What’s the Message from Treasury Yields?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTreasury Yields Befuddle

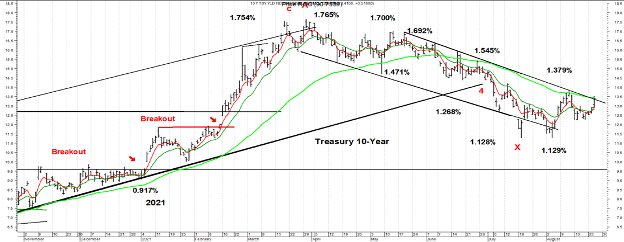

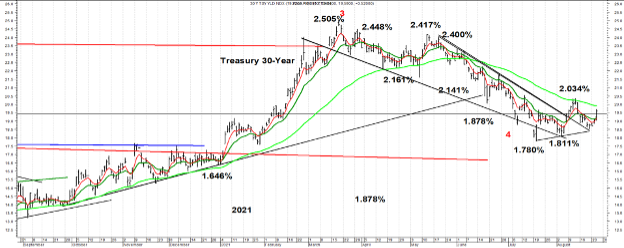

The 10-year Treasury yield finished 2020 at 0.917% and then climbed to 1.765% before topping on March 30. The 30-year Treasury yield rose to 2.505% on March 18 after ending 2020 at 1.646%. In the January 11 Weekly Technical Review (WTR) I noted that Treasury yields had broken out to the upside and that the 10-year Treasury yield would likely climb to 1.75% to 1.95% in 2021. “Treasury yields broke out on January 6 as expectations of more fiscal stimulus and technical selling kicked into gear. At some point in 2021, the 10-year Treasury yield could spike up to 1.75% to 1.95%.”

After the 10-year Treasury yield reached 1.765% in March the consensus was that it would quickly run to 2.0%. In the April 5 WTR the expectation was that Treasury yields were more  likely to fall than rise further. “After Treasury bonds experienced the largest decline in a single quarter, sentiment is even more negative according to the weekly survey by Consensus. In the last decade sentiment has only become this negative on four other occasions. This suggests that Treasury bond yields could fall for a period before the rising trend reasserts itself. In this instance the 10-year could fall to 1.50% as the 30-year drops to 2.25% at a minimum. TLT has the potential to rally to $143.00. Once this decline in yields runs its course, Treasury yields are expected to rise to higher highs in the second half of 2021.” Treasury yields did decline in the following four months and by more than expected.

likely to fall than rise further. “After Treasury bonds experienced the largest decline in a single quarter, sentiment is even more negative according to the weekly survey by Consensus. In the last decade sentiment has only become this negative on four other occasions. This suggests that Treasury bond yields could fall for a period before the rising trend reasserts itself. In this instance the 10-year could fall to 1.50% as the 30-year drops to 2.25% at a minimum. TLT has the potential to rally to $143.00. Once this decline in yields runs its course, Treasury yields are expected to rise to higher highs in the second half of 2021.” Treasury yields did decline in the following four months and by more than expected.

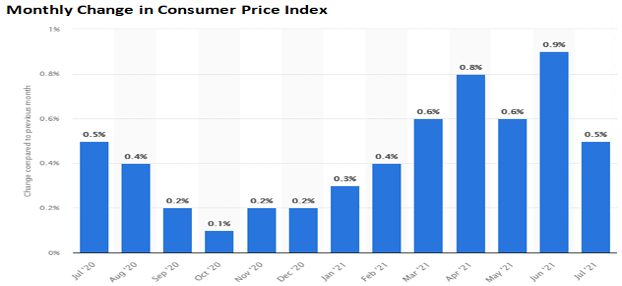

What made the decline in Treasury yields all the more befuddling for Wall Street and many analysts was that it occurred against a back drop of a significant acceleration in inflation as measured by the Consumer Price Index (CPI in April, May, June, and July). Although the month over month CPI only rose by 0.5% in July, it’s still rising at a 6.0% annual rate.

The 10-year Treasury yield fell to 1.128% on July 20 and the 30-year dipped to 1.780%. The decline in Treasury yields in the face of a multi-decade high in headline and Core inflation has led many on Wall Street to proclaim: “The bond market is looking through the surge in inflation and is telling me that this bout of inflation will prove transitory just as Chair Powell has said.” This is another example of the ‘Markets are a discounting mechanism’ that is repeated virtually every day on CNBC and other business shows. Let’s see, in March Treasury yields were projecting an increase in the 10-year to 2.0%, but now that yields have come down, Treasury yields are saying inflation is a whiff.

If Treasury yields rise as expected in coming months, the same folks will be saying, “Yields are going up because the Treasury market believes inflation won’t be transitory.”

Treasury yields are likely to rise before year end as the favorable supply / demand conditions that have dominated in recent months gives way to a much less favorable environment. Core inflation is expected to remain stubbornly high into the first quarter of 2022, which will only throw gas on the huge increase in supply fire coming in the fourth quarter.

