Transitory Inflation? Not so Quick

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Coming Arc of Transitory Inflation

Transitory is defined as being of brief duration, tending to pass away and not persistent. The problem facing the FOMC is that the four factors driving the current wave of inflation will each have a different and longer shelf life. Base Effects are contributing to the near term surge in headline inflation and will prove transitory. Supply chain disruptions will also be transitory but will last longer than Base Effects, so they will offset some of the initial unwinding in Base Effects. Core inflation is likely to continue to increase as service and shelter inflation trend higher. Finally, a number of factors are coming together to lift wage inflation in coming quarters as the reopening of the economy progresses and companies pay more to attract workers. As these four factors unfold headline inflation is unlikely to recede as much as expected and core inflation will hold significantly above the Fed’s 2.0% Core PCE target for the balance of 2021.

Base effect inflation – Temporary and Resistant

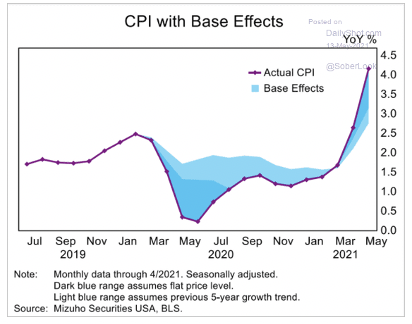

In the April and May issues of Macro Tides I discussed all the reasons why headline CPI inflation was poised to jump. “The increase in headline CPI inflation will exceed 3.0% and could approach 3.5% in the next few months and generate attention grabbing headlines.” On Wednesday May 12 the Bureau of Labor Statistics reported that the headline Consumer Price Index (CPI) for April soared 4.2% from a year ago. Base Effects played a big role but some of the comparisons were historic. The surge in the headline CPI was led by Energy prices which jumped 25% from a year earlier, including a 49.6% increase for gasoline, and 37.3% for fuel oil.

The plunge in the CPI in March and April in 2020 was due to falling prices for energy, airfares, hotels and motels, car rentals, events that attract large crowds i.e. sports and entertainment shows, and food prices in restaurants. The chart above illustrates the contribution to the decline in the headline CPI last year by showing the previous 5-year average growth in light blue. Last year these factors subtracted more than -1.5% from the CPI in April and May. The CPI uses a 12 month year over year calculation so the -1.5% reduction last year is adding +1.5% now. As the calendar moves beyond May the sling shot affect from Base Effects will subside.

One way to remove the volatility of Base Effects is to compare prices now to prices in January 2020 before the Pandemic shut down the economy. Most of the items that are much higher than they were in January 2020 are not likely to decline much in coming months with the exception of propane. Restaurants scrambled to buy outdoor heaters so they could serve diners outside their restaurants and needed propane to keep customers warm. They won’t need them once they can serve everyone indoors especially during the summer months. Most of the items that were hit the hardest and are still well below their January 2020 price level are going to recover, although it will take time for public transportation. As workers return to the office, they will be shopping to update their wardrobes, and just about everyone will be jumping on an airplane to go anywhere.

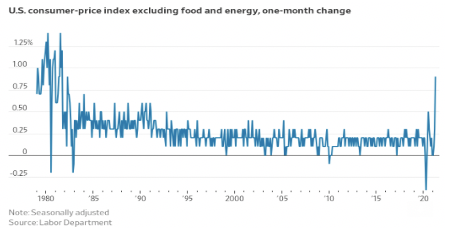

While the increase in the headline CPI was eye opening, the increase in the Core CPI was stunning. The 1 month increase in the Core CPI was 0.9% and the largest single month rise since 1981. Airfares jumped 10% in April from March, but since February 2020 are still down 15% at an annualized rate. As demand for travel soars in coming months the airlines are going to raise fares. For many years the majority of consumers were very cost conscious and religiously compared prices whenever they were about to make a major purchase. This was one of the factors that forced companies to hold the line on price increases in the wake of the financial crisis. Coming out of the Pandemic lockdown consumers have more money in their pockets and they just want to have fun and if it costs a few bucks more, so what!

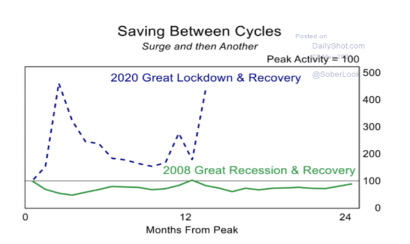

Personal income fell after the Financial Crisis and didn’t reclaim the prior peak for two years. Personal Income soared in April 2020 and again in 2021 after Congress passed two more stimulus plans that gave working and unemployed workers hundreds of billions of dollars. Personal income jumped above its long term uptrend by more than $450 billion in Q1. With much of the economy shut down consumers saved since they couldn’t spend their windfall going out to dinner, catching a movie, attending sporting and entertainment events, or travel.

More income and less spending is why the savings rate climbed to 27.6% in March up from 7.9% before the Pandemic. It dropped to 14.9% in April, still almost double the pre Pandemic level. As consumers were bottled up and unable to go out and spend, they chose to save and also pay down their credit card debt. According to the Federal Reserve Revolving Credit Card debt dropped from $1.022 trillion at the end of the first quarter of 2020 to $925.2 billion as of March 31, 2021, a decline of -9.5% in 12 months. Revolving Credit Card debt fell from a peak of $1.004 trillion in December 2008 to $789.7 billion in April 2011, after falling -21.1% over 28 months. The extended nature of the post Financial Crisis decline in Revolving Credit Card debt is understandable since personal income was weak for two years. These are the only annual declines in Revolving Credit Card debt since January 1968.

With historically high savings and much lower credit card debt, the U.S. consumer has more spending power than in any time in history, and after a year of involuntary restraint, consumers are ready to let it rip.

Food away from home accounts for 6.3% of the Consumer Price Index, compared with 2.8% for used vehicles and 0.6% for airfares. Food prices climbed 2.4% from the same month a year ago, including a 3.8% rise in the cost for restaurant meals. Since February 2020 food away from home has risen at a 3.6% annualized rate, much faster than the 2.7% average over the prior five years. In the past year restaurants have had to absorb two gut punches, as the cost of meat, chicken, and other staples have gone up a lot, even as revenue disappeared as they were forced to close and then open on a partial basis in the majority of states. The stampede of happy customers at their door will provide most restaurants the opportunity to increases prices and they will. The National Owners Association, a group representing U.S. franchisees, said in an email to its members on Sunday May 16 that strong sales should allow operators the choice to raise menu prices to offset higher spending on pay and benefits.“We need to do whatever it takes to staff our restaurants and then charge for it,” the association said.

In many sectors of the U.S. economy there is a mismatch between a big increase in demand and supply constraints, which is why prices for the majority of commodities is rising. Historically, producers will choose to increase capacity to satisfy higher demand. As capacity expands and supply increases prices come down. Economists refer to this process as the self correcting mechanism of a free market. High prices are the best antidote for a shortage just as low prices cause production to fall, so equilibrium between supply and demand is reestablished. The unique aspects of the Pandemic and fiscal spending response by the Federal government is leading some firms to forestall adding any new capacity, and keep prices higher for longer.

According to market-research firm Urner Barry, boneless, skinless chicken breast, the poultry industry’s flagship product, last year averaged around $1.00 a pound, but now costs $2.04 a pound. Over the past decade, the price averaged about $1.32 a pound, which means the current price is 55% above its long term average driven by a surge in demand. Fast-food restaurants’ servings of chicken wings were up 33% in March from a year ago, according to market-research firm NPD Group Inc. According to Department of Agriculture data, total chicks hatched over the first three months of 2021 trailed 2020’s first-quarter total slightly. High demand, prices, and flat supply is the perfect prescription for a chicken producer to expand capacity, but one of the largest poultry producers has decided not to expand. Sanderson Farms, the third-largest poultry producer in the U.S. has decided that it will not expand its operations, despite surging demand that has put it on the cusp of running out of chicken wings. Sanderson Farms decided that the cost of adding capacity was simply too high based on the price of steel, concrete, plastic, copper, and lumber. This means the imbalance between the demand and supply for chicken will keep chicken prices elevated for longer.

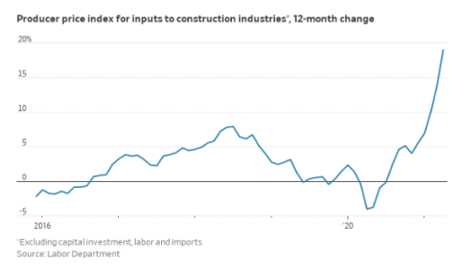

Lumber has almost become the poster child of soaring commodity prices and for good reason. In early 2020 lumber was trading near $400 and has since more than quadrupled. After reaching $1733 on May 10, lumber fell to $1327 on May 17 down -23.0% in a week. Even if lumber falls to $850 it will still be up 100% from where it was trading in early 2020. The big increase in lumber prices has added $36,000 to the cost of the average new home. The demand for new homes is projected to remain strong as Millennials buy their first home or use the appreciation of an existing home to trade up to a larger home. The supply of existing homes for sale was 1.16 million in April, just above the record low in March and representing only a 2.4 month supply at the current selling rate. The average home spent 17 days on the market in April, the shortest time ever and a reflection of the imbalance between demand and supply. Until the supply of existing homes for sale increases significantly, the competition with new home sales will remain low. High demand for lumber to build new homes, record high lumber prices, and the low supply of new homes on the market is the perfect prescription for a saw mill to expand capacity.

A new saw mill normally takes up to two years to build and costs hundreds of millions of dollars to build. Broken supply chains, shortages of microprocessors that help run a modern day mill, and the high cost of steel and construction products would extend the time to build a new mill and increase the cost. Korn Ferry advises forest-product executives and has told clients asking about building a new mill that now is not the time. In addition to the extended lead time and higher costs, finding workers where timber is abundant who can operate a computerized mill in a rural area is a big challenge. As Chad Hesters from Korn Ferry succinctly explained, “Trying to build capacity and make investments that have a lot of lead time at the top of a cycle is historically a good way to lose money.” With little new capacity to increase supply in the next two years, lumber prices may not fall as much as expected.

Headline inflation will likely reach a peak within the next 3 months as Base Effects top and begin to recede. However, many input prices aren’t likely to drop back to where they were in January 2020, so headline inflation isn’t like to drop as much or as fast as expected. Base Effects are not the only reason for the current surge in headline inflation.

Supply Chain Shocks

U.S. companies fined tuned the concept of just-in-time manufacturing over a period of decades. This process lowered costs from financing inventories, labor down time, plant size, and increased production, all of which boosted productivity. As more production of sub-components was shifted overseas, the ‘assembly line’ was extended to thousands of miles. This required more fine tuning with overseas plants, shippers, docks in the U.S., trucking firms to deliver the goods to the plants, and the coordination of labor and machines in U.S. facilities. As the number of links in the supply chain grew, the risk of a break anywhere along the global assembly line threatened to slow the production line. Prior to the Pandemic breaks in the global supply chain were few and they didn’t last long as the creed ‘time is money’ kept the pressure on every link in the chain. The Pandemic has disrupted the supply chains of many industries simultaneously, which is one reason why it will take longer to repair. In some industries the supply chain breakdown could take another six months, which will hurt supply and keep prices elevated for longer.

