Of all recent economic trends, sluggish employment growth is perhaps the most important for investors to watch, for three reasons.

First, because it’s holding back growth and fueling inflation pressures. Second, because it makes it harder to reduce income inequality. Third, because it undermines future employment growth by slowing the build-up of skills in the labor force and pushing companies toward automation.

What is happening to the US labor market, and why? Below I assess the five key issues:

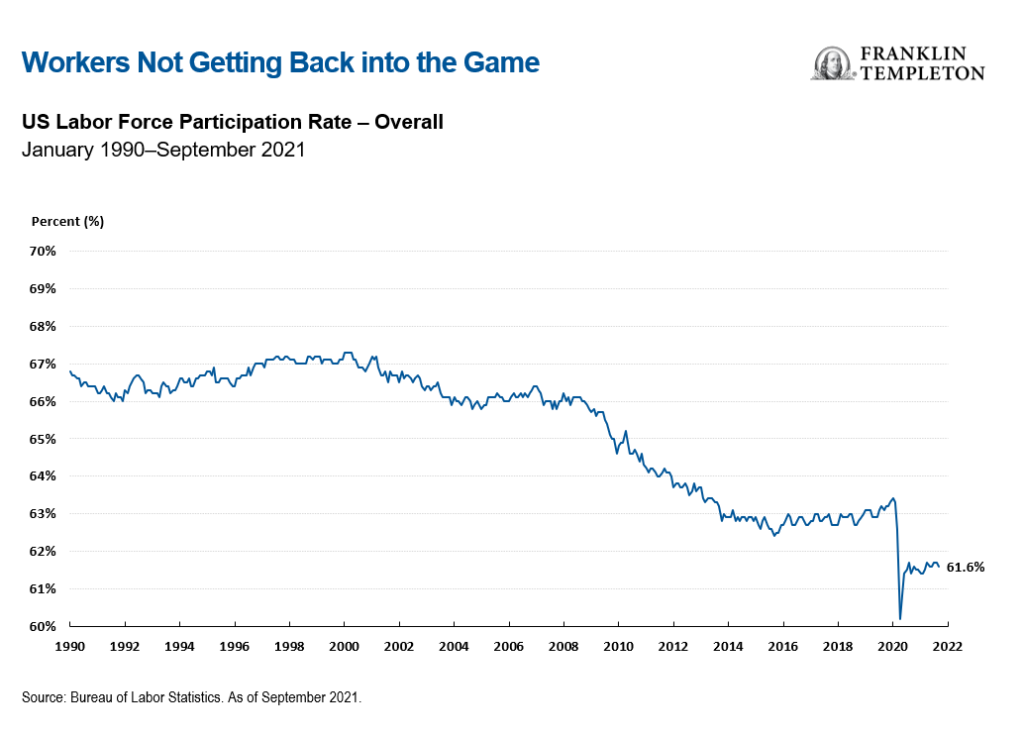

- Lower labor force participation

While labor demand has been recovering at a strong pace, many workers don’t seem to want to get back into the game. Labor force participation suffered a prolonged decline between 2000 and 2015, stagnated for a few years, and finally began a timid recovery in 2018-19, but the pandemic lockdowns knocked it down again and now it seems unable to get back up.

This is partly due to older workers who decided to retire earlier (the 65+ age labor force is running approximately 1 million workers below the 2007-2019 trend); but partly to younger workers sitting on the sidelines—the participation rate for people of prime working age (25 to 54 years old) is 1-½ percentage points below the pre-COVID peak.

- Rise in job switching

Much like in real estate, it’s a seller’s market. US job openings hover at around 11 million, and with lots of work opportunities on offer and limited competition, more workers are quitting their jobs: with the exception of the financial services and information industries, quit rates are well above their 2017-2019 average, and they correlate rather well with the abundance of job openings (also measured as excess over the 2017-2019 average). Quit rates are especially high in leisure and hospitality, but well above pre-pandemic levels also in manufacturing, retail trade and wholesale trade.

Quitting pays: wage gains for workers who switched jobs are much higher than for those who stayed in their current positions.

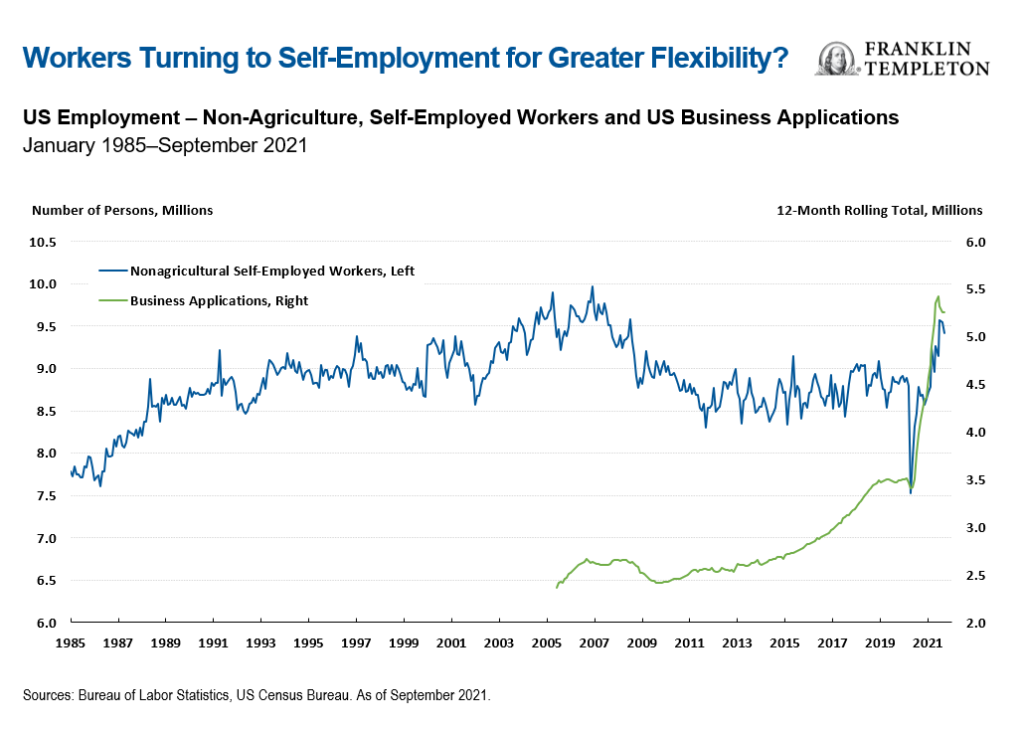

- Rise in self-employment

To make matters worse (for companies), self-employment has surged. The US Bureau of Labor Statistics reports a one million increase between November 2020 and September 2021. New business applications have risen sharply.

So even at a time when companies are granting more flexibility in working hours and location, many people prefer to strike out on their own. This upswing in entrepreneurial spirit reduces even further the pool of potential workers that companies can tap.

- What skills gap?

Some analysts and pundits have blamed the slow job recovery on a skills gap, arguing that the pandemic has changed the sectoral composition of the economy so that some skills that would get you a job two years ago are no longer in demand.

This makes little sense given that vacancies are especially high in leisure and hospitality, where most jobs do not require specialized skills. And companies are getting so desperate for workers that they would be happy to offer training to new workers.

- Higher government subsidies

Other factors holding back labor supply might be COVID-related: people worried about catching the virus at work, or reluctant to comply with vaccine mandates, or unable to secure childcare.

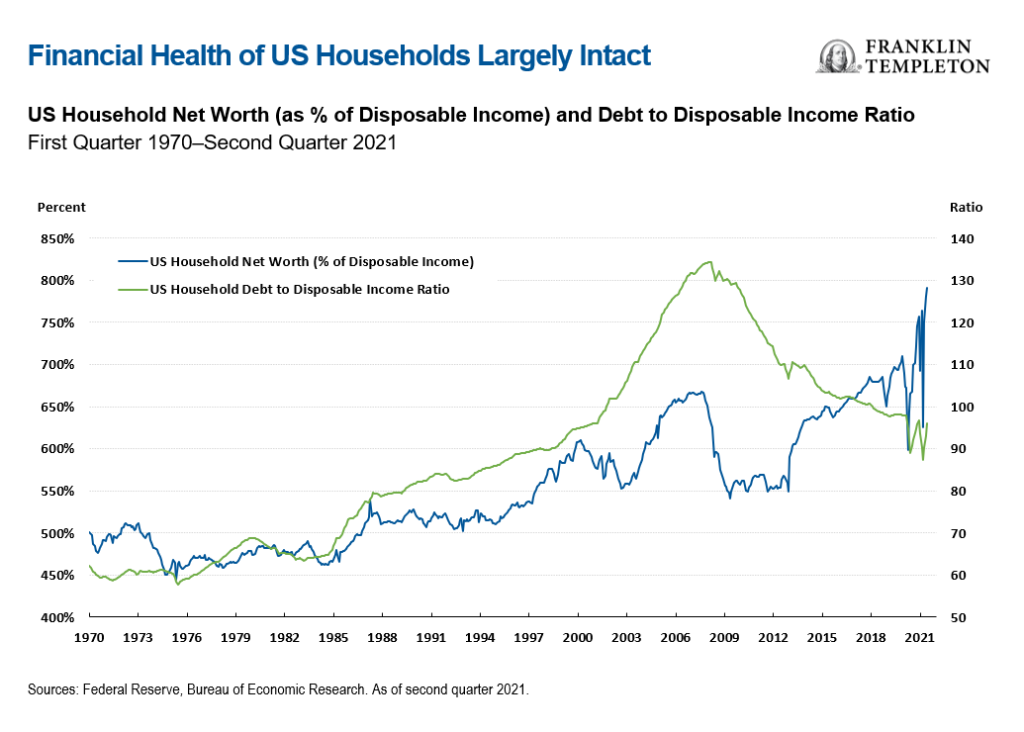

But probably more important is that households came out of the pandemic in a strong financial position, with high levels of financial assets and savings; and many households are still benefiting from generous government support.

Although the supplemental US federal unemployment benefits of US$300/week expired on September 5, state unemployment benefits will remain in place for anywhere between 16-26 weeks. These average US$319, or 26% of the average weekly wage. And 39 million American families are also eligible for the 2021 enhanced child tax credit, so households with two children, for instance, could receive an additional US$500-$600 (US$250 to US$300 per child) per month between July and December. That raises the wage coverage ratio to roughly 36%, and the government plans to augment it and extend it. Congress has also made available some US$46 billion in rental assistance to low-income households, and the Biden administration’s “Build Back Better” plan includes additional assistance in various forms, such as two years of free community college, expanded Medicare and Medicaid, twelve weeks of paid family leave, tax credits and government financing for affordable housing.

Higher inflation has triggered a sizeable 5.9% cost of living adjustment (COLA) for Social Security beginning January 2022 (the highest since the 7.4% increase in 1983), affecting nearly 50 million retirees and their dependents. Retirees’ pensions should be protected from inflation, but this also implies that rising prices will not induce older workers to get back into the labour force.

The Build Back Better plan meanwhile promises more subsidies to households, and some of these subsidies will also discourage work because they would be discontinued when a person takes a job.

In short, generous government support makes it easier—and rational—for more people to decide not to work. A number of people are staying out of the workforce because they can.

Investment implications

All these factors suggest that the labor market response will remain sluggish for quite a while. Over the past couple of decades labor had lost bargaining power, and its share of income has declined in favor of profits. This is now reversing, due also to the retreat of globalization and the government’s friendly attitude toward trade unions. This is not necessarily a bad thing, but in the short term, it is unambiguously inflationary. True, this is not like the 1970s, when wages were often indexed to past inflation; still, today employers have to raise wages to attract workers, and they have sufficient pricing power to pass higher costs down into higher prices.

US policymakers are quietly abandoning the “transitory inflation” argument, and the likelihood of rising prices and interest rates is higher than it’s been in the last several years. This reinforces the investment implications that our Franklin Templeton Fixed Income team has been pushing: limit duration exposure, and look for strong fundamentals to select opportunities in high yield corporate bonds, bank loans, municipal bonds and emerging markets.

For the medium term, the implications are more complex. If weaker labor supply dynamics become entrenched, they will tend to lower potential growth; technological innovation and automation will push in the opposite direction, boosting productivity. The net effect is as uncertain as it is important—with weaker economic growth, higher debt levels and rising social security obligations would jeopardize financial stability and could cause major bouts of volatility in asset prices. Stronger economic growth would have a stabilizing effect, but the combination of faster technological innovation, lower labor force participation and higher government subsidies could entrench and perhaps worsen income inequality.

An acceleration in labor supply would be the best guarantee of stronger and healthier economic growth.

For now though, investors had better prepare for sluggish labor supply, persistent inflation and rising financial volatility.

© Franklin Templeton

https://us.beyondbullsandbears.com/

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments