U.S. Economic Outlook, February 2021

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsHopes for a quiet start to 2021 were quickly dashed amid unrest in the nation’s capital, progress toward substantial stimulus, a surprising 50-50 Senate outcome, and a mix of excitement and frustration over COVID-19 vaccine availability. While we hope this year will be less volatile than 2020 was, January was anything but relaxing.

We start the year without much economic momentum. Indicators on hiring and retail sales show a slowdown. But real growth is likely to accelerate as the year progresses. Additional stimulus will help to move consumers and businesses past this difficult interval, and additional inoculations will help consumers return to their old spending habits. A robust recovery in demand across all sectors will support ongoing employment gains during the balance of 2021.

In the cold and dark months of winter, it is helpful to envision better days to come. At the moment, we continue to ride out the effects of the pandemic patiently.

Influences on the Forecast

- The most important way to continue the recovery is to achieve widespread distribution of COVID-19 vaccines. Greater inoculation will allow officials to relax restrictions and also mitigate the risk of new viral mutations. More federal stimulus to support vaccination will have a fast and rapid multiplier effect as more people can return to normal economic activity. We expect substantial progress toward broad immunity by the middle of the year, setting the stage for an interval of strong growth in the second and third quarters.

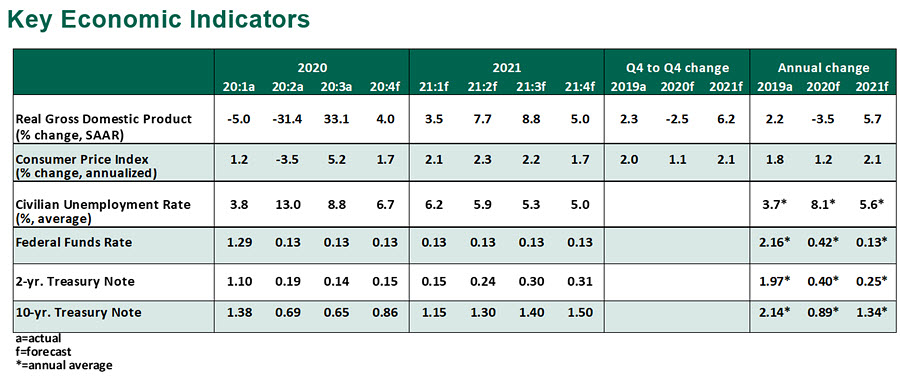

- Recent employment reports gave clear evidence of the slowdown caused by elevated COVID-19 infections. Only 49,000 jobs were created in January, following a loss of 227,000 in December. The unemployment rate fell to 6.3%, partly due to a decline in labor force participation. Total employment remains 8.7 million workers below its peak in February 2020. Weekly initial unemployment claims, persistently elevated since the first COVID shock, surged again at the start of the year; total participation in unemployment programs is hovering around 18 million claimants. Further recovery for labor markets will depend on demand recovering across all sectors.

- Real gross domestic product (GDP) grew by an annualized 4.0% in the fourth quarter, a stark slowdown from the 33% rate of recovery in the third quarter. Consumption growth of only 2.5% shows demand remains suppressed. Consumer spending will be the key that unlocks the recovery.

- The $900 billion compromise stimulus package passed at the end of 2020 is helpful for avoiding worst-case outcomes. The blanket $600 economic impact payments aided consumers on the margin; while some recipients do not need the money immediately, it will fuel additional consumption later in the year. After receiving no federal support for five months, unemployed workers are now receiving an additional $300 per week, and the return of the Paycheck Protection Program will keep some small businesses afloat.

- Before taking office, President Biden unveiled the American Recovery Plan proposal. Key features include greater vaccine funding, a $1,400 one-time economic impact payment, extended unemployment support and longer protections against evictions. Final deliberations are underway, but Congress appears ready to pass the bulk of the proposal, with potentially minor revisions to income cutoffs for one-time payments. The additional funding will support even more consumer spending in the middle of the year, and our forecast has been revised to include its likely passage. Further funding for infrastructure projects may also support growth in the year ahead.

- Despite the holidays, most categories of retail sales fell in December. And the emergence of more contagious strains of COVID-19 gives reason to fear another round of infections that will weigh on activity in the months to come.

- Dislocated demand continues to keep prices in check. The consumer price index (CPI) rose by only 1.4% year-over-year in December, while the deflator on core personal consumption expenditures grew by 1.5%. Sudden surges in demand at mid-year may drive some temporary price increases, but they will be met by surges in supply that will allow inflation to return to its typical growth.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All