FOMC Tightens as Economy Slows

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEconomic Concerns Increase

In 2021 the FOMC refused to accept and acknowledge that inflation was getting worse in the second and third quarter and continued with its monthly purchases of $120 billion in Treasury debt and Mortgage Backed Securities. At the November FOMC meeting the FOMC timidly lowered its purchases by just $15 billion a month, as Chair Powell belatedly retired the word transitory. As headline and core inflation ramped higher the FOMC increased the taper from $15 billion to $30 billion at the December meeting. The members of the FOMC have widely acknowledged that the FOMC is behind the inflation curve. In his testimony before the Senate Committee on Banking, Housing, and Urban Affairs on January 11, Chair Powell presented the path forward. ““As we move through this year … if things develop as expected, we’ll be normalizing policy, meaning we’re going to end our asset purchases in March, meaning we’ll be raising rates over the course of the year. At some point perhaps later this year we will start to allow the balance sheet to run off, and that’s just the road to normalizing policy.”

After waiting too long to begin to remove accommodation in 2021, the FOMC will be tightening just as the economy is slowing down. During February investors will be buffeted by economic reports showing that the US economy slowed markedly in January. We can expect to read articles and interviews on CNBC and Bloomberg that discuss the specter of the FOMC making another policy mistake by removing accommodation as the economy slows, which could push the economy into a recession before the end of 2022.

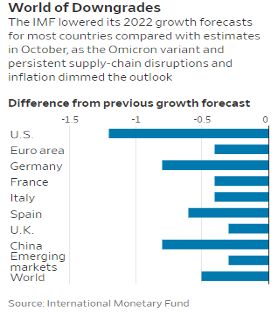

On January 25 the International Monetary Fund (IMF) lowered its global GDP forecast to 4.4% from the 4.9% it projected in the October 2021 forecast. The IMF cut the estimate for the US from 5.4% to 4.0%. The IMF cited the drag from Omicron in the first quarter, persistent supply chain disruptions, and the dimmed prospects for President Biden’s Build Back Better bill. The IMF also lowered estimates for Germany, France, Italy, Spain, United Kingdom, China, and Emerging Markets. The IMF trimmed its estimate for China by 0.8% and lowered the estimate to 4.8%. It also cut Brazil and Mexico by 1.2%, so Brazil will grow 0.3% in 2022 and Mexico 2.8%. Over the last 12 months Brazil’s central bank has lifted its policy rate from 2.0% to 8.0% as Brazil’s inflation rate soared to 35% (yes not a misprint) before falling to 17.8% in December. Mexico’s CPI reached 6.1% in January even though the Banco de Mexico increased its policy rate from 4.0% to 5.25% in 2021.

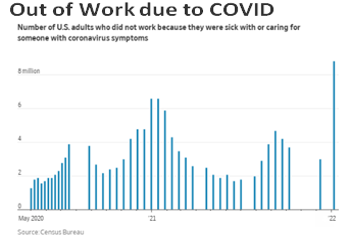

In December the Census Bureau conducted its monthly ‘Household Pulse’ survey and found that 3 million workers were not working due to COVID. They were home with COVID or were taking care of someone who was sick. In January the number of workers who weren’t at work mushroomed to 8.8 million, which represents more than 5% of the US’s workforce. This likely forced many small businesses to reduce production, output, or lower the number of hours their business could be open.

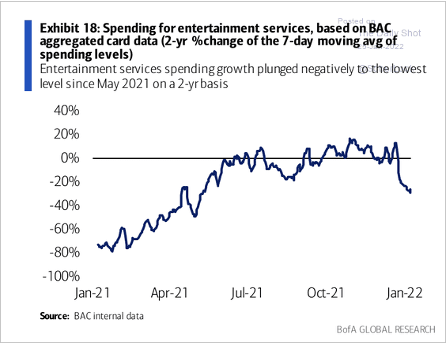

The surge in Omicron cases and hospitalizations in December and early January convinced many healthy people that hunkering down was warranted to minimize the risk of getting infected. People stopped going to restaurants, movies, or flying. On January 25, 1.05 million passengers went through TSA checkpoints less than half of the number that flew on December 19. According to aggregated credit card data by Bank of America, spending on entertainment services plunged by more than -20% in the first 3 weeks of January to the lowest level since May of last year.

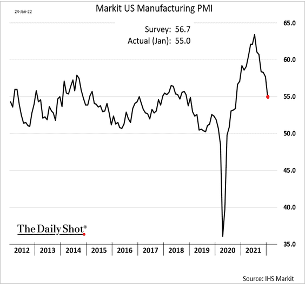

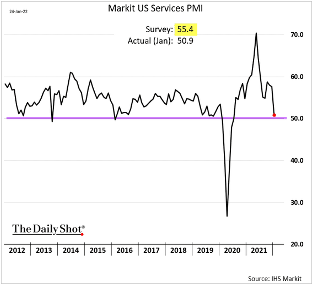

A foreshadowing of the coming weakness was illustrated by the Markit surveys for Manufacturing and Services for January. The estimate for Manufacturing was 56.7 but it came in at 55.0 and back to levels last seen in 2018. Services came in much weaker at 50.9 compared to the estimate of 55.4. The degree of the services miss is attention getting but understandable as services require much more face to face activity. The key lesson is that the majority of economic reports that will be released during February for January are going to come in lower than the estimates. This will give the impression that the economy is slowing more rapidly and raise the prospect of a recession beginning before the end of 2022.

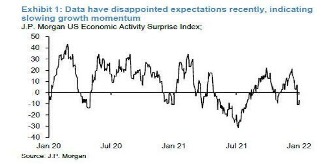

Economic Surprise Indexes are calculated by comparing actual data to estimates. When the economy emerges from a soft patch, data improves faster than economist’s estimates for growth, which causes the Surprise Index to rise. After a period when the economy is humming along, estimates improve reflecting crowing confidence. When growth decelerates, the actual data comes in below estimates so the Surprise Index falls. The real ‘surprise’ is that economists are consistently behind the curve. This is why the Surprise Indexes are a lagging indicator rather than a helpful forecasting tool. Ironically, the majority of those who use the Economic Surprise Indexes think they are a forecasting tool.

The spread of Omicron during December and January depressed the economy more than expected, which is why the J.P. Morgan Activity Surprise Index has been falling. The Commerce Department reported on January 28 that consumer spending fell by 0.6% in December. This caused the Atlanta Federal Reserve’s GDP Now forecast estimate the first quarter GDP to be slashed to just 0.1%. J P Morgan has cut its 2022 GDP estimate and Bank of America lowered its Q1 GDP estimate to 1.0% from 4.0%. The economy was decidedly weaker in January so the Surprise Indexes will fall more in coming weeks as January economic data is released in February. More firms will undoubtedly respond to the weaker data by cutting their estimates for Q1 and 2022. These negative revisions will further increase fears that the FOMC may tip the economy into a recession by raising interest rate as the economy slows.

Recession in 2022? Not Likely

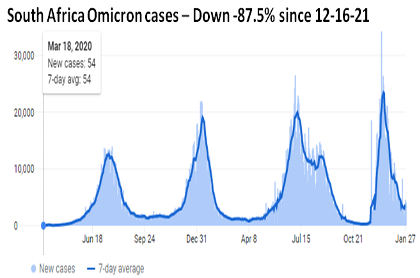

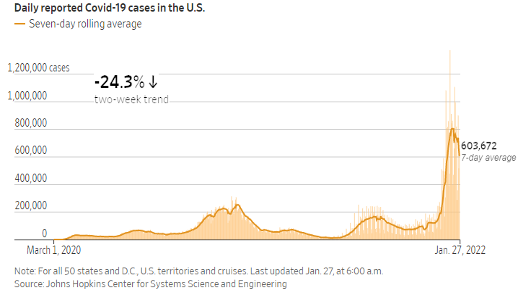

There are a number of reasons why a recession isn’t likely and why the slowdown in the first quarter will not become a recession. The primary reason the economy is slowing is due to the Omicron variant. As discussed in the January 17 Weekly Technical Review I thought there would be a peak in the number of cases within 10 days. “It appears that the number of Omicron cases have peaked in South Africa. The Department of Health in South Africa reported that the number of daily new cases had fallen by -29.7% as of December 25 (89,781 cases), compared with the number of new cases detected in the previous week (127,753). This is important since South Africa was the first country to identify the Omicron variant as being highly transmissible on November 26, 2021 and could now be signaling that it is over. In Great Britain the number of cases has plunged from 193,814 on January 5 to 70,160 on January 16. The number of cases in the US is likely to peak within the next 10 days.” It appears that Omicron cases have peaked in the US based on recent data. Hospitalizations and deaths should top out soon and reverse lower in the first two weeks of February. The US economy should respond quickly and display renewed growth in May as April data is released. This should alleviate recession fears significantly.

The Leading Economic Index (LEI) has historically provided a good advance warning before the onset of a recession. In the last 50 years the LEI has begun to decline prior to the start of a recession by at least 7 months with a median lead time of 10 months. Since the LEI hit a new high in January the LEI suggests a recession is unlikely in 2022.

In January the LEI continued to move higher so it hasn’t even begun to flatten out let alone turn down. (LEI charts provided by Doug Short Advisor Perspectives)

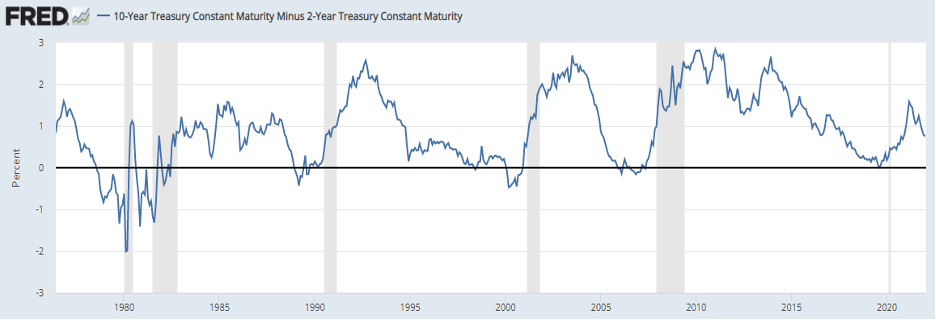

The yield curve is most often determined by comparing the 2-year Treasury yield to the 10-year Treasury yield. When the 10-year yield falls below the 2-year yield, the yield curve becomes inverted. The yield curve has provided excellent recession warnings in the last 40 years, with a median lead time of 19 months. The 10-year Treasury yield is 1.782% and the 2-year Treasury yield is 1.166%, so the yield curve is a positive 0.616% and not close to inverting.

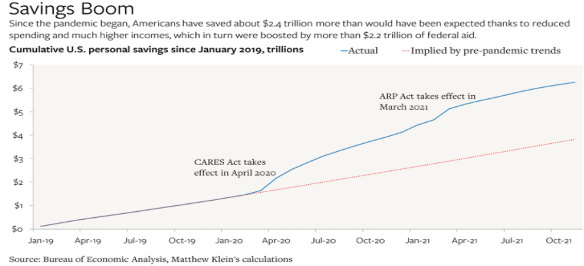

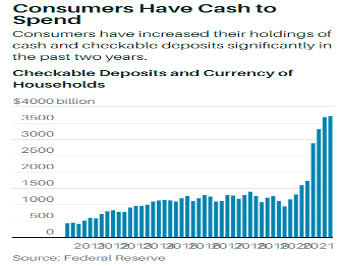

Consumer spending represents 70% of GDP so the financial health of the consumer is important. Entering 2022 consumers have more than $2.5 trillion is savings which amounts to 10% of GDP. Prior to the Pandemic consumers held less than $1 trillion in cash and checkable deposits. At the end of 2021 there was more than $3.6 trillion in cash and checkable deposits that will support economic growth through 2022 at least. The monthly Savings Rate was 7.9% in December and back to where it was in 2019 just before the Pandemic. Some have drawn the wrong conclusion and think this means consumers have used up all of their savings. This overlooks the accumulated savings that built up from March 2020 through August 2021 when the Savings Rate was above 10.0%. The savings rate for December reflects what consumers saved in the month of December and has nothing to do with accumulated savings during the Pandemic.

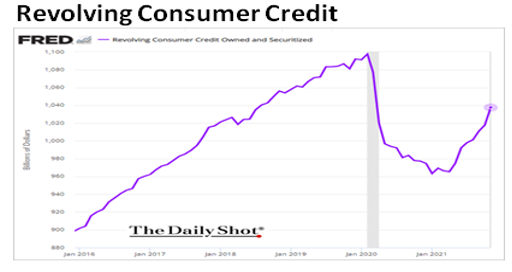

During the Pandemic consumers aggressively paid down revolving credit card debt. In February 2020, consumer’s revolving credit card balances totaled $1.0975 trillion and were down to $965.3 billion in April 2021. As the economy reopened in the second and third quarter of 2021 consumers increased their card balances to $1.0374 trillion in November. Surely, balances increased in December as consumers celebrated the holidays. Credit card balances were down -5.5% from the peak in February 2020 so consumers have more money to spend at the mall.

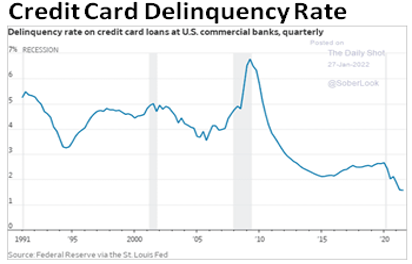

The delinquency rate on credit cards peak in Q2 of 2009 at 6.87% and fell to 2.52% by March 31, 2020. With the federal government transferring trillions of dollars to consumers whether they were working or not, the delinquency rate dropped to 1.46% by the end of September 30, 2021 as consumers prudently paid down high rate credit card debt. Credit card companies are aggressively offering cards to existing and new users, so demand from credit should increase.

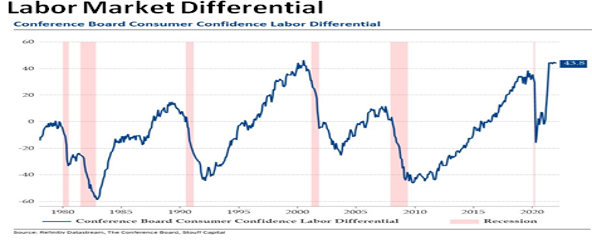

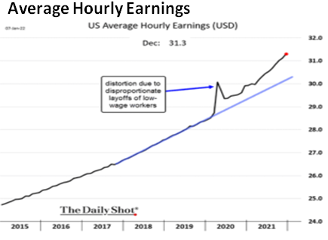

Labor market tightness may be the highest ever as businesses simply can’t find willing or skilled workers, despite raising wages or offering bonuses. Average Hourly Earnings are well above the pre Pandemic trend and will move higher as the labor market remains historically tight. The Labor Market Differential is derived from the Conference Board’s monthly Consumer Confidence Survey. The Conference Board subtracts the percentage of respondents that say ‘jobs are plentiful’ from those who reply that ‘jobs are hard to get’. When there is a plurality saying ‘jobs are plentiful’, it is a reflection of labor market tightness. When the percent of respondents say ‘jobs are hard to get’, a recession has followed usually within 12 months. The Labor Market Differential is still rising so the labor market is likely to stay tight for months and the risk of a recession is way down the road. In December Average Hourly Wages were up 4.9% from December 2021. Although wage increases will moderate in 2022, wage income will have reset at a higher plateau, which will continue support consumer spending, especially after inflation moderates and real wages grow.

Indicators that have done a good job of telegraphing an oncoming recession uniformly suggest that a recession before the end of 2022 is unlikely. There are geopolitical risks that could change this outlook literally overnight, so there are known unknowns. Based on what is known the economy is expected to rebound after the Omicron induced slowdown. That doesn’t mean there aren’t other known risks to monitor.

Inflation

My base case for inflation is that headline inflation is expected to fall measurably in the second quarter, although Core inflation is not likely to fall as much. The FOMC is expected to increase the federal funds rate by 0.25% at the March, May, and June meeting. The FOMC may then have the option to hit the pause button if inflation moderates and after increasing the funds rate from 0.10% to 0.85% in June. A review of the projected glide path for inflation in 2022 can provided clarity.

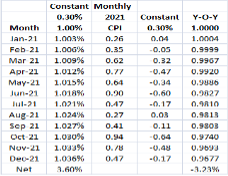

Reverse Base Effects will play a big role in 2022. The column entitled ‘2021 CPI’ shows the monthly change in the headline CPI during 2021. The monthly values for each month will be subtracted from the year-over-year calculation, and each month in 2022 will be added. Starting in March 2021, the monthly take away values increase significantly and increase to 0.77% in April, 0.64% in May, and 0.90% in June. The second column ‘0.30%’ assumes that headline inflation will increase 0.30% every month which is obviously not going to happen. But the assumption that headline CPI inflation may be 3.6% for all of 2022 seems a reasonable guess. If inflation does rise by 3.6%, something that cost $100 in December 2021 would cost $103.60 in December 2022. The third column entitled ‘Constant 0.30%’ shows what the monthly change could be in 2022 assuming headline inflation increases by 0.30% and after subtracting the monthly take away value from 2021. If headline inflation rises by 0.30% in March 2022, headline inflation will fall by 0.32% after subtracting the 0.62% increase in March 2021. In April headline inflation could fall by -0.47%, -0.34% in May, and in June by -0.60%. The CPI could drop by -1.41% even if prices rise by 0.30% each month. There is a chance that at some point in 2022 some of the largest drivers of inflation in 2021 could actually decline, which would cause the headline CPI to fall more rapidly.

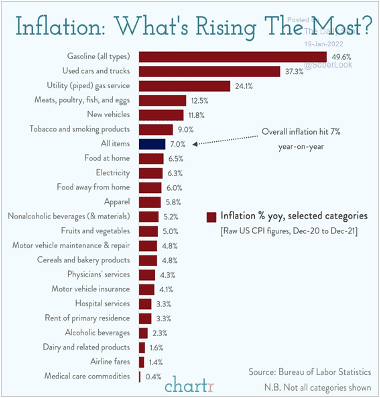

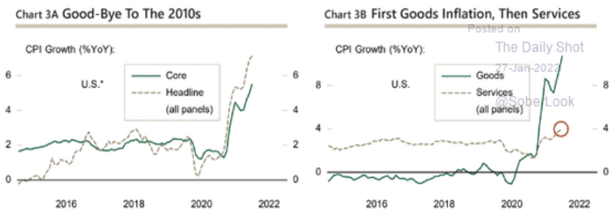

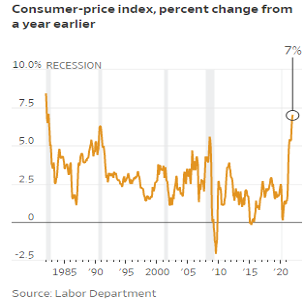

The headline Consumer Price Index (CPI) was up 7.0% in December 2021 from the prior December but the dispersion of the price increases within the CPI was broad. Gasoline was up 49.6% but Airline fares were only up 1.4%. The problem is that gasoline contributes 4.02% to the CPI while Airline Fares represent just 0.619%. If the CPI is going to fall more than expected the sectors with the largest run up will have to come off the boil.

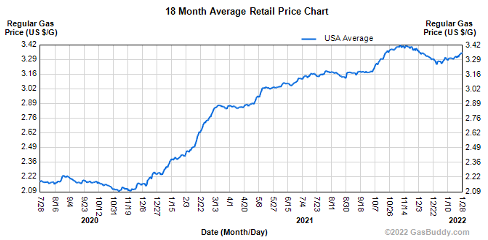

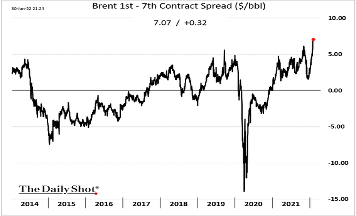

A gallon of regular gas cost $2.09 in November 2020 and a year later was up to $3.42. It dipped $0.15 after President Biden announced that oil would be sold from the Strategic Petroleum Reserve. If Omicron recedes as expected the demand for gasoline will increase with the summer driving season, so any price decline is likely to be modest. Gasline prices may fall if crude oil prices fall $15.00 a barrell in coming months. (Chart below) Crude oil is approaching a trend line connecting the 3 prior highs of the last year. The RSI is in the bottom panel and shows that Crude oil is overbought, which suggests this trend line will hold and result in a high. Crude rallied $11.00 off the low in early December and an equal move from the low of $81.90 would target a high near $92.80.

In the November 2021 Macro Tides I discussed why crude oil was likely near a high and likely to correct. “WTI Oil has traded between $83 and $85 a barrel and has ‘tested’ the intersection of three long term trend lines. WTI oil’s monthly RSI (blue line bottom panel) is near 70 which indicating that this rally is overbought and ready for a breather. Oil prices are higher for December 2021 delivery than for delivery in March 2022. This is unusual and is called backwardation. Periods of backwardation are usually rectified in a matter of months as more oil is delivered to the market.” Crude oil topped at $84.97 on November 10 and quickly fell to $62.42 on December 2. Backwardation has again become extreme so another decline is likely after crude tops above $90.00 a barrel. If crude oil drops $15 a barrel, regular gasoline could fall by $0.20 or more. Gas prices added 1.99% to the CPI’s 7.0% rise in 2021, and a decline of $0.20 would shave -.23 off the CPI.

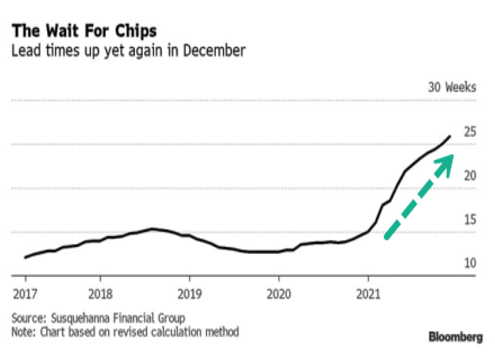

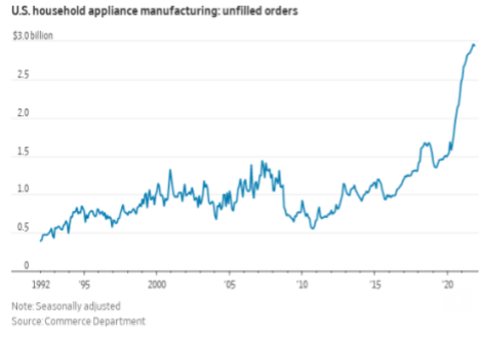

Used car prices were up 37.3% from December 2020 and New cars prices were up 11.8%. Used car prices represent 3.419% of the CPI and added 1.28% to the 7.0% increase in the CPI and New cars added 0.46%. The record increase was powered by a historic shortage of computer chips. In December the lead time for computer chips increased to 26 weeks up from 13 weeks in the fourth quarter of 2020. More worrisome was a January 25 report from the Department of Commerce that indicated inventories of computer chips were just 5 days compared to 40 days in 2019. Chips makers have already ramped up production and were operating above 90% of capacity in December. The 150 companies reported that median demand for chips was 17% higher in 2021 than in 2019 as soaring demand for smart phones, TV sets, and electric cars overwhelmed capacity. The firms surveyed don’t see chip shortages going away in the next six months. The lack of computer chips will limit how much new car production can increase, which should keep new and used car prices elevated even if they stop going up. Prices may fall but not by enough to provide meaningful relief within the CPI. The chip shortage is also slowing appliance production, delivery times, and lifting prices.

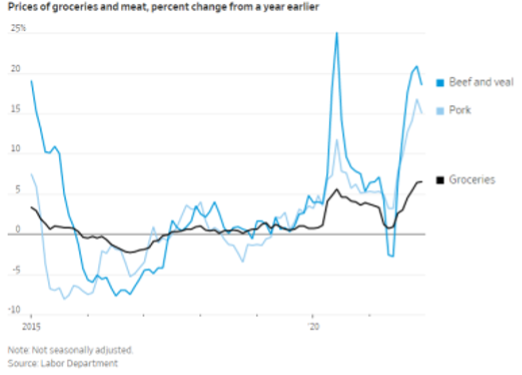

Food prices have increased significantly and probably won’t come down much as many companies are raising prices to consumers and restaurants. Food at home is 7.22% of the CPI and the cost of eating at home rose 6.5%. Eating in a restaurant or doing take out wasn’t a bargain as prices rose 6.0% the highest in 40 years. Food away from home is 6.26% of the CPI so food represents 13.48% of the CPI. Beef and pork prices were up a lot and aren’t likely to come down much as it takes time to increase supply and high fertilizer costs. Higher prices are causing consumers to substitute other foods for meats so meat prices may fall modestly as demand drops. The cost of food at home is expected to decline in 2022 but the relief will be gradual.

The categories that added the most to the CPI in 2021 will come down over the course of 2022, but are likely to fall more in the second half of 2022 than in the next six months. This may add to the impact of Reverse Base Effects in the second quarter and bring the headline CPI down more than projected.

In the decade before the pandemic, real purchases of goods in the U.S. expanded by about 3% per year. In 2020 they increased by 5% and in 2021 by an astonishing 13% funded largely by the $1.9 trillion American Rescue Plan passed in March 2021.

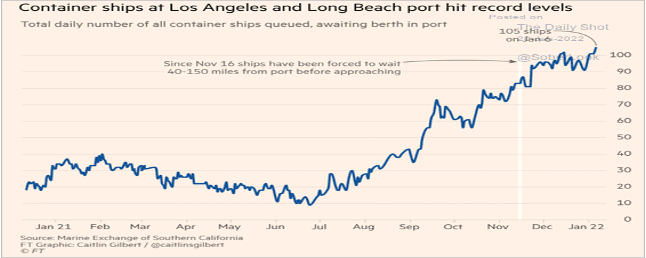

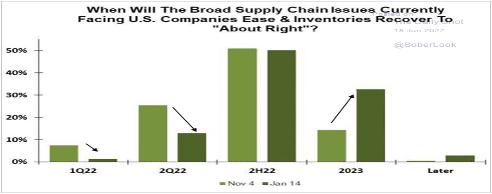

The Supply Chain didn’t fall apart until after demand for goods and products needing computer chips surged financed by government largesse. In June 2021 a combined total of 8 ships were waiting to be offloaded at the Port of Los Angeles and Long Beach. As of January 6 there were 105 ships waiting to unload. When asked when the supply chain issues will ease, CEO’s were more pessimistic on January 14 than they were on November 4. The number expecting the supply chain to improve in the first quarter was cut in half with the majority not expecting real improvement until the second half of 2022.

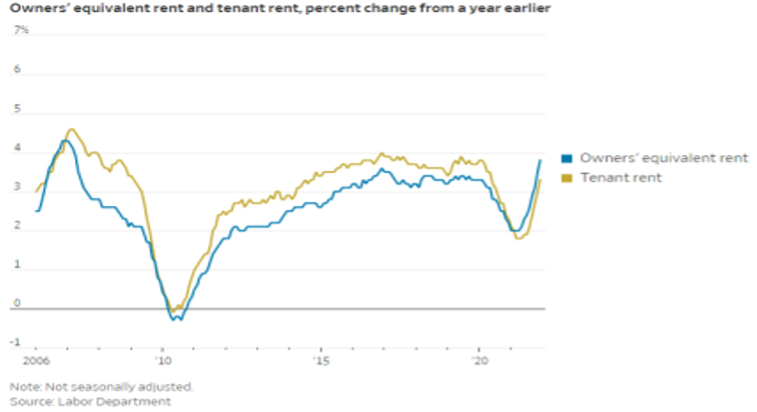

If Omicron fades as expected the amount of money spent on services is expected to accelerate as people resume more normal activities and spend less on goods. Goods comprise 19% of US GDP while services represent 77%. As this shift proceeds the price of goods is expected to come down while service inflation picks up. Higher service inflation could easily offset most of the decline in goods inflation simply based on the math. (77% vs. 19%) As I have discussed for many months Shelter comprises 33% of the CPI and the surge in home prices and rents during 2021 will continue to add to core inflation in 2022. Wage growth is the highest in a decade and high consumer demand has given companies pricing power. These are the reasons why headline inflation is expected to fall more than core inflation, but may not allow the CPI to fall enough to allow the FOMC to pause.

Federal Reserve

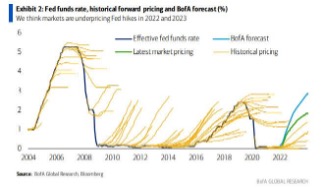

The November 2021 Macro Tides was entitled ‘Monetary Policy Can’t Fix Today’s Problems” because the FOMC can’t make computer chips, unload ships at ports, or solve the tightness in the labor market. In the January 2022 Macro Tides I suggested that financial markets were underestimating the shift in monetary policy and would experience “The Sting”. “The financial markets have taken the increase in the FOMC’s tapering from $15 billion a month to $30 billion in stride. The FOMC clearly communicated after the December FOMC meeting that it will increase the federal funds rate 3 times in 2022 and the financial markets shrugged. If inflation progresses as expected, with core inflation proving more persistent and sticky than the FOMC expects, the financial markets may experience some anxiety as the timing and number of rate hikes is reassessed by FOMC members in their speeches.” The S&P 500 had one of the biggest declines in January in its history.

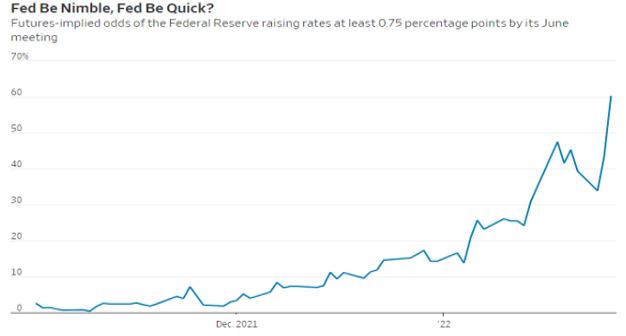

In early January the consensus was that the FOMC would increase the federal funds rate 3 times in 2022. On January 10 Goldman Sachs boldly upped its forecast to 4 hikes in 2022. On January 28 Bank of America joined the bidding war and said the FOMC would bump up the funds 7 times. In the December Macro Tides this is exactly what was expected to happen in the first quarter. “It is possible that markets will be pricing in multiple rate increases by the FOMC during the first quarter, just before inflation falls sharply. Core inflation is expected to not fall as much as headline inflation, but any meaningful decline will take a lot of heat off the FOMC.” The poor efficacy of forecasting future rate hikes based on the Federal Funds Rate Futures has been dismal. This is another example that markets don’t discount the future or know anything more than market participants.

In his press conference after the January 28 FOMC meeting Chair Powell made it clear the FOMC will remove accommodation and increase the funds rate as appropriate. “This is going to be a year in which we move steadily away from the very highly accommodative monetary policy that we put in place to deal with the economic effects of the pandemic.” Reporters asked Chair Powell if the FOMC would increase rates at consecutive meetings or by 0.50% at a meeting. As noted in the January 24 Weekly Technical Review “The FOMC will signal that the FOMC will increase the federal funds rate at the March 16 meeting. Signaling doesn’t mean the FOMC statement or Chair Powell will explicitly state that the FOMC will raise the federal funds rate but the message will be clear.” Chair Powell dodged specific details but other comments suggest the FOMC will not raise the funds rate at the gradual pace they did in 2017 and 2018 when the funds rate was raised quarterly. Chair Powell compared that period to the current environment and provided this assessment. “Inflation is running substantially above 2 percent. We still see growth substantially higher than what we estimate to be the potential growth rate. And we see a labor market where, by so many measures, it is historically tight.”

One of the primary purposes of forward guidance is to avoid upsetting the financial markets. The notion that the FOMC would raise the funds rate by 0.50% to shock and awe the markets is counter to the point of forward guidance. In order to raise the funds rate by 0.50% the FOMC would need time to prepare markets and they simply don’t have the time to do that. The FOMC used the January 26 meeting to tee up a rate increase at the March meeting. “The committee is of a mind to raise the Fed funds rate at the March meeting.” As discussed in the January 24 WTR this could be the pattern the FOMC follows at the next 3 meetings. “The FOMC would then be able to use the March meeting to prepare markets for a second increase at the May meeting, and use the May meeting to set up the third increase at the June 15 meeting.”

After getting burned last year when Chair Powell and the FOMC confidently repeated for months that inflation would be transitory, Chair Powell offered a more balanced and humble tone in his press confidence. “It isn’t possible to sit here today and tell you with any confidence what the precise path will be. Making appropriate monetary policy in this environment requires humility, recognizing that the economy evolves in unexpected ways. We’ll need to be nimble so that we can respond to the full range of plausible outcomes.” This approach allows the FOMC to shape expectations on the fly, but doesn’t rule out a series of rate increase as the FOMC assesses how much inflation falls in the second quarter, how much the economy snaps back after Omicron fades, whether some improvement in the supply chain materializes, sideline workers report for work, and if geopolitical concerns ease.

