Rising interest rates generated negative year-to-date returns for investment grade bonds in 2021, but the second half of the year looks more promising. We believe the combination of reduced supply and strong demand will create attractive opportunities, and we are constructive on corporate credit and asset backed securities (ABS).

2021 Performance: Tighter Spreads Were Overshadowed by Rising Rates

The start of 2021 was a challenging period for investment grade (IG) fixed income investors, as rates increased substantially from their pandemic lows, creating losses across the IG spectrum. Investment grade corporates did not go unscathed, returning -2.85% year-to-date as of the end of May.

As we’ve discussed in previous corporate reviews, the asset class is vulnerable to rising rates as duration exposure remains near all-time highs – a natural consequence of corporations issuing longer maturity bonds to take advantage of record low yields during the past few years. The option adjusted duration (OAD) of the Bloomberg Barclays IG Corporate Index was at 8.59 years as of May 31 (vs. 7.10 on 12/31/18).

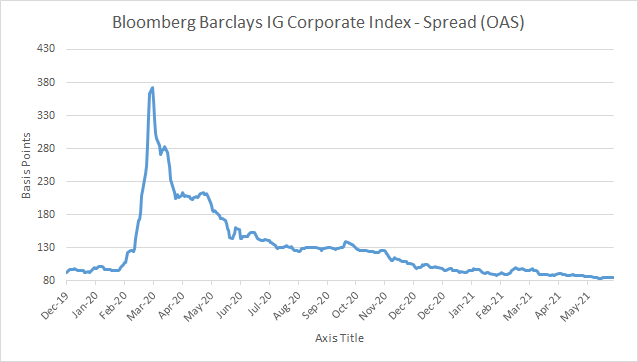

Fortunately, the interest rate losses were somewhat offset by tighter spreads, which helped corporate bonds outperform all other IG sectors. Spreads tightened throughout the period, ending May at 83.5 basis points, which is tighter than pre-pandemic lows.

Source: Bloomberg

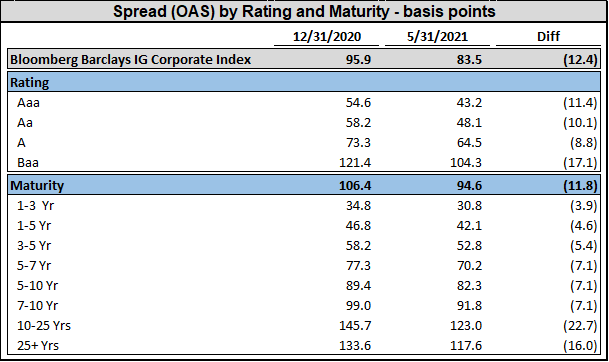

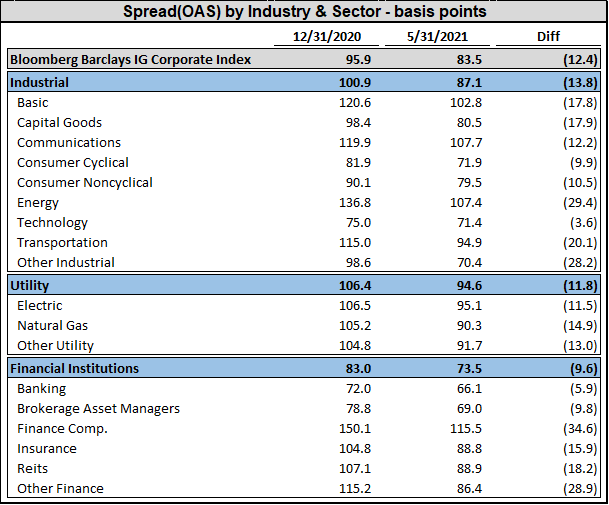

IG corporates outperformed duration-matched Treasuries by 1.54% as of May 31, with spreads tightening 12.4 basis points over the period. As the economy showed signs of reopening, investors piled into areas exposed to higher risk in search of yield. BBB/Baa rated bonds particularly outperformed, as did longer maturity issues. In addition, spreads tightened materially in sectors that were most impacted by the pandemic, including Energy and Other Finance (which includes aircraft lessors, where we have been investing).

Source: Bloomberg

Given the tight spreads across the index, it is likely that these trends will continue despite the Federal Reserve’s announcement that it would gradually begin selling its corporate bond holdings, as the search for yield continues to drive investment decisions. The reopening economy and continued fiscal/monetary support remains a catalyst for higher risk areas to continue to attract attention.

Credit Fundamentals Improved

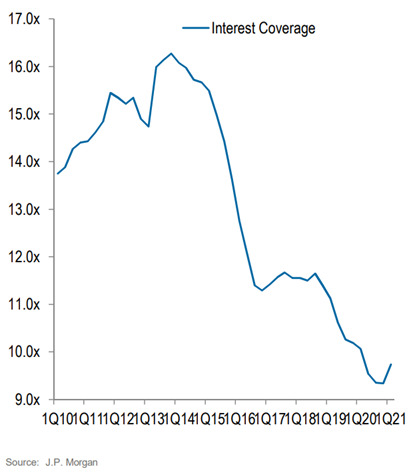

Credit fundamentals took a small positive turn during the first half of 2021. For the first time in nearly a decade, corporations reduced debt, which also decreased leverage and improved interest coverage ratios. IG borrowers benefitted from many of the stimulus packages put in place to mitigate the effects of the pandemic, and they were also able to control expenses due to the massive increase in employees working from home.

The combination of strong revenues and reduced expenses allowed corporations to let maturing debt expire without replacing it with new bonds. Additionally, the impact of the prolonged period of low interest rates and tight corporate spreads has continued to drive interest expense lower, which has led to an improvement in the interest expense coverage ratio.

The rating agencies responded positively to the improvement in credit metrics. The net ratings changes moved decisively positive in the first half of 2021, as May saw a record $127 billion in net credit ratings upgrades. To put this in context, at the start of the Covid-19 lockdowns last year, the change in ratings was a net downgrade level of $528 billion in March and another $409 billion in April.

We have also seen a dramatic reduction in concern about fallen angels, such that only $8 billion of BBBs now trade wide to the BB index level. When compared to the total size of the IG market (nearly $8 trillion), that is a very small and manageable volume should they ultimately end up getting downgraded.

Market Technicals Improved Even More

The investment grade market has also benefitted significantly from a positive technical backdrop. Most notably, the new issue volume for the first half of 2021 is nearly one-third less than in 2020. Much of this is due to the spike in issuance last year, as corporations hoarded liquidity while the economy shut down during the pandemic. This has led to a negative net supply year-to-date, as the amount of maturities/calls and tenders are exceeding the volume of issuance.

The steady inflows into investment grade funds provided an additional tailwind to corporate bonds. With the exception of one brief three week stretch, the market has experienced positive weekly inflows into high grade mutual funds and ETFs for the past 12 months. Not surprisingly, the combination of reduced supply and strong demand has been a major driver of the spread tightening discussed above.

Current Positioning: Reopening Bonds, Asset Backed Securities

Given the current market dynamics – improving credit and strong technicals – we are looking to make investments in areas where we see spread tightening opportunities. As the Bloomberg Barclays IG Corporate Index remains near historically tight levels, security selection continues to remain of upmost importance.

Within our corporate exposure we continue to focus on the reopening theme and invest in areas that we believe will benefit from pent up demand. We continue to like specific credits in areas such as aircraft leasing and hospitality, as we believe robust consumer demand for travel will enhance financial performance and offer value at relatively wider spread levels. We see less value in short, highly rated IG bonds, as they trade at very tight spreads. These issues have minimal carry and, in our view, little opportunity for appreciation, so we have substantially reduced our position in them.

Instead, we have rotated into asset-backed securities (ABS), which currently trade at wider levels compared to similarly rated corporates and have short maturity profiles (one to three years). In addition, the ABS sector very much aligns with our current macro view. ABS bonds are collateralized by income producing pools of assets such as loans, and the current environment should continue to be beneficial for borrowers to service their debts and for lenders to mitigate losses from defaults by liquidating assets at elevated prices.

We particularly like deals backed by auto loans, as we believe both the borrowers and the collateral are well-positioned. Likewise, we see opportunities in non-agency mortgages, as housing prices remain elevated due to low interest rates, building supply shortages, supply/demand imbalances, and borrowers unwilling to go into foreclosure. We continue to rotate our portfolio into short ABS positions and out of the tighter corporates when we see attractive relative value, and we will continue to do so as deals continue to perform well.

Looking Ahead: Opportunities Exist

The IG credit market experienced a roller coaster ride in 2020, along with most risk assets. The dramatic widening of credit spreads highlighted the vulnerability of a nearly $8 trillion market that has very few built-in shock absorbers and limited capacity to handle substantial selling pressure during periods of stress. Thanks to monumental support from the Fed, the market recovered quickly, and we believe that as long as Fed support remains in place until the pandemic passes, the IG market should remain stable for the foreseeable future. We feel the key to successful investing in the current environment is avoiding weak credits and fallen angels, as Fed support cannot provide protection against losses from individual securities.

Looking forward, we remain constructive on corporate credit even though the vast majority of the recovery in spreads has likely already occurred. We are expecting spreads to tighten a bit further, primarily due to technical performance drivers. Specifically, the combination of (1) anticipated slower pace of issuance for the balance of the year, (2) supply leaving the market through downgrades and tenders, and (3) ongoing strong investor demand will likely create tighter spreads.

In addition, we feel that the dispersion of returns in the index indicates that there are still many compelling opportunities within the IG universe. Although the specific constituents of the Agg sectors may be misleading or unexpected, the index can still be used as an effective guide to help find investment opportunities. We have always believed careful security selection and rigorous fundamental credit analysis are the foundation of performance, and that is especially true in a world upended by Covid-19. With so many sectors still wider to the index than their pre-pandemic levels, we believe there is a rich opportunity set to pursue.