Inflation: More Transitory than Expected

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMeasurement Problems

Stranded Ships

Walking the Tightrope

New Opportunities in Technology and Transformation

New York, Dallas, and Booster Shots

If the inflation numbers leave you scratching your head, join the club. The August data was especially perplexing. The Producer Price Index came in hot, up 8.3% in the last year, inviting 1970s comparisons. Obviously, our current situation is different in many ways. But so were the 1970s, at first.

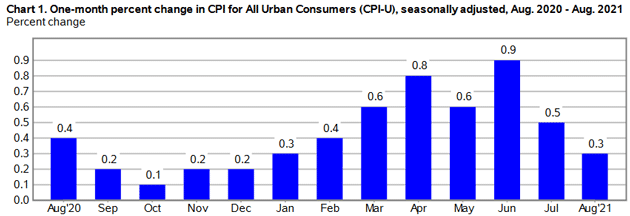

That was last Friday. On Tuesday the August Consumer Price Index data surprised in the opposite way, coming in lower than expected—but by no means “low.” Headline inflation rose 5.3% in the last 12 months.

Source: BLS

The pace may be slowing, though. The monthly CPI changes show an uptrend from January-June of this year, followed by two successively weaker months. But even 0.3% is higher than pre-COVID monthly inflation. If that pace continues, a year from now we will have experienced about 3.7% annual CPI growth.

That should be enough to meet the Fed’s inflation target and let it normalize policy. Whether it will do so or not, no one knows—not even the FOMC members. Today we’ll take another walk through the inflation debate. Is it still transitory or should we expect a light-1970s inflation going forward? The answer is critically important.

First a little history. Last May, Stephen Roach wrote a very important essay on inflation in the 1970s. He noted that Federal Reserve Chairman Arthur Burns (Roach had just started his career at the Fed during that time) would claim that every inflationary impulse was simply transitory. By the mid-70s Burns was calling 65% of the CPI “transitory.” Then he gave us this paragraph:

But the biggest parallel may be another policy blunder. The Fed poured fuel on the Great Inflation by allowing real interest rates to plunge into negative territory in the 1970s. Today, the federal funds rate is currently more than 2.5 percentage points below the inflation rate. Now, add open-ended quantitative easing—some $120 billion per month injected into frothy financial markets—and the largest fiscal stimulus in post-World War II history. All of this is occurring precisely when a post-pandemic boom is absorbing slack.

When he wrote this, real interest rates were -2.5%. Today they are below -5%. The parallels are becoming even more eerie, as the Federal Reserve appears to be claiming all the inflation they see is transitory.

Thus for good reason, inflation has been the topic du jour this year for everyone who follows economics. Jerome Powell has maintained the pressure we see isn’t because Fed policy is too loose. But that’s kind of what you would expect him to say.

Here in the real world, “transitory” doesn’t mean “inconsequential.” The Fed’s 2% inflation target, if actually achieved over time, would compound into 22% higher prices over 10 years, with no guarantee wages would rise to match it. Not to mention the loss of purchasing power for those on fixed incomes.

This is why measurement problems are so consequential. Policymakers flying blind is a recipe for disaster. They may think inflation is a problem when it’s not. Or, more likely, they may think it’s not a problem when it really is.

It’s not just policymakers, though. We all feel inflation differently based on our spending patterns, lifestyle, location, and more. The benchmarks like CPI and PCE are generalizations. Your mileage may vary. In fact, your mileage will vary.

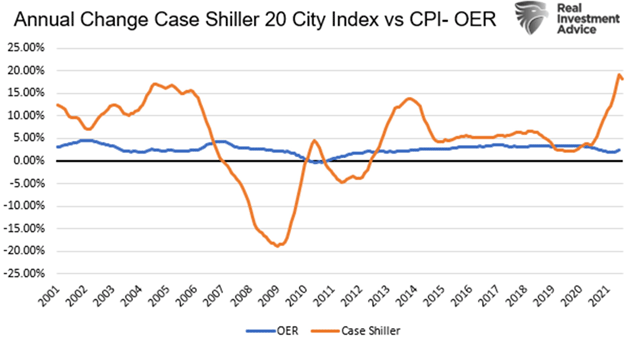

Six months ago, I described (see Inflation Is Broken) how the inflation benchmarks don’t properly reflect housing costs. They rely heavily on a concept called “Owner’s Equivalent Rent.” Homeowners are asked to estimate how much they would demand to rent their home to someone else, whether they intend to do so or not. Of course, the answers are all over the board, and bear little resemblance to what people actually pay.

In that March letter, I showed how OER disconnected from home prices around the year 2000, helping distort inflation since then. This new chart from Real Investment Advice demonstrates clearly that OER has no connection to home prices:

Source: RealInvestmentAdvice

Now we have a shorter-term distortion. Consider just the last two years. If you live in a home you purchased in 2019 or before, your monthly housing inflation has probably been running close to zero. Your payments may even have dropped if you refinanced at a lower rate.

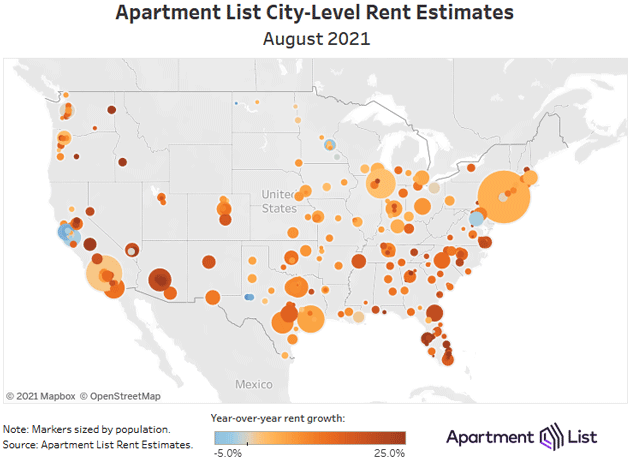

Not so for many renters. Apartment rents have been surging. Here’s a map from Apartment List showing 12-month changes as of August.

Source: Apartment List

All those reddish areas are places where average apartment rent is up 20% or more in the last year. The same is true for rental houses and condos. People who, for whatever reason, can’t buy a home are paying far more for housing in most areas. Yet the “Rent of Primary Residence” CPI component was up only 2.1% in this same period. Owner’s Equivalent Rent went up only 2.6%.

(There’s another element to this. In the pandemic, eviction bans and court slowdowns taught landlords they might be stuck with non-paying tenants for extended periods. Many responded, understandably, by raising rents to cover that risk. But the higher rents hit everyone, not just those who might have to be evicted.)

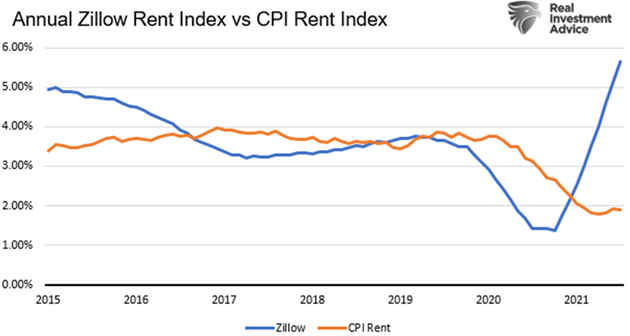

Another index from Zillow shows how completely disconnected actual rent is from CPI.

Source: RealInvestmentAdvice

On Friday Zillow released data showing that rents went up 1.7% just in August. My good friend David Bahnsen wrote last night:

Today Bloomberg ran a piece about rents in NYC going up as much as 70% from pandemic lows. It was not even a year ago that the predominant story was whether or not NYC real estate would ever recover. Now, there are almost complaints circulating over how much it has recovered.

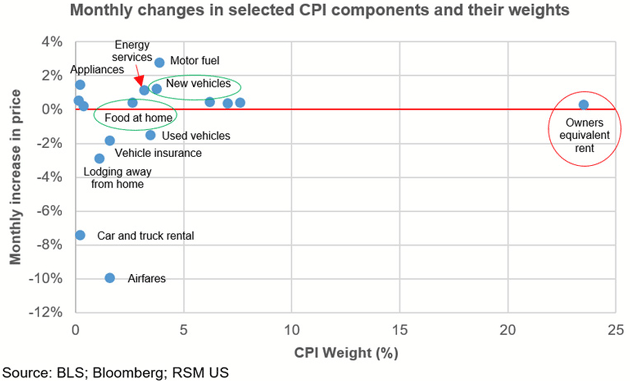

This matters to inflation because OER, which in no way reflects reality, has a huge CPI weighting. It’s a far outlier in this plot of August CPI change by weight.