Chair Powell noted how tight the labor market is and said the FOMC could increase rates without damaging the labor market. “There’s quite a bit of room to raise interest rates without threatening the labor market.” In the January 17 WTR I pointed out why the FOMC could increase rates at the March, May, and June without hurting the economy. ““The negative impact on the economy of increasing the federal funds rate from 0% to 0.75% is low so that represents easy lifting. Increasing the federal funds rate from 0.75% to 1.50% will have progressively more drag on the economy which increases the risk of going too far with each additional hike.” More than anything the FOMC wants to avoid tipping the economy into a recession. That’s easier said than done as history shows.

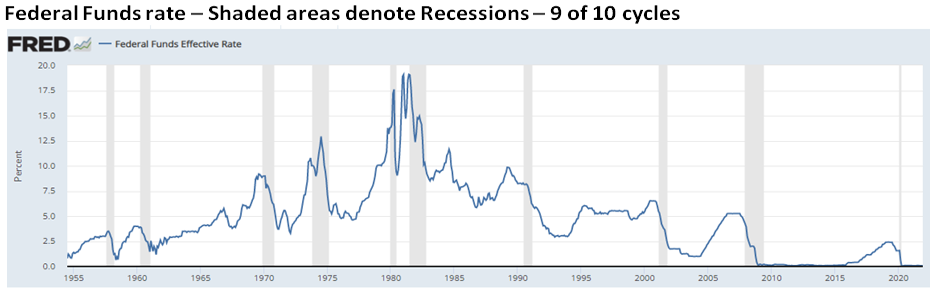

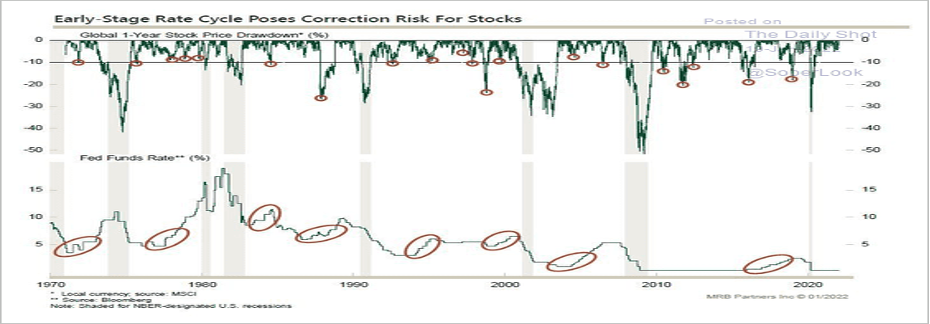

Since the mid 1950’s there have been 10 cycles in which the Federal Reserve increased the funds rate to slow economic growth and bring inflation down. In 9 of the 10 cycles since 1955 the Fed tightened too much and a recession followed. The one exception was in 1994 and early 1995 when the economy continued to grow, despite the Fed increasing the funds rate from 3.0% in January 1994 to 6.0% in May 1995. It would be fair to say that the Fed needs a bit more practice in engineering a soft landing. The FOMC will get that opportunity in 2022 but it won’t be easy. The FOMC is facing a myriad of forces that have never been seen before which doesn’t inspire confidence. Chair Powell saying the FOMC doesn’t know what the path will be is an accurate assessment.

Chair Powell did make one comment that reveals how much he wants to avoid hurting the labor market and get the results that developed in the labor market during 2018 and 2019. “We saw wages persistently higher for people at the lower end, and there were -- there really was no obvious imbalance in the economy that threatened that expansion. It could have gone on for years were it not hit by the pandemic. So, we'd love to find a way to get back to that. That's going to require price stability, and that's going to require the Fed to tighten interest rate policy and do our part in getting inflation back down to our 2 percent goal.”

I expect the FOMC to increase the funds rate by 0.25% at the March, May, and June meeting. As of January 26, and before the FOMC meeting on January 28, the odds of the policy makers raising rates by 0.25% at each of their next three meetings has increased from 45% to 60%. The key will be whether inflation falls enough during the second quarter to provide the FOMC an off ramp on immediate additional rate increases.

Stocks

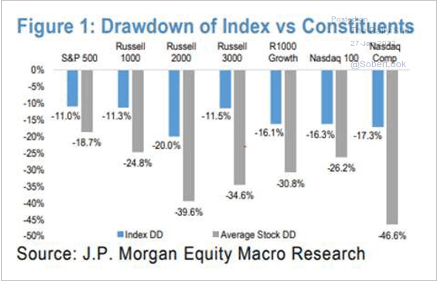

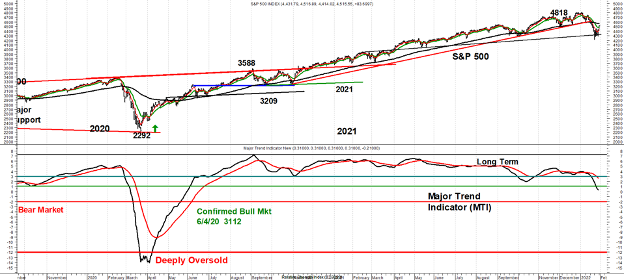

In the December Macro Tides I thought the stock market would be vulnerable to a correction based on the changing perception of monetary policy. “The stock market could be vulnerable to a correction of -10% or more in the first quarter if markets expect the FOMC to move more aggressively in the first half of 2022.” At the recent intra-day low the S&P 500 was down more than -11% but the majority of stocks had fallen much more. The average stock in the S&P 500 was off -18.7%, -26.2% for the Nasdaq 100, and a whopping -39.6% in the Russell 2000.

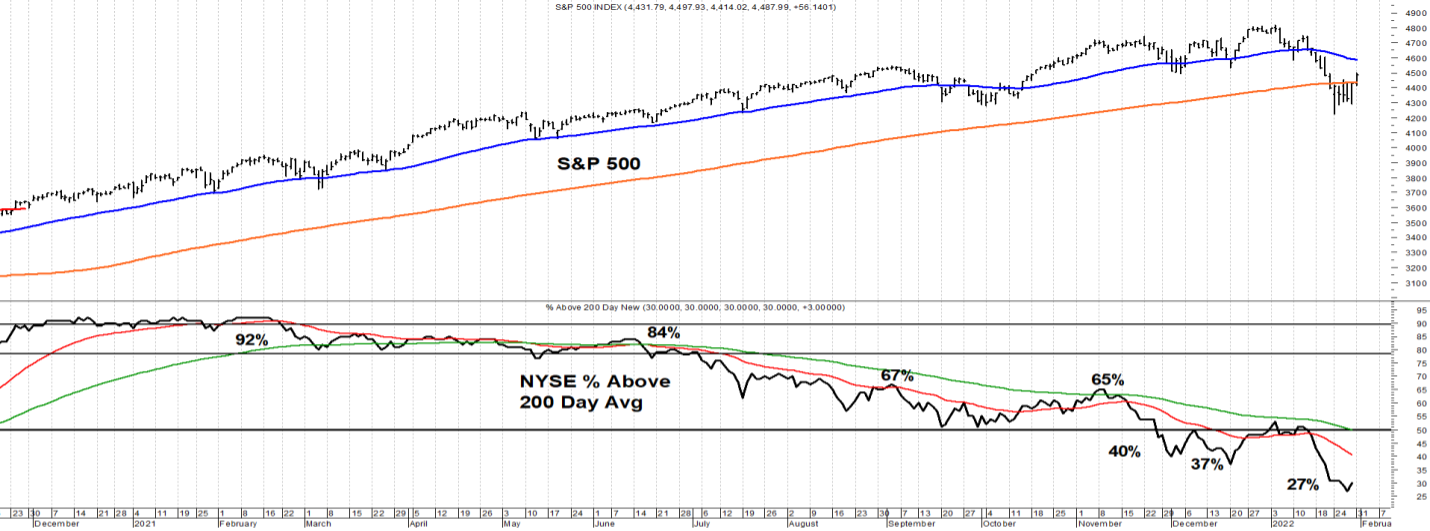

Only 27% of NYSE stocks were above their 200 day average on January 27 compared to 92% back in February 2021. The market is obviously oversold with so many stocks in bear market territory so a counter trend rally is coming. The challenge in coming weeks is that the positive news on Omicron will be somewhat offset by weaker data and hawkish speeches by member of the FOMC.

As discussed in the January 24 Weekly Technical Review the S&P 500 has experienced corrections of -10% to -20% as the FOMC lifted the federal funds rate from a cyclical low. The key point is that declines greater than -20% have been associated with recessions. There have also been ‘event’ declines of more than 20% that weren’t related to a recession. In October 1987 Portfolio insurance blew up and resulted in the S&P 500 falling by more than -30% with the market down more than -20% on October 19. Much like the 1987 Crash the Russia default crisis in 1998 was triggered by a liquidity event when a large hedge fund using 100 to 1 leverage collapsed. The Pandemic induced decline of more than -30.0% in 2020 certainly qualifies as an event bear market. Event corrections of more than -20% are usually compressed in time lasting less than 4 months and are quickly reversed. The important point was despite the large declines in 1987 and 1998 the US was in a strong position and solid growth continued. In 2020 Congress moved quickly to sustain incomes for the unemployed, liquidity and capital for small businesses, and income transfers to sustain consumer demand.

Based on the leading indicators the odds of a non event recession in 2022 is low, which should provide support for corporate earnings and the stock market. The unknown is whether inflation will run hotter than expected and compel the FOMC to continue raising rates and commence shrinking the balance sheet. There is no way to know with a high degree of certainty but the Major Trend Indicator is expected to provide guidance. Rather than go into great detail in this Macro Tides I will send a separate piece that explains how the MTI works and provides charts of market tops going back to 1937.

The current correction is bringing the MTI below the brighter green horizontal line and could push the MTI under the red horizontal line, which is a bear market warning. What has usually occurred prior to the onset of a bear market is a multi-week rally that lifts the MTI. If the MTI fails to move above the lower green line, the risk of a bear market will rise. If the MTI falls below the red line and subsequently rises back above the lower green line, the odds of a bear market will drop materially.

The S&P 500 rallied from a low of 3209 in September 2020 to the January 2022 high of 4818. The 38.2% retracement of this rally would bring the S&P 500 down to 4203, which is slightly below the January 24 low of 4223. After this correction, the S&P 500 is expected to rally above 5,000 in the second half of 2022, if inflation moderates as expected and allows the FOMC to pause raising rates. Even if Core inflation holds above 3.0% throughout 2022 which is the expectation, any moderation will provide the FOMC a window to pause.

Dollar

Positioning and sentiment often play a key role when a market is nearing an intermediate inflection point. In January 2017 speculators were aggressively long the Dollar which was one reason I thought the Dollar was nearing a peak. I turned positive on the Dollar when positioning became defensive in the first quarter of 2018, as discussed in the February 26, 2018 WTR. “Sentiment toward the Dollar is very negative and positioning in the Dollar shows a net short position, which has preceded a rally in the Dollar in recent years. By the fourth quarter of 2019 long positing in the Dollar had reached a high level as noted in the October 2019 WTR. “The positioning in the Dollar is still showing too many longs, which can provide selling pressure once the Dollar closes below 98.15.” The Pandemic caused a flight to safety which allowed the Dollar to spike higher in March 2020 which was quickly reversed. In January 2021 positioning was net short the Dollar which was expected to produce a trading low. This was discussed in the January 11, 2021 WTR. “Sentiment and positioning have been indicating that a trading low in the Dollar was approaching and the price action began to confirm a low as noted last week. “The Dollar fell to a new low today and reversed, so it’s possible it completed at least Wave 3. As noted last week, “Any new price low is likely to be accompanied by a positive divergence on the Dollar’s RSI”, which is exactly what occurred on January 4. The positive RSI divergence increases the odds that at least a decent bounce is coming soon.”

The Dollar rallied and then retested the January 2021 low in May, which was discussed in the June 7, 2021 WTR. “The big news is that the coming low may be the end of the correction that began after the Dollar peaked in January 2017 at 103.82. Wave A of the correction lasted from January 2017 until the Dollar bottomed at 88.25 in February 2018. Wave B of the correction carried the Dollar up to its high in March 2020, with Wave C now near completion. The price pattern suggests the Dollar has the potential to rally above 100.00 in the next 12 months.”

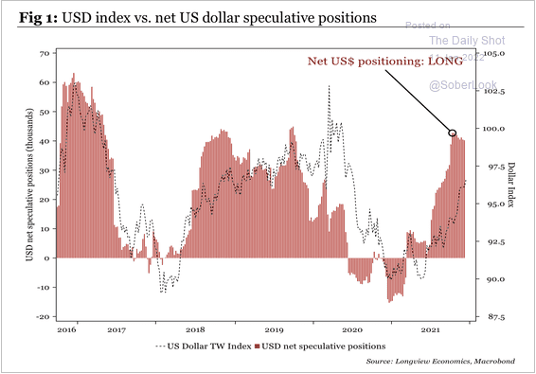

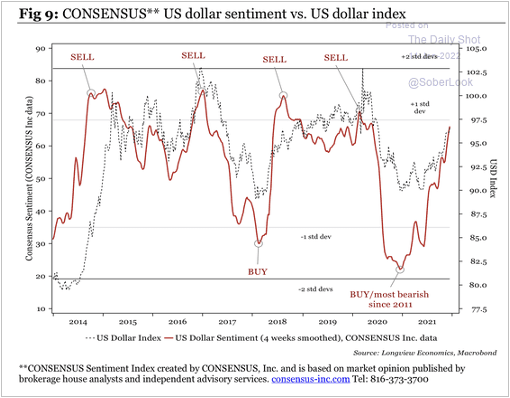

The Dollar was expected to benefit from the FOMC moving toward removing accommodation sooner and faster than the ECB. This would create a bullish tailwind for the Dollar and it did. The FOMC is now about to increase the funds rate 4 times or more in 2022 and may begin to shrink its balance sheet. For many this is why they expect the Dollar to continue to rally and the logic is compelling. Traders have bought into this logic which is why positioning is now heavily long and sentiment has become far more bullish than it was in January and June 2021. This may become another classic case of investors looking through the rear view mirror to guide their investments. (Chart compliments Consensus Inc.)

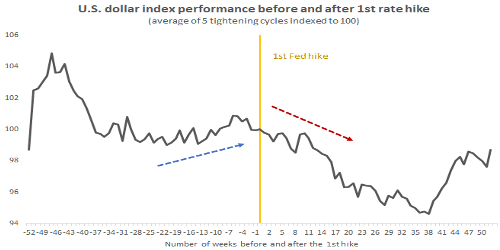

Just as the Dollar benefited from changing perceptions of monetary policy after the June FOMC meeting, the Dollar will suffer from changing perceptions of how the relative growth of the US economy will weaken as the FOMC increases the funds rate, while the ECB maintains it extreme monetary accommodation. In the prior 5 tightening cycles going back to the late 1970s, the Dollar has actually declined for 9 months after the first rate hike. How’s that for logic!

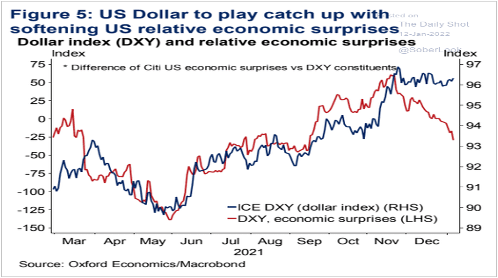

In 2021 the correlation between the Dollar and the Citi US Economic Surprise Index was high. The Index fell through May and then turned higher as did the Dollar. Since mid November the Economic Surprise Index has been falling but the Dollar recorded a higher high on January 28. The gap between the Surprise Index and the Dollar is expected to close as the Dollar declines. The Surprise Index is expected to decline more as data for January proves to be weaker than estimates, which could put pressure on the Dollar.

As forecast in the January 24 WTR, the Dollar was expected to rally above the November 24, 2021 high of 96.94 and reach 97.50 – 97.75. On January 28 the Dollar traded up to 97.44 and then dropped by more than 1%. The decline in the Dollar may be fairly shallow in the next few months, as FOMC members give hawkish speeches in February. This will likely keep the buyers driven by logic positive. A pullback to 94.50 or lower is expected in coming months.

Emerging Markets

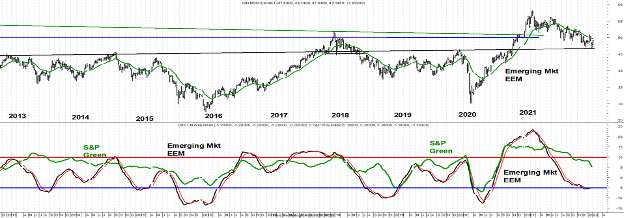

Emerging Markets’ (EEM) daily Relative Strength (RS) to the S&P 500 improved in January. For the first time since February 2021 the RS moved above its green moving average. The improvement in the daily RS has enabled the weekly RS to show more signs of bottoming. This suggests that adding to the initial position in EEM on weakness is warranted. In the December Macro Tides investors were advised to establish a 33% position in EEM if the traded below $47.25 which it did on December 20. Investors can increase the position from 33% to 66% if EEM trades below $48.50, or if EEM closes above $50.00. For an explanation of the weekly Relative Strength chart, please refer to the January Macro Tides.

Gold

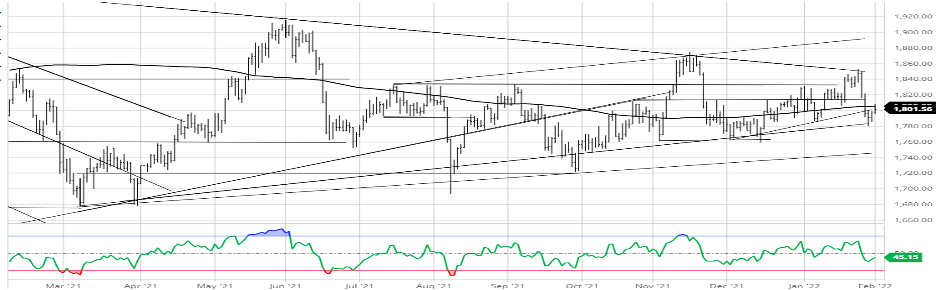

Gold was expected to test the down trend line at $1855, which it did, and then reversed lower. As discussed in the January 31 Weekly Technical Review, Gold remains in a triangle but there are concerns. “Gold has essentially been trading in a large triangle since bottoming in March 2021 and it tested the higher trend line when it traded down to $1780.75 on January 28. Gold would fall to the lower trend line just above $1740 if it closes below $1780. Until Gold closes above $1850 the downside risk must be respected as the FOMC members talk tough in coming weeks.”

Gold

Stocks

The stock market became extremely oversold and sentiment turned bearish in late January, which normally supports a multi-week rally. The expectation is that the S&P 500 will eventually decline below the January 24 low at 4223 after a bit more upside. This was discussed in the January 31 WTR. “It’s possible that the January 24 low represents Wave A of a larger correction. The S&P 500 could experience a choppy Wave B rally that would ultimately lift the S&P 500 to 4600 – 4650. Wave a of this rally would lift the S&P 500 up towards 4550 - 4600 that would be followed by a 3 wave decline down to 4350 – 4400 for wave b. Wave c would then carry the S&P 500 up to 4600 – 4650 for wave c of B. This rally would consume 1-2 weeks which would alleviate the oversold condition, allow sentiment to become far less bearish, and set up the next 595 point drop for Wave C. (4818 – 4223 = 595 Wave A) A drop to 4000 – 4100 would then complete the correction probably before the next FOMC meeting on March 16. The S&P 500 could also drop below 4223 and then begin the Wave B rally or the rally to new highs. This is why buying below 4223 is prudent as both patterns suggest a solid rally should follow.”

After a weak first quarter due to Omicron, the economy is expected to rebound, which is why a rally to a new all time high is expected in the second half of 2022.

The Daily Shot

Every month I include dozens of charts and the majority of them come from The Daily Shot. I highly recommend those who like charts of economic data to subscribe to The Daily shot.

Jim Welsh

@JimWelshMacro

[email protected], MacroTides.com

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All