The worst foreign policy fears came true this week as Russia attacked Ukraine, the biggest aggression by one nation against another in Europe since World War Two. The conflict could have significant geopolitical and humanitarian outcomes, but is unlikely to materially alter the economic outlook for the world. Unsurprisingly, concerns about the ongoing impacts of the conflict led to increased volatility, which could be the start of an enduring shift in risk sentiment.

We will closely monitor the evolving situation, especially as sanctions take shape. We do not believe the incursion will change the outlook for central banks; the news will only reinforce the cautious approach the European Central Bank was already taking.

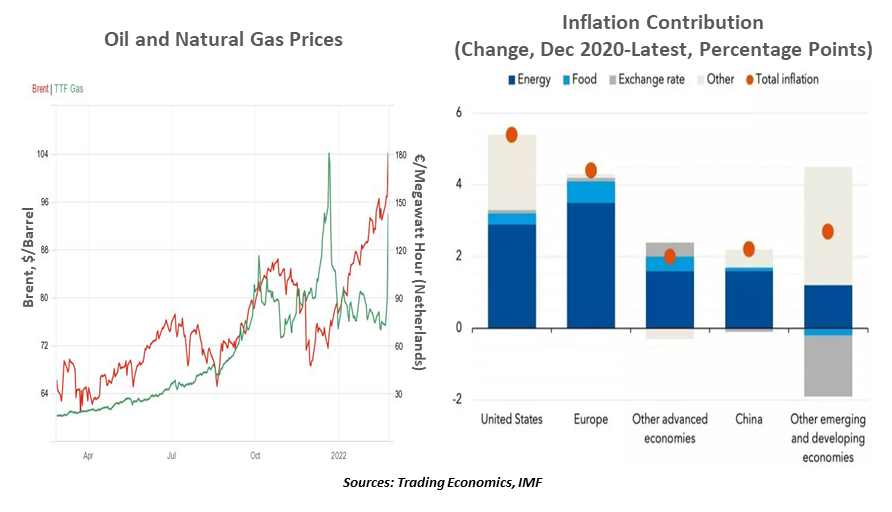

The main channel of transmission will be the commodities market. Moscow is a major exporter of energy and food, and Kyiv is an important source of crops like wheat and barley for Europe. Russia is not only the second biggest exporter of oil, but also the world's top natural gas and wheat exporter. As a result, fossil fuel prices soared. The spot price of European gas jumped 50% on the day of the attack, while Brent moved above $105 a barrel for the first time since 2014.

While higher natural gas prices will be concentrated in Europe, oil shocks will impact all nations. Crude prices were already on the rise this year. Demand has outstripped supply as more economies reopened and factories increased production. The return of services like travel is further boosting demand. According to the International Energy Agency (IEA), global oil supply is at least one million barrels per day below demand.

Supply-side dynamics have been equally responsible for surging energy costs, an issue that cannot be fixed easily. The impact of prolonged demand uncertainty due to COVID-19 during its initial phase forced producers to tighten output. Amid the global energy transition, tighter regulations have led to lower investments in fossil fuels and oilfields in recent years, leading to the IEA backtracking from calls for the immediate suspension of all investments in production of these commodities. Earlier this month, the U.S. administration halted new oil and gas drilling leases. Weather has also been a disruptor. Hurricane Ida-related outages badly hit supply in the U.S. last August, offsetting the increased production by the Organization of the Petroleum Exporting Countries and its allies.

Oil remains one of the most important commodities in the world. It accounts for about 3% of gross domestic product and is more than just a fuel, with uses in products ranging from personal protective equipment to plastics to fabrics and even solar panels. While high oil prices are a boon to producers, they present a challenge for importers who will face higher inflation, slower growth and worse external account deficits.

|

The conflict adds upward pressure to energy prices that were already elevated.

|

In advanced economies, oil is not the biggest factor in inflation indices. The energy component, generally, accounts for up to 10% of the consumer price basket, but large swings in prices can nonetheless make significant contributions to overall inflation. For instance, a 10% increase in oil prices in euro terms leads to a 25bps rise in headline inflation in the eurozone.

On the other hand, emerging markets’ greater sensitivity to oil prices is a key factor in their monetary policy considerations. A $10 increase in oil prices adds as much as 60bps to inflation in Asian economies like India, Philippines and Malaysia. Higher prices, if sustained, can also have indirect effects on core items, transmitted through production costs or travel-related services.

Another spike in energy and food costs is the last thing that central banks and consumers would have wished for. Rising prices could further squeeze consumer incomes. And the longer inflation stays above target, the higher the chances of seeing a wage-price spiral.

The world’s immediate attention is on the attack and countermeasures like economic sanctions. The Russian economy will be targeted, but the consequences of this week’s developments will be felt worldwide. Energy costs will be the first to show stress. The sooner the conflict can be contained, the better the outcome will be for everyone.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions

© Northern Trust

Read more commentaries by Northern Trust