The Great Jobs Reset

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsInterest Rates, Federal Reserve, and Unemployment

Tough Job Market

Skill Mismatch

Permanent Changes

The Incentives of Unemployment

Puerto Rico

We are almost through February and (knocking on wood) the US COVID-19 situation is improving daily. The B117 and other variants haven’t yet made a big impact. Possibly they will, but as time passes more people are getting at least partial protection through vaccines. The “race” I’ve described seems to be going the way we hoped.

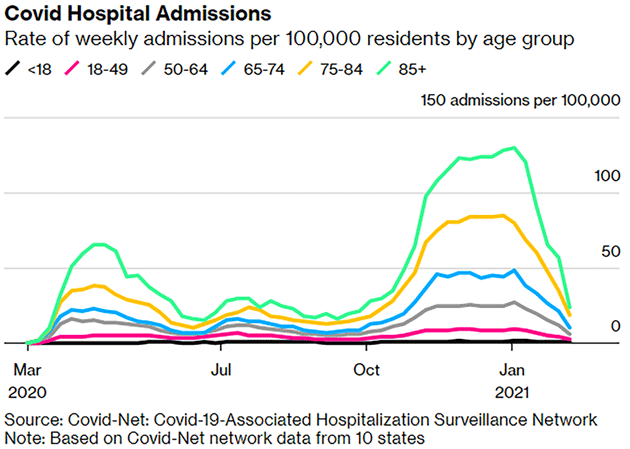

In the US, hospitalizations for those age 85 and older dropped 81% from January to February, according to Bloomberg. This chart below summarizes data from 10 states.

Source: Bloomberg

Another case surge, variant-driven or otherwise, shouldn’t be as deadly since so many vulnerable and older people have been vaccinated. The vaccines appear extremely effective at minimizing severity even when they don’t stop infection. And the fact that every age group—including those who haven’t yet been offered vaccines—is seeing lower hospitalizations is very encouraging.

If this continues, and we all hope it does, it means we can start looking ahead to the other side of all this. By no means have we reached the other side. It is not yet time to relax. Nevertheless, it looks like we can, as President Biden has said, “approach normalcy” by year-end.

But that raises a question: What normalcy will it be? I don’t expect to simply go back to the way things were. The economy as it was structured in December 2019 is gone forever. The world is different now. The economy will be different, too.

We’ll see this in myriad ways but in this letter I’ll focus on just one: jobs. That is the key way in which most people participate in the economy. How they do it matters. And, as you’ll see, many will do it in new and different forms.

Interest Rates, Federal Reserve, and Unemployment

The Federal Reserve is primarily focused on unemployment and not inflation, according to numerous officials and Jerome Powell. They are willing to let the economy “run hot.” That means tolerating higher inflation for some period while they try to reach what they consider “full employment.”

However, as is so often the case in government, the left hand is not working with the right hand. The bond market has not been happy the past few weeks. Last week’s Treasury auctions were ugly. The “yield to cover” was the worst in history.

Below is the seven-year yield (courtesy of Peter Boockvar)…

Source: Peter Boockvar

Yes, yields are up significantly since the summer lows but are roughly where they were a year ago. The recession and pandemic pushed yields down and the market is beginning to suggest recovery. Yet the Fed says yields should stay low.

This “battle” is important. From 1966 to 1997 inflation was the primary driver of the markets. In general, the bond market and the stock market moved in opposite directions. Starting in 1997–8 up until (maybe) this week, they mostly moved in tandem. If we see what The Bank Credit Analyst calls a regime change, where once again bond yields and stocks diverge, that means that as rates go up, the stock market will fall.

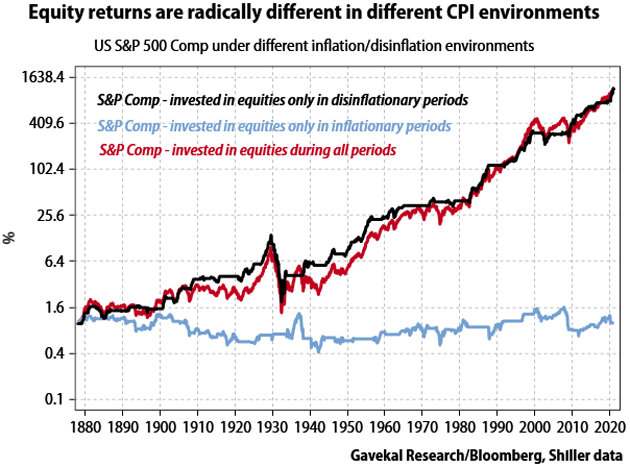

There is a marked difference between how the stock market performs in periods of disinflation versus inflation. This chart from Charles Gave at Gavekal shows how basically all stock market returns for the last 140 years came in disinflationary periods. Quoting Charles:

All—and we mean all—of the excess returns from owning US equities in the last 142 years came in disinflationary periods, while no excess returns were achieved during the inflationary times.

Source: Gavekal

I have written about this in the past. The “regime change” is exactly what the Federal Reserve does not want to happen. A few days doesn’t make a trend. But if this goes on for weeks? Will we see the “bond vigilantes” rise from the dead?

The single biggest danger to the stock market is that the Federal Reserve in particular and central banks in general, “lose the narrative.” When the market stops believing the Fed can control interest rates and influence markets, we enter a scary new world, and likely a bear market for stocks.

This is something the Fed can’t allow. A few more weeks of rising interest rates in the face of $120 billion per month of Federal Reserve purchases will force Fed officials (at least in the opinion of your humble analyst) to take action. The last thing they want is actual Yield Curve Control (YCC). That is akin to getting on the back of an angry tiger. While they may be able to ride it for a time, the dismount would make the taper tantrum look like a Sunday school picnic.

More likely, they will do YCC through the back door. They have several options. Right now they’re buying $40 billion per month of “agencies,” basically mortgage bonds. They can reduce the amount of agencies and increase their Treasury debt purchases, thus influencing the bond market. They can increase the amount of actual QE, which given the deficits that the government is running, may actually be necessary to control interest rates. And, I would rate it better than 50–50 odds they move out the yield curve to the 10-year bond. All of this will influence yields without actually invoking YCC.

The effect on unemployment? If rising rates spark a stock bear market (as happened in 2000), a recession could follow. That is by definition deflationary and would increase unemployment. Not what the Fed wants.

I did a webinar yesterday with Lacy Hunt, and we both basically took the deflation side of the future. But in summary, we acknowledged we could see inflation in the short term (i.e., starting soon and lasting until perhaps the end of the year).

Part of that “rise” in places is going to be easy year-over-year comparisons. Inflation dropped significantly with the onset of the pandemic, so year-over-year comparisons for March, April, and May will likely show annualized CPI inflation over 2% for the first time in almost 10 years. I think it will be transitory as the overall trend of the decade is going to be disinflationary/deflationary.

If you look back over two years, the inflation will not be apparent. But the markets focus on annual changes, which is why rates are rising. And that matters for the 17 million people who are currently on some type of unemployment assistance.

As we know, the pandemic and its many ramifications drove US unemployment to Great-Depression levels in a hurry. We have seen some improvement but it is still quite high—likely higher than the official data indicates.

Unfortunately, all our jobs data sources have limitations. Many look at weekly jobless benefit claims, which have the advantage of being high-frequency, but they also depend on state-level data collection, which varies (let’s just say that Texas and some southern states had an excuse last week, which showed up as lower initial claims).

Meanwhile, the “headline” unemployment rate only measures people who say they are looking for work. In this situation, many are not, for various reasons. Another confounding factor is the “birth/death rate” (of businesses, not people) the Labor Department uses to adjust its survey data. Millions have turned to freelancing not because of entrepreneurial dreams but for lack of better options. Other businesses closed, sometimes permanently and sometimes not. Sorting out all this in an economy as large as the US has always been difficult. It is impossible now. The methodology is simply broken as it is based on past trends which have no bearing on our current reality.

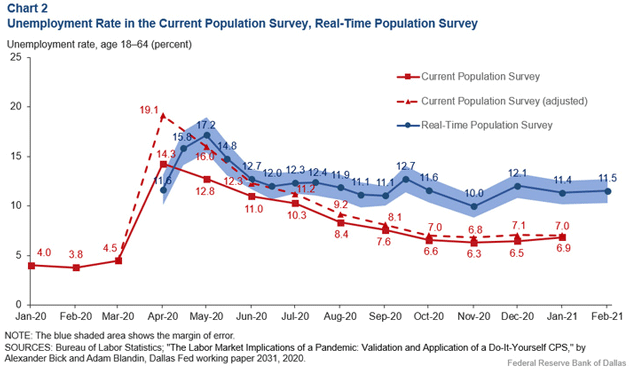

On top of all that are the usual problems with survey data. The unemployment rate comes from a Census Bureau collection program called the Current Population Survey. Its process is necessarily rigorous in order to be consistent over time. But these are not normal times. Researchers working with the Dallas Fed recently constructed an alternative Real-Time Population Survey (RPS) specifically to measure labor market trends. In the RPS methodology, January’s headline unemployment rate would have been 11.4% instead of the official 6.9%. It also peaked considerably higher and a month later in 2020 (17.2% in May vs. 14.3% in April).

Source: Dallas Fed

Of course, we should be wary about picking the data that “feels” right. But really, this seems a lot closer to reality when you look at unemployment claims and other similar surveys. It’s a tough, tough job market that doesn’t seem to be improving.

Nonetheless, it should improve once we get COVID-19 off our backs. But it won’t improve for everyone.

When we talk about returning to normalcy, many imply a simple return to pre-pandemic conditions. This seems unlikely to me. Many of the specific 10 million+ jobs that have been lost are not going to come back. But as an optimist, I believe other jobs will replace them and those 10 million people will find different employment. The problem is in the transition from here to there.

First, people will gain confidence at different rates. It will be a gradual process, not a sudden “reopening” like Black Friday used to be.

Second, many people will return with new attitudes. I would not assume mass events—concerts, sports, conventions—will regain their previous popularity in the short or medium term.

Third, probably most important, the pandemic brought innovations that affect how we work, and therefore the type and number of jobs the economy will support.

I’ll use myself as an example. I was one of the planet’s most frequent flyers, at least as measured by American Airlines. My business (at least I thought) required it and I actually enjoy it. I’m eager to fly again—but I won’t do it anywhere near as often. In the last year I learned how to hold online video meetings, accomplishing in a few hours things that would have once required two full days just for travel time, costing thousands of dollars in airfare, hotels, and restaurant meals.

Sometimes that’s what it takes, but as I learned, not as much as I thought. And I’m not the only one who learned this. The economy will need fewer flight attendants, hotel housekeepers, chefs, and so on. These occupations also account for a large part of the currently unemployed. Many, and perhaps most, will not be resuming that same kind of work.

By the way, business travel is different from pleasure\tourist travel. At some point, people are once again going to want to take vacations and weekend getaways. I think conventions will come back as they are efficient ways to see a lot of people in a short time. But not this year.

At the same time, demand is growing in some occupations. According to a recent WSJ report, jobs site Indeed.com is seeing above-average growth in postings for driving, warehousing, construction, and manufacturing jobs. These stem from two trends that predated the pandemic and were accelerated by it: a housing boom and e-commerce.

Our housing needs are changing, both in type and location, which creates new construction work. Concurrently, we are shopping online and having products delivered. This generates new warehouse and transportation jobs, even as it eliminates in-store salespeople.

The challenge is a mismatch between the kind of jobs that are available and the skills of those who need work. That’s not new; it has always been the case as economies grow and change. Now it happens faster. Someone who was a barista in 2019 might be a good framing carpenter, but will need retraining. This takes time and the transition period is often difficult.

These are relatively short-term problems, though. The Decade of Disruption is just getting started, and we haven’t fully grasped how the pandemic changed it.

I started with good news about virus fears receding this year. If that happens—and it’s not guaranteed—it doesn’t necessarily mean our economic challenges will recede at the same pace.

Back when all this started, George Friedman said the recession would turn into depression if it went on too long. The difference, in his view, is that a depression doesn’t just suppress growth for a while; it permanently changes everyday life.

Has that happened yet? Maybe not, but we aren’t yet through this. Even in the relatively optimistic scenario I now foresee, many small businesses are still months away from customers gaining enough confidence to return in significant numbers, even if the various health restrictions are lifted.

And beyond that, we just don’t know what kind of permanent lifestyle changes will come out of this. I mentioned travel, and that’s an obvious one. But I suspect other, less obvious changes are brewing. They will affect the employment picture.

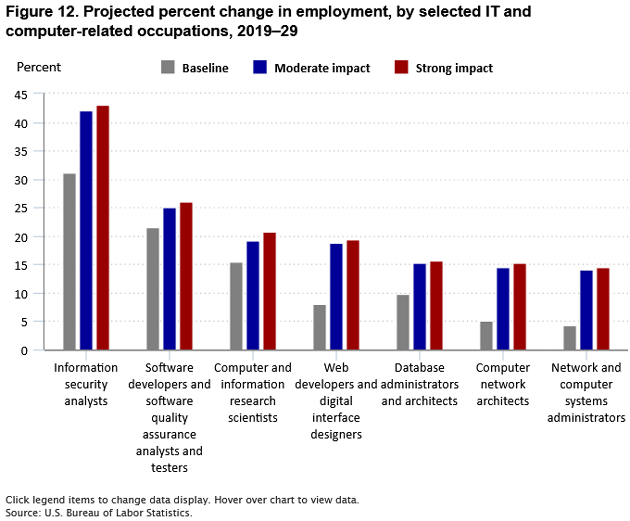

The Bureau of Labor Statistics—the same agency that reports the unemployment rate—periodically does a 10-year jobs forecast. Of course it requires many assumptions. Their last one was based on pre-pandemic data but they recently updated it, considering “moderate” and “strong” pandemic impact scenarios.

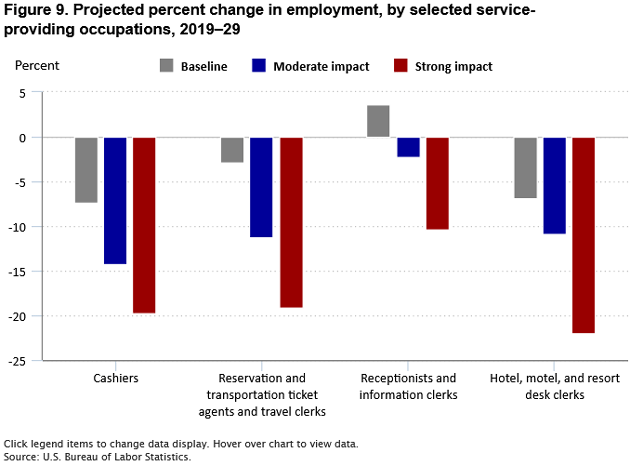

Here’s a chart that cuts to the chase. The gray bars are the percentage employment change BLS expected from 2019–2029 in some selected job categories. The others are a new projection based on moderate pandemic impact (blue) and strong impact (red).

Source: BLS

Note that in these four “service” occupations, BLS already expected either little growth or outright losses even before the pandemic, often due to automation. And in all cases, it thinks the pandemic will make it even worse. Ditto for restaurant and bar jobs.

But BLS foresees the opposite in many technology and healthcare occupations. They think the pandemic will actually create long-term jobs in those categories.

Source: BLS

These kind of tech jobs, already expected to show solid growth, should grow even more in the post-pandemic era, thinks BLS.

Unfortunately, these growing occupations generally require more education than the shrinking ones. And in terms of raw numbers, there just aren’t as many of them. That leaves a big problem: What will happen to workers in these disappearing occupations?

How many of us work at the same kind of jobs we studied for in school? How often have we changed careers? Twisted career paths are nothing new. If the path doesn’t lead where you want, maybe it’s time to blaze a new one. Millions will be doing so in the coming decade.

The Incentives of Unemployment

I served for several years on the board of a public company (Ashford, Inc.) which managed hotel REITs with 125 hotels, including the Ritz-Carlton in the Virgin Islands. Shane and I were married there and my fellow board members gave us a week as a wedding gift. A few years later (after hurricane Maria) I wanted to take Shane back. I learned the hotel was still closed. It having been some time, I asked why. I was told the company was making more on business interruption insurance that it would by actually operating the hotel. Magically, hotels all over the Caribbean generally opened up about the time the insurance ran out.

In December, Congress and President Trump agreed on an $800 billion pandemic relief bill. We are now contemplating another $1.9 trillion in “relief.” Much of that money will be spent after this year and as late as 2029, but a good bit of it will hit in the second quarter. Some of it may actually incentivize unemployment.

As noted above, there are jobs available, but if you can get paid unemployment that is more or less equivalent (plus cash, plus child tax credits, and other benefits) your incentive to seek one of those jobs is lower.

I would not for one second begrudge any jobless person the safety net of unemployment insurance. It is necessary. But it was meant as transition assistance while trying to find a new job, not a substitute.

In summary, the economy is recovering. Government transfer payments boosted personal income 10% in January, with spending up 2.4%. GDP is likely to be very strong for the first two quarters at least. The already-passed and soon-to-be-passed relief spending could be inflationary in a growing economy. (As an aside, surveys show that 37% of the $600 stimulus checks will end up in the stock market.)

Yet, millions of people are unemployed and many of them will have to make career changes. Transitions are never easy or swift. The Federal Reserve is committed to low rates and easy monetary policy at least until 2023, even with a growing economy. The markets want higher rates, but the Fed doesn’t. This is the type of fight where both sides will lose, even if one appears to win. Jerome Powell’s term as chair ends in February 2022. You can expect a more dovish chair (likely Lael Brainard) will replace him.

Unemployment is going to be “stickier” than we would like to see, especially in a recovering economy for the reasons stated above. All of this is going to produce more market volatility.

There are lots of places to employ your investment capital. I am bullish about some and bearish about others. I don’t have to risk my capital in the midst of an economic bar fight. I can choose to go to another, more tranquil establishment.

You need to seek out absolute returns over passive relative returns. Fixed income ETFs and mutual funds offer very low yields and capital loss in times of rising interest rates. When we don’t know what’s going to happen, maybe find an alternative? There are many.

It has been basically muy tranquilo here in Dorado Beach. The “winter” here brings temperatures into the low 70s and sometimes even in the 60s in the evening. The humidity is not that much. That being said, there are lots of friends and opportunities for more friends and local investment.

I find I am doing more and more Zoom calls. It turns out that people really do want to see one another, and a telephone call simply doesn’t scratch that itch. I am enjoying the lifestyle here far more than I thought I would. I couldn’t blow Shane out of here with dynamite.

With that short note I will hit the send button. Be sure you follow me on Twitter. You have a great week.

Your ready to get on a plane analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All