with a few key unknowns. Perhaps most importantly, we will face a lot of uncertainty as the vaccine rolls out across the country and we try to put the pandemic behind us.

Another layer of uncertainty is how and when the economy will find its footing. At best, we expect a somewhat uneven recovery, with sectors most directly impacted by the pandemic to be slowest to recover – these include hospitality, travel, and brick and mortar retail. Unemployment rates have fallen sharply from their highs set during the depths of the pandemic, but the economy will struggle to reach the full employment target the Fed seeks without a return to pre-pandemic activity. Many businesses have shuttered permanently and are not likely to be replaced by like endeavors that can easily absorb displaced labor supply. A true recovery probably requires re-training and deployment of these workers into other areas. This will take time.

Inflation is another big question in 2021. The Fed has committed to keeping rates at zero until it sees inflation rise above 2% for some time to make up for the period in which it previously trailed. Fiscal stimulus is the easiest path to stoking inflation, and the Fed has been curiously vocal in pressing the powers that be to agree on fiscal policies to complement the monetary stimulus the Fed provided so quickly.

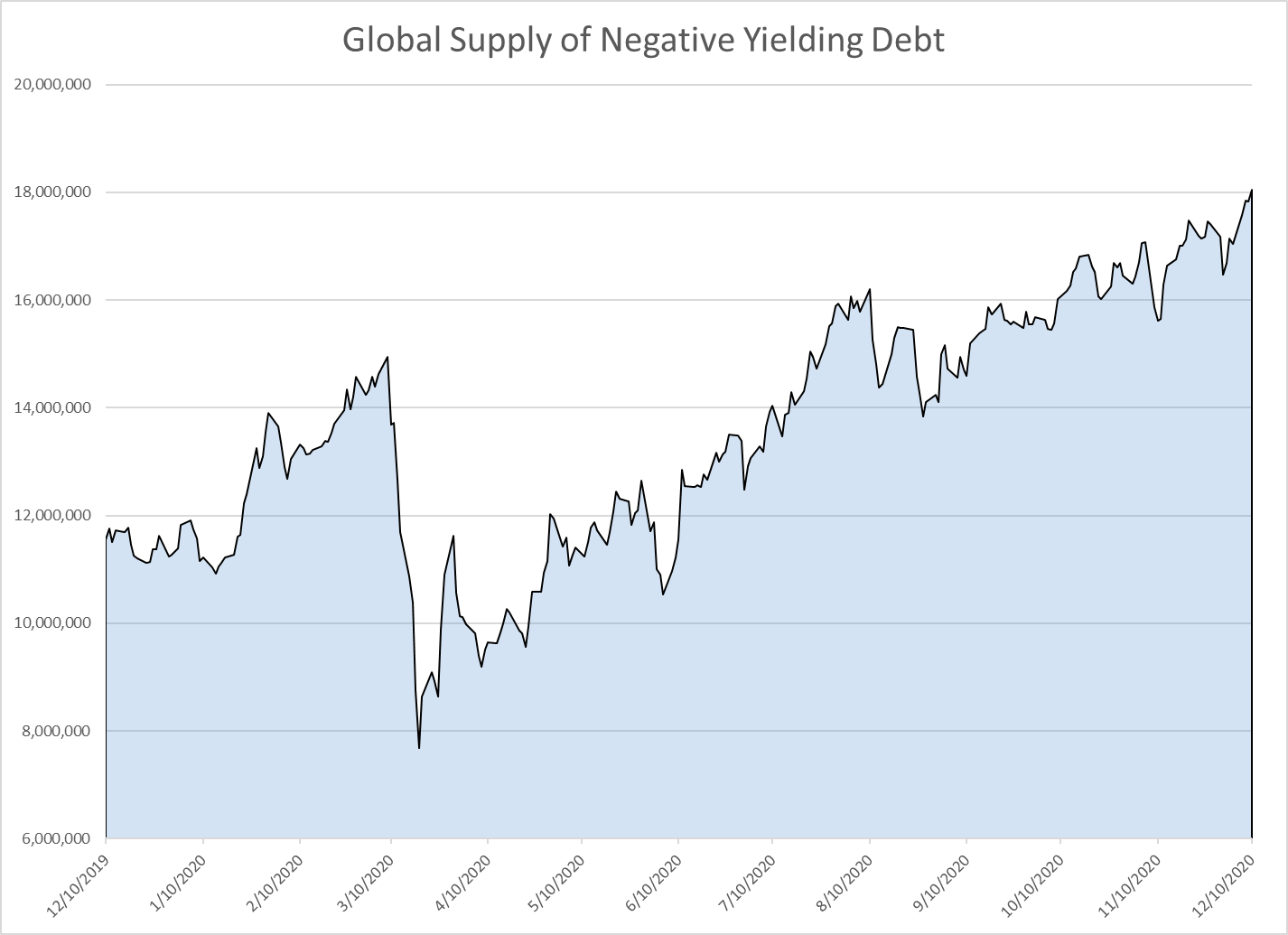

