With inflation surprising to the upside and lasting longer than most expect, we believe investors will need to rethink portfolio management and what it means to own a balanced portfolio. Below we address many of the questions related to our view on inflation and its implications for the future.

Question: What is RBA’s view on what appears to be booming inflation and the potential for stagflation?

Prices have clearly surprised to the upside and have already lasted for longer than most expected. In fact, today’s supply disruptions have now surpassed the duration of the 1973/1974 oil embargo. The real question is how long will these inflationary pressures persist? Regarding stagflation, we see nothing in the data to suggest this problem. Stagflation consists of rising unemployment and low growth with higher inflation. Today, and we think for the foreseeable future, we have the opposite: falling unemployment, strong growth, and though high, what will likely be moderating inflation later next year.

Question: Can you explain transitory versus persistent inflation?

Persistent inflation refers to changes to the structural inflationary dynamic. We see three main reasons why inflation may be structurally higher in the coming years.

1) A reversal of globalization

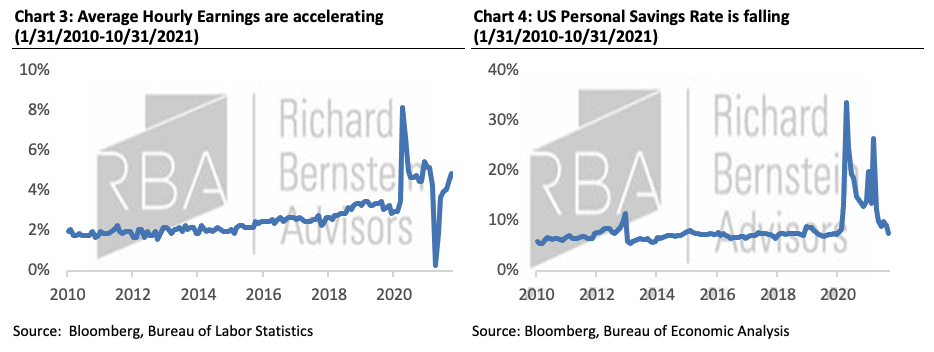

2) Wage pressure

3) Baby boomers evolving from a generation of savers to a generation of spenders

Transitory is less time-dependent and is more a function of whether there are reasons why the inflationary impulse might subside. For example, it is likely that at some point manufacturing capacity will increase as employees come back to the workforce.

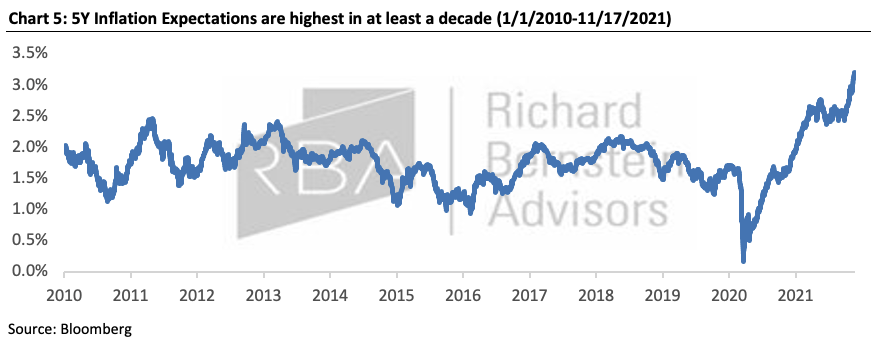

Ultimately, we think secular forces – deglobalization, wage pressures, the aging population– will tilt inflation above 2% for longer than expected. Additionally, transitory factors can become persistent if inflation expectations increase and remain elevated, creating difficult choices for the Fed down the road.

Question: Does the Fed changing their inflation mandate to an average of 2% change anything?

The longer the Fed goes without tightening policy because they want inflation to average 2%, the more inflation expectations could increase, the more persistent they may become, and the harder it could be for the Fed to rein it in. Under such circumstances, the Fed could risk losing control of the inflation narrative, thereby necessitating faster monetary tightening, and causing a slowdown in economic growth. Though we don’t think the Fed will aggressively hike rates in 2022 - as the high inflation we see today begins to fall - we do believe risks created by the average inflation mandate exist if inflation expectations continue to increase.

Question: We hear a lot about supply chain bottlenecks, can you explain what that means?

Supply chain bottlenecks are just a way of saying there is a mismatch between production and demand. COVID shut down manufacturing for lengthy periods of time and demand was only shut down for a fraction of that time. That mismatch created a situation where manufacturing couldn’t keep up with demand and employers couldn’t keep up with hiring enough people to meet that demand.

What has made things worse is that the supply chain is a global network, and the recovery from the pandemic has been very uneven. Since the 1970s, companies have increased the outsourcing of production, particularly of sophisticated products, to increase margins while keeping costs down for consumers. One way to think about the global supply chain is like a symphony: If one instrument is off, suddenly, the entire orchestra is off. When all the world’s recoveries are at different stages it's very hard for this symphony to be in sync any time soon, in our view.

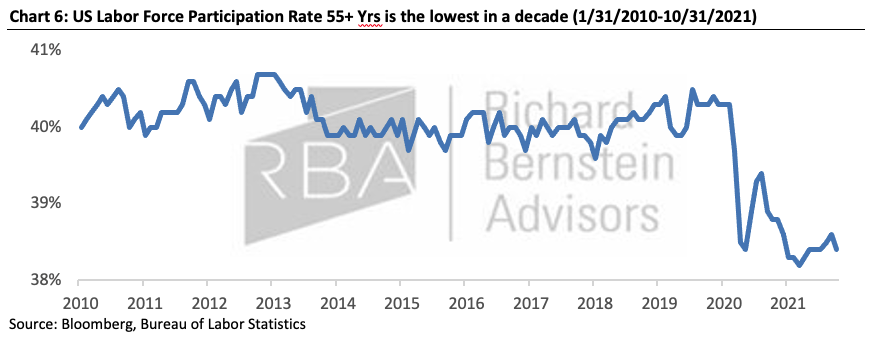

Question: If labor shortages are a key to supply chain issues, why have those not yet alleviated themselves?

We think labor shortages can be explained by a combination of government assistance during the pandemic, mobility of labor creating alternatives for the workforce, a lack of childcare options, a decrease in immigration, and older workers not returning after the covid shutdown. None of these issues likely resolve quickly.

Question: What are the market implications of these inflationary dynamics?

We believe investors should be overweight inflationary assets like Energy and Materials, as well as overweight sectors that will do well in a higher rate and steeper yield curve environment, like Financials.

On the flip side of the coin, we believe investors should be underweight growth and speculative Technology as these areas behave as long duration assets. If we’re right that inflation will drive interest rates higher, then a company whose valuation is based on future earnings should be worth less in today's dollars.

In fixed income, we prefer having exposure to credit risk rather than interest rate risk. We also prefer inflation protected securities like TIPS, curve steepeners, and cash-like instruments. We want to position the portfolio in a low duration manner and underweight Treasuries.

Question: Any final thoughts, advice, projections?

If we're right on the inflationary environment lasting for longer than expected and at a higher rate than expected, then portfolio management is going to have to change. The traditional 60/40 portfolio could have a lot of trouble performing to the level it has in the past, especially if rates going higher is the reason for lower equity prices. We think the way investors manage their portfolio needs to be more balanced across the different risks. That's a totally new dynamic we don't think most money managers have thought about for the last 20 years.

Michael Contopoulos

Director of Fixed Income

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

More Global Markets Topics >