Our K2 Advisors team is optimistic about the opportunity set in the year ahead, and thinks that active management alpha will be key to success in 2021. Brooks Ritchey and Robert Christian provide the team’s first-quarter hedge-fund strategy outlook.

Strategy Highlights

Long/Short Equity

Long/short equity managers have been resilient on a year-to-date basis. While stocks are trading at high valuations, we believe there are still asymmetric dispersion opportunities that could lead to incremental alpha generation in particular areas of the market.

Relative Value

Favorable outlook for volatility arbitrage and convertible arbitrage strategies driven by persistent inefficiencies in pricing among various asset classes. Negative outlook for fixed income arbitrage based on depressed volatility due to excess central bank liquidity.

Event Driven

Neutral outlook for merger arbitrage, as spreads for “safe” deals have been tightening. Attractive opportunity set remains in the more complex merger situations as well as special situations equity and credit investing where manager experience is more likely to produce superior outcomes.

Credit

Long/short credit managers are increasingly focused on event-driven situations given low yields and tight spreads. Uncertainty in structured credit may lead to high levels of dispersion at the instrument, market and manager level.

Global Macro

As the macro shocks of the last year appear to be normalizing, fundamental dispersion between regions, countries and asset classes may become an increasingly important driver of returns. Managers focused on this dispersion, particularly within emerging markets, may benefit from a rich opportunity set in the year ahead.

Commodities

The global economic recovery is supportive of increased commodity demand across sub-strategies. As supply-demand tightens into 2021, volatility is expected to increase and favor relative value strategies.

Insurance-Linked Securities

Both insurance and reinsurance pricing trends are positive as higher-than-average natural catastrophe insured losses, broader industry COVID-19-related losses and low interest rates result in higher pricing across the sector including ILS strategies.

Macro Themes We Are Discussing

Will inflation expectations continue to rise given vaccinations, global financial conditions and expected economic growth?

The start of 2021 offers a new beginning in the sense that the economic slowdown due to COVID-19 appears to be coming to an end. Individuals and corporations have been buoyed by enormous stimulus from governments, and for the most part, have weathered the storm of 2020. Structural trends of e-commerce, deglobalization of supply chains, health care, security, software and sustainability were accelerated due to the economic environment and global lockdowns.

Going forward, if economic growth, earnings and sentiment overreact to the upside in speed and magnitude, inflation will inevitably surface. However, we could have a period of reflation without inflation, which would be very favorable for equities. Conversely, there are many paths to a derailing of the recovery such as failed vaccination implementation, a mutated virus, a sustained second wave or even another global lockdown.

Currently, the markets are quickly moving to price in perfection, reflation with minimal inflation and a robust global economic recovery. We expect challenges to this pricing to arise periodically over the course of 2021, keeping volatility and dispersion elevated and creating rich opportunities for active management.

Will the global chase for yield continue but deemphasize sovereign fixed income in favor of alternative yield products?

Many assets are priced to a flat forward curve, putting a high premium on forward cash flows. If the forward curve were to rise (steepen), a repricing downward of these duration assets would be expected in 2021. Given that real interest rates are historically low, we expect sovereign fixed income to be challenged and for interest rates to eventually rise. Investors that are yield- and income-centric will most likely have to rotate into alternative yield products such as ILS that provide yield for taking on insurance risks.

Dispersion in credit markets coupled with the need for yield should also provide a good opportunity for long/short credit managers and dispersion trading as many industries and companies are disparately dependent on a speedy recovery. We expect that the bigger, stronger companies will be very active in strategic business dealings to further strengthen their advantages over weaker competitors.

Will emerging markets recover faster than developed markets?

If the global recovery is strong and fast, commodities should experience dispersion due to supply/demand dynamics, and emerging market (EM) risk assets could follow suit. That is especially true in countries exporting commodities and those that have already dramatically devalued their currency. Additional fuel to these dynamics would be a weakening US dollar.

Finally, global yield hunters should be enticed by the developing market’s yield premium in fixed income. As a result, we find both EM equities and foreign exchange attractive on a relative valuation basis.