One area where we do not expect much uncertainty is the U.S. Treasury market – we expect rates will be rangebound in 2021. In addition to the Fed’s QE program, foreign investment in Treasuries remains robust thanks to negative interest rate policies from both the European Central Bank and Bank of Japan. Despite the rise of U.S. rates of ~60 basis points (bps) from the lows of March, the index of negatively yielding debt sits at an all-time high of an eye-popping $18 trillion.

Source: Bloomberg

Moreover, we feel that any near-term rise in rates will be countered by the modern-day version of QE2 (Operation Twist) – in the form yield curve controls and extension of the weighted average maturity of the Fed’s portfolio. Still, any progress toward normalization of the economy should bring longer rates higher. We currently face a yield curve that is entirely below the Fed’s inflation target of 2%, and the TIPS market affirms the view that the government will have some ability to effect a rise in inflation as all real yields are negative. It seems likely that significant fiscal stimulus will be required to meet this inflation target – something that the Fed itself cannot deliver.

2021 Challenge: IG Credit and MBS Priced to Perfection

Like other IG bonds, the spread on the Bloomberg Barclays Investment Grade Corporate Index has essentially returned to pre-Covid levels. The market experienced a sharp selloff in the early days of the pandemic, but sentiment quickly reversed in March when the Fed announced its bond buying program.

