This article is relevant to financial professionals who are considering offering model portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

Cart Master: Bring out yer dead!

Customer: Here's one…

Dead Person: I'm not dead!

Cart Master: 'Ere. He says he's not dead!

Customer: Yes, he is.

Dead Person: I'm not!

Cart Master: He isn't?

Customer: Well, he will be soon. He's very ill.

Dead Person: I'm getting better!

Customer: No, you're not. You'll be stone dead in a moment.

(From the film, “Monty Python and the Holy Grail,” released 1975)

We try to avoid hyperbole in our market commentary, so you will not find any references here to the death of the 60/40 portfolio (60% equities and 40% bonds). It is a tried-and-true moderate risk portfolio that has performed well for millions of investors over the years.

That said, it is not inappropriate to challenge conventional wisdom, as both we and others have done (e.g., Goldman Sachs, Deutsche Bank, Bank of America)1. We also were one of the first asset management shops to build Model Portfolios explicitly challenging the wisdom of a traditional 60/40 approach, specifically the Siegel-WisdomTree Models, which we launched in November 2019.

Let’s remind ourselves of the investment mandates we were solving for when we built and launched these Models.

First, most investors have four common investment objectives with respect to their investment portfolios (though each person’s “weighting” to an objective may differ):

-

Maintain or improve their current lifestyle (i.e., optimize current income)

-

Not outlive their money (i.e., make sure the portfolio lasts at least as long as they do)

-

Ensure that family legacy or impact/philanthropic goals can be met

- Minimize fees and taxes along the way

These common objectives face two primary challenges as we consider the investment horizon.

-

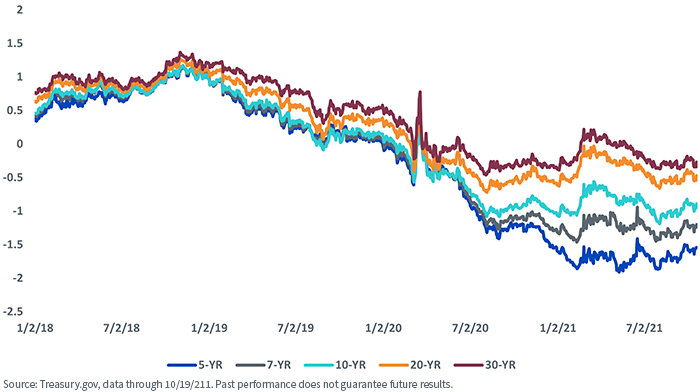

Low interest rates: Interest rates remain very low, and though we do see them grinding higher from current levels as the economy improves—perhaps hitting 1.75%–2.00% by year-end—we simply do not see many catalysts driving them significantly higher in the foreseeable future. Massive federal debts and deficits, an aging population and the corresponding demand for assets to hedge equity market risk are all working to keep rates low by historical standards.

Currently, Treasury real levels of interest rates (the nominal rate minus the inflation rate) remain negative across the entire yield curve. In addition, corporate credit spreads remain historically tight. Assuming a buy and hold strategy, the “starting yields” on a bond historically have a been a good predictor of the expected return on that bond.

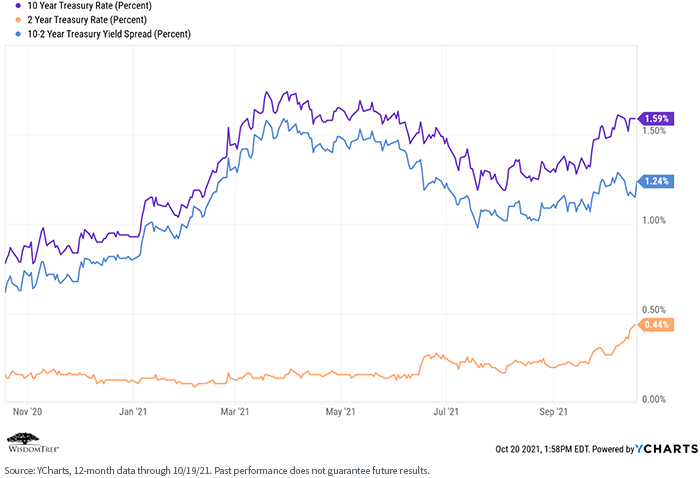

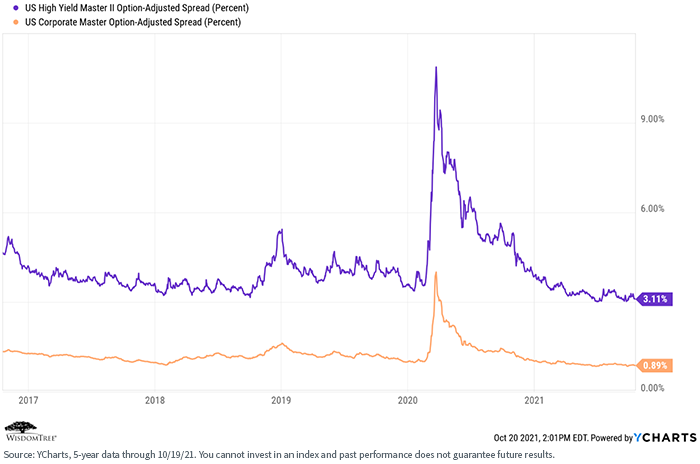

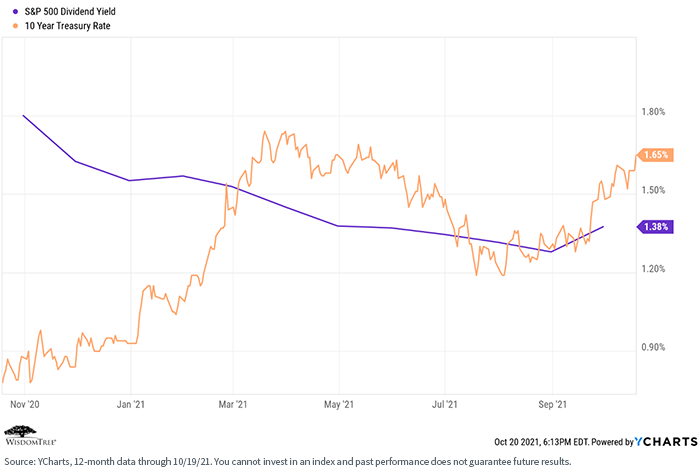

Today that yield (using the current 10-Year nominal Treasury rate of approximately 1.59% and an average corporate credit spread of approximately 0.89%) is roughly 2.48%.

The implication is that it will remain difficult to generate sufficient current income or future returns with fixed income portfolio to maintain or improve current lifestyles, without taking unwanted additional risk (i.e., increased duration or credit risk).

U.S. Treasury Real Yields (%)

For definitions of terms in the chart please visit the glossary.

-

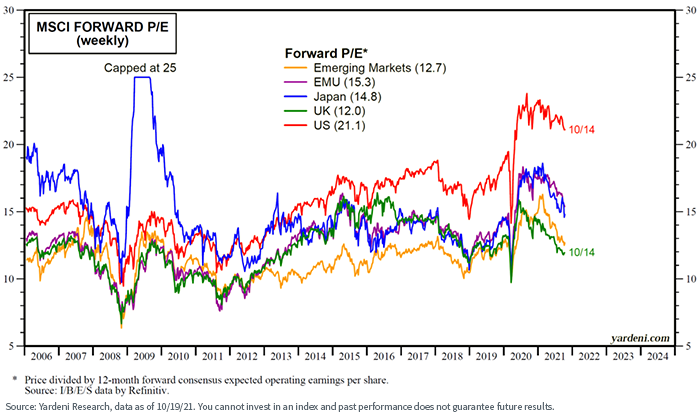

Lower forecasted equity returns: The potential return on any investment is at least partly a function of what you pay for it today. Given today’s equity market valuations, investors may potentially face a lower return regime going forward. Our own estimates are for roughly 4.5%–5.0% real return, versus an historical real return rate of 6.5%–6.7%.

The implication is that it may be more difficult to build portfolios that have a sufficient longevity profile to accommodate increased life expectancies without taking on additional equity risk.

So, the question becomes—can we build a better mousetrap than the traditional 60/40 portfolio, which can potentially address most investors’ mandates in the face of current and expected future market environments? Let’s start with dividends.

Given the run-up in equities and rise in rates, current dividend yields are once again lower than bond yields. We argue, however, that equity dividend yields are far more sustainable, with expected improvement as earnings and the economy recover. In addition, equities hold the potential for upside total return, while bonds do not (if held to maturity).

The Siegel-WisdomTree Model Portfolios

It was with these facts on the ground that, in collaboration with Dr. Jeremy Siegel of Wharton, a since-inception Strategic Advisor to WisdomTree, we launched, in November 2019, the Siegel-WisdomTree Model Portfolios—a Global Equity Model and the flagship Longevity Model.

The Longevity Model explicitly is our attempt to build a better mousetrap than the traditional 60/40 portfolio:

-

A 75% (as the policy weight) allocation to yield-focused equities to improve current income generation, the longevity profile and the legacy potential of the overall portfolio (Investor Objectives #1, 2 and 3). The yield-focused nature of the selected equity securities mean they tend to have a lower equity beta profile.

-

The fixed income allocation is constructed for quality income generation in a risk-controlled manner and to act as an appropriate equity risk hedge (Investor Objective #1).

-

Selectively implement alternatives such as commodities to help maintain purchasing power over time (Investor Objectives #1 and 2).

- The portfolio is constructed entirely with ETFs, to potentially optimize fees and taxes (Investor Objective #4).

We built the Global All-Equity Model on the same principles but in recognition that many advisors prefer to manage their own fixed income portfolios and/or want to create different risk profile portfolios than our suggested 75/25 Model (keeping in mind, however, that the further you deviate from 75/25, the further you drift from our underlying investment thesis).

The potential results of our asset allocation, portfolio construction and security selection decisions are:

-

Improved current income generation.

-

A better longevity profile (i.e., reduced short-fall risk).

-

Better potential for funding legacy objectives.

-

A low cost and tax efficient portfolio.

- An expected standard deviation slightly higher than a traditional 60/40 portfolio. That is, the investor and advisor are accepting slightly higher short-term volatility in exchange for increased current income and a better longevity profile.

We launched these Models in late 2019, so they now have almost two years of live performance under fairly extreme market conditions (in both directions) and, so far, they have performed as expected both from a total return and a yield perspective. The current allocation to “alternatives” reflects the fact that we took positions in gold and broad-basket commodities at different times after we launched to mitigate the perceived risks of inflation as the economy recovers.

Conclusion

As an early adopter of the notion of challenging the traditional 60/40 portfolio, we launched the Siegel-WisdomTree Model Portfolios in an attempt to address what we believe are some of the primary issues and conditions that investors will face in the foreseeable future.

Our view is, simply, that the traditional 60/40 portfolio will face significant headwinds in meeting investor objectives as we move through this decade and the next. We believe we have succeeded in constructing a “better mousetrap.”

Financial advisors can learn more about these Models, and how to successfully position them with end clients, at our newly launched Model Adoption Center.

1 See, for example.

© Wisdom Tree

https://www.wisdomtree.com

© WisdomTree, Inc.

More Global Markets Topics >

---siegel-wt-longevity-model.png?h=657&w=700&hash=0DA14C8A9017DD213C06FABBB3086780F0EDA3BE)