With that said, investors do have to be selective in EMs due to challenges of operating in these countries. EM companies face challenges from foreign companies entering their markets, ongoing global trade tensions, and vaccination distribution challenges. In addition, fiscal and monetary stimulus has been led by developed markets relative to EM counterparts.

Summary for 2021

As we enter 2021, we are very optimistic about the opportunity set while recognizing that our views are based on a swift global recovery that is becoming consensus among allocators. Our underlying hedge fund managers are identifying many opportunities, both on the long and short side, and think that active-management alpha will be key to success in 2021 as beta-driven momentum slows. With data throughout the year, we will be constantly challenging our own thinking and making adjustments as necessary. As a result, we believe it is prudent to be growth-oriented in our portfolio positioning while also holding hedged alternative investments that exhibit low correlations to broader risk assets.

First-Quarter 2021 Outlook: Strategy Highlights

Long/Short Equity—International

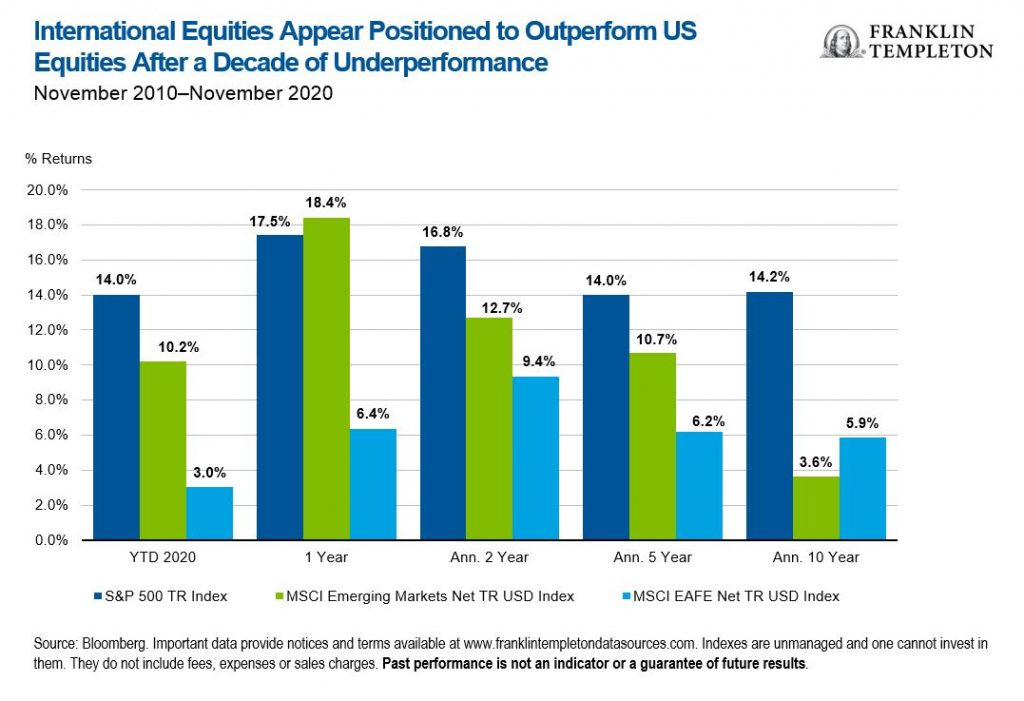

Given the impressive recovery of US equities since the first quarter, we believe that international long/short strategies are poised to outperform. European and Asian markets have generally traded in tandem with the United States throughout the COVID-19 pandemic, but foreign companies, as captured by the MSCI EAFE Index, have consistently underperformed their US peers over the last decade.

Moreover, non-US equity markets could be further buoyed by their natural bias toward cyclical and value-type names in contrast to US market reliance on the overstretched technology sector and growth companies more broadly. In addition to non-US developed markets, we believe emerging markets may outperform. The reopening of local economies should benefit their respective economically sensitive industries, and any incremental stimulus in the United States should weaken the US dollar.

