Is the FOMC Impotent?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMonetary Tools Can’t Fix Today’s Problems

In March 2020 the Federal Reserve was able to use old and new tools to manage the unimaginable – a Pandemic. The Fed stabilized the Treasury bond market and the municipal bond market through its purchases and back stopped government loans to small and medium sized businesses to keep them from going under. The Fed had the capacity to contain the financial and economic fallout in its role of being the lender of last resort. With Jay Powell as Chair, the FOMC did a masterful job in a time of national crisis.

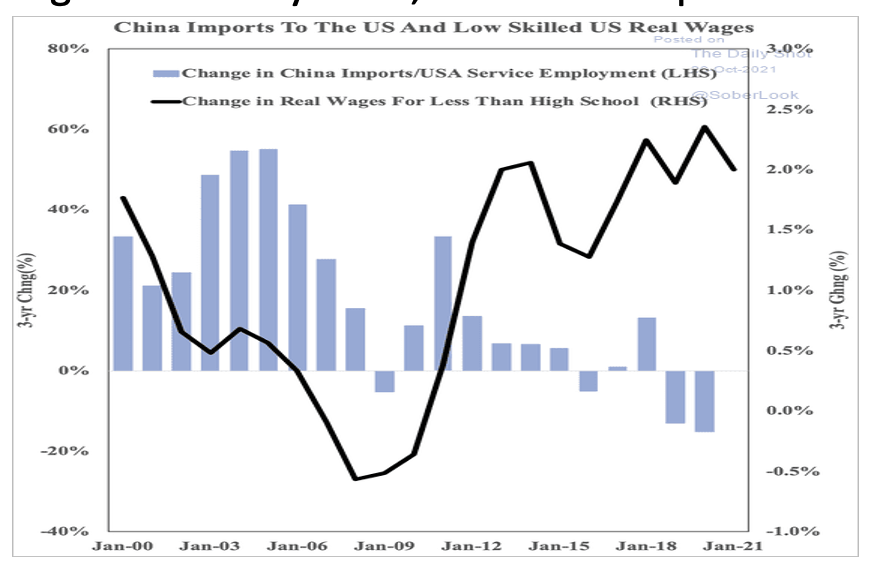

Since the Fed formally adopted its 2.0% inflation target in January 2021, the Fed has spent most of the past decade failing to reach it. There were many reasons why inflation remained so subdued. One of them was China’s entrance to the World Trade Organization in 2001 and especially in the years following the financial crisis. As more jobs were moved from the US to China, wage growth for low skilled jobs in the US stagnated, and the cost of goods imported from China declined. China not only imported toys, clothes, furniture, and washing machines but with those lower cost goods it also imported deflation. This dynamic was beyond the control of the Federal Reserve but it was a headwind for their inflation target.

In August 26, 2020 the FOMC announced that it was adopting ‘Average Inflation Targeting’. In guiding monetary policy the FOMC would no longer react if inflation exceeded 2.0% for a period of time. According to AIT, the FOMC wants inflation to average 2.0% over a complete business cycle, so brief periods of above 2.0% inflation would subsequently be offset by a decline below 2.0% during a recession. In announcing the change Chair Powell called it a ‘robust updating’ of policy and was clearly enthusiastic. “The Fed will not just emphasize actual inflation over forecasted inflation, but will also attempt to push the inflate rate above its 2% target. It’s a whole new ballgame.” As noted last year the FOMC couldn’t have picked a worse time to adopt its new framework since I expected the Pandemic to raise inflation comfortably above the 2.0% target.

The Pandemic created many factors that have contributed to the largest increase in inflation in more than a decade. The first domino was a surge in demand after Congress passed $5.3 trillion in COVID-19 relief in 2020 and in March 2021. Of that total $865 billion were direct payments to individuals and couples filing jointly, and $592 billion in unemployment benefits. Combined these payments totaled $1.457 trillion. These figures don’t include the hundreds of millions paid by states to unemployed workers and the rent and mortgage moratorium.

The majority of Americans who received income transfers were stuck at home and unable to spend money on normal activities. The Savings Rate soared to a record 33.8% in April 2020 and 26.6% in March 2021 after Covid-19 relief programs were passed in March 2020 and March 2021. In the three years leading up to the Pandemic the Savings Rate averaged 7.5% and in September 2021 it was back to 7.5%. Wage growth has accelerated for hourly workers, and especially for lower income workers. This is also making it easier for some workers to pad their savings, although higher inflation is lowering ‘real’ wage growth.

The higher Savings Rate during the last 19 months has enabled consumers to amass a large pool of excess savings. Excess savings is the difference between what would have been saved if there hadn’t been a Pandemic, and how much savings consumers currently have. The actual amount of excess savings is an estimate and I found a range from $1.5 trillion to $2.7 trillion and this estimate by J.P. Morgan of $2.357 trillion. A large portion of the pool of savings is held by middle class workers who earned less than $75,000 as a single filer or $150,000 as a couple and received funds. No matter how it’s sliced the amount of excess savings is significant and it will provide the wherewithal for most consumers to keep spending well into 2022 and beyond.

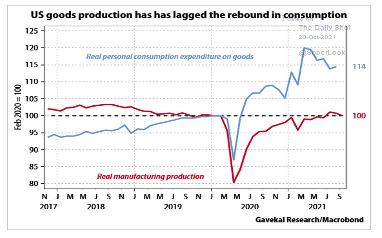

Since the onset of the Pandemic and the disbursement of funds by federal and state governments, consumers rushed to buy stuff. From technology to be able to work from home, moving out of an apartment into a suburban home, redecorating new or existing livings spaces with new furniture and appliances, exercise equipment, and larger TV’s to binge watch everything. Prior to the Pandemic manufacturing production easily exceeded goods consumption. This positive imbalance kept goods inflation low as sellers were more interested in maintaining market share. After years of mediocre demand the Pandemic surge caught many manufacturers flat footed, after many curbed production after the country was shut down. The mismatch between the demand for goods and the relative supply is the primary push behind soaring prices for goods. The gap between demand and supply is still huge and will be sustained as consumers keep spending and manufacturers play catch up.

After a tax cut in 2003 demand jumped but it took more than 3 years for inventories to match the level of orders. After the Financial Crisis it took almost 3 years for the back of orders to be cleared by more inventories. After President Trump lowered personal income taxes in December 2017 order backlogs popped, but the increase in inventories was halted by the Pandemic 14 months later. The gap between order backlogs and inventories is far larger than any other time since 1998. Even under the best of circumstances it has usually taken up to 3 years to close the gap. But these are far from the best of circumstances as many industries are hampered by a labor shortage, the inability to find skilled workers, and difficulty in getting the necessary parts to make products.

The federal government sent money to people earning more than the median income of $67,500 whether they were working or not. Federal and state unemployment benefits often exceeded a worker’s pre-Pandemic wage so unemployed workers were more than made whole. Government income transfers funded a meaningful portion of the big increase in demand since April 2020 that has effectively broken the global supply chain. The blue line shows the trend growth in Retail Sales from 2015 into 2020. The dramatic jump above this trend line highlights just how government income transfers goosed Retail Sales. Even though the year over year increases will show a rapid deterioration in coming months, the mountain of excess savings consumers are sitting on should keep Retail Sales elevated well into 2022.

Given the huge imbalance between demand and supply the last thing needed is anything that increases demand further. A number of FOMC members have said that spending legislation under consideration in Congress could add too much stimulus to the economy. As Tom Barkin the president of the Richmond Federal Reserve succinctly put it, “I don’t think we need more demand stimulus right now.” It may be bad policy now but Congress is likely to pass an additional $2.5 trillion to $3.0 trillion in additional spending before year end. Although the bulk of this potential increase will be spread out over the next 10 years, the infrastructure component will add to incremental demand for raw materials in 2022 and 2023. Industrial metals prices are higher than at any time in the last 20 years. As state and local governments get bids to fix bridges, roads, and install broadband internet, they will be paying a lot. Many commodities have been in short supply for 6 to 12 months. The additional demand generated by more government spending has the potential to keep many commodities in short supply and sustain record high prices. Higher input prices will allow companies to increase their selling prices since competitors are in the same boat. This is already occurring. Companies that don’t raise prices will see their profit margins narrow. Soaring input costs have been so severe that the choice is between two unfavorable outcomes – higher inflation or lower profit margins.

In recent weeks Chair Powell has acknowledged that supply chain disruptions are getting worse and not better and the increase in energy costs is adding a new dimension. “Supply-side constraints have actually gotten worse in some cases…and now we’re getting upward pressure on energy. The risks are clearly now to longer and more-persistent bottlenecks, and thus to higher inflation.” The majority of economists (32%) don’t expect a meaningful improvement in the supply chain until the second quarter of 2002, but more (45%) think supply chain disruptions could persist until the second half of next year. The problem facing the FOMC is that monetary policy can do nothing to address supply chain bottlenecks or increase the supply of oil and natural gas to alleviate soaring energy prices.

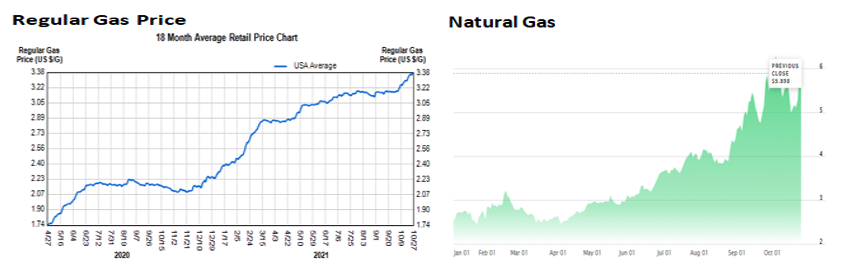

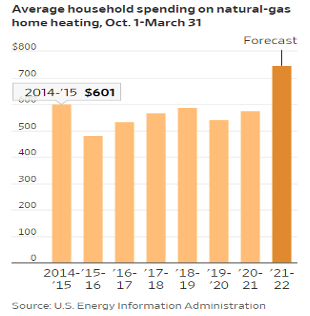

As the leaves fall off the trees in many parts of the US and the first chilly days require a jacket, awareness builds that cold weather and heating bills are right around a corner. Burrr! Winter heating costs can be a big deal if the winter is colder than normal or the price of natural gas or heating oil are higher. Natural gas prices have soared from $2.50 to $6.00 or by 140%. Heating oil is up 37% in 2021. In January the national price for a gallon of regular gas was $2.35 which has become $3.38, an increase of 43.8%. Gasoline prices are a great transmitter of inflation perception, since most people refill their gas tank at least once a week and it’s easy to remember what it cost a week or a month ago. After months of paying more to refill a gas tank and hearing stories about how much natural gas and heating oil have gone up, people are aware that there is an energy problem and are worried about their budgets. According to the Energy Information Administration, those using heating oil can expect to pay 43% more than last year and about 31% more for natural gas. How prices respond to the severity of this winter is asymmetrical. Prices will fall less if it is warmer and rise more if it is colder since higher demand and lower supply will push prices up more. The difference between the price increase in natural gas and the EIA’s estimates is that many consumers can lock in their cost with an annual contract. The provider can then hedge their costs in the natural gas futures market.

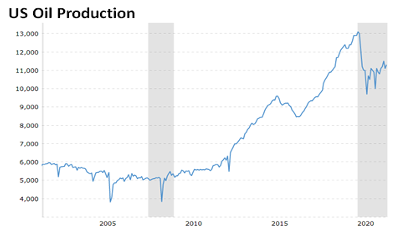

During his October 21 Town Hall meeting on CNN President Biden was asked what he could to do to bring energy prices down. The coherency of his response speaks for itself. "We're about $3.30 a gallon most places now when it was down in the single digits -- I mean single digits. Dollar plus. And that's because of the supply being withheld by OPEC. And so there's a lot of negotiation that is — there's a lot of Middle Eastern folks want to talk to me. I'm not sure I'm going to talk to them. But the point is it's about gas production." The ‘strategy’ is for the US to ask OPEC to produce more oil, if President Biden will even talk to them. In February 2020 the US was producing 13.1 million barrels a day but in October 2021 production was down -9.1% to 11.3 million barrels. The US has the capacity to quickly increase production by 500,000 barrels or more (down-1.8 million barrels), but President Biden is more willing to ask OPEC than US producers to increase production.

The optics of President Biden supporting an increase in oil production in the US would be unbearable to the ideologically driven progressive-socialist arm of the Democratic Party. The ideology of the ‘green energy only’ energy policy is so strident that any practical deviation is verboten. It appears that President Biden has decided that the burden of higher energy costs for the average American is a smaller problem than him having to listen to the outrage from members of his party. Let’s hope President Biden picks up the phone when OPEC calls.

For the ‘green energy only’ advocates, whatever financial burden middle and low income people will bear this winter for using fossil fuels to heat their home is simply a small price to pay when the goal is ‘saving the planet’. From where we are today, the coming valley of not having enough reliable green energy is intentionally overlooked. It will take many years before green energy can reliably provide all the needed energy to keep economic growth on track. The poster child of the coming energy valley is the capacity to recharge cars at night when the sun isn’t shining and the wind isn’t blowing all the time everywhere.

Great Britain is learning this lesson the hard way. In 2021 wind is only providing 7% of the country’s energy needs, down from the 25% it generated on average in 2020. California has no common sense plan to bridge the energy valley. During the summer when demand is high, the operator of the power grid is forced to issue warnings that often last for 2-3 days. The Independent System Operator (ISO) asks consumers to cut back on usage from 4pm to 9pm to avoid power outages. (Rates are higher during this window.) As more people buy EV’s this is going to become an unpleasant fact of life for more Californians. The best solution for the US is to emulate France, which gets 72% of its electricity from nuclear power and has for decades. Nuclear power provides the cleanest energy of ANY source when everything is included. Sorry, the ‘green energy only’ folks are not in favor of nuclear power so this viable and intelligent option is DOA. The power outages in California may be coming to a utility near you in coming years.

This is a discussion that the ‘only green energy’ folks simply won’t tolerate let alone learn from. Between June 2009 and March 2020 the US experienced its longest economic expansion in its history. Besides its duration, the other milestone is that CO2 emissions actually declined even as the US economy kept growing. Previously, every expansion in the last 250 years was accompanied by an increase in emissions, which only fell during a recession. Emissions fell during the deep 1982 recession and modestly during the shallow recessions in 1990 and 2001-2002. Emissions dropped sharply during the Financial Crisis but didn’t reverse up in the following years.

If someone had a clear crystal ball and told people in 2009 that the US was about to embark on the longest business expansion in its history and that oil production would increase 138% during the expansion, most people would have reasonably assumed that CO2 emissions would have gone up. The Financial Crisis recession ended in June 2009 and the expansion ended in February 2020. As the US Oil Production chart on page 6 shows, US oil production more than doubled from 2010 (5.5 million barrels) to 13.1 million barrels in 2020. As the chart on page 7 illustrates, CO2 emissions peaked in 2008 and have been trending lower ever since. This unprecedented decline was made possible by drilling for more fossil fuels, which is why the ‘only green energy’ groups have opposed to fracking and continue to do so. Fracking unearthed huge quantities of natural gas which drove the price down, so utilities found it was less expensive to use natural gas rather than dirty coal. In the last 10 years fracking has lowered CO2 emissions in the US more than all the green energy solutions combined. That will change going forward but there is lesson here. If one is ideologically driven, unconventional solutions will never be accepted since they may not fit into the approved group of solutions. If the ‘only green energy’ groups had their way in 2006, CO2 emissions would be much higher today. Those groups were wrong about fracking in 2006 and wrong today about nuclear power.

Historically, the trend in oil prices has led to changes in drilling in the US and around the globe. Higher prices were followed by more drilling and lower prices caused drilling activity to fall. Since 2005 the correlation during the oil price cycle has been tight, but the correlation since the low in April 2020 has broken down. The pattern in the US is the same. Oil reserves are replenished by new drilling, so the decline in drilling means there will be less oil in coming years.

Global production of oil was nearly equal to global consumption from 2016 until the Pandemic. As the US and global economy has rebounded since mid 2020, a gap between consumption and production has been persistent and explains why oil prices have been climbing. Oil inventories in the US are the lowest in many years, so supplies are likely to remain tight and be supportive of high prices for longer.

In the short term there are two factors that are likely to lead to a decline in oil prices. With demand higher than oil supplies, oil prices are higher for December 2021 delivery than for delivery in March 2022. This is unusual and is called backwardation. Oil consumers are willing to pay more than $7.00 a barrel for oil delivered in December than waiting for delivery in March. When the oil supply was ample the spread was negative with the out contract trading below the nearby contract. Unless there is a shortage, this is how the oil market normally trades. The willingness to pay a large premium underscores how much demand is exceeding supply now. Periods of backwardation are usually rectified in a matter of months as more oil is delivered to the market. President Biden has ruled out additional production in the US which is why the US is now more dependent on OPEC or Russia to increase their production.

The second reason why WTI oil is likely to pullback is based on oil’s chart. WTI Oil has traded between $83 and $85 a barrel and has ‘tested’ the intersection of three long term trend lines. WTI oil’s monthly RSI (blue line bottom panel) is near 70 which indicating that this rally is overbought and ready for a breather. The other 3 times the RSI was this high, oil prices fell or traded sideways. If WTI oil rallies above these 3 trend lines in the future, it would lead to an assault on $100 a barrel or higher.

In February 2020 the US was the largest oil producer in the world and far less dependent on other producers than in 2005 when production was much less. President Biden and the ‘only green energy’ lobby are willing to make the US more energy dependent in the name of their green ideology. One would think there is a common sense approach that would allow for progress on lowering CO2 emissions and maintaining energy independence. Energy could become an ongoing inflation issue if future supply lags global consumption and the decline in drilling suggests it may. Higher energy prices will make alternative green solutions more attractive. If one wants the world to adopt green energy, higher fossil energy prices are a tailwind. Machiavellian? Maybe, or crazy like a fox. Intentional? Worth pondering.

The Federal Reserve has no control over the global demand and supply of crude oil or the politics guiding US energy policy. Nonetheless, energy prices could make the FOMC’s job more difficult in coming years.

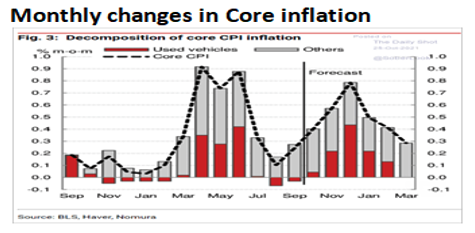

The path of Core Inflation will resemble a roller coaster in the next 8 months. The low take away values from October 2020 through February 2021 will make it easy for Core inflation to move higher until February 2022. After that the large takeaway values in April, May, and June 2020 will surely cause Core inflation to drop sharply in the second quarter of 2022. Last spring Chair Powell and the majority of economists were talking about how the low takeaway from the spring of 2020 would lead to an inflation peak in the second quarter of 2021 due to Base Effects. Chair Powell stuck to the ‘inflation will be transitory’ narrative because he expected supply chain and computer chips disruptions to begin to improve in the third quarter. Supply chain bottlenecks have worsened and will continue to be problematic into the first quarter. The computer chip shortage hasn’t improved. Powell also expected the labor market to improve in August and September as schools reopened, Covid-19 fears dissipated, and the Federal unemployment ended the weekly unemployment benefit of $300 on September 6. Employment growth should have improved in October as Delta cases fell and accelerate in coming months. When all is said and done the labor shortage should ease but not disappear, which will continue to apply upward pressure on wages in 2022.

In the spring of 2022 Core inflation will fall due to Reverse Base Effects. Will Core inflation will be under 3.0% and heading toward sub 2.5% in the third quarter or not?

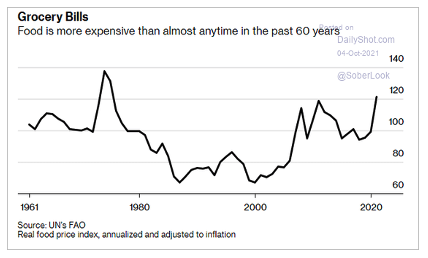

The nearby Table shows the weight each category has in the CPI and how much each went up from September 2020. At some point the increase in prices within each of these categories will stop going up. We can thus guess how much the CPI may fall for each category during 2022 if prices merely stay the same relative to where they were in April, May, and June 2021. The contribution to the CPI from New Cars (if the price is flat) would be -0.33% (0% flat X 3.8 weight), Used cars -0.83%, Gasoline -1.60%. Food is more expensive than at any time in the past 50 years, so Food prices aren’t likely to flat line in 2022. We’ll assume that Food prices and Home furnishings will go up at half the September 2021 rate. The CPI would fall for Food at home by -0.17% and Home furnishings by -0.18%. In total these categories represent 28.7% of the CPI and could lower the CPI by -3.11%. In September the headline CPI was up +5.4% but all of these categories won’t subtract from the CPI at the same time so it would be mistake to say the CPI will drop by -3.11%. If the prices for each category go up instead of sideways, the collective impact would be less than a -3.11% deduction. Conversely, the impact could easily exceed -3.11% if prices for these categories are lower in the second quarter of 2022. The expectation is that the headline CPI will below 3.0% by the middle of 2022. The Core CPI is not expected to decline as much as the headline CPI, so the headline CPI is likely to drop below the Core CPI.

Monetary policy can’t magically resolve supply chains bottlenecks, increase the number of computer chips desperately needed by the auto manufacturers, jumpstart the number of workers willing to reenter the labor force to slow the surge in wages, or directly reverse the surge in home prices and rents. As discussed in recent months, higher shelter inflation is already embedded in the Core CPI for 2022 due to the 20% increase in home prices which will bleed into the Shelter component of the CPI into 2023. Rents in many regions of the US have experienced a double digit increase. Zumper’s October national Rent Index shows that the median one-bedroom rent has risen by 11.8% since March 2020, and the two-bedroom median is up 14.3% over the same period. Rent increases represent pipeline inflation as each tenant renews their lease in future months and pays the higher rent. This is why Rents will add to Shelter inflation throughout 2022.

Owner’s Equivalent Rent (OER) and Rent of Primary residence represents 31.6% of the headline and Core CPI, which excludes Food and Energy. Shelter inflation is expected to add +1.4% to the Core CPI in 2022, based on the weights of OER and Rents, and the expected increases in OER and Rent in 2022. If New and Used car prices flat line as discussed above, the Core CPI will fall by -1.16 with Food at Home and Home Furnishing subtracting another -0.35%. The subtraction to the Core CPI from these categories would be -1.51%, but Shelter inflation could add +1.40% neutralizing the impact. With energy subtracting -1.60% from the headline CPI, it’s easy to see headline CPI dropping below the Core CPI.

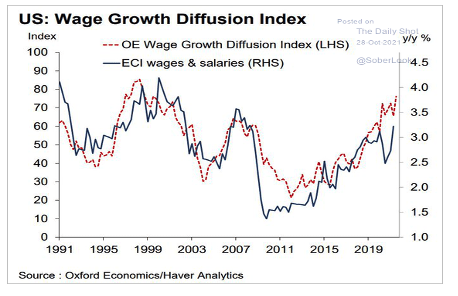

Although higher wage increases aren’t a category within the CPI, they can contribute to inflation as companies raise prices to offset higher labor costs. In September Average Hourly Earnings were up 4.6% and in the last 6 months up 6.0%. This indicates that wage inflation has been intensifying and there are no signs it is slowing down. Wage growth could add up to 0.5% to the Core CPI if wage growth persists in 2022, according to Goldman Sachs. More industries are increasing pay which is why Oxford Economics Wage Growth Diffusion Index is climbing and well above the Employment Cost Index (ECI). In the last 30 years the ECI has narrowed the gap before peaking as wages went up. The Diffusion Index has tended to top before the ECI which has yet to occur.

Wage growth started to pick up in 2017 when there were more Job Openings than Total Unemployed people. In April 2017 wages were up 2.55% from April 2016, but by March 2019 were up by 3.44%. There were 135 Job Openings for every 100 unemployed workers in September. Demand for workers is likely to remain high well into 2022 as consumers spend some of their savings. More workers are quitting their job than at any time in the past 20 years as the excess demand for workers gives them the confidence and leverage to switch to a new job. Wage growth for switchers is 2% higher than those who stay in the same job.

The National Average for small businesses having a tough time filling open positions is 65%, according to a recent survey of small businesses by Alignable. In some industries the labor shortage is so severe that it may take a year or more to reduce it to a manageable level. One of the kinks in the Supply Chain is Transportation and the US needs 80,000 new truck drivers to pick up goods at ports and deliver them. Trucks move more than 70% of all goods shipped in the US so this shortage is a big deal and is expected to last into the second half of 2002 at least. There are many reasons why the supply chain can’t simply be switched on and this is one of them.

There are two reasons why all the lost jobs are not going to be recovered. An extra 1.5 million Baby Boomers retired above the prior trend once the Pandemic hit. Most of these older retirees won’t return quickly. Between February 2020 and March 2021 almost 1.4 million moms of school aged children left the labor force. After a sharp rebound in mid 2020 the improvement since has been gradual and as of September has only recovered half of the decline. The improvement of the last 9 months will continue but a return to the January 2020 level isn’t likely. Of the 7.7 million unemployed people in September 2021 roughly 2.2 million were workers that won’t be reentering the labor force for many months. This is another reason why wages are likely to continue to grow by more than 4.0% in the first half of 2022.

Federal Reserve

Inflation has been hotter and more persistent that the FOMC expected. At the December 2020 meeting the FOMC estimated that PCE inflation would be 1.8% in 2021and 1.9% in 2022. Core PCE was projected to be 1.8% in 2021 and 1.9% in 2022. In September the projections for 2021 and 2022 jumped to 4.2% in 2021 and 2.2% next year, with Core PCE being 3.7% this year and 2.3% in 2022. The FOMC and Chair Powell have lost credibility after having missed so badly relative to the projections made in December 2020 and every meeting since.

All of the factors that caused the FOMC to be off so badly aren’t going to materially improve in the first quarter and may persist until mid 2022. More than one link in the Supply Chain is broken and the improvement when it comes will be gradual. The number of times the word shortage has been used in the Beige Book has increased from 12 last December to more than 70 leading up to the September FOMC meeting and the meeting on November 2-3. This Port Crisis isn’t going to improve for a long time according to this 28 year veteran truck driver. In his view the system of moving goods off ships, out of warehouses, and onto trucks is FUBAR. https://www.zerohedge.com/markets/ive-been-driving-trucks-20-years-ill-tell-you-why-americas-shipping-crisis-will-not-end

Oil prices may not fall much as supply remains constrained. Although Reverse Base Effects in the second quarter of 2022 will bring headline inflation down, Shelter inflation will offset a good portion of that improvement. Upward pressure on wages will continue as companies can’t fill open positions unless they increase pay. The labor market will remain tight as Baby Boomers sit out, and moms with children inch back into the labor market. With inflation holding up through the first quarter, the FOMC’s and Chair Powell’s credibility will take a further hit as inflation climbs in coming months.

Chair Powell has repeatedly said touted the Fed’s tools and that "No one should doubt that we will use these tools to guide inflation back down to 2% over time.” Does anyone really believe that the FOMC will ever vote to aggressively address inflation? I’m skeptical and the way the FOMC has handled the run up to the taper announcement has added to my doubting Thomas view. Home prices have increased by more than 15% from a year ago for many months, so continuing to buy $40 billion a month of Mortgage Backed Securities has been indefensible. With Treasury yields so low, the rationale for purchasing $80 billion a month of Treasury debt is unwarranted. Using 5 months to tee it up tapering so the financial markets don’t throw a tantrum has also undercut the FOMC’s credibility. It reinforces the impression the FOMC will never do anything that may result in an OMG correction in stocks.

Markets are ready for the taper announcement at the November 3 FOMC meeting and have adjusted to the prospect that the FOMC will taper by $15 billion a month rather than the $10 billion expected a few weeks ago. The tapering process would finish in 8 months rather than 10 months if the monthly purchases are reduced by $15 billion a month.

There is another option that would likely increase the FOMC’s credibility and the perception of their commitment in addressing inflation. The FOMC would be served well by shrinking their monthly purchases by $20 billion. The whole taper process would end in six months so the FOMC could evaluate the timing of a rate increase 2 months earlier. That additional flexibility could prove helpful since numerous FOMC members have said they won’t taper and raise rates at the same time. Increasing the amount of the taper wouldn’t hurt economic activity much, so the economic downside would be negligible. In contrast, financial markets might reassess the FOMC’s resolve and think the FOMC will not allow inflation to get out of hand after all. The FOMC is concerned that inflation expectations might become ‘unhinged’ and there are indications that it’s already happening. The 3-year measure of inflation expectations is already the highest in more than a decade. By increasing the amount of the taper the FOMC may be able to better hold inflation expectations in check, even as inflation rises in coming months.

When the FOMC releases its statement after the November 2-3 meeting and during Chair Powell’s press conference, the tone is likely to be more hawkish than it’s been, whether or not the taper is $15 billion or $20 billion a month. Chair Powell will emphasize that the bar for increasing the federal funds rate is higher than tapering and dependent on improvement in the labor market. The inflation target has been met since inflation has been way above the FOMC’s target of 2.0% for a period of time.

Treasury Yields

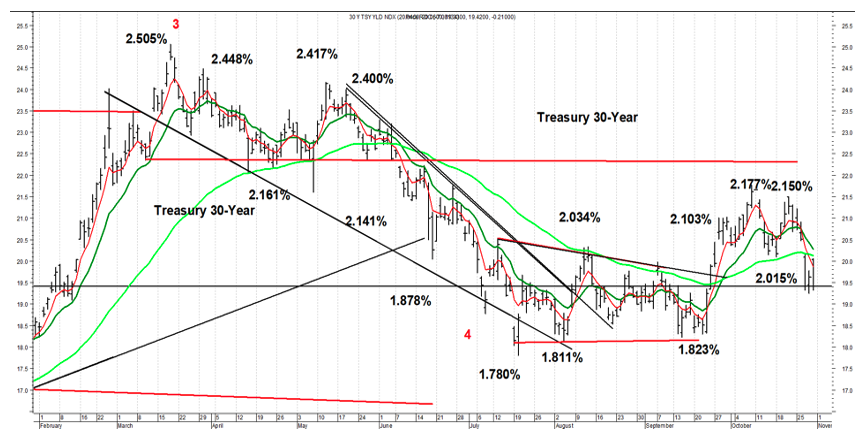

In late March the 10-year Treasury Yield exceeded its early March high of 1.754% when it rose to 1.765%. The 30-year Treasury Yield didn’t confirm this new high as it posted a lower peak. (2.448% vs. 2.505%) This inter market divergence suggested a trend change was likely and rather than continuing to climb, Treasury yields would actually fall, and they did.

In October the same inter market divergence developed as the 10-year exceeded 1.617% when it jumped to 1.691%, but the 30-year Treasury yield topped at 2.15% versus the prior high of 2.177%. This suggested that Treasury yields were set up for a decline in coming weeks. Treasury yields are expected to exceed the highs reached in March 2021 in the first half of 2022.

If the FOMC and Chair Powell adopt a more hawkish tone or decide to taper by $20 billion, Treasury yields are expected to decline more as the bond market responds to the FOMC’s inflation fighting prowess. There is a large short position in Treasury bonds. If Treasury bonds don’t decline after the Taper announcement those short may be compelled forced to cover, which would push Treasury yields down.

Stocks

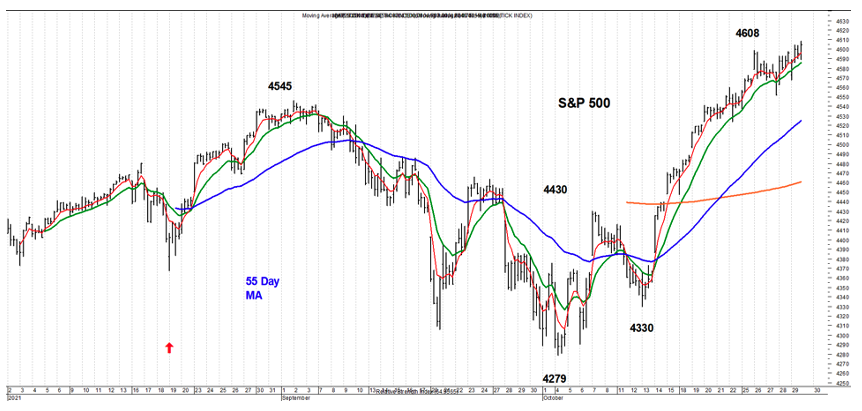

The S&P 500 has pushed to a new all time high and as long as the 5 day Moving Average (red) is above the 13 day Moving average, the trend is up. The S&P 500 will have to fall and stay below 4590 for that to develop. If the FOMC is less dovish or tapers by $20 billion, the S&P 500 is expected to pullback to 4450 – 4500. The major trend is up and bullish.

Gold

After topping just above $1900 in early June, Gold has been correcting. Chair Powell has finally acknowledged that inflation won’t be transitory. As discussed previously, inflation is likely to run hot for at least another 4 months. As expected Gold bottomed above $1720 and quickly tested the rising trend line just above $1800. Gold is expected to break above this trend line and potentially test $1800 as inflation becomes a tailwind for Gold.

Supply Chain Issues

Jim Welsh

@JimWelshMacro

[email protected], MacroTides.com

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All