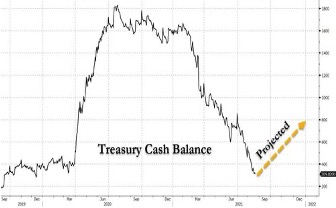

In the second and third quarter of 2020, the Treasury built up a large balance at the Federal Reserve since Congress was expected to pass another large spending bill in August 2020.  That $900 billion relief bill didn’t pass until December 2020. As a result of not spending much money in the fourth quarter of 2020, the Treasury had a balance of $1.6 trillion at the Federal Reserve in the first quarter of 2021. In March Congress passed another $2.1 trillion bill which led to the Treasury’s balance falling sharply as the Treasury disbursed funds. The major point is that the Treasury didn’t have to issue new Treasury debt in the second quarter because of the large balance at the Federal Reserve. While new issuance was almost nothing in the second quarter, the Federal Reserve’s monthly purchase of $80 billion of Treasury debt absorbed all of the issuance. This created an extremely favorable environment for Treasury yields to decline, even as inflation was exceeding expectations by a wide margin.

That $900 billion relief bill didn’t pass until December 2020. As a result of not spending much money in the fourth quarter of 2020, the Treasury had a balance of $1.6 trillion at the Federal Reserve in the first quarter of 2021. In March Congress passed another $2.1 trillion bill which led to the Treasury’s balance falling sharply as the Treasury disbursed funds. The major point is that the Treasury didn’t have to issue new Treasury debt in the second quarter because of the large balance at the Federal Reserve. While new issuance was almost nothing in the second quarter, the Federal Reserve’s monthly purchase of $80 billion of Treasury debt absorbed all of the issuance. This created an extremely favorable environment for Treasury yields to decline, even as inflation was exceeding expectations by a wide margin.

In 2016, 2018, 2019, and in 2020 before the Pandemic, the Treasury maintained a balance of $350 billion to $400 billion at the Federal Reserve. Congress failed to increase the debt ceiling by July 31, so the Treasury can’t issue new debt and has  been instead winding its cash balance below $400 billion at the Federal Reserve. The Treasury’s balance at the Fed will continue to fall until Congress does increase the debt ceiling. If Congress fails to act, sometime in late October the Treasury’s balance will be $0 and the federal government will be forced to shut down. In the current partisan firestorm anything can happen.

been instead winding its cash balance below $400 billion at the Federal Reserve. The Treasury’s balance at the Fed will continue to fall until Congress does increase the debt ceiling. If Congress fails to act, sometime in late October the Treasury’s balance will be $0 and the federal government will be forced to shut down. In the current partisan firestorm anything can happen.

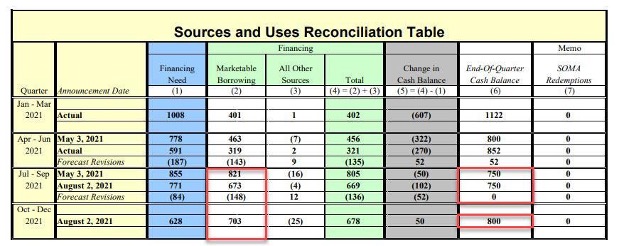

Sooner or later Congress will increase the debt ceiling (likely after some 11th hour shenanigans and drama), which will unleash a torrent of Treasury debt issuance. In the third quarter the Treasury had expected to issue $673 billion of new Treasury bonds. (Column 2 Marketable Borrowing in the table below) If Congress dallies until the end of September, the Treasury’s balance at the Fed could be down to $150 billion or less. The Treasury could be expected to lift its balance toward $400 billion and issue $673 billion of new debt it had planned to issue in the third quarter AND another $703 billion it had planned to issue in the fourth quarter. In total, the Treasury may issue $250 billion, $673 billion, and $703 billion = $1.626 trillion of new Treasury debt in the fourth quarter. After no meaningful new supply in the second quarter and until Congress increases the debt ceiling, the mountain of supply coming in the fourth quarter may give Treasury bond traders a severe case of Whiplash. (If you don’t want to wait until the fourth quarter to watch a whiplash, you can watch Whiplash the movie. https://www.youtube.com/watch?v=fHAfUSBc0pg

Federal Reserve Distorts the Treasury Market

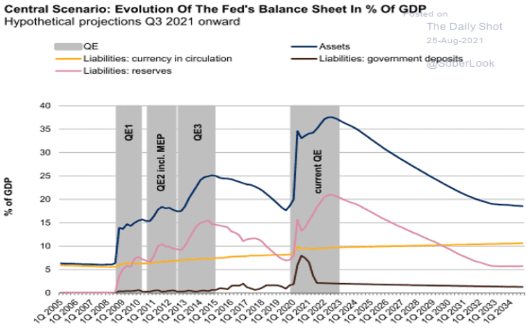

In response to the financial crisis the Federal Reserve increased its balance sheet from $900 billion in 2007 to $4.5 trillion in the fourth quarter of 2014. In 2018 the FOMC decided to  gradually shrink the balance sheet and by August 2019 the Fed’s balance sheet was ‘down’ to $3.76 trillion. At that level the Fed’s balance sheet was 4 times its pre-financial crisis level after 10 years of economic growth. If the Fed can’t shrink its balance sheet back to a normal level after 10 years of growth, it will never be able to shrink it. After reversing course on raising the federal funds rate anymore in December 2018, the FOMC began to allow the balance sheet to expand and by February 2020 it was $4.18 trillion. As a percent of GDP the Fed’s balance sheet reached 25% in 2015, 18% in August 2019, after the Fed shaved its balance sheet by $800 billion and GDP continued to grow.

gradually shrink the balance sheet and by August 2019 the Fed’s balance sheet was ‘down’ to $3.76 trillion. At that level the Fed’s balance sheet was 4 times its pre-financial crisis level after 10 years of economic growth. If the Fed can’t shrink its balance sheet back to a normal level after 10 years of growth, it will never be able to shrink it. After reversing course on raising the federal funds rate anymore in December 2018, the FOMC began to allow the balance sheet to expand and by February 2020 it was $4.18 trillion. As a percent of GDP the Fed’s balance sheet reached 25% in 2015, 18% in August 2019, after the Fed shaved its balance sheet by $800 billion and GDP continued to grow.

