The first quarter saw an accelerated normalization in markets, as equities hit new highs, while Treasury yields rocketed higher. With widespread dissemination of demonstrably efficacious vaccines underway, the market has shifted its focus to continued stimulus and the potential for inflation.

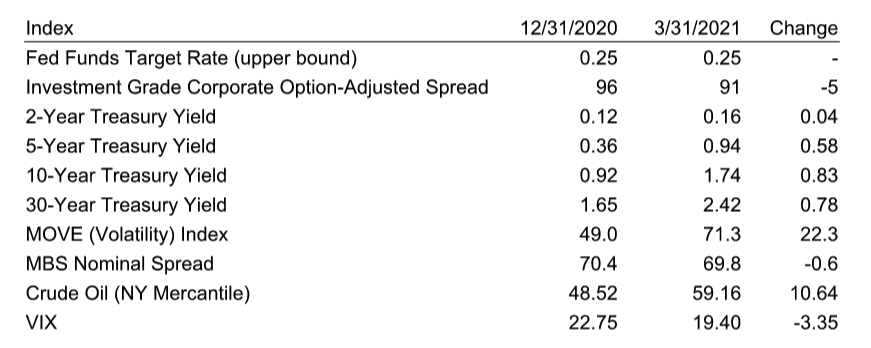

The table below highlights the dramatic recovery across the markets.

Besides the vaccine distribution, the other major event of the first quarter has been the advancement of broader fiscal stimulus measures, courtesy of the Democratic sweep of the Georgia runoff that gave the Democrats a majority in the Senate. This has buoyed risk taking across markets, at the expense of Treasuries. Particularly telling is the fact that the MOVE Index, which measures the volatility of Treasury options, has risen sharply, in the absence of equity volatility (VIX). Economic data across the spectrum have exceeded expectations across most, if not all segments of the economy.

The question is whether this manifests as inflation. We have a potent concoction with the fed funds rate pegged at zero, quantitative easing, and fiscal stimulus as many risk assets are breaching new highs - not to mention creative stores of wealth, including cryptocurrencies and trading cards. The consumer’s balance sheet has largely improved over the past year, save for those whose jobs have been disrupted by pandemic lockdowns. This is in stark contrast to the period that followed the Global Financial Crisis (GFC). In that time, the consumer withstood a double whammy of falling equity prices and falling home prices, with homes representing the largest asset for many. Real estate assets back then were often recklessly levered, courtesy of extremely lax lending standards.

The post-GFC experience has led many to debate traditional monetary theory vs. Modern Monetary Theory. Specifically, one can point to the period of QE1-3 (2009-2014) as a time when extraordinary monetary stimulus failed to stoke inflation. Let’s take a deeper look at this period, compared with today’s experience.

The traditional monetarists abide by the simple relationship:

M x V = P x Q = nominal GDP

where M = Money Supply, V = Velocity of Money, P = Price of Output, and Q = Quantity of Output.

One of the ideas behind quantitative easing was a massive increase in money supply. However, given the plight of most households during the GFC, money created during this wave was largely saved, not spent – as evidenced by the decline in velocity. As M and V offset, there was little change in the price and quantity of output. This is reflected by our slow recovery with low inflation during the period.

Looking at 2021, markets tell a different story. Investors are seeking new avenues for investing cash as traditional risk markets have reached new highs. We’ve seen a massive increase in M2 money supply – and some evidence of rising output and rising prices. Anecdotes of rising producer prices, as well as recovery of pandemic-stricken industries continue to trickle across the newswires. GDP estimates, both in the U.S. and globally, are projected to exceed the prior QE-regime. It stands to reason that even if the velocity of money were to fall slightly, the sheer size of money supply growth will support this economic expansion. It will become increasingly important to track producer price indices and GDP to see just how different the next couple years will be, compared to the prior ten.

Turning our focus to investment grade (IG) sectors, the IG corporate market suffered a total return of -4.65% in the first quarter of 2021, its worst quarter since the depths of the financial crisis in 2008. In contrast to that period, the poor return of the corporate index last quarter was entirely attributed to a selloff in the underlying risk-free Treasury rate. The credit component of the index, measured by the OAS, actually tightened 5 basis points. The spread tightening combined with carry produced an excess return of +95 basis points above Treasuries.

As we expected (see our 2021 annual outlook), performance was driven by the widest trading sub-sectors. In fact, every sub-sector that started the year wide of the index outperformed the broader index. These sub-sectors lagged the most in the recovery of 2020 and largely represent the areas of the economy that will benefit the most from the reopening. This dynamic was also seen by ratings, as BBBs outperformed single As by 91 basis points of excess return. The new issue market saw supply exceed ~$450 billion, which was well ahead of expectations as the full year estimate for supply is $1.25 trillion. While we acknowledge that the first quarter is a seasonally strong new issue period, we continue to believe that supply will end the year meaningfully ahead of Wall Street estimates, though likely lower than 2020’s record issuance. Looking forward, we maintain a small overweight towards investment grade credit. The credit fundamentals should continue to improve as the economy springs back to life and the technical backdrop should be favorable as we expect an abatement to the pace of supply and higher yields will attract buyers. At the risk of repeating ourselves, it will be more important than ever to avoid credits that underperform. We are operating in an environment with little to no margin for error.

In mortgages, the large rise in rates (and rate volatility) triggered a momentary panic reminiscent of the taper tantrum in 2013, with current coupon mortgage spreads rising nearly 24 basis points over a two week period in February, punctuated by a very weak 7-year Treasury auction that sent Treasury yields to local highs. However, higher rates also signify diminished supply, as there is less incentive for borrowers to refinance at newly higher rates. Coupled with constant demand in the form of Fed MBS purchases, mortgage spreads finished the first quarter largely unchanged.

This inflation narrative prioritizes our focus on interest rate exposure across the portfolio. In the near-to-medium term, the fixed income market will be driven primarily by rising inflation expectations and concerns about higher rates. We feel these concerns are warranted, as we believe this bout of monetary and fiscal stimulus could have a very different impact on the economy than was previously witnessed. In our view, the risk of higher rates mandates a shorter duration profile across all asset classes, which we currently maintain.

We thank you for your confidence in us and welcome any questions or comments you may have.

Best regards,

Eddy Vataru

John Sheehan

Daniel Oh

Past performance is no guarantee of future results. This commentary contains the current opinions of the authors as of the date above which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed. It is not possible to invest in an index.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

A mortgage-backed security (MBS) is a type of asset-backed security that is secured by a mortgage or collection of mortgages.

The Chicago Board Options Exchange (CBOE) Volatility Index, or VIX, is a real-time market index that represents the market's expectation of 30-day forward-looking volatility

Duration measures the sensitivity of a fixed income security's price (or the aggregate market value of a portfolio of fixed income securities) to changes in interest rates. Fixed income securities with longer durations generally have more volatile prices than those of comparable quality with shorter durations.

Merrill Lynch Option Volatility Estimate (MOVE) Index – USD – is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options.

A yield curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates.

Spread is the difference in yield between a risk-free asset such as a U.S. Treasury bond and another security with the same maturity but of lesser quality. Option-Adjusted Spread is a spread calculation for securities with embedded options and takes into account that expected cash flows will fluctuate as interest rates change.

Holdings and sector allocations may change at any time due to ongoing portfolio management. References to specific investments should not be construed as a recommendation to buy or sell the securities by the Osterweis Total Return Fund or Osterweis Capital Management.

Coupon is the interest rate stated on a bond when it's issued. The coupon is typically paid semiannually.

A basis point is a unit that is equal to 1/100th of 1%.

Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care.

The Osterweis Funds are available by prospectus only. The Funds' investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible.

The Osterweis Total Return Fund may invest in fixed income securities which are subject to credit, default, extension, interest rate and prepayment risks. It may also make investments in derivatives that may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. The Fund may invest in in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility or illiquidity compared to higher-rated securities. Investments in foreign and emerging market securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks may increase for emerging markets. Leverage may cause the effect of an increase or decrease in the value of the portfolio securities to be magnified and the fund to be more volatile than if leverage was not used. Investments in preferred securities have an inverse relationship with changes in the prevailing interest rate. Investments in Asset Backed and Mortgage Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. It may also make investments in derivatives that may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. The Fund may invest in municipal securities which are subject to the risk of default.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OSTE-20210409-0185]

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management