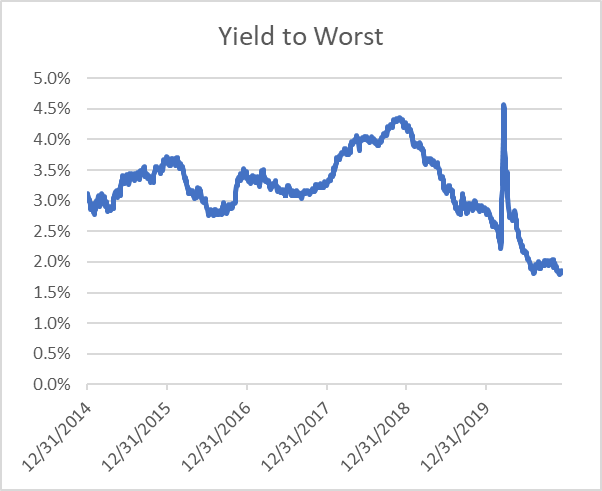

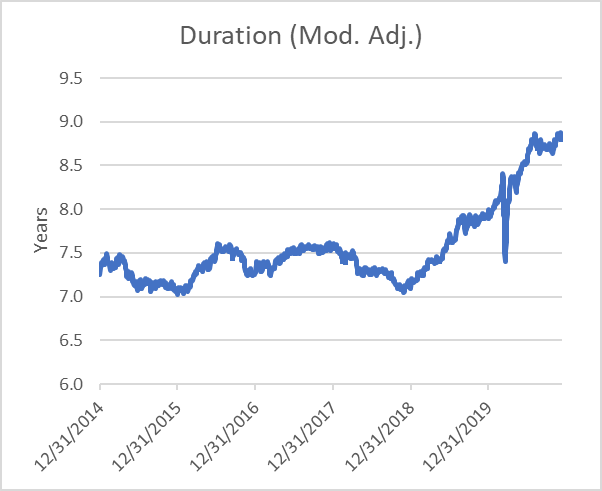

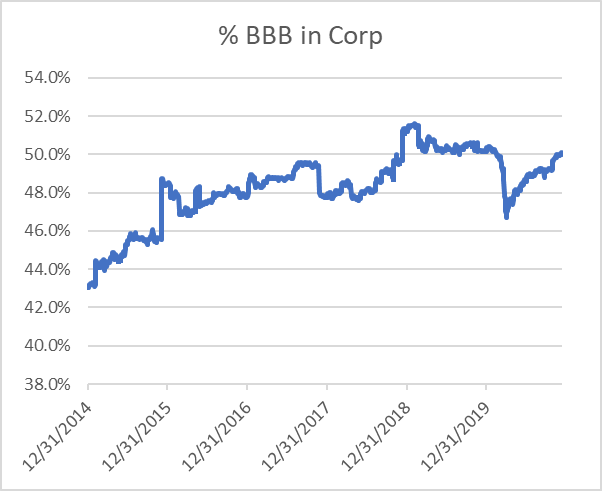

We believe the IG market will be difficult to navigate in the new year as investors will have very little margin for error. The corporate index is hitting record low yields with dollar prices hitting close to historic highs, duration continues to expand as corporates have termed- out debt, and the percentage of BBB credits in the index continues to remain at elevated levels. Thus, investors are left in a position in which they are taking more credit risk (higher concentration of BBBs), duration risk, and default risk (high dollar price) while yields are near historic lows.

| KEY METRICS: IG CORPORATE INDEX |

|---|

Source: Bloomberg

We see a similarly challenging market in MBS. Most of the index is comprised of higher coupon pools which are largely refinanceable at current mortgage rates. Further, the Fed has concentrated its purchases in new pools which are comprised of loans originated at lower interest rates. They have also engineered an unusual technical condition in which mortgage investors can purchase these lower coupon pools synthetically by purchasing To Be Announced (TBA) contracts instead of pools.

At the last FOMC meeting the Fed stated that they will continue the current pace of Treasury and MBS purchases. As a result, we believe that both assets classes will benefit going forward, but we also see a scenario where Treasury supply grows at a faster pace than MBS supply to fund the expanding federal deficit. Additionally, MBS continues to maintain a spread and carry advantage over Treasuries with a substantially shorter duration profile, thus giving MBS a more attractive risk reward profile.

When comparing MBS against IG Corporates, we continue to believe that both currently sit at the tighter end of valuations. However, for as much as IG Corporates have tightened since March, they continue to maintain their spread advantage over MBS.

A Deeper Dive Into Credit: Fundamentals Improving

Although the spread of the corporate index is already near its all-time tight level, we expect it will tighten further in 2021. Specifically, we expect the widest sectors to tighten disproportionately and the tighter sectors to stay rangebound – driving the overall index tighter.

In our view, the spread dispersion within the index is the key to outperforming in 2021, although we anticipate total returns will be lower than last year. Also, we believe 2021 will be a period in which we expect to create as much value from the securities and sectors we avoid as from those we select.

We think the fundamentals of corporates should improve as the vaccines are distributed and economic activity returns. During the pandemic, EBITDA fell due to shutdowns and companies were forced to borrow to shore up balance sheets. Thus, gross leverage increased as corporates rushed to raise cash in the debt markets, maintaining a defensive posture. According to Barclays, gross leverage for U.S. non-financials increased to 4.0x, which is historical high. Yet, net leverage (leverage calculated net of cash) of corporates only grew 0.2x given how much cash remained on balance sheets.

Moving forward, EBITDA growth is expected to be around 15%, roughly 6% above 2019 levels, by Barclays estimates. This presents both an opportunity and risk to investors. As corporate cash hoarding becomes less essential, the use of that cash comes into question. We expect IG corporates with BBB ratings to pay down debt (see next section for more) in order to bring balance sheets back to pre-pandemic levels, and we think there is a high likelihood that better-rated issuers may maintain elevated levels of leverage, with the cash being used for equity payouts and M&A.

Fewer Fallen Angels

In 2020, there were several high-profile fallen angels – names with large weightings in the index that were downgraded from investment grade to high yield. All such firms were known to be at risk even before the pandemic, and ultimately the Covid-19 lockdowns pushed them over the edge.

Looking forward to 2021, we do not anticipate anywhere near the same volume of downgrades. Our rationale is based upon the fact that three of the most vulnerable names have already fallen out of the index and IG companies have had great opportunities to shore up their balance sheets during the recovery. Our view is supported by how the market is currently pricing this risk, as only $26 billion of BBBs (out of the entire $7 trillion IG market) is currently trading at BB levels.

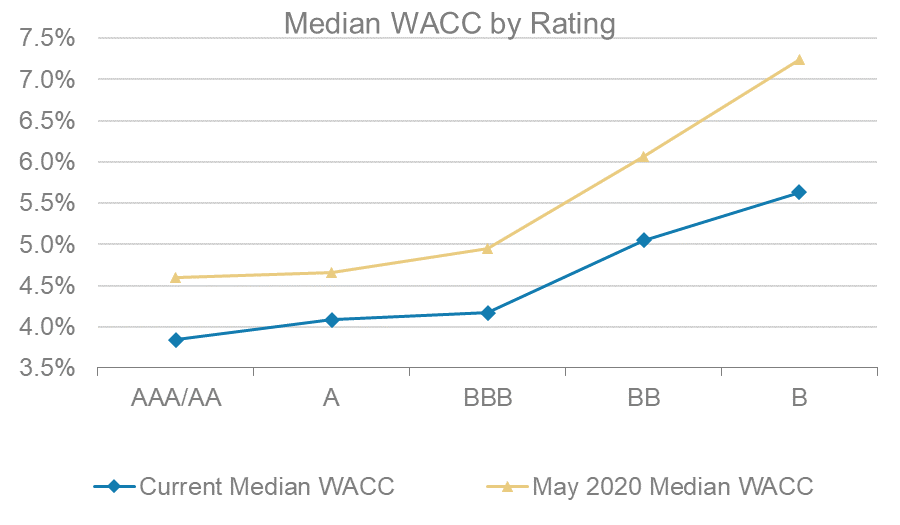

Another reason we expect to see fewer fallen angels is that issuers are highly incentivized to remain in the IG universe. As per the Morgan Stanley chart below, the weighted average cost of capital (WACC) curve shows a steep cost of moving from BBB to BB. Companies do not want to lose access to cheap financing, as it provides maximum flexibility, particularly in uncertain economic times. This is also why we believe that most BBB companies will use the excess cash on their balance sheets to pay down debt rather than use the funds for share buybacks or dividend payouts. They need to keep their leverage ratios in line with other BBB issuers to remain investment grade.

Source: Morgan Stanley

However, we will not be surprised to see more companies allow themselves to fall from A to BBB. As the above chart shows, the WACC curve remains relatively flat between those two rating grades, which incentivizes higher rated companies to maintain or even increase their leverage.

Supply Should be Materially Lower, But Exceed Expectations

One of the most compelling reasons to be long credit in the coming year is that the market is expecting a dramatically reduced supply of new bonds. In 2020 IG companies issued nearly $2 trillion of debt, setting an all-time record. The consensus expectation across the Street is calling for a gross supply of ~$1.25 trillion and net supply of ~$500 billion. Those supply numbers would represent a reduction of a third and a half, respectively. Additionally, as we mentioned above, we expect to see an uptick of liability management transactions of tenders and exchanges in the BBB cohort, which we see potentially reducing supply further.

At the same time, we think the consensus estimates of new issuance are likely too low. As we consider issuer behavior in the current low yield environment, our favorite Oscar Wilde quote comes to mind: “they can resist all things but temptation.” In our view, the levels where issuers can access the capital markets right now are likely too attractive for CFOs to pass up.

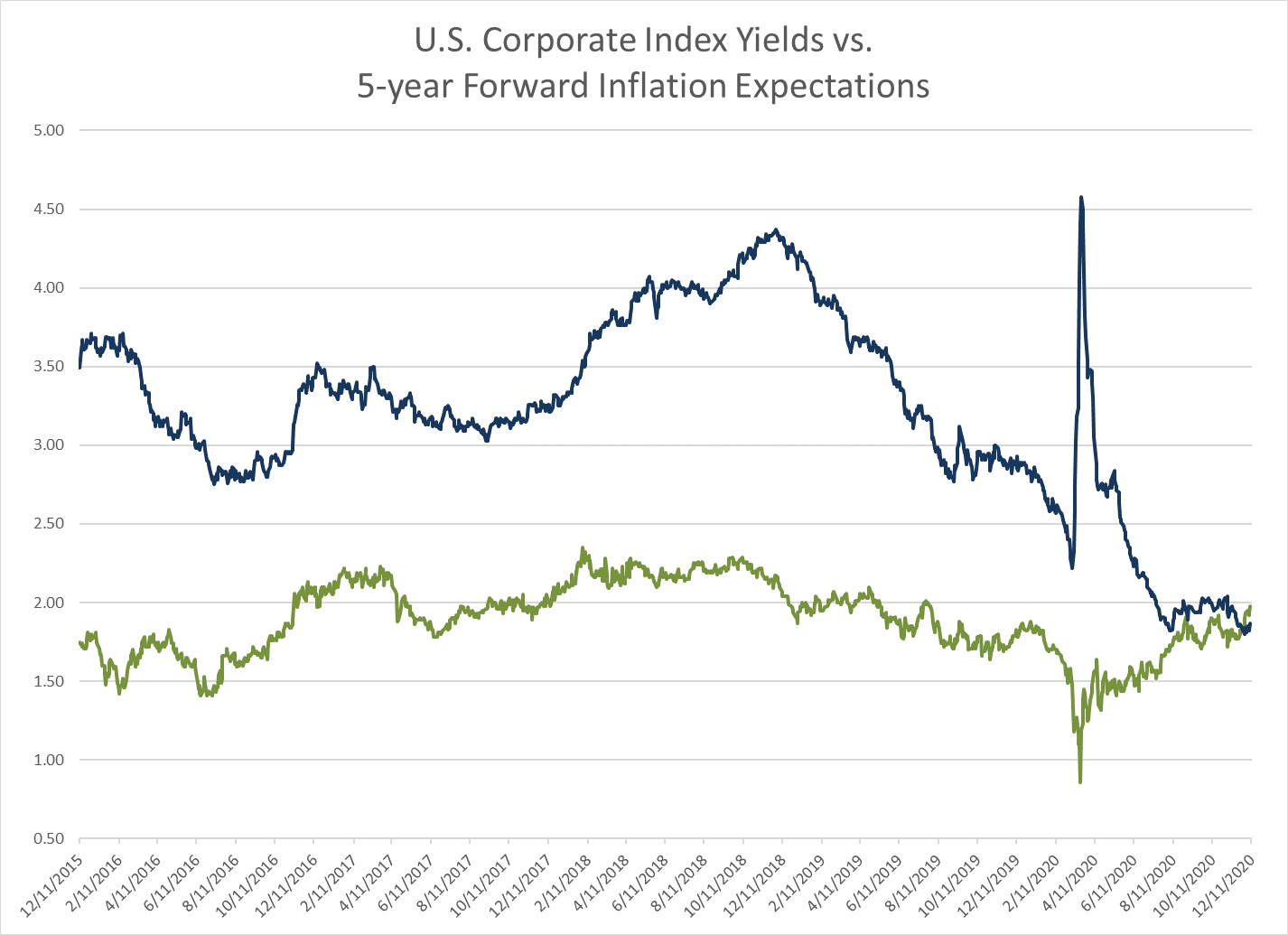

The borrowing conditions are exceptional – in addition to historically low interest rates, we are entering a period of rising inflation expectations. As the graph below shows, the current yield of the Bloomberg Barclays U.S. Corporate Index is now below the U.S. Fed 5-year forward inflation expectation rate. In other words, the average IG corporation can now raise money at negative real yields! We think this will drive issuance above the Street’s current estimates, though we still do not expect it to approach last year’s pandemic-induced borrowing frenzy.

Source: Bloomberg

Global Demand Remains Robust

In addition to reduced supply, we remain very constructive on the strength of demand for IG credit in 2021. As discussed above, we have synchrony among the three major central banks (Fed, ECB, and BOJ) coupled with meaningful fiscal stimulus. This has depressed yields around the world, driving foreign investors to the U.S. markets. While domestic IG grade yields are historically low, on a relative basis they are still very attractive. For example, in Europe 36% of IG corporate bonds trade at negative yields. To put the U.S. IG market into perspective, domestic corporates make up just 13% of total investment grade bonds outstanding globally, but they pay 41% of their yield. Lastly, the cost of hedging USD currency exposure has fallen for European and Japanese investors. We expect substantial overseas demand as buying long duration USD IG credit on a currency-hedged basis remains attractive.

Another impact of the unprecedented amount of liquidity injected into the financial system is that there is a high level of balances in money market funds (MMFs). We think the rotation out of cash into products with higher yield will continue. With inflation expectations at 2% and MMFs returning close to zero, the inflation-adjusted cost of sitting in cash the highest that it has been in years.

We think the global landscape of low/negative yields will continue to drive demand for U.S. IG from overseas investors. Likewise, the U.S. Treasury curve is steeper than Euro and Yen government curves so the incentive for overseas buyers to extend out the curve in U.S. corporates is an added driver of demand.

