Economic Commentary: Productivity, Australia, Returning to Work

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- Today’s Investments Build Tomorrow’s Productivity

- Australia: Isolation Nation

- Returning To Work: Incentives Matter

Ryan offers thoughts on how the pandemic might affect productivity.

Last summer, I visited a newly expanded local brewpub. Once our party was seated at our reserved outdoor table, the host instructed us to access the restaurant’s online menu and order with our smartphones. All payments were made online, and the server’s only job was to carry food and drinks from the kitchen to the tables. I realized in hindsight that these enhancements allowed one waitress to attend to 20 tables at a time, without breaking a sweat. A productivity breakthrough was happening before my eyes.

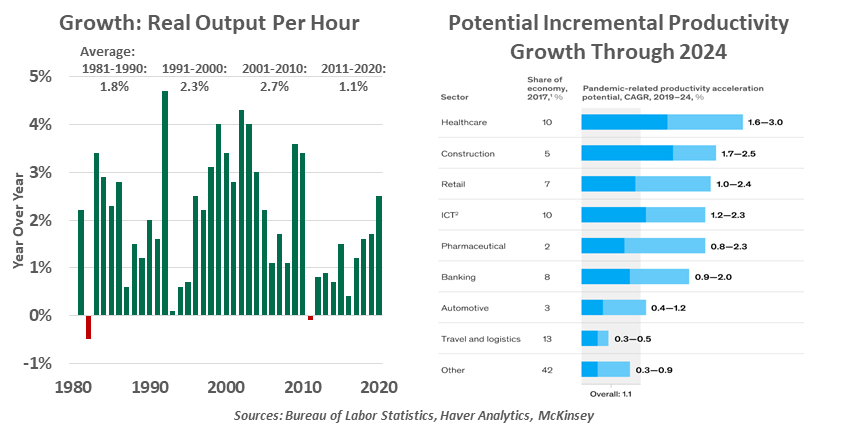

Productivity is simply the ratio of output to input: the amount produced for a given unit of input, like an hour of labor or dollar of capital. As a broad economic measure, productivity is cited in terms of a whole nation’s output divided by the total number of hours worked.

In recessions, it is common for productivity to surge. When output falls, the number of hours worked also declines. Amid layoffs, the remaining workers put in extra effort to maintain production, leading to a brief rise in productivity.

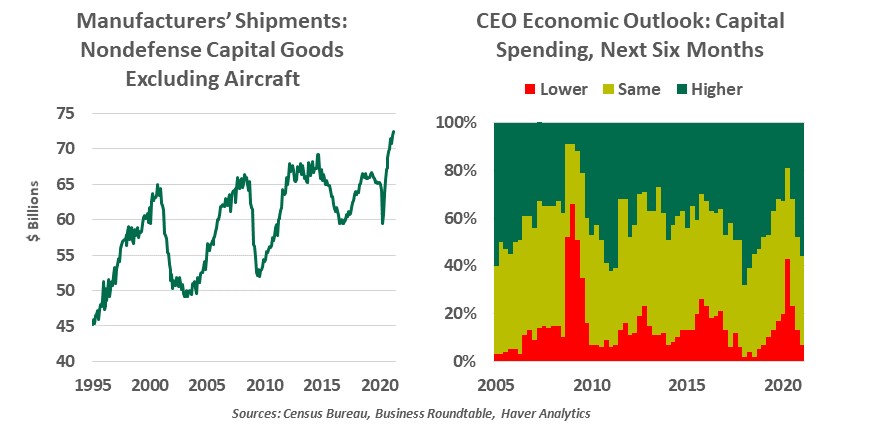

Sustained productivity growth comes from investment: either businesses invest in technology and equipment to allow their workers to produce more, or workers gain training and experience to make better use of their time. The COVID-19 downturn prompted many businesses to increase their investments to sustain operations during a disruption; now, those same investments can set a higher course for productivity growth.

A higher trend for productivity would be welcome, as the pre-COVID-19 growth cycle was one of modest productivity gains. The slow pace of recovery after the 2008 financial crisis kept employers cautious about making investments, which limited incremental efficiencies. Productivity growth is a key component for economic growth, which raises standards of living and helps to keep debt levels sustainable.

The pandemic has taken a toll on the other key ingredient in the growth equation: the labor force. Slower birth rates, a lost year of immigration, early retirements and COVID-19 deaths have diminished the long-term trajectory for labor force growth. With the supply of workers likely to expand much more slowly in the decade ahead, employers will be motivated advance their investments in technology.

|

Sluggish prospects for labor force growth support the case for investments in productivity. |

High-frequency reports of manufacturing activity show that businesses are making more capital expenditures, and surveys are also reflecting greater intent to invest. These trends bode well for the cycle ahead. In the quarters to come, economic growth will be led by the consumer recovery, but we will soon expend the sugar rush of pent-up demand. Elevated business investment will set the stage for more durable growth, and the outcomes of those investments will be a more productive workforce and moderate levels of inflation.

