Delta Force, ECB's Strategy Review, State of the States

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- Delta Force

- The ECB’s New Groove

- State and Local Governments: Back In Business

The recent holiday weekend here in the U.S. was a joyous one in our home. My wife was able to gather with her sisters on July 4 for the first time in 18 months. While they had kept touch virtually during the pandemic, visiting in person proved emotional and restorative. It went so well that my wife invited everyone back the next day for another dinner…which I was happy to prepare.

Jokingly, I suggested that we take advantage of being together to roll out raviolis for the holidays. (The work is normally done just after Thanksgiving, with the output frozen for Christmas.) My suggestion got a big laugh, as everyone assumed that the pandemic was fading and that we would be free to gather at regular intervals going forward.

I am wondering whether I should have pushed the group harder on pasta production. Wave three of COVID-19 is appearing in a number of countries, the U.S. among them. The dominant variant, referred to as “Delta,” is allowing the virus to spread rapidly. With vaccination programs incomplete, public officials around the world may have to consider renewed restrictions. The pandemic, and its impact on the global economy, is still very much with us.

It’s been almost a year and half since COVID-19 emerged in a significant way. During that interval, a broad range of strategies have been employed to bring contagion under control. Among them, vaccination has proven to be the most effective and durable. Rising rates of vaccination have allowed the lifting of public health restrictions in many locations, and commerce has boomed.

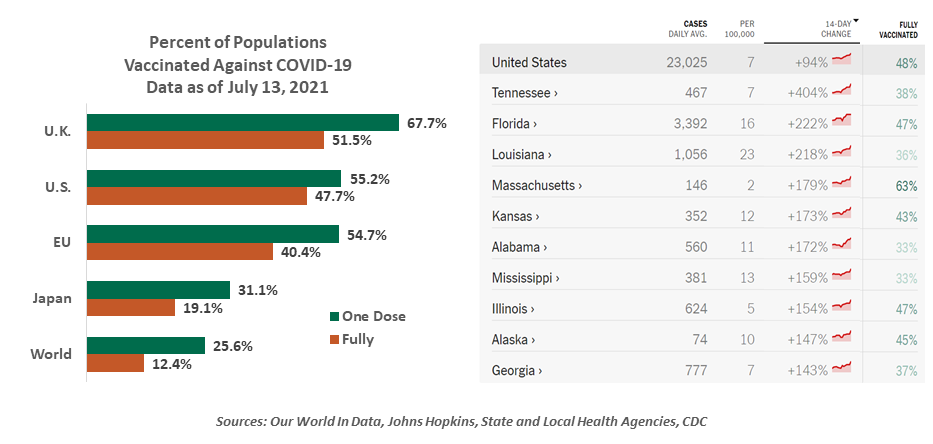

Vaccination rates vary quite a bit from place to place. In the United States, 48% of the population has been fully vaccinated, but state-level figures show a range of 37% to 75%. States with low vaccination levels are seeing some of the biggest increases in cases.

Internationally, the dispersion is even greater. Japan and Australia, for example, recently implemented new COVID-19-related restrictions to protect populations whose full vaccination rates are only 19% and 9%, respectively. Japan’s low level of coverage forced them to ban spectators from the upcoming Olympic Games. Russia and China are reportedly experiencing new surges of COVID-19 cases; their citizens are covered by vaccines of their own making, which have proven much less effective against the Delta variant. Many emerging markets have barely started on vaccination, and remain especially vulnerable.

|

Despite aggressive campaigns, vast portions of populations remain unvaccinated. |

The development of COVID-19 vaccines was a tremendous achievement, and vaccination programs in developed markets gained steam after slow starts. But the data suggest that these efforts have stalled. In the United States, daily doses have declined by more than 80% from the peak reached in April. To some degree, this was expected; those who remain uncovered live in more remote locations or are hesitant to be vaccinated. But coverage levels in most countries remain well below what scientists think is necessary to deliver herd immunity.

Those vaccinated by more reliable products still have a high level of protection against the Delta variant. And if they contract it, they are highly unlikely to require hospitalization. But majorities in many U.S. states and many countries are uncovered and remain vulnerable to the full consequences of COVID-19. In these areas, hospitalizations are increasing, and intervention from public health officials is becoming more likely.

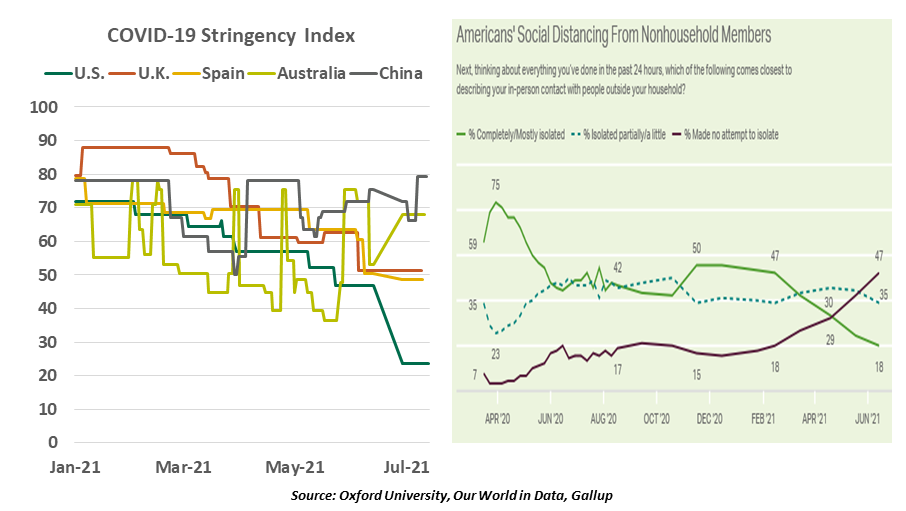

A decision to reimpose restrictions will be a difficult one. Citizens in many countries are enjoying their newfound freedom, and will be loath to take a step backward. In the United States, limitations have fallen quickly, as have personal precautions.

Schools are scheduled to begin reopening in just over a month; bringing students back to full-time, in-person instruction is critical. Apart from providing pupils a better learning experience, reopening classrooms will allow parents to participate more actively in the labor force.

But with the Delta variant spreading and children ineligible for vaccines, there will certainly be parents who will push back against in-person attendance. Those same parents may hesitant to return to offices. Many firms have initiated efforts to bring workers back together, but establishing a sense of safety is essential to success. Even if formal restrictions are not reintroduced, a heightened sense of risk among populations will create complications for commerce.

The third wave of infection that is developing could also hinder global supply chains. Already strained by the pandemic, international production and shipping systems will be further challenged if component countries have to sustain restrictions. International tourism is still a fraction of what it used to be; Delta will extend the slump in global travel.

|

The Delta variant will complicate reopening efforts around the world. |

The ongoing interruptions caused by COVID-19 are also contributing to inflation in developed markets. This week, both the United States and the United Kingdom reported higher-than-expected increases in their price levels. Fear of infection is one of the reasons why workers have been hesitant to rejoin the labor force; difficulty in securing adequate staff has forced wages and prices up in a range of service sectors. The pandemic is also partly accountable for sizeable increases in the cost of shipping, which is being passed along to consumers.

As we have been saying for the past year and a half, the path of the economy depends critically on the path of COVID-19. Diseases of this kind rarely die out quietly; they tend to mutate in unpredictable ways that allow them to persist. Societies will be challenged to manage, and manage with the virus, which may require lasting changes to behavior and business practices. Ravioli production in July may not be ideal, but our family may need to adapt to changing circumstances.

Scope Creep

The story of central banks goes back to the seventeenth century with the establishment of the Swedish Riksbank, which was tasked with lending the government funds and acting as a clearing house for trade. Central bank mandates have come a long way since then, broadening to include objectives of economic and financial stability.

At present, many central banks are reworking their mandates, refining old objectives and adding new ones. The European Central Bank (ECB) is the latest one to have completed a review of its strategy, with results published last week. Some outcomes were sensible, and expected; others, a bit more aspirational.

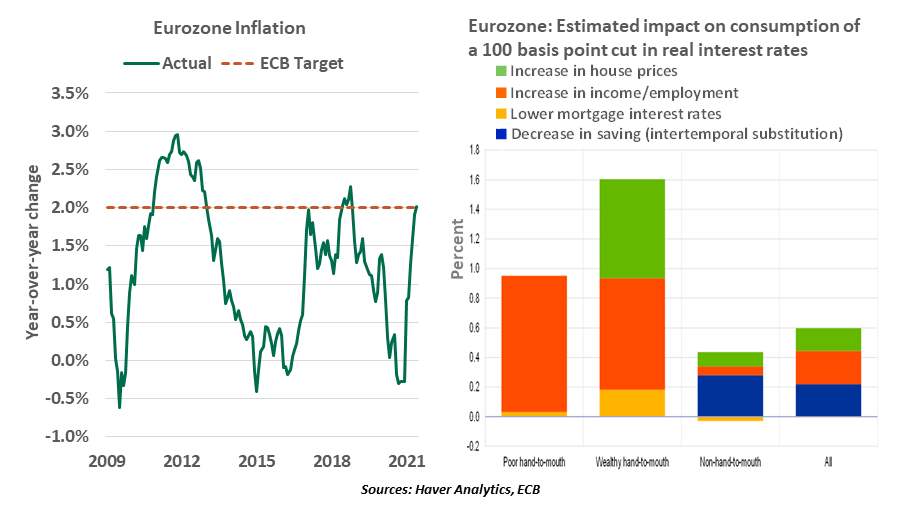

The ECB’s 19-month-long review, the first since 2003, concluded with a fundamental shift in how the central bank defines its core mandate of price stability. After years of undershooting its inflation objective, the ECB ditched its target of “close to, but below, 2%”, an opaque phrase that implied a cap on price growth. Instead, it will now have a symmetric inflation target, and will tolerate a transitory period in which price increases are moderately above target, when deemed necessary. The ECB’s step is in keeping with the new approach to inflation targeting announced by the Federal Reserve last year.

The Governing Council also confirmed that the harmonized index of consumer prices (HICP) remains the appropriate price measure, but called for inclusion of owner-occupied housing (OOH) in the inflation calculations. The move will have a small impact, estimated to boost inflation by 0.2 percentage points—but when low inflation is a struggle, every bit helps.

One frontier facing monetary authorities is climate risk. Merely gaining agreement to take on the topic is no small feat. Many believe the issue is best left to legislatures to be addressed. It is a broader challenge than any central bank alone could address, and mixing environmental mandates with financial regulations could easily lead to undesired outcomes.

However, climate change can have profound implications for economic and price stability, warranting central banks’ attention. The ECB announced it will adjust the allocation of its corporate bond purchases, within their mandate, to investing more in green bonds. The move could attract further political criticism, as allocating capital from countries to corporates will likely raise more eyebrows. Unfortunately, corporate bonds account for only a portion (less than 10%) of the ECB’s net asset purchases, which are heavily concentrated in sovereign debt. Moreover, small changes in funding costs are not the most efficient way to meet emissions goals. Fiscal and structural policies will be needed to address this issue.

|

Fixing climate change and inequality is primarily the responsibility of elected governments. |

And if that weren’t enough, monetary authorities are considering what they can do to address the unequal distribution of income. While the ECB didn’t focus on inequality in its strategy review, it has been pushing for deeper analysis on the subject. In the eurozone, monetary easing has not only led to a substantial reduction in the unemployment rate, but also reduced inequality by helping lower-skilled workers find employment and boost incomes of poorer households (see above chart).

Some studies have shown that easy monetary policy tends to increase inequality. Lower interest rates and quantitative easing lead to increased asset prices, benefitting those at the top of the income pyramid; the gains to lower earners are limited. However, in a recent report, the Bank for International Settlements concluded that “inequality is largely the result of long-term structural forces that are independent of monetary policy.”

Central banks cannot fix climate change and inequality alone, as they lack the mandates and tools to target these challenges. Fiscal policies, along with structural reforms, will hold the key in addressing these pervasive challenges. However, central banks can certainly provide support with virtuous prudential regulations and by focusing on their core policy objectives.

The ECB is hoping that setting a more sensible inflation target will bolster its credibility. But broadening its horizons to address social issues may expose it to legal and political resistance.

Tax Relief

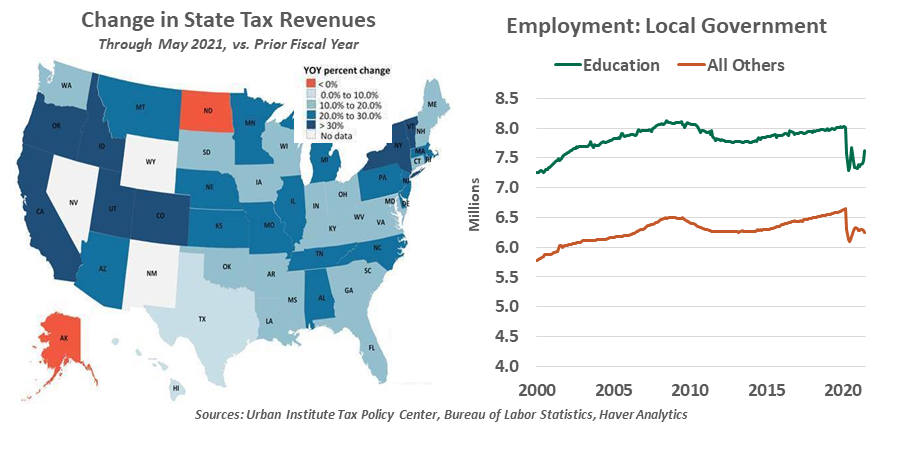

While sorting the economic wreckage of the pandemic last year, we were especially worried about the fate of state and local governments. A year later, we are glad to report that they are not only still standing, but thriving.

States and municipalities fund themselves through a some mix of sales, personal income, corporate income and property taxes. Each of those appeared to be at risk when COVID-19 struck. Commerce shut down, immediately curtailing sales taxes. Contractions impair corporate income, lowering business tax receipts. Businesses respond with layoffs that cut into income taxes while increasing the demands for support programs like unemployment insurance.

|

Rumors of demise among state and local governments were greatly exaggerated. |

The fear was not merely hypothetical. At the height of lockdowns, local leaders used layoffs to stay solvent. Job losses for state and local government employees were immediate and unprecedented; the sector had usually been stable through past recessions. Budget cuts affecting schools, public works and first responders risked diminishing local quality of life.

But as we know, commerce merely paused for a few months in 2020. While in-person experiences were curtailed, households spent more on goods, a composition shift that was beneficial: A majority of states do not tax services but do charge tax on sales of goods. The move to e-commerce was not a problem, as the Supreme Court’s Wayfair decision in 2018 endorsed a requirement for online sellers to collect and remit local sales taxes, even if they do not have facilities in the buyer’s state.

As more people returned to work, income tax collections returned closer to their normal levels. Meanwhile, high home prices will keep a floor on assessments for property taxes. And to ensure a minimum of scarring, federal stimulus included support for local governments. An Urban-Brookings Tax Policy Center survey of state financial officers bears out the good news: On average, total state revenues declined only by 1% in fiscal year 2020, while 2021 is forecast to result in 6% growth. A feared wave of municipal bankruptcies did not emerge, and muni bond investors can expect a resilient year ahead.

The recovery is not complete. As of June, employment in state and local government institutions, such as schools and transit systems, remains one million workers below its February 2020 peak. We are optimistic for tax receipts to stay elevated and the employment recovery to continue.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All