About a week ago, an unprecedented polar vortex descended upon the southwestern United States. The deep cold forced power plants in Texas to take production offline, leading to rolling blackouts and leaving more than four million households without power. Simultaneously, demand for power rose significantly as residents attempted to heat their homes, which created a significant imbalance in the market and drove power costs sky-high. As of Friday morning, February 19, power had returned to much of the state, but significant water safety concerns remain for about 13 million Texans.i This systemic market failure can be attributed to a number of factors:

- Abnormally cold temperatures froze critical infrastructure at natural gas, coal and nuclear facilities, many of which were not winterized to withstand such temperatures.

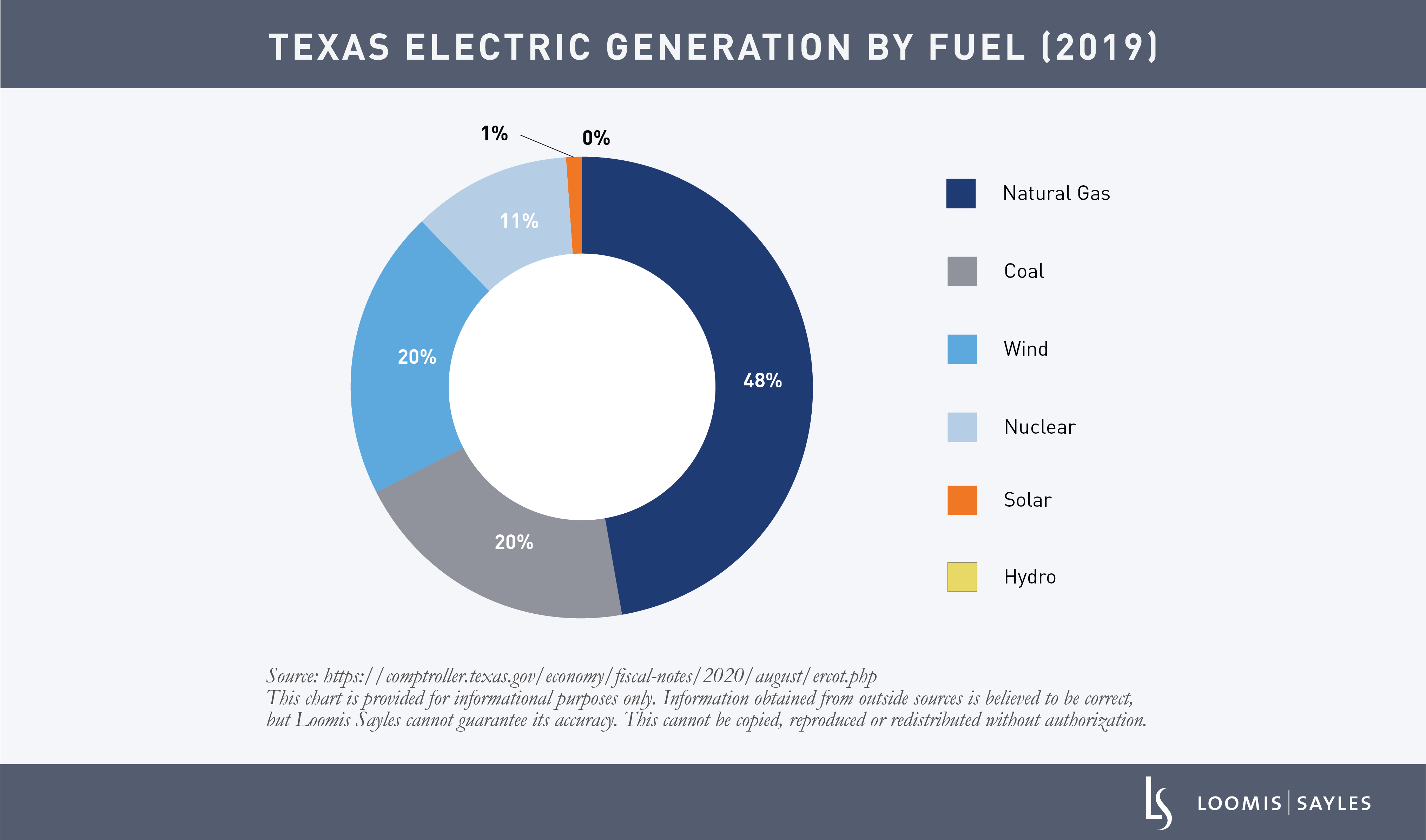

- Snow and ice rendered renewable energy resources such as wind turbines and solar panels largely inoperable. Texas, typically one of the warmest states in the US, hadn’t equipped its turbines with cold-weather tools such as heating mechanisms or lubricants.

- Texas’ power grid operates through the Electric Reliability Council of Texas (ERCOT), which allows utilities to buy and sell excess power into an integrated market. ERCOT, however, differs from other regional independent system operators in that it lacks connectivity to other states. This has isolated the market and created supply constraints in Texas.

Tools to weather the storm

Texas municipal power providers are likely to feel pain on multiple fronts. Although demand has increased, revenues will likely be temporarily disrupted since providers are unable to consistently deliver power. For utilities that need to purchase additional power to meet demand, increased power prices will pressure expenses until the market is back in balance and functioning properly. However, municipal power providers possess several mechanisms to help weather volatility. They tend to benefit from unregulated rate-setting capabilities that can allow cost recovery to help recoup lost profitability.

Historically, these cost recovery mechanisms have led to solid liquidity and coverage metrics, providing an additional financial cushion for municipal power providers. Retail providers in Texas have an average of 253 days cash on hand and debt service coverage of 3.1x, while wholesale providers have an average of 360 days cash on hand and debt service coverage of 1.8x.ii Utilities may have to dip into reserves, but I expect credit implications to be temporary. FEMA is providing aid, the inclement weather is subsiding, and the power market should stabilize.