Measurement of productivity is notoriously difficult, and the pandemic has only complicated matters. For example, as more activity moved to e-commerce, consumers’ time spent shopping (which was “free” time spent filling carts) became monetized time, employing fulfillment workers and delivery drivers. Remote workers have likely found some of their former commute time and lunch and tea breaks consumed by work, leaving a challenge for employees and managers alike to ensure that time is spent productively.

The restaurant sector exemplifies how new technologies can become a visible piece of the customer experience, but other sectors are poised for gains in this cycle as well. Healthcare providers have increased their use of telemedicine, in many cases recommending it as the first encounter between a doctor and a patient. For routine checkups and quick consultations, the provider’s time is better spent, and the patient wastes fewer unproductive hours getting to and from the medical office; those trips are reserved for more serious problems.

Large retailers have transitioned as much as possible away from brick-and-mortar and into e-commerce, a trend that was well underway but is now a fixture of the economic fabric. Even smaller retailers have adapted to online ordering and curbside pickup, which can facilitate more transactions without adding space, inventory or headcount.

Office workers can also attest to a radical reinvention of work. Over the past year, workers stayed home out of necessity. Now, as restrictions are lifted, many workers and their bosses have found the new approach mutually suitable for the long run. Employers can reduce their rent expense by providing fewer desks, achieving the same output with a lower property cost base.

Higher productivity has wide-reaching benefits.

These gains carry high potential because they have reached all types of businesses. Historically, only the largest, leading firms in a given industry had the capital and scale necessary to make breakthrough investments. For example, Ford Motor Company could build an assembly line well before its nascent competitors could justify such a major investment. But in this cycle, advancements that can come from digitalization are available to businesses of all sizes, and this dispersion can raise average growth meaningfully.

On balance, McKinsey estimates today’s technological enhancements could boost productivity growth by one percentage point per year through 2024, a substantial gain for a measure that has shown only modest recent growth. But we must not get ahead of ourselves: demand must stay strong to keep up pressure for firms to make productive investments. Fiscal policy to support demand can help, as can nudges to support investment through the tax code.

Change does not come easily, and disruptions to routine may bring frictions. But after hard days of adapting to our evolving workplaces, we can take solace that it has never been easier to place an order for happy hour.

On An Island

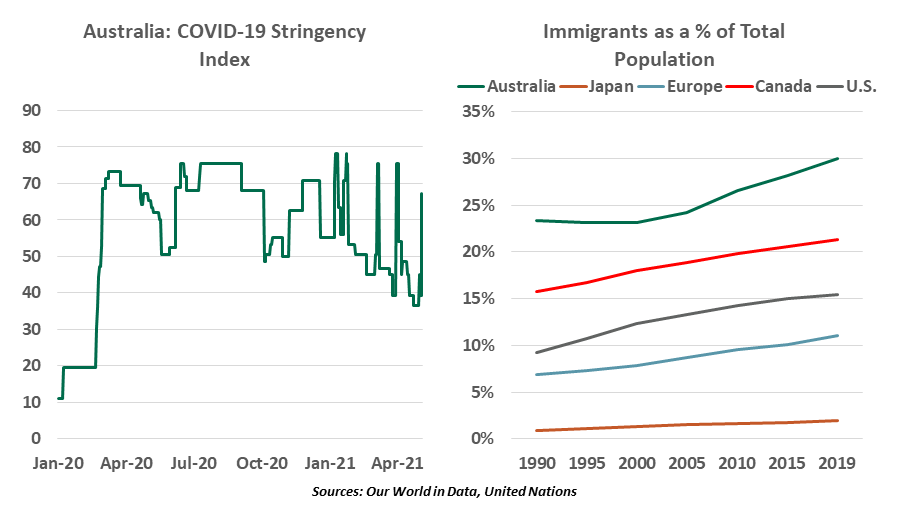

The Commonwealth of Australia, separated by thousands of miles of ocean from other major economies, has been among the more successful nations in containing the spread of COVID-19. The nation has relied on its distant geography and a figurative lifting of its drawbridge for containment. But recent experience shows that testing, tracing, quarantining and border control are not sufficient to bring the virus to heel and liberate an economy.

The pandemic led to a rarity in the modern Australian economy: a recession. 2020 marked the end of three decades of growth, which set a record. Australia’s economic recovery is now complete, underpinned by substantial fiscal and monetary stimulus. The contraction was far less severe than seen in other developed countries.

Australia’s experience with COVID-19 was another differentiator. Case counts per capita there were, and are, infinitesimal compared with Europe and the United States. The Australian government employed distancing and aggressive containment measures to achieve this result, but isolated outbreaks in individual states have still arisen. As they do, restrictions are reinstated, leading to the stop-start pattern shown in the following chart. The recent snap lockdowns in the Australian state of Victoria suggest that the virus is far from defeated.

Australia’s immunization drive has faced significant challenges. With only 2% of the population fully vaccinated thus far, the government’s target to immunize all adults by the end of the year could prove to be a Herculean task. The program has been beset with delays, partly owing to hesitancy among portions of the population.

Against this backdrop, the Australian government has decided to keep its borders closed for international travel until mid-2022. Australian citizens seeking to return home from COVID-19 hot spots have been blocked from entering Australia, and travel between Australian states has periodically been closed. This has taken a predictable toll on tourism and interstate commerce. While temporary, there are concerns that closed borders will cause a more lasting change of stance towards immigrants and immigration.

Australia is a nation built on a foundation of migration. Australia's historically strong population growth is drawn from a combination of natural increase and net migration from overseas. The newcomers now make up almost 30% of Australia’s population. With the international borders closed since the onset of the pandemic, population Down Under has declined for the first time since World War I.

|

Tourism and immigration are key to Australia’s growth story. |

Immigrants are of significant economic importance to the economy. According to the Migration Council Australia, the influx of new immigrants will create a 5.9% gain in Australian GDP per capita by 2050. Outsiders have reaped economic gains from relocation, in the form of employment and incomes, but domestic residents also benefit, through a faster rate of economic growth.

Keeping the borders closed for another year will also dent prospects for Australia’s tourism and education industries. The economy is already suffering from lost tourism, which accounts for a little over 3% of gross domestic product (GDP) and provides employment to 660,000 Australians (5% of country’s workforce). According to Ernst and Young, Australia's economy is losing $5.9 billion per month from its closed borders.

There are challenges on the trade front too, as tensions with China, Australia’s largest trading partner, are running high. As we wrote earlier this year, a lasting severance of trade ties with China will inflict visible damage on the Australian economy. Heightened tensions could also affect the tourism industry, as China is not only the largest source of international visitors, but visitors from China spend A$12.4 billion annually during their visits.

During its long expansion, Australia was dubbed by the media as “The Lucky Country.” To keep its luck from running out, Australia will have to ramp up its vaccination efforts.…and roll down the drawbridge.

Careful Calculus

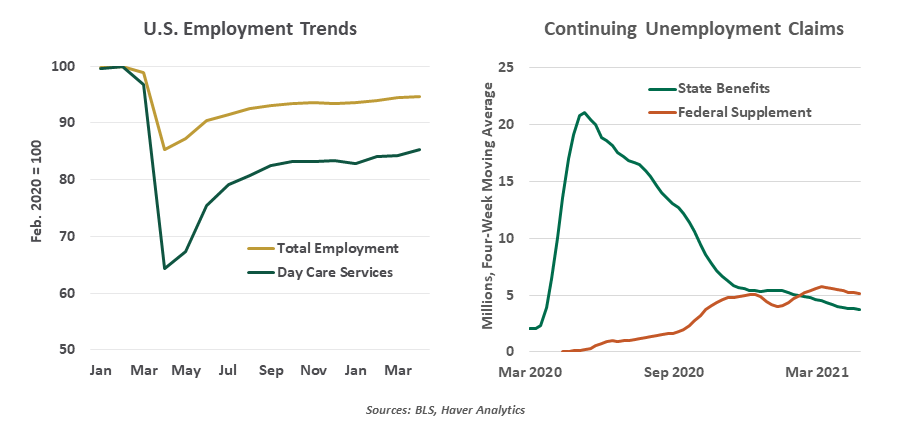

As U.S. economic activity accelerates, job openings are becoming plentiful. According to the Bureau of Labor Statistics, there are more than 8 million positions now available; that is roughly equivalent to the number of Americans that have stopped working since the pandemic started.

The comparison of the two totals isn’t entirely appropriate: there are mismatches of skills and geography between open posts and available workers. But that hasn’t stopped some observers from suggesting that people are choosing to stay away from the labor markets because jobless benefits are overly generous. To address the situation, half of the states are winding down access to the $300 per week that its unemployed citizens were receiving from the Federal government.

Theoretically, unemployment insurance payments are a disincentive to work, and they are inevitably part of the calculus that families consider when allocating time. But they are not the only economic consideration.

The closure of schools and child-care facilities has scrambled schedules, forcing parents to make alternative arrangements. In many cases, this took the form of a parent stepping away from work.

|

The cost of working is keeping some workers out of the labor force. |

The good news is that many of the jobs idled by COVID-19 are being restored. Openings in the leisure and hospitality industries have doubled since the start of the year, to more than 1 million. The bad news is that schools and day care centers continue to operate at a fraction of capacity. Barely more than half of all U.S. districts are open to full-time in-person learning. Employment among child care workers remains well below its pre-pandemic peak, and the cost of care is rising by much more than the overall rate of inflation.

Many families have concluded that the cost of caring for their children is higher than the wages they would earn by returning to work. Unemployment benefits make that an easier decision to make, but the generosity of those payments is often overstated. Many have exhausted their state-provided benefits, and the Federal supplement will expire at the beginning of September.

Restricting benefits is one way of realigning incentives. But as we’ve argued, reinforcing day care and reopening schools must be part of the mix. Getting the formula right will be critical as policy makers seek a return to full employment.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visitnortherntrust.com/terms-and-conditions

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All