1. Rising rates can be a double-edged sword for high yield credit. On the one hand, the sector’s shorter average duration can draw fixed income investors away from longer-duration assets when rates are rising. On the other hand, rising rates often go hand in hand with tighter financial conditions, making it more expensive for companies to borrow. How do you expect the sector to perform if rates begin to rise?

We believe strong credit fundamentals and strong earnings growth will continue to support high yield credit spreads in a rising rate environment. Credit outlook revisions have been positive among Loomis Sayles’ credit analysts and street analysts, suggesting that more companies are likely to have their credit ratings upgraded rather than downgraded. We believe this trend of positive credit outlook revisions will continue into 2022, helping to provide a potential tailwind for the high yield market.

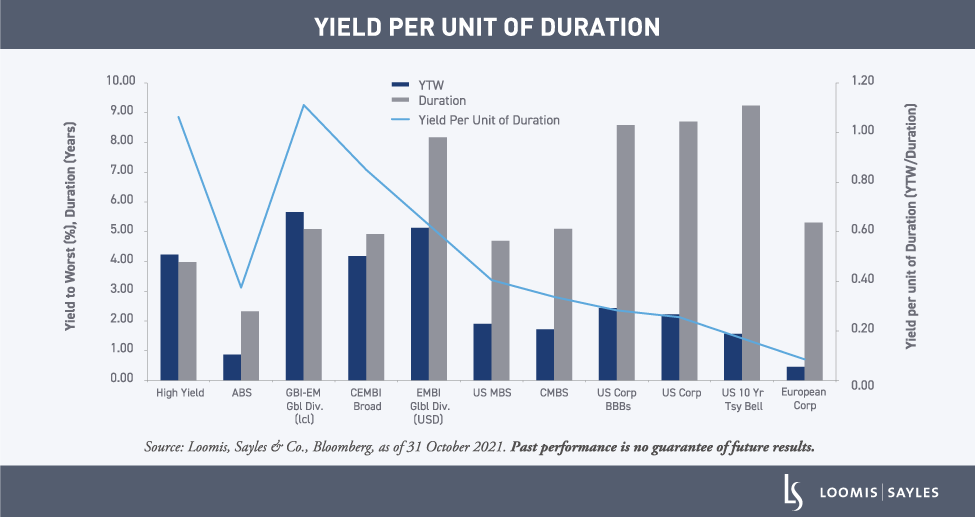

When it comes to duration, we think high yield credit currently stands out relative to other US credit offerings because of its relatively attractive yield per unit of duration (see chart below).

2. Some market participants are expecting CCC-rated bonds to outperform this year, due to low defaults and attractive carry. Do you agree with that take?

We don’t disagree that CCC-rated corporate bonds have traditionally offered an excess spread that can act as a natural hedge against rising base rates. However, we currently view single-B-rated corporate bonds as a better trade in 2022.

We believe that CCC-rated corporate bonds will struggle as we progress through the expansion phase of the credit cycle, which has historically been a phase when CCCs lag both BB and B-rated bonds. There’s also potential defaults to consider. While we expect the low default environment to continue into 2022, we believe defaults reached a cycle low in 2021. We think investors will likely price an additional risk premium into CCC cohort as default rates gently increase.

We like the single-B-rated cohort of the high yield credit markets because we believe it’s currently better-positioned to absorb the rise in base rates while maintaining strong credit fundamentals and negligible defaults/downgrades.

3. With spreads tight and valuations elevated, it seems like a bond picker’s market. Which areas of the market do you think offer the most value?

We believe nearly any market can be a bond picker’s market! The high yield credit market has been trading in a tight range and dispersion is currently near all-time lows. But we believe opportunities can continue to arise for discerning investors.

We see potential for continued volatility within COVID-19-affected or reopening industries, which could present opportunities to add potential alpha through careful selection. We currently favor issuers that are focused on improving their balance sheets and aspire to achieve investment grade ratings.

We also think selected communication names look attractive. The communications industry benefited from revenue that was pulled forward during the pandemic, but battles a perceived slowing of growth. We like the industry’s defensive nature, which has delivered durable cash flows and typically performs well in the expansion phase of the credit cycle.

Past performance is no guarantee of future results.

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Commodity, interest and derivative trading involves substantial risk of loss.

Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy.

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

MALR028339

© Loomis, Sayles & Co.

Read more commentaries by Loomis, Sayles & Co.