Source: RSM

In most areas, both actual rents and an accurately measured OER would be much higher than CPI shows. Together, those are almost 30% of the index. CPI would be running much, much higher if it reflected true housing costs. A quick estimate says inflation would be at least 3% higher under the real-world measurements mentioned above. An 8% inflation number—which is entirely realistic—would certainly grab more attention. The Fed would have to deal with it sooner rather than later.

The generally rising prices that add up to broad inflation don’t come out of nowhere. Supply and demand factors cause them. As the COVID era drags on, adapting to the various changes it generated is increasingly difficult, and therefore increasingly expensive.

These changes aren’t crazy or complicated. Compared to 2019, Americans are eating more at home, buying more goods via e-commerce instead of in stores, fixing up their backyards instead of going on vacations, etc. Yet they add up to giant changes in the industrial supply chains in a relatively short time. This is causing problems.

For instance, the Financial Times reports shippers can’t find enough metal shipping containers to transport all the stuff we want to buy.

Chinese manufacturers are pumping out record volumes of freight containers after shippers ordered vast stacks of the steel boxes in an attempt to smooth out disruptions in the global supply chain…

The world’s biggest box manufacturers, China International Marine Containers (CIMC), Dongfang International Container and CXIC Group, are struggling to meet demand, even though production has been increased with workers’ hours extended.

“The factories are running pretty hard out,” said Brian Sondey, chief executive of Triton International, the world’s largest container leasing company, which rents boxes to shipping groups.

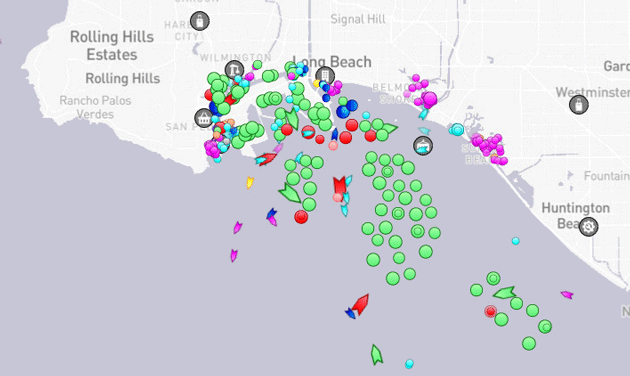

Even if the boxes can be found, they often arrive at US ports only to spend a week or more waiting for dock space to unload. Here’s a look at the Long Beach port last week. The green dots offshore are anchored container ships, each holding thousands of containers packed with stuff we need.

Source: Marine Traffic

As every investor knows, time has value. Extending the time it takes for goods to reach the buyer has a cost. Prices can rise while the new supply that might bring prices back down sits a few miles offshore. Multiply this millions of times over for many different products, and inflation is the result.

Nor is it just finished goods. Some of those ships have components US factories need to build other products. Lack of one key part can shut down an entire assembly line, idling its machinery and workers. That has costs, too.

The economy can adapt to all this, but not instantly. And it’s starting to look like the process will take longer than we thought a few months ago. That means inflation may be less “transitory” than we thought, too.

I’ve been on the “transitory” side of this year’s inflation debate. I still think we will avoid long-term sustained severe inflation, but I must admit it’s looking less transitory than expected, with inflation possibly running well above 2% for several years unless the Fed acts. The factors that are pushing home and other prices higher aren’t changing. Maybe they will, but they haven’t.

The other side of the argument, best articulated by Lacy Hunt, is that rising debt will cap inflation by holding back the velocity of money, thereby reducing GDP growth. This will reduce demand for housing and consumer goods, bringing prices back down. No more inflation.

Debt was already at crazy, unsustainable levels before the pandemic. I lack the words to describe what’s happened since then. Federal Reserve policy is both supporting government debt expansion and encouraging businesses and consumers to add leverage. Nor is it over. Congress is considering a pair of infrastructure bills that will add trillions more. Some of it will be productive debt, spent on public works projects we really do need (like better port facilities). But most will go to other, less productive programs. The part that isn’t debt-financed will be paid for with tax increases which, depending on exactly who and what is taxed, may also depress growth.

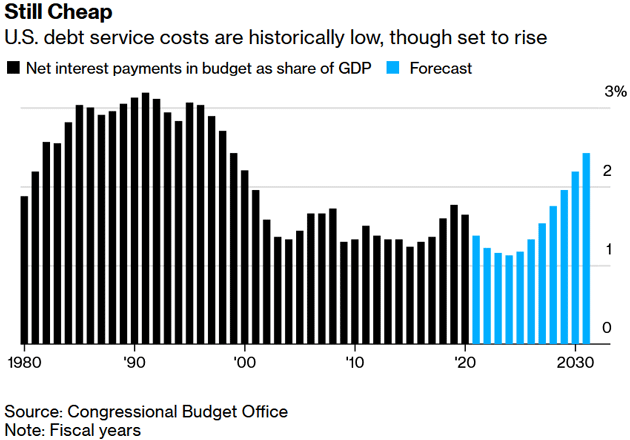

All this goes into the mix as the Federal Open Market Committee decides if and when to start tapering its asset purchases. The bond purchases and low rates are effectively subsidizing government debt. Servicing government debt is actually costing the economy much less than it used to as old higher-rate bonds roll off and are replaced with lower-rate ones.

Source: Bloomberg

Note the blue projection bars assume current law, and don’t yet account for what may soon be added. If inflation takes hold, the new debt will be issued at higher rates than CBO presently projects, driving interest costs higher.

On the other hand, inflation is historically the debtor’s friend. Borrowers can repay their debts in currency whose purchasing power is lower than it was when they received the loan. Is that thought somewhere in Jerome Powell’s head? A little inflation may be welcome if you are in charge of the world’s largest debtor, as Powell’s White House and Capitol Hill bosses are.

Powell and the FOMC may think they can walk this tightrope, keeping the free-spending politicians happy while also avoiding economic calamity for everyone else. I’m not sure they can. More moderate inflation numbers could actually be problematic if they encourage the Fed to further delay tapering. They may wait too long and find they have to step on the brakes hard and fast.

My friend Peter Boockvar ended his CPI analysis with a haunting note.

I remain strongly in the belief that sticky and persistent inflation will continue, that we have entered a stagflationary environment and we are not going back to a pre-Covid trend for a while to come. Wages are moving higher thankfully but unfortunately inflation is running faster for many.

However…

We don’t need to have inflation stay at the current elevated levels to remain an issue. All they have to do is moderate to a 3-4% trend as a world of negative and zero interest rates, negative real rates, drum-tight credit spreads, high equity valuations and an enormous amount of global debt is not positioned for that.

The real danger isn’t a return to something like the 1970s inflation. Given where the economy is now, we could have big problems long before it reaches that point.

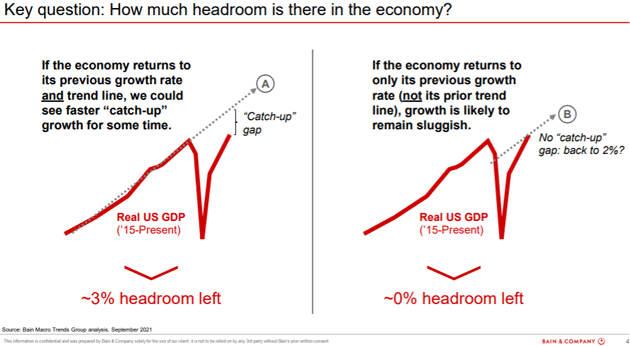

My friend Karen Harris and her team at Bain’s Macro Trends Group are worried about slower trend growth. In a recent presentation they noted the decelerating US recovery leaves the economy at a crossroads.

Source: Bain’s Macro Trends Group

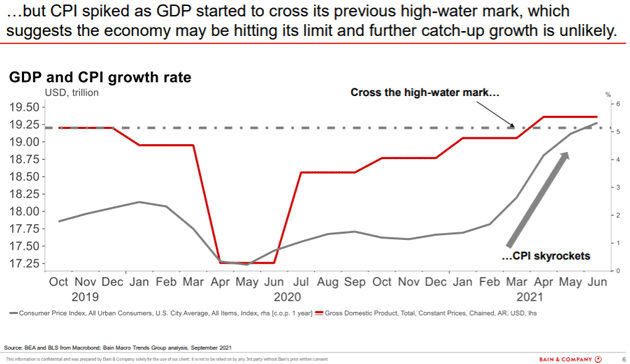

While they acknowledge that it is possible the economy catches up to previous trend line growth, given other factors it is more likely that we begin to moderate to 2% growth from where we will be in a few months. For me that would be the best-case scenario. Why? Their next graph shows the reason:

Source: Bain’s Macro Trends Group

GDP has already recovered back to 2019 in nominal terms. But inflation has skyrocketed and will become a drag. Workers will eventually come back, mostly to different jobs, and the supply/demand problems will settle out. That is how the economy works.

Bain asks a very good question: “Why does the US economy ‘all of a sudden’ need approximately 8 million fewer workers to achieve the same level of economic activity? Is it a structural gap in GDP and the number of workers needed?” This leads me to ask if we would see a GDP boom if 3 to 4 million workers come back We are in such uncharted territory that you can easily make a very bullish or very bearish case, looking at the same data.

That assumes the Fed begins to deal with the problems of inflation. If they do nothing or wait too long, we get back into a mini-70s-type problem as the Fed will be forced to remove QE faster and raise rates more quickly, likely triggering recession. That’s the last thing they want, but waiting too long will force the issue.

I believe this is why you are seeing more FOMC members talk about tapering sooner. It won’t surprise me if they start tapering as soon as Biden reappoints Powell. If he chooses Brainard or another monetary dove, we could easily find ourselves in the latter scenario. Shades of Chairman Arthur Burns, part two.

Remember my sandpile story. The fingers of instability are growing and eventually one grain of inflationary sand will hit the sandpile and trigger an avalanche. It doesn’t really matter which one does it. Barring another pandemic (the chance of which is hopefully decreasing), nearly all the problematic grains of sand come from the government and/or central banks. We don’t have to predict the exact disaster to know one is coming. And like the ‘70s, those fingers of instability lead to recessions and market volatility. This is a worldwide phenomenon, not just a US problem.

I said last week we are in danger of stagflation. That won’t be great if it happens. But if stagflation is all that happens, we should be grateful. Eventually this will all settle down but getting there could be very bumpy.

New Opportunities in Technology and Transformation

I have an ask. I would like to establish a strategic relationship with a small handful of larger professional investors; be you a hedge fund, mutual fund, pension fund, insurance fund, family office, or a large non-US funds manager. My objective is to share a select few transformational ideas that have, in my opinion, excellent potential investment profiles. I say a small number of professional investor relationships due to availability capacity in deal sizes and realistic time management.

More frequently than you might imagine, because of my connectivity, I am introduced to transformational technology companies that really do have the ability to creatively and positively disrupt our world. I see a number of opportunities; however, only a select few interest me. Often the companies are private so regulators require certain net worth thresholds before I can share them. And for a number of reasons, there are even fewer that I am able to invest in with my own and client capital.

This is not a solicitation for a specific offering. I want to start at the relationship level and move forward. If you are a large institutional investor you can contact me at [email protected]. Please give me your contact information and I’ll be in touch.

If you are interested in learning more, please know I will be working with you through my firm Mauldin Securities, LLC, where I am president and a registered representative, member FINRA and SIPC and Amera Securities, LLC, member FINRA and SIPC (where I am co-registered and a registered representative).

New York, Dallas, and Booster Shots

My next scheduled trip is to Dallas for Thanksgiving. We will get there a few days early to see some friends and then Thanksgiving with the family out at Lake Granbury (south of Fort Worth). I hope to get my booster shot in a few weeks and then plan more regular trips to New York and other cities for presentations and dinners.

I did a video podcast with Bill Walton in DC a few weeks ago and it is out. This is the second part, where we get a little more optimistic. It was a fun conversation.

I do appreciate it when you forward this letter and especially when you encourage your friends to subscribe. And don’t forget to follow me on Twitter. Now I will hit the send button and wish you a great week!

Your hopeful that we stumble through together analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All