Our Strategy: Buy Wide, Avoid Tight

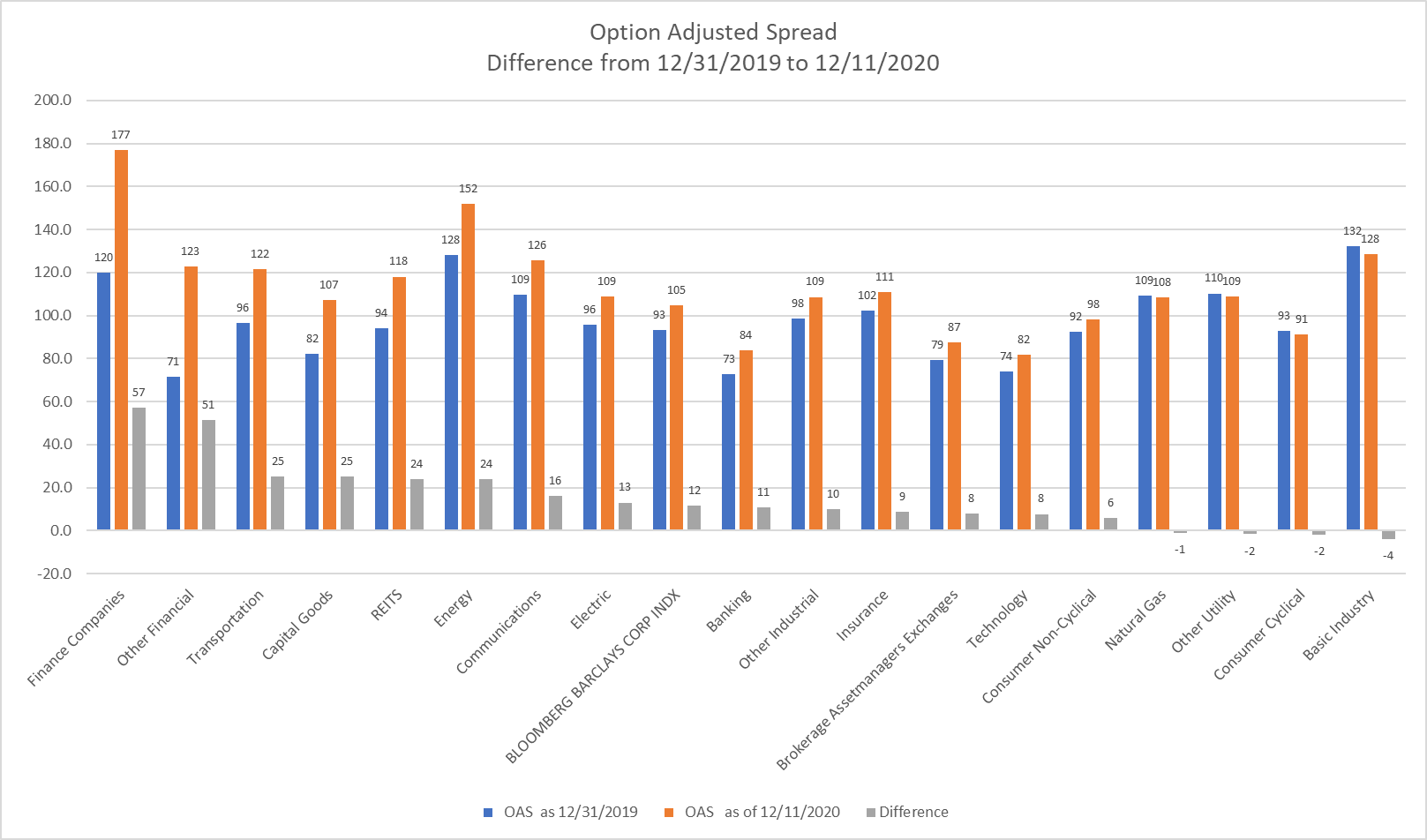

Although the current spread of the IG index is comparable to its pre-pandemic level, there remains significant dispersion among the individual sectors within the index.

Source: Bloomberg

Currently, we are focusing on sectors with the widest spreads, including financial companies and transportation. We find considerable relative value in these sectors, as we have identified issuers with improving fundamentals that are proactively terming-out debt and beginning to de-lever through tenders. We also like the wider sectors because they are comprised primarily of BBB names, which we believe reduces our potential exposure to ratings downgrades and spread widening.

We are proactively avoiding sectors that have tight spreads, which we believe have little room to tighten and at best present additional carry. These sectors are priced to perfection, leaving minimal upside but plenty of downside. As mentioned above, we also believe some of these issuers are likely to allow themselves to be downgraded to BBB in order to optimize their balance sheet, which would be detrimental to current debt holders.

Final Thoughts: 2021 Portfolio Positioning

As we consider the various challenges and opportunities in 2021, we remain modestly bullish on IG credit and plan to maintain an overweight to that sector. Likewise, we feel Agency MBS are likely to do well in the new year, and we will also maintain an overweight to that sector. Within MBS, we prefer lower coupon securities that have higher yields, less prepayment risk, and a tailwind provided by the Fed MBS market “squeeze.”

We plan to remain underweight Treasuries with an opportunistic allocation, generally when spread rallies are exhausted, within the 5-7 year part of the curve as it’s the most attractive at this time. There is significant carry and roll-down in the intermediate part of the Treasury curve without taking the substantial duration risk of Treasuries with more than 10-years to maturity. Treasuries also figure to get a boost from yield curve controls, which we believe are likely to be incorporated in the first half of the year, as the Fed may lose patience with weaker inflation data or an economic recovery stunted by employment stagnation. We will likely maintain some duration exposure as that process plays out.

© Osterweis Capital Management