In response to the Pandemic the FOMC has rapidly expanded its balance sheet to $8.34 trillion in mid August 2021 and 35% of GDP. Even if the FOMC decides to taper its purchases the Federal Reserve’s balance sheet will continue to grow.  If the FOMC lowers its purchases from $80 per month to $70 billion per month, its balance sheet will be $720 billion larger after 12 months of tapering. If the FOMC cuts its monthly purchases to $65 billion, the balance sheet will be $480 billion larger eight months later. Many have referred to tapering as tightening which is not accurate as the Fed’s balance sheet will grow. If the FOMC was driving a car, the car would decelerate from 60 mph by 6 miles per hour per month. By this measure the FOMC will modestly take its foot off the gas and let the car gradually slow down. This is not the equivalent of hitting the brakes.

If the FOMC lowers its purchases from $80 per month to $70 billion per month, its balance sheet will be $720 billion larger after 12 months of tapering. If the FOMC cuts its monthly purchases to $65 billion, the balance sheet will be $480 billion larger eight months later. Many have referred to tapering as tightening which is not accurate as the Fed’s balance sheet will grow. If the FOMC was driving a car, the car would decelerate from 60 mph by 6 miles per hour per month. By this measure the FOMC will modestly take its foot off the gas and let the car gradually slow down. This is not the equivalent of hitting the brakes.

As the Fed’s balance sheet has grown so has it holdings of Treasury Bills, Treasury Notes, and Treasury Bonds. Treasury Bills have a maturity of up to one year. Treasury notes have maturities of 2, 3, 5, 7, and 10 years.  Treasury Bonds have a maturity of 20 and 30 years. On January 20, 2020 the Fed’s balance sheet was $4.15 trillion and increased by $4.19 trillion to $8.34 trillion in August during the Pandemic response. Since February 2020 the Fed’s holdings of Treasury Notes and Bonds has jumped from $2.2 trillion to $4.5 in August representing 54.9% of the increase. The New York Federal Reserve has provided a breakdown by maturity of the Fed’s Treasury holdings. The Fed now owns about 53% of all the outstanding Treasury Notes and Bonds that have a maturity of 10 to 20 years, almost 30% of Treasury Notes with a maturity of 7 to 10 years, and 30% of Treasury Bonds with maturities of 20 and 30 years.

Treasury Bonds have a maturity of 20 and 30 years. On January 20, 2020 the Fed’s balance sheet was $4.15 trillion and increased by $4.19 trillion to $8.34 trillion in August during the Pandemic response. Since February 2020 the Fed’s holdings of Treasury Notes and Bonds has jumped from $2.2 trillion to $4.5 in August representing 54.9% of the increase. The New York Federal Reserve has provided a breakdown by maturity of the Fed’s Treasury holdings. The Fed now owns about 53% of all the outstanding Treasury Notes and Bonds that have a maturity of 10 to 20 years, almost 30% of Treasury Notes with a maturity of 7 to 10 years, and 30% of Treasury Bonds with maturities of 20 and 30 years.

The 10-year Treasury yield is the benchmark most investment professionals reference when discussing the Treasury market. Based on these numbers an educated guess would estimate that the Federal Reserve owns around 40% of all outstanding 10-year Treasury  Bonds. With 40% of 10-year Treasury Bonds having been removed from trading by the Federal Reserve, it seems absurd that any investment professional would believe that the Treasury market is capable of providing a clear message for the economy or whether inflation will be transitory. The notion that financial markets possess an inner wisdom that only a select few can interpret is silly but embraced without question on Wall Street. Consider this: when the 10-year Treasury yield was above 15.0% in 1981 was it correctly telling everyone who was smart enough to listen that hyper inflation was coming? Nope. The 10-year Treasury yield declined for the next 40 years.

Bonds. With 40% of 10-year Treasury Bonds having been removed from trading by the Federal Reserve, it seems absurd that any investment professional would believe that the Treasury market is capable of providing a clear message for the economy or whether inflation will be transitory. The notion that financial markets possess an inner wisdom that only a select few can interpret is silly but embraced without question on Wall Street. Consider this: when the 10-year Treasury yield was above 15.0% in 1981 was it correctly telling everyone who was smart enough to listen that hyper inflation was coming? Nope. The 10-year Treasury yield declined for the next 40 years.

Delta Variant Weighs on the Economy

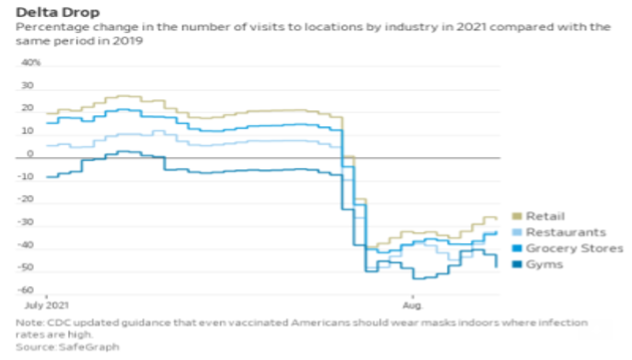

In the last two weeks of July and through August the Delta variant has caused a retrenchment in those sectors that were most impacted by shutdowns – airline travel, hotels, restaurants, gyms, and leisure and hospitality. The nearby chart compares current data with 2019 to avoid the distortions if compared to 2020. In the first three weeks of July the comparisons with 2019 were strong and then dropped sharply as Delta cases soared. Data collected for the July employment report was taken on July 12 and the August report will be based on data on August 12. The growth in jobs during could be tempered by the impact from Delta when the August Employment report is released on September 3. It is likely that the majority of data points for August will come in below estimates as economic reports are announced in September due to the Delta variant.

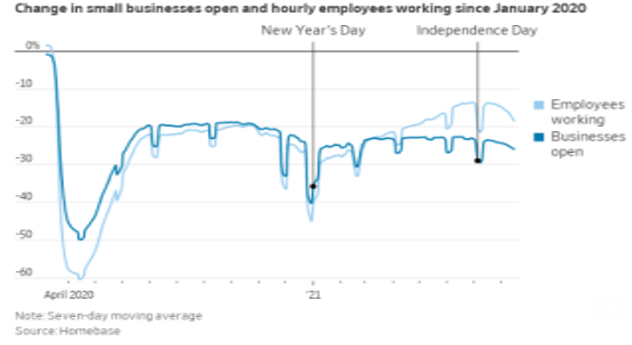

The Delta variant is delaying when more employees will be returning to the office in most urban downtowns. This  delay is going to hurt many small businesses that have been hanging on waiting for a big influx of workers in September. Many small businesses were highly dependent on office workers which were the staple of their businesses before the Pandemic closed downtown areas. According to Kastle Systems an average of 35% of the workforce had returned to traditional office space in July in the 10 major cities monitored by Kastle Systems. That was up from 23% in the middle of January but may dip as firms wait for Delta to recede.

delay is going to hurt many small businesses that have been hanging on waiting for a big influx of workers in September. Many small businesses were highly dependent on office workers which were the staple of their businesses before the Pandemic closed downtown areas. According to Kastle Systems an average of 35% of the workforce had returned to traditional office space in July in the 10 major cities monitored by Kastle Systems. That was up from 23% in the middle of January but may dip as firms wait for Delta to recede.

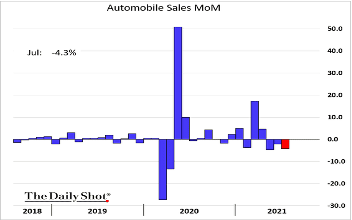

In August there were economic reports that appeared weak based on the headline but the details were solid. Retail Sales fell -1.1% in July according to the headline. Upon further review a decline in auto sales accounted for 0.7% of the decline (63.6%). The drop wasn’t due to a falloff in demand but scarce dealer inventories. Retail sales are 17.2% above their pre-pandemic level, which is a sign of strength. A modest slowdown in retail sales is likely in coming months but unlikely to signal real weakness for the economy.

Durable Goods orders fell -0.1% in July, after being up a strong 0.8% in June. The decline was attributable to a -48.9% plunge in orders for aircraft and parts as orders for commercial airlines were down. Excluding this category which is extremely volatile on a  monthly basis, Durable Goods would have been up + 0.7%. Unfilled orders for durable goods excluding transportation reached an all time high in July, which is hardly a sign of weakness. The decline in Retail Sales and Durable Goods orders weren’t a sign that the economy was slowing much faster than expected. Instead, the details under the headline suggest an economy that is slowing from a level of GDP growth that was the highest since 1983 but remains fundamentally healthy.

monthly basis, Durable Goods would have been up + 0.7%. Unfilled orders for durable goods excluding transportation reached an all time high in July, which is hardly a sign of weakness. The decline in Retail Sales and Durable Goods orders weren’t a sign that the economy was slowing much faster than expected. Instead, the details under the headline suggest an economy that is slowing from a level of GDP growth that was the highest since 1983 but remains fundamentally healthy.

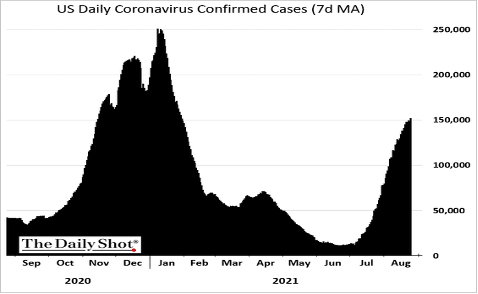

The Delta surge has hit southern states with low vaccination rates exceptionally hard but this is some good news. The number of Delta cases and hospitalizations are up significantly from the lows in June, but are still more than 30% below the January peaks. More importantly, the 7 day average of deaths rose to 1260 on August 31, but that’s 65.4% below the January 13 high of 3,643, according to CDC data. The problem with Delta is it is overwhelming the medical resources in a number of hard hit states and non-stop media magnification.

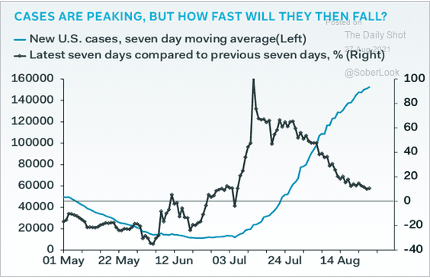

There is an early indication that Delta may be nearing a peak. The Rate of Change on the 7 day average of new cases has been coming down for 3 weeks but is still above 0%.  The law of small and big numbers is playing a role. The 7 day average in June was low so any increase would register a large percentage increase and the rate of change peaked at almost 100% in mid July. With the case count so high now, it is more difficult for the rate of change not to fall which it has. A stronger signal will be provided when the rate of change drops below 0% as that would indicate an absolute peak in cases. As of August 31 the Rate of Change on the 7 day average of new cases was +6.7%. The burden on overworked health care workers won’t fall for at least a couple of weeks after cases begin to fall. The track of Delta will have an influence on the taper discussion at the FOMC’s September 22 meeting.

The law of small and big numbers is playing a role. The 7 day average in June was low so any increase would register a large percentage increase and the rate of change peaked at almost 100% in mid July. With the case count so high now, it is more difficult for the rate of change not to fall which it has. A stronger signal will be provided when the rate of change drops below 0% as that would indicate an absolute peak in cases. As of August 31 the Rate of Change on the 7 day average of new cases was +6.7%. The burden on overworked health care workers won’t fall for at least a couple of weeks after cases begin to fall. The track of Delta will have an influence on the taper discussion at the FOMC’s September 22 meeting.

Redefining the Meaning of Transitory

Chair Powell has assured financial markets that any uptick in inflation would be temporary

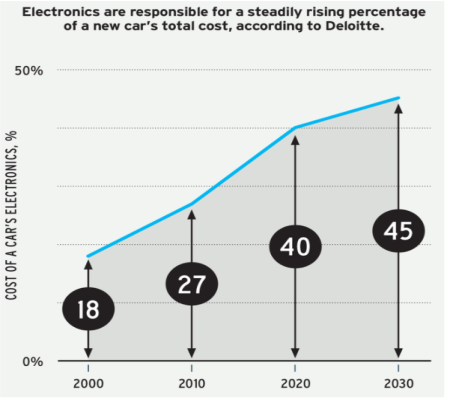

since March and adopted the term transitory after the April 28 meeting. Chair Powell emphasized that inflation from supply chain bottlenecks and the shortage of computer chips for vehicles would improve materially by late summer, hence the application of the word transitory.It’s almost six months since Chair Powell began using the word transitory as a calming mantra, but supply chain bottlenecks are worse and the computer chip shortage is still a big problem. Taiwan Semiconductor, the largest computer chip manufacturer in the world, announced it will increase the price of low end chips by 10% and the high level chips needed in vehicles by 20% sometime in the fourth quarter. Electronics are responsible for 40% of a new car's total cost, according to an analysis by Deloitte. The increase in the cost of chips will increase vehicle costs and likely lead to higher prices.

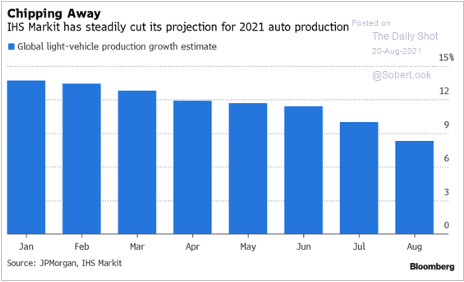

The lack of computer chips is a problem for vehicle manufacturers globally. Toyota recently said it would slash global production in September from 900,000 units to 500,000. IHS Markit estimates that up to 2.1 million fewer cars and trucks will be built in the third quarter, and 7.1 million less in 2021. With such large scale  production cuts the prices for new cars are not coming down anytime soon and may continue to rise in coming months. Although Used Car prices are going to fall, they may not fall as much as they would if new car production increased. The lead time for computer chips is not getting better as the delivery time is now 20.2 weeks, up from 12 weeks at the end of 2020. This is the most stretched delivery times have been in 2021 so real improvement in auto production is still at least four months away.

production cuts the prices for new cars are not coming down anytime soon and may continue to rise in coming months. Although Used Car prices are going to fall, they may not fall as much as they would if new car production increased. The lead time for computer chips is not getting better as the delivery time is now 20.2 weeks, up from 12 weeks at the end of 2020. This is the most stretched delivery times have been in 2021 so real improvement in auto production is still at least four months away.

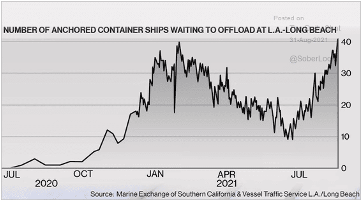

Shipping is an integral part of the supply chain in terms materials being delivered on time so production can proceed and cost of production. In March Chair Powell expected the extreme disruptions and delays that were widespread in February to dissipate within a few months. The delays at ports around the world and in the U.S. at the Port of Los Angeles and Long Beach did improve for awhile. The number of ships anchored at the Port of Los Angeles and Long Beach peaked in February at 37 and fell to less than 10 in June. Part of this improvement was due to the closure of a large port in China which reduced the number of ships coming to the U.S. Since late June the number of ships waiting to unload has shot up and hit a new record high in late August. Not much improvement is likely since the shipping industry is facing the seasonal surge in traffic due to the holidays.

As delays improved during the spring, the cost of shipping barely dipped and has since rocketed to new highs. The increase in shipping costs is staggering. In June 2020 the cost of moving a 40 foot container from Shanghai to Los Angeles was less than $2,000 and in mid August was up to $11,400. According to DHL Global Forwarding Asia Pacific, “The combination of a year of disruption, lack of containers, port congestions and a shortage of vessels in the right positions is creating a situation where cargo demand far exceeds available capacity. We do not expect freight rates to stabilize in the near term." If DHL’s assessment is correct, shipping costs in the 2021 holiday season will be up 400% to 500% from 2020 levels. Most firms can’t absorb an increase of that magnitude and will raise prices.

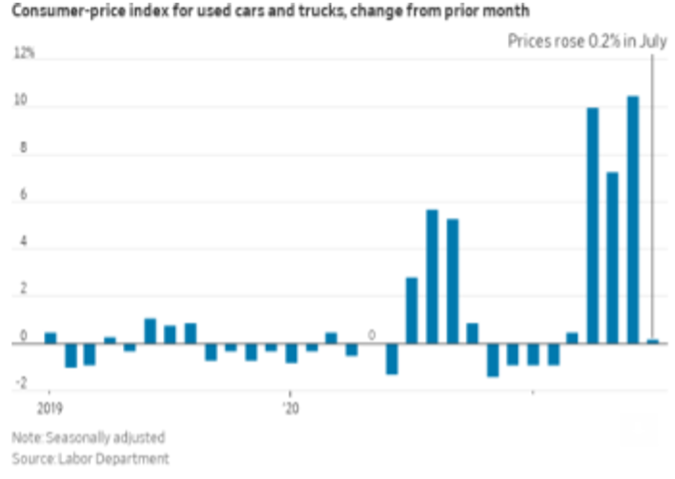

In his Jackson Hole speech Chair Powell noted that the prices of some goods and services that were most affected by the Pandemic are starting to fall. “Used car prices, for example, appear to have stabilized; indeed, some price indicators are beginning to fall. If that continues, as many analysts predict, then used car prices will soon be pulling measured inflation down.” In July Used Car prices rose just +0.2% after soaring +10.5% in June, as discussed in the July 19 Weekly Technical Review. “New cars are about 5.1% above where they were two years ago, but Used car prices are up 41.3%. In June new car prices were up 2.0% from May while used car prices soared 10.5%. These increases are unsustainable and there are signs that the surge in used car prices has topped. In June the Mannheim Used Car Vehicle Value Index fell -1.3% to 200.4 and the first decline since December. The Mannheim Index is still up 42% from two years ago, but is likely to moderate more in coming months. Used car prices represent 3.1% of the CPI and New cars are  3.7%. If the Mannheim Index falls to where it was in January 2021 (165) in the next few months, it will shave -0.55% off the CPI.” In mid August Used Car prices fell more and are now down -4.6% from the peak in June, which will lower headline inflation for August.

3.7%. If the Mannheim Index falls to where it was in January 2021 (165) in the next few months, it will shave -0.55% off the CPI.” In mid August Used Car prices fell more and are now down -4.6% from the peak in June, which will lower headline inflation for August.

Although the Mannheim Used Car Vehicle Value Index will fall to 165, it won’t happen in the next few months. The demand for used cars jumped as those who moved out of urban centers to the suburbs realized they were going to need a car. The new suburbanites were often shocked to find that the supply and selection of new cars was sparse.  This led them to look at used cars which often cost less than a nonexistent new car. The price for some used vehicles (trucks) that were in high demand became more expensive than a new truck. The big increase in used car prices was the result of an influx of urban dwellers moving into the suburbs and the lack of new cars. The migration to suburbs has mostly ebbed but the supply of new cars has fallen. The national inventory of New Cars is less than 200,000 which is 80% below the pre-Pandemic of 1.2 million vehicles. The lack of inventory lifted New Car prices 1.7% in July from June. With so little new car supply available the demand for Used Cars will not fade, so the decline in Used Car prices will be gradual.

This led them to look at used cars which often cost less than a nonexistent new car. The price for some used vehicles (trucks) that were in high demand became more expensive than a new truck. The big increase in used car prices was the result of an influx of urban dwellers moving into the suburbs and the lack of new cars. The migration to suburbs has mostly ebbed but the supply of new cars has fallen. The national inventory of New Cars is less than 200,000 which is 80% below the pre-Pandemic of 1.2 million vehicles. The lack of inventory lifted New Car prices 1.7% in July from June. With so little new car supply available the demand for Used Cars will not fade, so the decline in Used Car prices will be gradual.

Chair Powell sidestepped the coming increase in shelter inflation (Owner’s Equivalent Rent OER) and Rent that comprise a large portion of core inflation measures. Rent and OER represent 39.5% of the Core CPI and 17% of the Core PCE. The Core CPI garners far more attention than the Core PCE which means it will have a greater impact on consumer’s expectations of inflation. The FOMC pays a lot of attention to inflation expectations and is why the Fed has labored hard to get inflation expectations higher. The FOMC sees this as a key to getting inflation up to near its 2.0% inflation target. The coming rise in shelter inflation may allow the Fed to succeed too well.

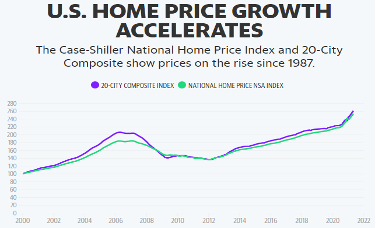

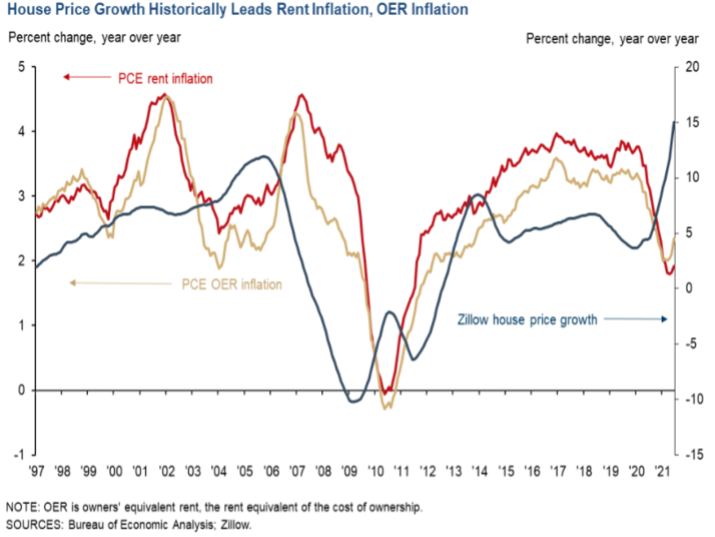

The Federal Reserve of Dallas has done extensive analysis on the correlation between home prices, rents, and OER. Increases in the 12 month annual increase in home prices, leads OER by 16 months and Rent by 18 months. These have a high correlation coefficient of 0.75 for OER and 0.74 for Rents. The Case-Shiller Home Price Index for June was up 16.8% from June 2020 and the largest annual increase since 1987 when data was first collected. The National Association of Realtors reported that the median home price rose 17.8% in July, reinforcing how broad the price increase has been.

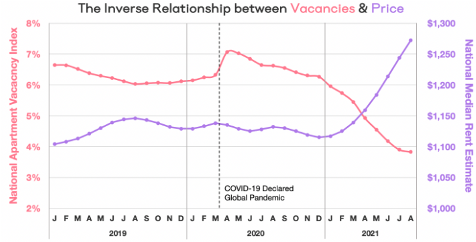

According to the Apartment List National Rent Report, the national median rent is up 7.6% from August of 2020 but is up 13.8% since January 2021. The Month-Over-Month increase in August slowed to 2.1% from 2.5% M-O-M in July, but still rising at an annual rate of more than 24% in August. The vacancy rate is down to 3.9% from 6.7% in January 2019 which will keep pushing rents higher. The annual increase will continue to rise from the 7.6% in August and likely exceed 10.0% by December. By comparison, the average annual increase in median rents was 3.6% from 2017 through 2019.

Home price increases lead changes in Rent by 18 months and OER by 16 months. The correlation between these data sets indicate that the contributions to the Core CPI and Core PCE from shelter inflation will continue for at least 18 months, since there are no signs that home prices or apartment rents have stopped going up.

Shelter inflation  is expected to add 1.4% in 2022 and 2.7% in 2023 to the Core CPI Index, based on the weights of OER and Rents, and the expected increases in OER and Rent in 2022 and 2023. Shelter is projected to add 0.6% to the Core PCE Index in 2022 and 1.2% in 2023. The increase in shelter inflation could keep the Core CPI above 3.0% well into 2022, which will make claims of inflation being transitory sound increasingly shrill. There is a good probability that the Core PCE will hold comfortably above 2.5% through the first quarter of 2022, which is too far above 2.0% to allow some members on the FOMC to remain comfortable with the outlook for inflation.

is expected to add 1.4% in 2022 and 2.7% in 2023 to the Core CPI Index, based on the weights of OER and Rents, and the expected increases in OER and Rent in 2022 and 2023. Shelter is projected to add 0.6% to the Core PCE Index in 2022 and 1.2% in 2023. The increase in shelter inflation could keep the Core CPI above 3.0% well into 2022, which will make claims of inflation being transitory sound increasingly shrill. There is a good probability that the Core PCE will hold comfortably above 2.5% through the first quarter of 2022, which is too far above 2.0% to allow some members on the FOMC to remain comfortable with the outlook for inflation.

Chair Powell did discuss wages and their importance.  “We also assess whether wage increases are consistent with 2 percent inflation over time. If wage increases were to move materially and persistently above the levels of productivity gains and inflation, businesses would likely pass those increases on to customers, a process that could become the sort of "wage–price spiral" seen at times in the past. Today we see little evidence of wage increases that might threaten excessive inflation. Broad-based measures of wages that adjust for compositional changes in the labor force, such the Atlanta Wage Growth Tracker, show wages moving up at a pace that appears consistent with our longer-term inflation objective. We will continue to monitor this carefully.”

“We also assess whether wage increases are consistent with 2 percent inflation over time. If wage increases were to move materially and persistently above the levels of productivity gains and inflation, businesses would likely pass those increases on to customers, a process that could become the sort of "wage–price spiral" seen at times in the past. Today we see little evidence of wage increases that might threaten excessive inflation. Broad-based measures of wages that adjust for compositional changes in the labor force, such the Atlanta Wage Growth Tracker, show wages moving up at a pace that appears consistent with our longer-term inflation objective. We will continue to monitor this carefully.”

One risk to Powell’s sanguine outlook is a potential labor shortage that may not be resolved after Unemployment benefits are ended on September 6 for the 70% of those still  unemployed, and Moms reentering the labor force once schools are fully open. Total Employment is still 5.7million jobs lower than in February 2020, even after 943,000 jobs were added in July. The overall Labor Participation Rate was 61.7% in July, but 1.6% lower than in February 2020. The Labor Participation Rate has not recovered much for those 55 and older as up to 3 million older workers may have retired during the Pandemic. This is likely to keep the overall Participation Rate from recovering fully and could contribute to a lasting labor shortage.

unemployed, and Moms reentering the labor force once schools are fully open. Total Employment is still 5.7million jobs lower than in February 2020, even after 943,000 jobs were added in July. The overall Labor Participation Rate was 61.7% in July, but 1.6% lower than in February 2020. The Labor Participation Rate has not recovered much for those 55 and older as up to 3 million older workers may have retired during the Pandemic. This is likely to keep the overall Participation Rate from recovering fully and could contribute to a lasting labor shortage.

The National Federation of Independent Business said 49% of the owners it polled had an open position in July but couldn't find a worker to staff it. July’s level was about 50% higher than the previous high in 2001. In response to the difficulty of landing workers, a record number of small businesses have offered a signing bonus and increased compensation to the highest level in 48 years to attract employees, with a record number planning to increase wages even more.

According to the Labor Department unfilled job openings rose to 10.1 million in June, the highest level since record keeping began in 2000. This compares to the 9.5 million people who were looking for a job in June. Since 2000 the only time there were more unfilled jobs compared to those looking for a job was from mid 2018 until the Pandemic hit in February 2020. Average Hourly Earnings grew at an annual rate of less than 3.0% from 2010 into early 2018. In March 2018, AHE were up by 2.8% from March 2017, but quickly jumped to 3.45% in June 2019 when there more unfilled jobs than job lookers. In July 2021 AHE were up 4.0% compared to July 2020. For obvious reasons the data since April 2020 has been noisy but should be less volatile in coming months. As long as there are more unfilled jobs than people looking for a job, there will be upward pressure on wage inflation. In July AHE were up 4.0% Y-O-Y.

Shelter inflation will add to measures of Core inflation for the next 18 months. The labor shortage will become less severe after unemployment benefits end on September 6 and schools reopen. However, it is likely that there will continue to be a persistent labor shortage that will contribute to higher AHE and a more pronounced impact for the labor intensive sectors. Companies will offset a portion of their higher labor costs by raising prices. Headline and core inflation are going to fall from multi-decade highs, but not enough to fulfill the definition of transitory.

Perfect Storm for Treasury Bonds

Once Congress increases the debt ceiling the surge in borrowing by the Treasury has the potential to overrun the Treasury market. By the end of the first quarter next year the Treasury will bring almost $2 trillion of issuance that the market must absorb without a hiccup. That includes $673 billion the Treasury didn’t auction in the second quarter, $703 billion it plans to bring to the market in Q4, and another $675 billion in Q1 of 2022. The Treasury will need to auction another $350 billion to build its balance up to the $400 billion comfort level at the Federal Reserve. The Treasury has indicated that it wants its balance at the Fed to be $750 billion at the end of Q3 and $800 billion at year end. (See Column 6 ‘End of Quarter Cash Balance’ in Reconciliation Table on page 5.) This suggests the Treasury will need to sell another $300 billion to reach their higher target balance relative to previous years. In total a tsunami of $2.6 trillion may have to be auctioned in the next 6 months. At the peak of the Pandemic the Treasury was able to issue more than $2 trillion in debt as fear was rampant. In coming months GDP growth will be solid and inflation is going to be higher than projected, so the environment will be dramatically different than in the spring and summer of 2020. And somewhere during this the FOMC will begin tapering it QE purchases by $30 billion to $45 billion a quarter.

Congress may soon pass $1 trillion for infrastructure and another $3.5 trillion in spending to address poverty and climate change before the end of September, according to House Speaker Nancy Pelosi’s timetable. Both bills will be lumped together and passed by reconciliation that allows Democrats to spend $4.5 trillion without any Republican support in the Senate. The Democrats have said tax increases will cover most of the increase in spending, although the Congressional Budget Office (CBO) reported that the infrastructure bill will not be fully paid for and will increase outstanding federal debt by $250 billion. The CBO hasn’t scored the $3.5 trillion bill since the details aren’t known.

Before year end the Treasury market will have to deal with enormous supply, sticky inflation, less Federal Reserve buying, and spending increases well over the horizon. Sure sounds like a perfect storm is forming that could cause a sharp increase in Treasury yields that few are even aware of. Everyone is focused on when and how much the Fed will taper, but the bigger problem is the wave of supply that could capsize the Treasury market.

The 10-year Treasury yield is expected to exceed its March peak of 1.76% and the 30-year should top its March high of 2.505%. One way to take advantage of an increase in Treasury yields is to purchase the 1 to1 inverse Treasury bond ETF TBF.

In the short term Treasury yields may not increase much as the Treasury can’t issue new debt and the Federal Reserve continues to buy $80 billion a month of Treasury debt.

Stocks

If Treasury yields rise rapidly in the fourth quarter, the stock market will fall. Higher Treasury yields will compress the high valuation Mega Cap stocks that carry a 22.8% weighting in the S&P 500. A sharp increase in yields would be expected to hurt cyclical stocks as prospects for GDP would be adjusted lower. A close in the 30-year Treasury yield above 2.15% will provide a key warning. A correction of 10% or more could follow.

Dollar

As the FOMC moves closer to tapering and Treasury yields rise, the Dollar is expected to rally. A stronger Dollar and higher interest rates would be expected to weaken Gold, Silver, and Gold stocks.

Gold

Unless Gold is able to close above $1840 and stay above $1840, Gold has the potential to fall under $1550 in the fourth quarter.

Gold Emerging Market ETF EEM

Emerging Markets

A stronger Dollar would pressure Emerging Markets by increasing debt service costs on $13 trillion in Dollar denominated EM debt. The trend is down until EEM is able to close above the green down trend line.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All