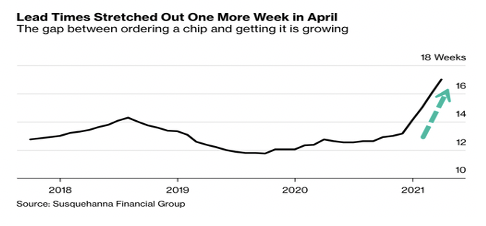

According to Goldman Sachs, 169 U.S. industries embed semiconductors in their products. The bank is forecasting a 20% average shortfall of computer chips among affected industries, with some of the components used to make chips in short supply until at least this fall and possibly into 2022. Chip giant Taiwan Semiconductor Manufacturing Co. is also warning that the shortage will continue throughout this year and maybe extend into 2022. In 1995 the U.S. was home to 37% of the world’s semiconductor manufacturing, but now is down to just 12%. This means the U.S. is more dependent than ever on overseas production and has less control over addressing the supply shortage. In April the time it takes for a company to order a chip and take delivery increased to 18 weeks an all time high. The increase in the Lead Time suggests the current computer chip shortage should last for at least another 4 months. The steep trajectory of the Lead Time suggests that demand is accelerating and that some companies are ordering more than they need in hopes of getting a larger allotment and boost their inventory. Over ordering is a classic sign of an imbalance between supply and demand. Once supply catches up to demand, and companies are confident about future supply, a sharp price decline is likely, since they will have a larger than needed inventory supply. If Goldman Sachs and Taiwan Semiconductor are correct in their assessments, the coming downward price adjustment may wait until late this year or in the first quarter of 2022.

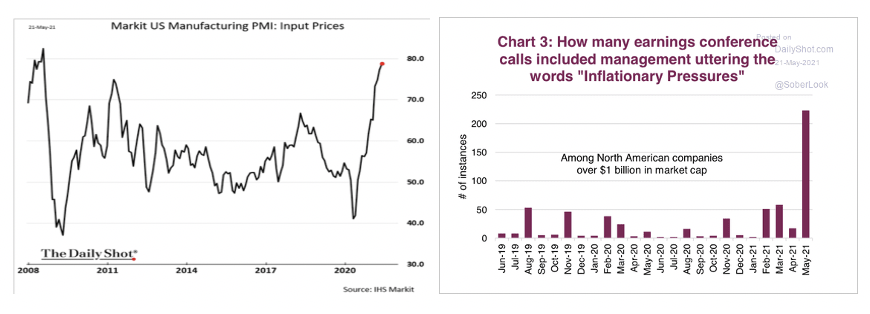

The minutes from the April 28 FOMC meeting were released on May 19 and included comments suggesting a number of FOMC members are concerned that supply chain problems might last longer than expected. “A number of participants remarked that supply chain bottlenecks and input shortages may not be resolved quickly and, if so, these factors could put upward pressure on prices beyond this year. They noted that in some industries, supply chain disruptions appeared to be more persistent than originally anticipated and reportedly had led to higher input costs.” The concern regarding input costs are justified as manufacturing Input Prices in May rose at the fastest rate since July 2008, according to Markit’s U.S. manufacturing PMI. In 2008 the surge in input costs was largely driven by oil, which reached $147 a barrel in July 2008, compared to $68 a barrel now. The current surge is broad based covering many commodity prices, which is why so many large companies are talking about ‘inflationary pressures’ on their earnings conference calls. This graphic was published on May 20 with another 11 days left in May, and the number of mentions was 20 times higher than in 2019.

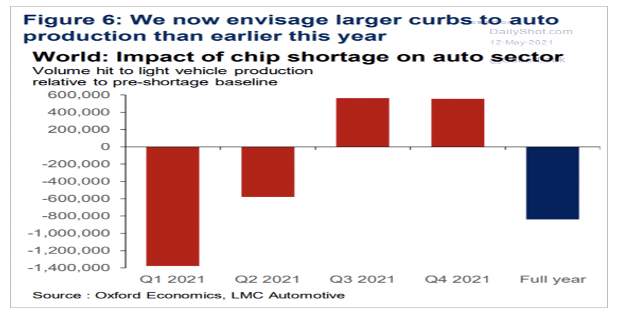

The auto industry is the sector that has been most visibly impacted by the computer chip shortage. Vehicle production will be lowered by 1.2 million units as the automakers can’t get enough chips for safety systems, brakes and engines, according to Auto Forecast Solutions. Despite lower production due to the chip shortage, vehicle sales were near the best levels ever in March and April, as consumers flush with government stimulus money bought whatever vehicle they could find. The average price for a new vehicle was $37,572 in April up 7% from a year ago, according to J.D. Power. When potential car buyers aren’t able to find a new car they have bought a used vehicle. U.S. sales of used-vehicles hit 3.4 million in April, up 58% from a year earlier, according to car-shopping website True Car. The average price for a pre-owned vehicle hit a record of $25,463 in April up 12.3% from a year ago.

The semiconductor shortage has slashed vehicle production so much that rental-car companies can’t get the new cars they need, so they have resorted to buying used vehicles at auction. Last year Hertz was force to sell 200,000 of its cars as part of its bankruptcy deal and is rebuilding its fleet by buying used cars at auctions. The Manheim Index measures prices at wholesale auctions and is up 48% as of mid May. Retail used car prices follow the wholesale price index with about a 6 week lag, so used car prices may not peak until July. New car production will increase in the second half of the year as the chip shortage eases, but not enough to fully reverse the huge increase in used vehicle prices. This means the contribution to inflation from the shortage of computer chips will come down slowly in the second half of this year. Car rental companies are taking advantage of the surge in travel and shortage of cars to rent. The cost to rent a car is up 80% from a year ago, if you’re lucky to get one. Rental car prices may be the ultimate example of Base Effect inflation with a twist of supply constraint thrown in. Car rental prices will surely come down in the fall as the rental car companies replenish their fleets.

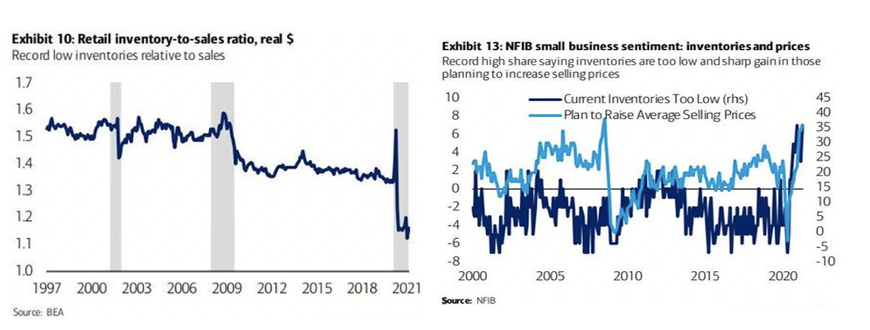

Retail sales have exceeded retail inventories for the first time in decades. Demand soared in March after consumers spent a portion of their stimulus checks, whether they were working or not. From 2012 through 2019 the increase in retail sales followed a trajectory that allowed a straight trend line to track the growth path. The stimulus checks in March 2020 reversed the sharp plunge in retail sales after the economy was locked down to contain the Pandemic. The additional funds received in December 2020 and March 2021 funded a historic spending spree that lifted Retail Sales almost 20% above the eight year trend line. As products flew off the shelves, inventory levels plunged so that the inventory-to-sales ratio fell to the lowest level in at least 25 years. GDP will get a lift as inventories are replenished. Prices will rise as consumers are willing to buy without the incentive of a discount. In the April survey of small business owners by the National Federation of Independent Businesses (NFIB) the highest percent of businesses since 2000 said their inventories were too low and 36% said they were raising prices the highest rate since July 2008.

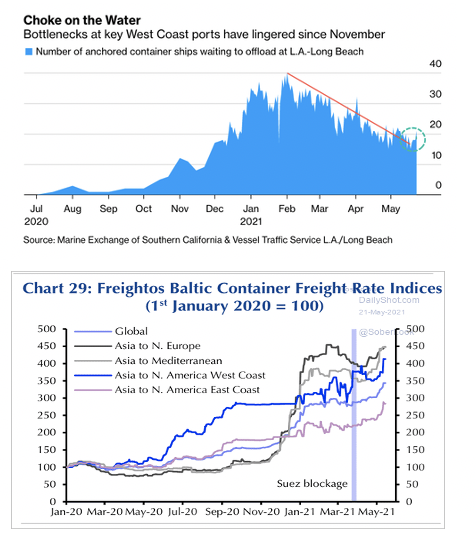

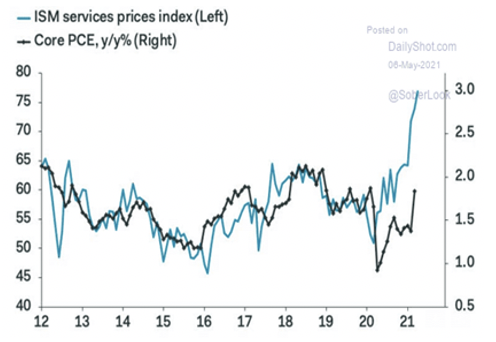

Rebuilding inventories has been a challenge in recent months as the time for goods to be shipped from Asia and unloaded at U.S. ports has increased. It normally takes 14 days to sail from Shanghai to Los Angeles but now takes 33 days. The time sailing hasn’t changed but ships are spending twice the time to unload their cargo at San Pedro and the Port of Los Angeles, according to Moller Maersk the world’s biggest container operator in terms of capacity. The cost of moving a 40-foot sea container from China to U.S. West Coast ports in mid May was $5,650, up 34.5% since the start of 2021, 228% higher than the same period last year, and more than 400% from January 2020, based on the Freightos Baltic Index. In January 2020 the on time rate was 65% but was 40% in May 2021. Since peaking in early February the number of ships waiting to be offloaded has dropped from 40 to 20 as of May 21, so the bottleneck has eased and will continue to do so. The cost of shipping will come down as the volume of containers coming from Asia falls and U.S. ports catch up. But will prices fall as much as they’ve gone up? Nope.

Service Inflation

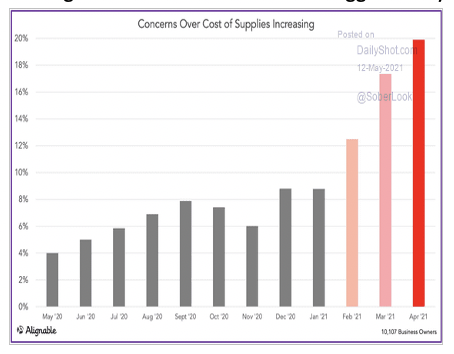

As noted in the May Macro Tides, “A bigger threat to the FOMC’s mantra that the pick-up in inflation will be transitory may come from a steady but persistent increase in core inflation. For the first time since the Pandemic began Service inflation rose in March and will continue to rise in coming months.” In the April ISM Services survey 76.8% of respondents reported that their prices were rising and were up at an annual rate of 3.0%. According to the ISM Services summary, “Input costs faced by service sector firms increased at an unprecedented rate in April. The substantial rise in cost burdens was often linked to hikes in supplier prices and greater transportation fees. Companies particularly noted higher costs of plastic, packaging, PPE and fuel." Historically there has been a tight correlation between ISM Services prices and the Fed’s preferred inflation metric the Core Personal Consumption Expenditures Index (PCE). In the next few months the Core PCE will significantly climb above the FOMC’s inflation 2.0% target.

In April the Core CPI rose 0.9% which was the biggest monthly increase since April 1982. The Core CPI was up 3.0% from April 2020, which was the highest level since January 1996. The large increase wasn’t lifted by Owner’s Equivalent Rent (OER), which rose only 0.2% in April and 2.0% from April 2020. For years the PCE Housing Price Index rose by more than 3.0% before falling to 2.0% during the Pandemic. The decline was fueled by a drop in rents as people moved out of major cities into the suburbs causing rents to fall. Renters who lost their job were protected from eviction and given a moratorium from having to pay their rent, which also lowered shelter inflation. After lowering rents to attract new renters, rents are rebounding as people return to work in metro areas. The double digit increase in home prices is pulling rents higher as well. According to the Census Bureau Median monthly rent rose in the first quarter of 2021 compared to Q1 in 2020.

All of these factors will gradually bleed in coming months into the Owner’s Equivalent Rent calculation and lift Core inflation as noted in the May Macro Tides. “In March 2021 OER was 2.0%, but will rise as the rising rents bleed into the monthly calculation. OER comprises 24.1% of the CPI and Rents add another 7.9%, so the change in trend for rents will boost Core CPI in coming months.” The increase in OER will offset some of the decline in Base Effects within the Core CPI and lead to a gradual increase in the Core PCE. The Rent component of OER will tick higher in July after the moratorium on rent payments ends on June 30. According to Goldman Sachs the moratorium lowered shelter inflation by 0.25% since it was enacted, so shelter inflation could rise by an equivalent amount before year end.

Many small businesses were hurt by a decline in revenue during the Pandemic and are now dealing with an increase in costs they haven’t seen in a very long time. Even firms that benefitted from the Pandemic are struggling with higher costs. As the CEO of Kellogg recently commented, “We haven’t seen this type of inflation in many, many years.” The surge in input costs is affecting every company in each sector, so every firm is in the same boat. Businesses can raise their prices knowing that they won’t lose market share, since their competitors need to raise prices too. According to Moody’s, U.S. households accumulated an amount of excess savings during the Pandemic that is the equivalent to 12% of GDP. Consumers can now make up for the lost year and they will be less cost conscious than they were after the Financial Crisis. This is a dream come true for businesses that need to pass along some of the price increases they are absorbing. This dynamic should keep prices elevated in coming months and enable core inflation to push higher and remain significantly above the Fed’s 2.0% target for the Core PCE.

Wages

The labor market is stronger than the April employment report suggested as discussed in the May 10 Weekly Technical Review entitled ‘The Big Miss.’ “The Labor Department reported that only 266,000 were created in April compared to estimates of 1,000,000 or more. There are a number of reasons why the number fell short by such a wide margin. The Labor Department's seasonal adjustment process has been disrupted by the extreme volatility in the labor market due to the Pandemic and recovery. On an unadjusted basis the economy created more than 1 million new jobs in April for the third month in a row. This suggests job growth is stronger than the official adjusted numbers.” There are a number of reasons why job growth was less than expected, but none of the reasons reflect economic weakness. Supply chain problems are also taking a toll. Auto manufacturers, who have idled assembly lines because of semiconductor shortages, cut jobs by 27,000 in April, even though demand for vehicles is strong.

From 2011 through 2019 an average of 2.0 million Baby Boomers retired each year with 1.5 million retiring in 2019 (chart bottom of pg. 11). However, in 2020 3.2 million Boomers retired. Some of these people will reenter the labor market when herd immunity has been achieved, they feel safe, and after a few months of boredom. In the short term the excess number of Baby Boomer retirees will continue to weigh on job growth. Some mothers are still at home since schools haven’t completely reopened around the country, while others may still be too worried about contracting COVID to return to work.

The National Federation of Independent Business (NFIB) said 44% of small-business owners reported job openings they couldn’t fill in April, the highest level in records dating back to the 1970s. The Labor Department reported that the Job Openings and Labor Turnover Survey (JOLTs) for March found there were 8.1 million jobs available in March. In April the Labor Department reported that there were 9.8 million unemployed people, so job openings represented 83% of people out of work.

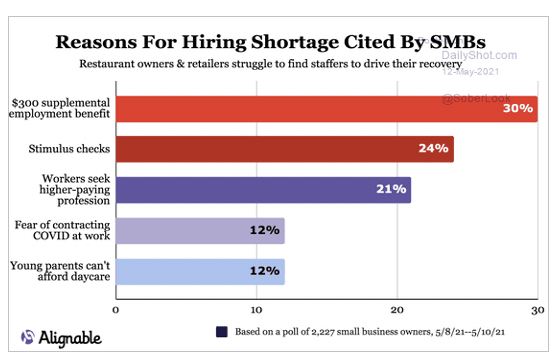

In the week ended May 8 more than 15.8 million people received unemployment benefits, including gig workers and the self-employed who are typically not eligible for such payments, according to the Labor Department. State unemployment benefits average $318 a week and Congress has added an additional $300 a week on top of regular state benefits. An unemployed worker receiving $618 a week is earning $16.07 an hour. The National Restaurant Association reported that in January 7% of restaurant operators rated recruitment and retention of workforce as their top challenge and by April that number had risen to 57%. A survey of small business owners in early May found that the majority of them (30%) believe the $300 in federal supplemental benefits is the reason why they are having difficulty finding workers. Another 24% point to the stimulus checks as why potential workers aren’t filling open positions. Paying workers not to work more than what they would earn is definitely keeping some workers from returning to work. The federal unemployment benefits will end on September 4, 2021. After listening to complaints from small business owners, more than 22 states are ending the emergency unemployment benefits by the end of June. The primary reason for The Big Miss was due to seasonal adjustment factors, but other factors played a role. The April report doesn’t change the bigger picture: a surge in job growth in the next few months is coming.

The May employment report due on June 4 could come in below forecasts. Sidelined workers who are concerned about getting sick, mothers waiting for their children’s school to reopen, or those enjoying an extended vacation funded by government benefits may result in fewer new jobs than the 675,000 estimate. Each of these reasons is going away as more people get vaccinated, every state reopens, states eliminate benefits, schools restart in-person learning, and Federal unemployment benefits end on September 4. This suggests job growth should accelerate in July and continue to be strong going into the fall.

Average weekly hours for private sector employees have reached their highest level in at least a decade. This is another reflection of employer’s difficulty in hiring new workers and should be followed by an increase in hiring. An increasing number of companies are increasing wages to attract new workers. In the first quarter wages were up 3.0%, the most in more than 20 years, according to Moody’s Analytics. High profile firms like Amazon, Costco, Walmart, McDonalds, Target, and Chipotle have increased their minimum pay to $15.00 an hour, or will do so in the next few years. Although job growth slumped to just 266,000 in April, Average Hourly Earnings jumped 0.7% or an annual rate of 8.4%. Workers in Retail saw their wages rise by 1.4% and Leisure and Hospitality workers earned 1.6% more in April, more than double the 0.7% for all workers. This is an indication that more mid size and small firms are being pressured to compete with the big name firms by raising their wages too. Changes in Unit Labor Costs in lead changes in the Core PCE and Core CPI inflation by about 3 quarters. The increase in Unit Labor Costs in Q1 is another factor suggesting that upward pressure on Core measures of inflation will persist for another 6 to 9 months.

The FOMC will watch the increase in labor costs closely since they will persist well after Base Effects and Supply Chain bottlenecks are resolved. Wages are the largest cost component for services and most goods. This is why persistent wage inflation leads to higher prices for services which represent 85% of GDP. If labor market tightness eases as schools reopen and employment benefits disappear, the upward pressure on wages evident in the April employment report should subside somewhat in the fall.

Inflation Impulse Time Line

Although Base Effects will temper headline inflation after July, strong demand will keep goods prices elevated. Supply Chain disruptions are likely to persist and also offset some of the unwinding of Base Effects. The computer chip shortage will last at least another 4 months and could endure to some extent into 2022. This will limit the increase in the supply of cars and trucks, which will keep demand for used cars and trucks high and prevent prices from falling much. Service inflation will trend higher even as headline inflation recedes. Sectors hurt by the Pandemic will increase prices in response to the surge in demand, and higher rents will lift Owner’s Equivalent Rent. Many industries are struggling to find workers and have increased wages or offered bonuses to attract new hires. If this continues more firms will be forced to increase wages in order to retain existing workers. There are many dynamics at work in the labor market that could sustain wage increases or lead to a higher plateau of annual wages increases.

Bank of America has produced a chart that pretty much mirrors my analysis of the path Core CPI inflation is likely to take for the remainder of 2021 and early 2022. In April the Core CPI rose to 3.0% and B of A’s forecast is that it will rise to 3.5% soon and then hold above 3.0% until early 2022, as noted by the dashed line. I have no idea if the Core CPI will hold near 3.5% until early 2022 given all of the moving variables. However, if core inflation significantly exceeds the FOMC’s median estimate of 2.4% for the Core PCE inflation through the end of this year, the FOMC’s ‘inflation is transitory’ narrative will come into question.

Federal Reserve

As discussed in the April Macro Tides, “As part of its Forward Guidance policy the FOMC will want to communicate months in advance any changes in its balance sheet, as any change in the federal funds rate will come after tapering. With inflation ramping higher and job growth increasing robustly in the next few months, speculation will mount as to when the FOMC will signal it’s considering tapering its $120 billion in monthly purchases.” This has begun with the April FOMC meeting minutes acknowledging a discussion about tapering occurred, “A number of participants suggested that if the economy continued to make rapid progress toward the committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.” We will hear more Fed Presidents say they are open to discussing the issue as long as the economy performs as expected, blah, blah, blah. The FOMC is on the tapering runway and it’s just a question of when the FOMC will announce the takeoff.

The May employment report may underwhelm as previously discussed and the CPI report for May could lead some people to think Base Effect inflation has peaked, as discussed in the May 17 Weekly Technical Review. “If the CPI for May comes in a bit lower than 4.2% (i.e. 3.8%) when it is released on June 10, the narrative that the pick-up in inflation is transitory would likely gain traction. The decline from 4.2% to 3.8% would allow Fed Chair Powell and the FOMC more wiggle room to hold to their narrative that this bout of inflation will prove transitory. Had the April CPI met expectations for a 3.6% increase and if May does come in at 3.8%, the psychological impact would be far different, even though the number (3.8%) is the same. In the first case headline inflation would be lower and reassuring, while inflation would still be climbing and worrisome in the second case.” In July the markets may receive a jolt if June job growth is strong (July 2 jobs report), minutes from the June 16 FOMC meeting tilt toward tapering sooner than expected (July 7), and the June CPI report shows higher than forecast core inflation when it is released on July 13.

The next six months could be tough for the FOMC as it tries to balance its messaging and the need to become less accommodative as noted in the May Macro Tides. “The FOMC is about to be tested. In the next few months many factors are going to combine to make it look like a serious bout of inflation is beginning. The current surge in prices is stronger than at any time in more than a decade. Companies have the need and opportunity to raise prices into the post Pandemic demand funded by government stimulus and they will. Headline and core inflation rates are likely to reach uncomfortable levels for a FOMC that will continue to insist this bout of inflation is transitory. This scenario could increase concerns that the FOMC may be forced to move more aggressively through balance sheet tapering and earlier rate hikes in 2022 as it tries to play catch up.” This scenario sets the stage for Treasury yields to exceed their March 30 high and a correction in the stock market.

Treasury Yields

Treasury yields soared in the first quarter with the 10-year Treasury yield climbing from 0.917% on December 31 to 1.765% on March 30 and the 30-year Treasury yield reached 2.505%, up from 1.64%. Despite the carnage in the first quarter I thought Treasury yields were about to decline, which was a true contrarian forecast. “The Treasury bond market has just experienced its worst quarter in decades and sentiment has reached a negative extreme. The price pattern in the 10-year and 30-year Treasury yield suggests they can drop by -0.25% or so in the next two months, before rising to a higher high in the second half of the year.” The 10-year Treasury yield fell to 1.471% and the 30-year treasury yield declined to 2.161% on May 7 after the employment report only showed 266,000 jobs were created in April. The price pattern in the 10-year and 30-year Treasury yields suggests that yields will climb above the March 30 highs. As discussed in recent Weekly Technical Reviews, “In the second half of this year the 10-year is expected surpass 2.0% and could reach 2.25%, and the 30-year Treasury yield is expected to climb to 2.85% and could jump to 3.15%.” If this increase in Treasury yields comes to pass the stock market will be vulnerable.

Stocks

As discussed in the April Macro Tides, I thought the stock market would hold up until mid year, as the economy improved and Treasury yields declined. “The equity market is likely to be supported by good economic news in the short run, but buffeted by the prospect of a less accommodative FOMC in the second half of 2021 and the prospects of higher taxes.”

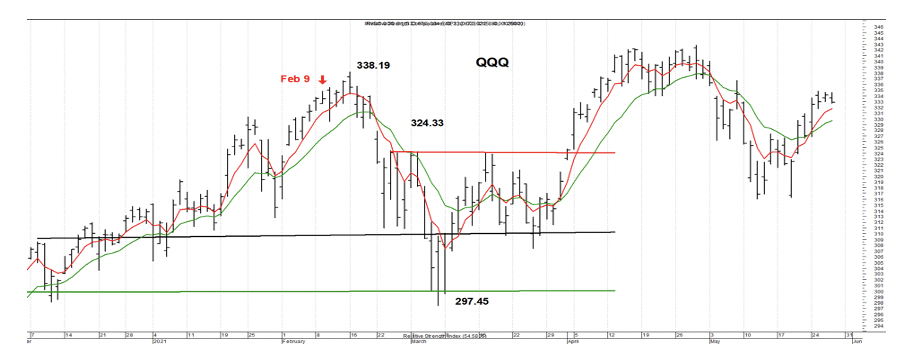

When the 10-year Treasury yield broke out above the horizontal red trend line on February 9, the Mega Cap stocks that dominate the Nasdaq 100 (QQQ) topped 3 days later on February 12. As the 10-year Treasury yield marched higher in February, QQQ dropped -12.0% until it hit an intra-day low of 297.45 on March 5. After a bounce QQQ recorded a secondary low on March 30, just as the 10-year Treasury yield was topping. As Treasury yields declined QQQ rallied to an all time high on April 29, before pulling back to another higher low on May 12. If Treasury yields drop to near their May 7 low, QQQ is expected to rally and test the April 29 high.

Industrials stocks as represented by the ETF XLI rallied even as Treasury yields rose during February and March. Investors took the rise in yields as further proof the economy was rebounding strongly. In contrast, QQQ corrected as yields rose and the Mega Cap stocks saw their valuations trimmed. I recommended the Industrial ETF XLI on February 22 and suggested buying on weakness. The Industrials ETF XLI closed at $91.27 on February 22 and traded down to $90.19 on February 23. The average recommended sell price was $103.60 so the gain from the February 22 close was 13.4%, and more if XLI was bought on weakness as recommended.

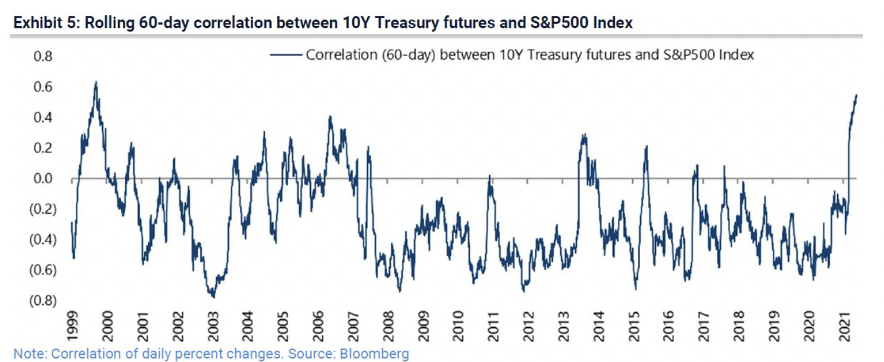

Correlation between the S&P 500 and 10-year Treasury Bonds

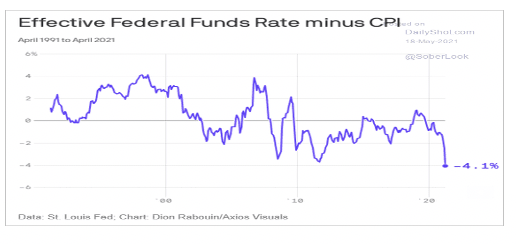

After the Federal Reserve lowered the federal funds rate to 1.75% in December 2001, the real after inflation federal funds rate became negative. In the past 20 years the real federal funds rate has been negative for most of the time. In 2006 and 2007 the real federal funds rate was positive after the Federal Reserve increased the funds rate to 5.25%. In the wake of the financial crisis the real federal funds rate has consistently been negative. Treasury bond yields fell after 2001 as the FOMC held the federal funds rate at 0% for extended periods of time, purchased trillions of Treasury bonds during Quantitative Easing programs, and by investors reaching for yield in a low yield world. The extraordinary change in monetary policy since 2001 altered the historical correlation between the S&P 500 and Treasury bond prices and could prove problematic.

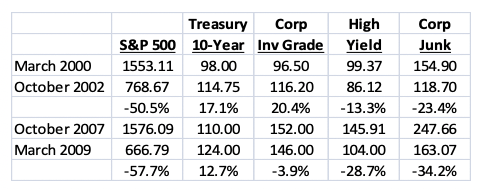

Financial advisors and investors who had a traditional allocation of 60% stocks and 40% bonds during the bear markets of 2000-2002 and 2007-2009 were insulated from equity losses that exceeded 50%. Treasury bonds rewarded diversification with meaningful gains that helped offset equity losses in both bear markets. Investment Grade corporate bonds performed well in the 2000-2002 bear market and helped portfolios during the financial crisis with only a modest decline. During both bear markets High Yield and Junk bonds lost money although far less than equities. Given this recent history many financial advisors and investors are likely to expect Treasury bonds to perform similarly in the next equity bear market.

There are two reasons why financial advisors and investors may not be rewarded with positive returns from Treasury bonds during the next equity bear market. Treasury bond interest rates peaked in 1981 and trended lower until March 2020. During this secular bull market, each high in the 10-year Treasury yield was below the prior high and each low was below a prior low, which is the definition of a downtrend in yields and uptrend in bond prices. The 10-year Treasury yield topped just below 2.0% in November (1.971%) and December 2019 (1.947%), so this level is important. The expectation is that the 10-year Treasury yield will ‘test’ this area of resistance in the second half of this year, and potentially exceed it. Should the 10-year exceed 2.0% it would send a message that the secular bull market in Treasury bonds that began in 1981 may have ended in March 2020.

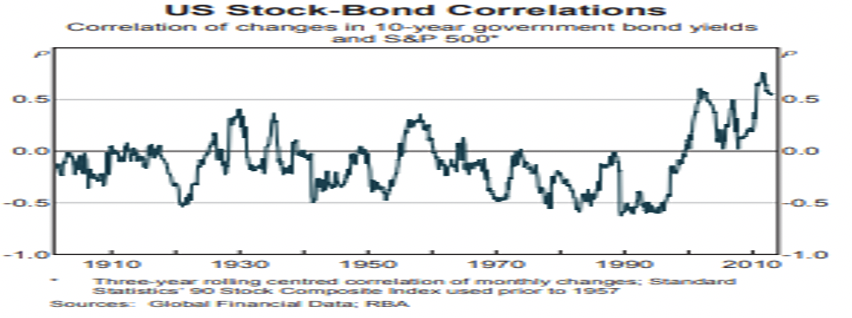

The second reason is that the negative correlation between Treasury bond yields and the S&P 500 is a relatively new phenomenon. From 1900 until 2001 Treasury yields and the S&P 500 had a positive correlation most of the time. As Treasury yields went up the S&P 500 declined, and rallied when Treasury yields fell. The exception was during the 1930’s and in the late 1950’s.

The above chart is based on Treasury yields and uses a 3–year moving average. The next chart is based on Treasury prices (futures) and uses a 60 day moving average of the correlation. Since it is based on prices and not yields, the axis of correlation is reversed with bond prices rallying while the S&P 500 falls and declining as the S&P 500 rallies. The 60-day moving is much shorter than the 3-year moving average, so it is more volatile but captures the short term swings that aren’t apparent in the above chart. In May 2013 the Taper Tantrum is clearly visible in the chart below, as the 10-year Treasury bond futures declined along with the S&P 500. This window of positive correlation between bond prices and the S&P 500 proved brief and was followed by years of negative correlation.

Starting on May 10 bond prices and the S&P 500 declined together for 7 consecutive days, which lifted the 60-day correlation to the highest level since 1999. On May 12 the Consumer Price Index hammered Treasury bonds and stocks, so higher inflation was a problem for both markets. The expectation is that inflation will continue to surge in coming months and Treasury bond prices will sink lifting the 10-year Treasury yield to at least 1.95% and potentially 2.15%. The increase in the correlation suggests the S&P 500 will decline as Treasury yields go up, with the S&P 500 falling to 3850 and potentially 3750 before the end of 2021.

Jim Welsh

@JimWelshMacro

MacroTides.com

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All