Fed's Patience Tested, Slow Labor Markets, India's COVID Crisis

IN THIS ISSUE:

- Can The Fed Stay Patient?

- Labor Markets: Rapid Contraction, Gradual Recovery

- Global Consequences of India’s National Trauma

I watched the film “Apollo 13” again recently. For those too young to remember, a mission to the moon that launched 50 years ago almost ended in disaster; working feverishly, ground control was able to bring the astronauts back safely. The tale of science and perseverance triumphing over adversity resonates during these pandemic times.

Among my favorite scenes is one where the crew has to initiate a short engine burst to place themselves on course for a successful landing. The engineers in Houston labor over their slide rules to calculate trajectories and determine precisely how long the maneuver should be. The fatigued pilots must execute the procedure flawlessly. There is a lot of suspense involved: even though the earth is still tens of thousands of miles away, even a slight error in setting direction could lead the capsule to overheat upon re-entry.

I was thinking of that scene last week as U.S. Federal Reserve Chairman Jerome Powell addressed reporters. After two days of meetings, the Fed reached the same conclusion it had in March: because the U.S. economy is a long way from achieving its objectives, no change of course is necessary. But because monetary policy works with long lags, failing to alter direction now could bring the possibility of economic overheating onto the horizon.

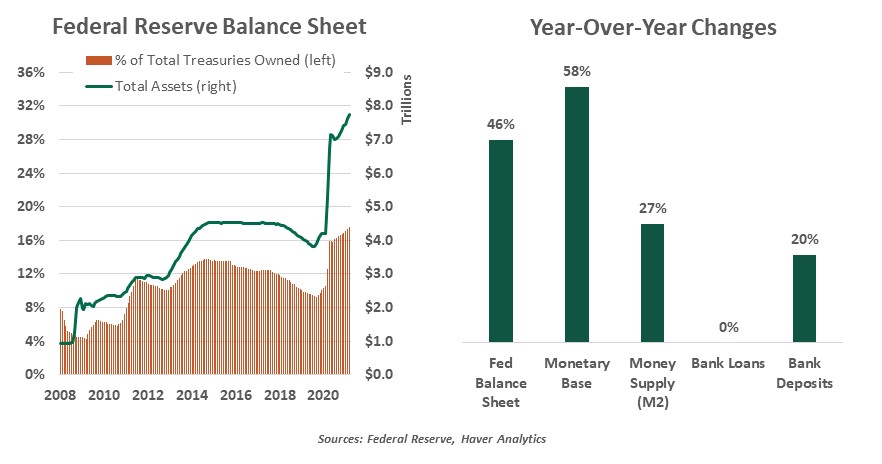

Like other major central banks around the world, the Fed has loosed an immense amount of liquidity on the U.S. economy since the pandemic started. With interest rates at zero, quantitative easing has taken center stage as the main avenue of stimulus. Since April of 2020, the Fed has increased its securities portfolio by almost $3 trillion; it now owns 17% of outstanding U.S. Treasury debt.

The Fed continues to purchase $120 billion of new bonds every month, and shows little inclination to taper this amount. Paying for the new securities has resulted in outsized increases in the money supply, cascading across the financial system. Some has been spent and some has been invested, putting upward pressure on the prices of goods and assets.

More inflation in the prices of goods and services is not altogether unwelcome. Despite a strong pre-pandemic economy, increases in the price level were falling well short of target, leading inflation expectations lower. In response, the Fed announced a new objective: averaging 2% inflation over the medium term. Readings above 2%, at least for some period of time, are now seen as desirable; in theory, this will lead inflation expectations higher, but not too high.

|

Will transitory inflation become permanent? |

The Fed has also indicated that it will de-emphasize the use of forecasts for setting policy. Unless actual readings on inflation have met their standards, it will stay the course. To a degree, this is understandable; forecasts of inflation over the past decade have routinely over-estimated. In retrospect, the modest interest rate increases implemented between 2015 and 2019 were unnecessary, and they may have hindered the achievement of broader economic gains.

The difficulty with waiting for realized inflation is that monetary policy takes a long time to have an impact. It could take several quarters for reduced accommodation to curb the economy, by which time prices may be rising much more rapidly than desired.

On that front, recent news has not been reassuring. Inflation readings have been pushed higher by base effects and bottlenecks created by the pandemic. In developed markets, demand is resurgent as economies reopen and pent-up demand combines with pent-up saving. In some cases, supply is struggling to respond, leading to pressure on costs; in spots, producers are able to pass those costs along to consumers.

The Fed is viewing these stresses as temporary. Eventually, it reasons, kinks in supply chains will straighten. For services, labor supply should recover over the coming months as the impacts of COVID-19 wane, schools reopen and unemployment benefits sunset. We generally agree, though there will be some fits and starts along the way. And, as we’ve discussed, secular governors like technology and e-commerce should continue to contain inflation over the longer term.

But what if we, and the Fed, are wrong? In that case, monetary policy will have to be tightened sooner and more aggressively than currently planned. Unless the transition is carefully communicated and executed, markets could become unsettled. As noted earlier, the Fed’s provision of liquidity has inflated that value of some assets; deflation in this arena could risk financial instability.

|

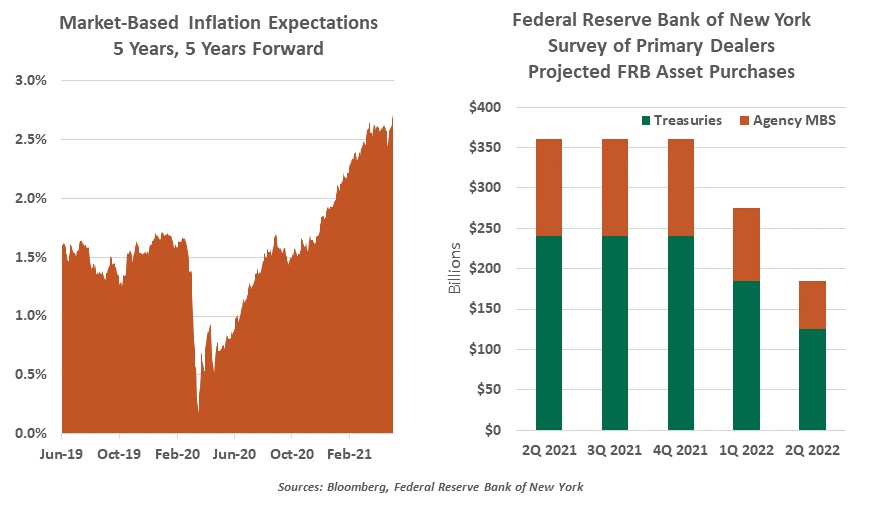

An abrupt change of Fed policy could be unsettling to markets. |

Market indications are always to be taken with a grain of salt, as they change frequently and are affected by technical factors that can wax and wane. But investor expectations for inflation recently touched a 15-year high. And surveys foresee the Fed tapering its asset purchases and raising interest rates much sooner than intended. Janet Yellen, the current Secretary of the Treasury and former Fed chairman, suggested this week that higher rates might soon be necessary to contain inflation.

An early change of course will present political challenges. Since the pandemic began, the Fed has helped to finance the relief programs passed by the U.S. Congress. Bond purchases by the central bank have helped keep government borrowing costs modest, a condition that makes it possible to contemplate the long-term fiscal ambitions put forth by the Biden administration. But while partnership between central banks and governments has been essential during the pandemic, separation between the two is essential in the long run. If the Fed fails to reinforce its independence when the time comes, market performance may be affected.

To be clear, we expect inflation to settle after the summer, and believe the Fed can remove accommodation at a leisurely pace. But absent a viral resurgence, the upside risks to prices seem more pressing.

When the Apollo 13 capsule re-entered the earth’s atmosphere, its radios went silent. The communications gap lasted four anxious minutes before the astronauts splashed down successfully. The Fed is in for some anxious moments over the next few months; hopefully, it will communicate clearly and steer inflation to a soft landing.

Getting Back to Work

Anecdotes are building in the press of business owners struggling to hire and even temporarily closing for lack of staff. As we have previously discussed, the steep drop in employment caused by the pandemic will take a long time to reverse.

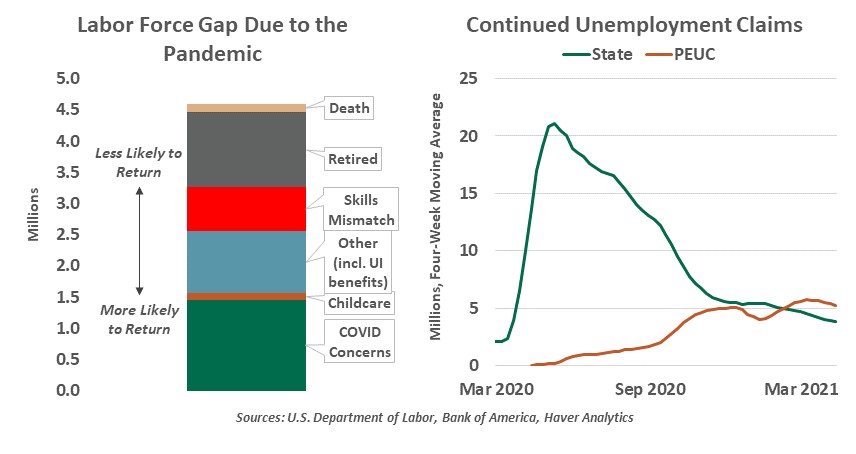

We are moving in the right direction. Payrolls rose by 266,000 in April, led by gains in the leisure and hospitality sectors. But opportunities are recovering slowly, leaving over eight million Americans not participating in the labor force. As a result, jobs on the bottom end of the wage spectrum are becoming hard to fill: hotels and restaurants are especially struggling to recruit. The lowest-paid workers were the subset that experienced the greatest displacement last year, so the solution seems clear: Call those workers back! But many frictions are slowing the process.

Labor force shifts in the pandemic are preventing some hiring. Sectors like restaurants and tourist attractions had the most severe layoffs last year and looked likely to face a long impairment. Their employees viewed the pandemic as a chance to move into jobs that were in greater demand, where they will remain. Meanwhile, the nature of many jobs has changed. Employers increased investments in automation, and once a job is automated, it rarely comes back.

The pandemic slowed immigration, which continues to weigh on recruitment, especially for seasonal and temporary work. Shutdowns also prompted many people to retire. The virus put older workers at greater risk, and now that an end is in sight, some feel life is too short to go back to work. And though it is grim, we cannot ignore that at least 110,000 U.S. COVID-19 mortalities were people of working age.

Other workers remain sidelined for personal reasons. Child care is a barrier to work outside the home—and sometimes to productively working from home. Many day care providers closed while schools opened inconsistently, often with shorter hours and unpredictable quarantines. Extended day and extracurricular activities were often unavailable, giving parents even less flexibility, while distancing guidelines reduced fellow parents’ willingness to help with children outside their own family. As schools reopen in the fall, parents will gain more capacity to work.

|

A series of factors are delaying re-entry to the U.S. labor force. |

And regardless of children, many workers remain hesitant to expose themselves to COVID-19 by interacting with the public. The good news around vaccinations takes focus away from the ongoing pandemic. Though we have improved our practices for managing the virus, we haven’t beaten it. Workers with comorbidities or medically fragile family members will be the last to return.

Of course, a safety net simplifies the decision not to return to work. Most states offer 26 weeks of unemployment insurance, with 14 states offering up to an additional 20 weeks of extended benefits. The federal government is providing an emergency supplement of $300 weekly to workers who had exhausted their state benefits. Higher wages are certainly available from many employers, but this supplement could be enough to keep some workers home voluntarily.

Many of these factors will be temporary. As progress against COVID-19 continues, fewer workers will stay away out of fear of infection. Hopefully, school closures should be a rarity when the next school year starts, which coincides with the expiration of supplemental jobless benefits in early September. However, there is no policy solution for workers who have retrained, retired or passed away, leaving jobs unfilled. Employers are putting more effort into recruitment, and it appears offering higher wages does compel more applicants to come forward.

“Help wanted” signs may be a fixture of our lives for some months to come—but eventually, workers will arrive to take them down.

Epicenter

India, the world’s fifth-largest economy with a population of over 1.3 billion, is going through a crisis of unprecedented proportions as daily virus infections and deaths explode. And when a country of its size goes through a crisis of this magnitude, it raises alarm bells for others.

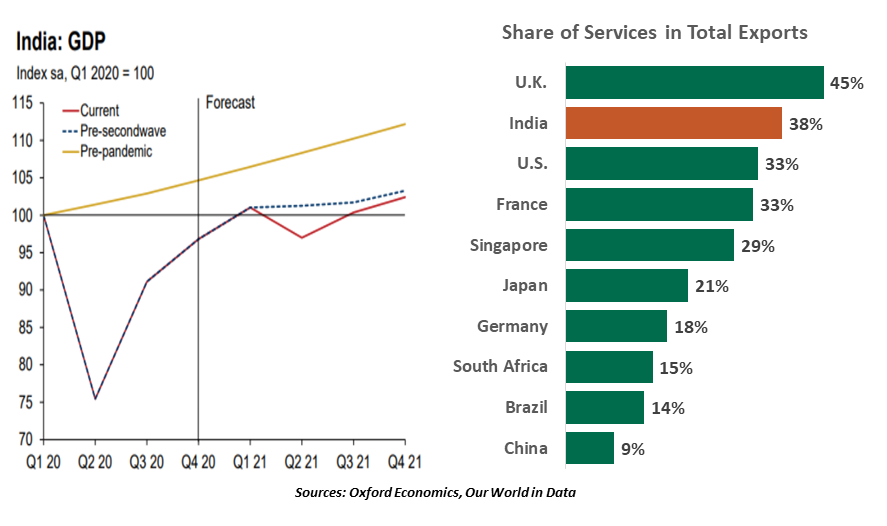

Major advanced economies may have managed to bring the virus under control. But India’s crisis will not likely be contained within its own borders, presenting risks to global and economic health. Supply chains are coming under further strain: India is well integrated in global value chains with 16% foreign value-added content in its exports. India is also one of the largest sources of sea crew; with more crew members contracting the disease, ports have started denying entry to vessels.

India is a major importer of goods and is among the top trading partners of the world’s biggest economies like the U.S. and China. It is also the world’s third-largest oil importer. A meaningful slowdown in demand will likely weigh on oil prices and producers. Exports of services are another important part of the Indian economy; India has emerged as the preferred destination for outsourcing and key back-office functions in the health, financial and technology sectors. Illnesses among India’s professionals have potential implications for global businesses.

|

The impact of India’s disruption will be felt everywhere. |

Lasting or frequent disruptions in India will not just hurt global trade, supply chains and investment, but will also affect global healthcare. India’s pharmaceutical industry is the world’s third-largest, accounting for one-fifth of the global exports of generic drugs and over two-thirds of vaccines. Failure to provide vaccine supplies to the rest of the world, particularly to lower-income economies, will keep those parts of the world vulnerable to future waves and recurrent lockdowns.

India isn’t the only emerging market (EM) struggling, with case counts also rising in countries like Brazil and Turkey. EMs, which account for more than half of the world’s economy, are at risk of falling far behind their advanced counterparts, putting them on the downward leg of the K-shaped recovery. While these places may seem far away, the medical and economic consequences of their current struggles could hit very close to home—wherever home is.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.