More importantly, EM countries are in a strong fundamental position given the creation of long-term wealth through a rising middle class and more recently, less reliance on fiscal support during the pandemic.

Macro—Emerging Markets

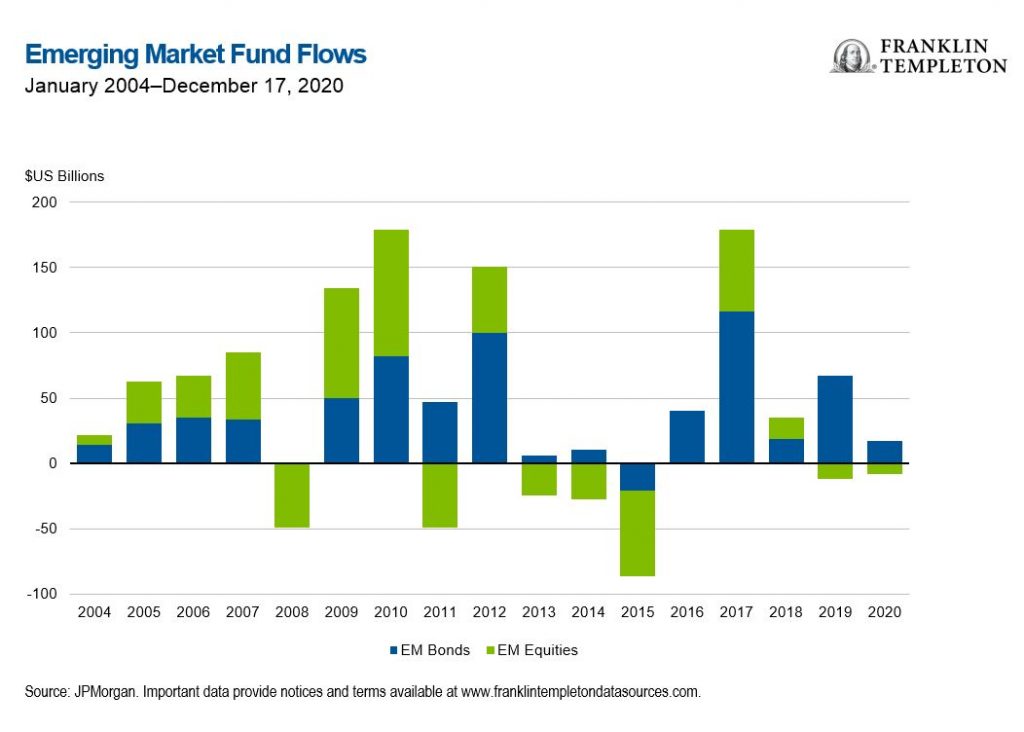

Emerging markets may benefit from a confluence of rebounding growth, sustained policy support, and improving fund flow dynamics. Many investors reduced their exposure to growth-sensitive emerging market assets in the wake of the pandemic. If recent momentum in the recovery persists while policy remains accommodative, these regions may see a resurgence of interest. Macro specialists focused on emerging markets may benefit from these tailwinds as well as wider dispersion in country and asset-class performance in the wake of the last year’s crises and divergent policy responses.

Insurance-Linked Securities

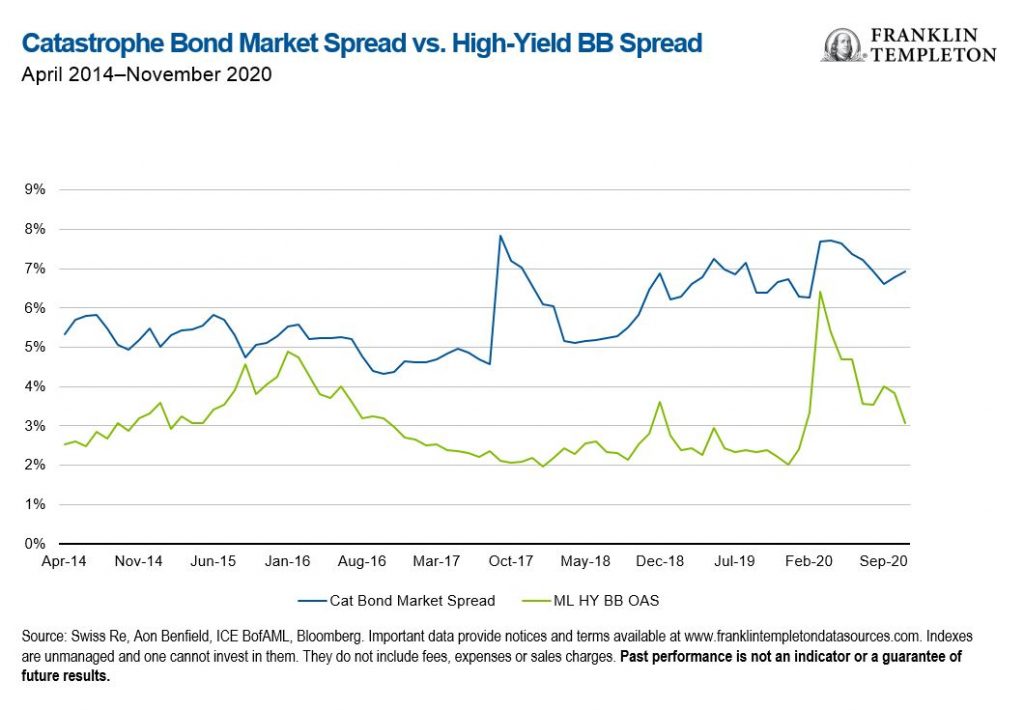

Swiss Re Institute estimates natural catastrophe events caused $76 billion of global insured losses in 2020, 6.6% above the previous 10-year average. While 2020 resulted in a record number of North Atlantic named storms (30), US hurricane-insured losses were much lower than 2005 and 2017 stress years as 2020 landfalls were in lower-insured, less-populated areas.

Willis Towers Watson estimates an additional $32 billion to $80 billion of insured losses from COVID-19, which is supporting higher pricing across the insurance industry. Cat bond spreads remain attractive versus US corporate high yield as we enter a lower-risk part of the ILS calendar prior to the next US hurricane season in June 2021.

What Are the Risks?

All investments involve risks, including possible loss or principal. Investments in alternative investment strategies and hedge funds (collectively, “alternative investments”) are complex and speculative investments, entail significant risk and should not be considered a complete investment program. Financial derivative instruments are often used in alternative investment strategies and involve costs and can create economic leverage in the fund’s portfolio which may result in significant volatility and cause the fund to participate in losses (as well as gains) in an amount that significantly exceeds the fund’s initial investment. Depending on the product invested in, an investment in alternative Investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. There can be no assurance that the investment strategies employed by K2 or the managers of the investment entities selected by K2 will be successful.

The identification of attractive investment opportunities is difficult and involves a significant degree of uncertainty. Returns generated from alternative investments may not adequately compensate investors for the business and financial risks assumed. An investment in alternative investments is subject to those market risks common to entities investing in all types of securities, including market volatility.

Also, certain trading techniques employed by alternative investments, such as leverage and hedging, may increase the adverse impact to which an investment portfolio may be subject.

Depending on the structure of the product invested, alternative investments may not be required to provide investors with periodic pricing or valuation and there may be a lack of transparency as to the underlying assets. Investing in alternative investments may also involve tax consequences and a prospective investor should consult with a tax advisor before investing. In addition to direct asset-based fees and expenses, certain Alternative Investments such as funds of hedge funds incur additional indirect fees, expenses and asset-based compensation of investment funds in which these alternative investments invest.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the date of publication and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

The information in this document is provided by K2 Advisors. K2 Advisors is a wholly owned subsidiary of K2 Advisors Holdings, LLC, which is a majority-owned subsidiary of Franklin Templeton Institutional, LLC, which, in turn, is a wholly owned subsidiary of Franklin Resources, Inc. (NYSE: BEN). K2 operates as an investment group of Franklin Templeton Alternative Strategies, a division of Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Investments are not FDIC insured; may lose value; and are not bank guaranteed.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments