The smallest companies in the market may be overlooked by many investors, but can offer big potential. Here, we posed some questions about micro-capitalization (microcap) stocks to Franklin Mutual Series Portfolio Manager Oliver Wong, who explains how they have fared recently and where he’s finding opportunities.

Microcap companies have had a significant run recently, why do you believe this segment is still attractive?

Microcap stocks tend to perform well in an expansionary environment due to their high sensitivity to the domestic economy. Comments from both the US Federal Reserve and Treasury clearly indicate that interest rates will remain low for the foreseeable future, which should further fuel the economic recovery from COVID-19.

However, valuations can appear optically high for some microcap stocks as investors anticipate a degree of fundamental recovery for these stocks. Therefore, we believe active management is the best way to participate in microcap stocks in today’s environment via exposure to those select names that appear best positioned to benefit from a continued rebound in the economy.

What’s so interesting about microcap stocks in your view—and how do you define them?

As of their latest reconstitution in May 2020, all securities within the Russell MicroCap Index* were below $1 billion in market capitalization.1 We believe this niche asset class deserves a role in many equity investors’ portfolios for two main reasons.

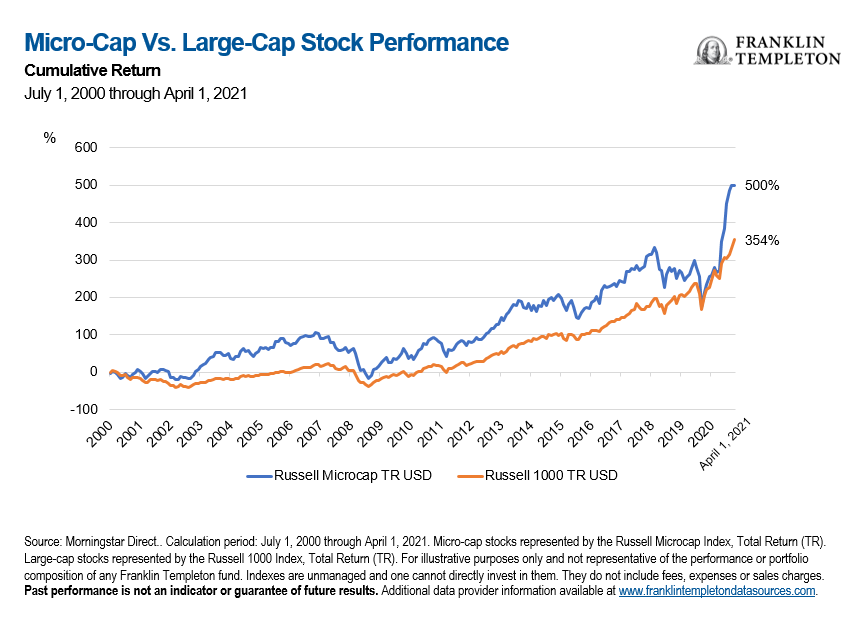

First, US microcap stocks, as measured by the Russell Microcap Index, have provided strong absolute returns since 2000, outperforming their large-cap peers in the Russell 1000 Index.2

Second, microcap stocks tend to be an under-researched area, which increases the odds of discovering attractive investment opportunities. This is because larger-cap stocks dominate the overwhelming majority of US equity trading. As a result, the brokerage firms orient their research capabilities in that direction, leaving the microcap space largely unattended.

As active microcap managers, we scour this vast investment universe of under-researched stocks looking for good companies that have been ignored, overlooked or temporarily beaten up. We believe the fact that most institutional money managers aren’t even looking in the microcap space allows us to find stocks that offer superior performance potential over the long term.

Microcaps seem to be a very niche part of the stock market, as you stated. How did you get involved with microcaps?

I joined Franklin Templeton in 2012 as a research analyst covering small and microcap stocks globally. Personally, I find these small, oftentimes neglected public companies fascinating because the outcomes are so varied. One microcap stock could be a super high-growth company that’s blazing new trails in its industry. Another could be a former large-cap stock headed toward extinction.

Given this wide divergence of fortunes, I believe that successful long-term investing in this space requires a focus on higher-quality companies and an adherence to value principles. This is the investment framework that I’ve always used and continue to apply today as a portfolio manager.

What are some of the main characteristics you look for in these companies?

We assess value through multiple lenses, including sustainable earnings power, cash flow generation, balance sheet strength, and quality of management.

Sometimes stocks look cheap by typical valuation measures because they operate in an industry that is currently out of favor, or they may be facing company-specific problems. Regardless of the situation, a large part of our job is to determine whether these issues are temporary and will eventually pass, or whether they will persist long term.

We typically avoid the latter. But if we think the problems are temporary or fixable, then we like to see a healthy balance sheet with little or no net debt, and positive cash flow generation. We generally assume that it will take time (in some cases years) for things to get better. We want to see the company in good financial shape to weather the inevitable near-term challenges.

What advice would you give investors looking to invest in microcap value stocks now?

According to Bloomberg, there are nearly 15,000 common stocks traded in the United States, of which almost 9,000 have a market cap of $1 billion or less.3

Given the sheer breadth of the microcap universe, my advice would be to carefully consider active management for microcap investing. Yes, there are passive investment options, but they invest in many stocks that reported zero or negative cash flow from operations in their last fiscal year, or had net debt that exceeded their earnings before interest, tax, depreciation and amortization (EBITDA).4

Remember that companies on their way to bankruptcy are also part of the microcap universe!

We think microcap investors are better served focusing on the higher-quality end of the spectrum, and that can only be adequately achieved through active management. In addition, active management can potentially lower volatility of returns, compared to a microcap index or exchange-traded fund.

Important Legal Information

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any industry, security or investment.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investing in smaller-company securities that may have limited liquidity involves additional risks, such as relatively small revenues, limited product lines and small market share. Historically, these stocks have exhibited greater price volatility than larger-company stocks, especially over the short term. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Value securities may not increase in price as anticipated or may decline further in value. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

1. Russell defines microcap stocks as the smallest 1,000 securities in the small-cap Russell 2000® Index, plus the next 1,000 smallest eligible securities by market cap.

2. Source: Russell Indices. The Russell 1000 Index is an index of approximately 1,000 of the largest companies in the US equity market by market capitalization. The Russell Microcap Index is a capitalization-weighted index that captures the smallest 1,000 companies in the Russell 2000, plus 1,000 smaller U.S.-based listed stocks. Indexes are unmanaged and one cannot directly invest in an index. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future performance. See www.frankintempletondatasources.com for additional data provider information.

3. Bloomberg, as of April 30, 2021.

4. EBITDA is a measure of a company‘s overall financial performance and is used as an alternative to simple earnings or net income in some circumstances.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments