Moderate inflation can be good, especially for some value stocks. Christian Correa breaks down why investors should not be afraid of the current inflationary or rising rate environments and explains how they can actually help some businesses and areas of the equity market.

Moderate inflation can be good, especially for some value stocks. Yet, the word “inflation” strikes fear into the hearts of many investors. Those who are old enough to remember might think about the United States in the 1970s or Brazil and the former Yugoslavia in the early 1990s. Today’s environment is very different. We believe we are in a period of transitory price increases which will last months, not persistent high inflation lasting years. We think current cost-push inflation is poised to give way to a healthy, regenerative demand-pull environment, replete with moderate economic growth that is beneficial for the value companies in which we invest.

Under Pressure

History has shown moderate inflation can be good for value stocks, as illustrated in the chart below. We consider “moderate” to be between 2% and 4%. Compared to historically low inflation rates since the global financial crisis (GFC) over a decade ago, this may feel like a shock. However, modest demand-pull inflation is healthy and normal. Demand-pull inflation occurs when increased consumer demand for products allows companies to raise prices. This usually coincides with a period of moderate economic growth, as consumer demand makes up about 70% of US gross domestic product (GDP). When consumers and businesses consume more, the economy grows. This creates a favorable environment for many value companies.

The pandemic has caused cost-push inflation. The cost of inputs has gone up due to component and labor shortages. Investing in businesses that can absorb these price increases or pass them along to their customers in the form of higher prices without it affecting their market share is the first line of defense in a cost-push environment. In our experience, companies with strong brand names or whose products are in high demand and have few substitutes can achieve this. These companies may also benefit when the inflationary environment abates, as they can continue to charge a higher price for their product, leading to margin expansion which may lift the stock price.

Companies with low pricing power, such as companies with fixed-price contracts or those which do not have a powerful brand name behind them, might struggle to raise prices when their cost of materials increases. This leads to margin erosion and can weaken the financial standing of the company, reducing the stock price. This intricate understanding of a company, its place in the market, and the effect of inflation on its business can only be gained by in-depth fundamental research performed by an industry expert.

Golden Years

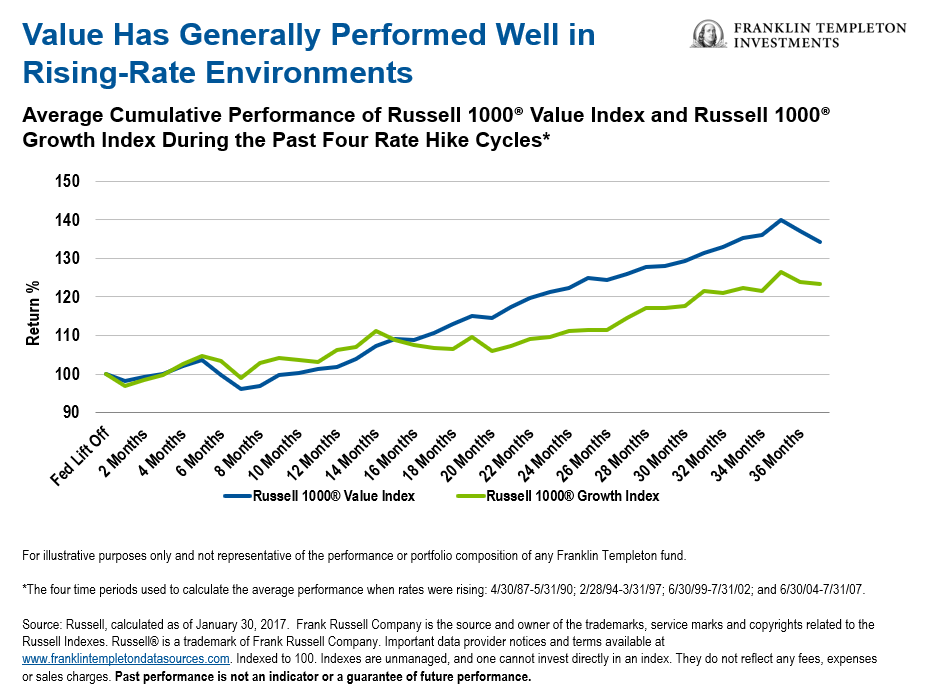

People usually associate interest rates with bond prices. What many investors may not consider is the profound effect interest rates also have on equity prices, particularly growth stocks. Rates have been historically low since 2009. During this time, prices for stocks with long-dated cash flows, or long duration, have soared to dizzying highs, creating a golden period for growth investing. In fact, the S&P 500 Index is currently at a record concentration of growth stocks versus value stocks due to the notable outperformance of growth versus value. 1

While interest rates are unlikely to rise back to levels seen in the 1980s, we expect they will soon increase. This should hurt growth stocks much more than financially sound value companies with low leverage. The prospect of higher interest rates provides real consequences for investors in long duration assets, because when the discount rate increases, the current value of the future stream of cash flows will fall, potentially taking the stock price with it. The interest rate effect is more pronounced when future cash flows are significantly greater than near-term cash flows. Companies currently trading at 30x earnings are doing so based on very long-dated expected cash flows that could be heavily affected when rates rise. However, value stocks trading at relatively low multiples of current cash flows or earnings—where near-term cash flow streams are larger relative to longer term cash flows—are less affected by increases in the discount rate and offer a better defense in the face of rising rates.

Black Tie White Noise

The recovery from the GFC brought on a period of unprecedented technological innovation, which encouraged increasing allocations to growth stocks. We believe the economy, as well as the market, has entered a new phase. Currently, we see cost-push inflation brought on by COVID-19-related supply chain issues. As the post-COVID economic recovery progresses, we expect cost-push inflation will subside as regions responsible for supplying the raw components for saleable goods ramp up production, and labor and logistical challenges also fade. The economy can then transition to moderate demand-pull inflation fueled by consumer demand and spending power, and a resulting period of moderate economic growth.

Value stocks, which have done well in an environment of moderate economic growth and inflation and are generally more insulated from rising rates due to their shorter duration profile, provide much-needed balance to long duration growth stocks and are well poised to offer some of the best yields in the marketplace, if you know where to look. An environment of moderate growth also provides a perfect foundation for the execution of turnaround stories and restructuring plans that unlock shareholder value, which are common characteristics of value equities as well. An investment team that has been evaluating companies for decades across various inflationary and rising rate environments knows how to ignore the white noise and stick to what it does best, which is identifying companies that are less subject to these impacts and can continue to generate value for shareholders across multiple environments.

What Are the Risks?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors or general market conditions. Value securities may not increase in price as anticipated or may decline further in value. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Indices are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this presentation has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com - Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Franklin Distributors, LLC. Member FINRA/SIPC. Prior to July 7, 2021, Franklin Templeton Distributors, Inc., and Legg Mason Investor Services, LLC served as mutual fund distributors for Franklin Templeton.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments