Global Economic Outlook: Summer Boom

Many economies are now in advanced stages of economic reopening, but some are still struggling.

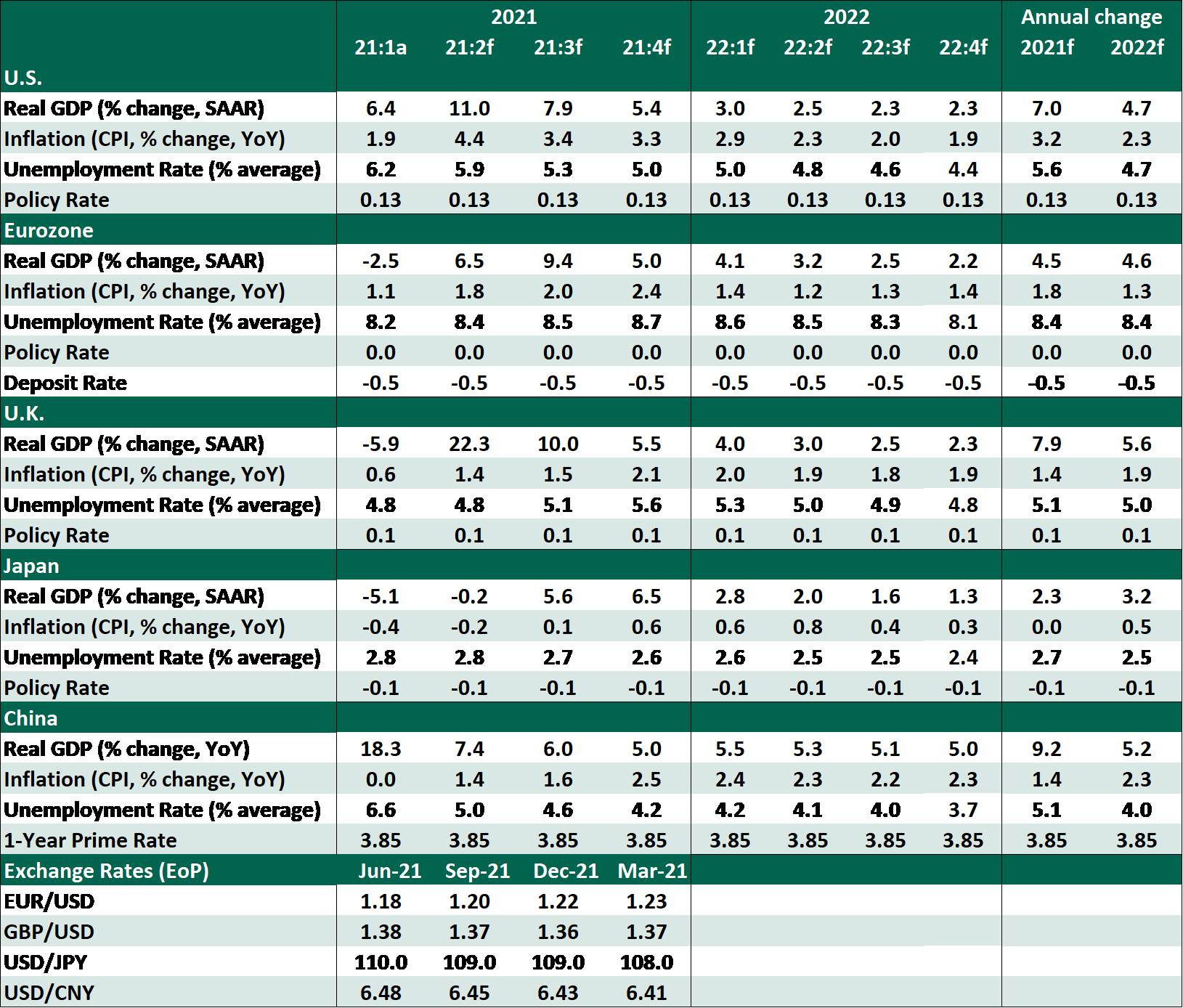

Most advanced economies are now in advanced stages of economic reopening. The incoming data of recent weeks has continued to surprise to the upside, confirming a sharp summer rebound. Economic growth is rebalancing away from goods and manufacturing and towards the services sector. A strong second quarter is expected in the U.S. and Europe on the back of relaxed COVID-19-related restrictions.

In contrast, Japan and emerging markets outside China are likely to see growth slow or even contract in the second quarter due to a surge in COVID-19 cases. These situations illustrate that rising infections remain a key risk to public health and economic performance.

For most economies, the current rise in inflation is driven by positive base effects, temporary shifts in supply and demand dynamics and some idiosyncratic events. We expect inflation to moderate as the year progresses, as supply rises and demand ebbs.

This month’s edition offers a deep dive into the economy of Japan, which has struggled lately to contain infections.