Other Possibilities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGentle or Aggressive

Energy Assumptions

“The Outlook Is Deflationary”

What Is the Market Expecting?

Where the Wild Risks Are

Power, Bird Flu, and the SIC

An old Danish proverb, later attributed to everyone from Mark Twain to Nostradamus to Yogi Berra, says, “Predictions are difficult, especially about the future.” I would refine it a little: Predictions are actually pretty easy. Accurate predictions are very difficult.

We can never know the future because it’s not here yet. We can only make educated forecasts and sometimes even the best are wrong. Yet the forecasting process has great value. It helps us think through the possibilities and how we can react if necessary.

Right now, my economic forecast is we are entering an inflationary recession or “stagflation” period. I believe it will result in a bear market, as all recessions do. I’ve shown you a lot of evidence in recent weeks. I’m still reasonably confident in that outlook… but I also have to consider other possibilities.

Today we’ll consider the risks to my stagflation forecast. Note that’s different from the risks of my forecast, should it prove accurate. I’ve described those already but it’s important to ask how I might be wrong.

As you’ll see, the other possibilities aren’t appreciably better. They’re just bad in different ways. Well, except for the soft landing scenario to which I give a vanishingly small possibility.

This entire letter needs to be put into context. The Federal Reserve has created the problem it is now trying to resolve. Ben Bernanke explicitly engineered QE2 and QE3 to increase stock market valuations. Not a speculation on my part; we have quotes and names and times. I wrote at the time that it was ironic how the very people who dismissed Ronald Reagan’s “trickle-down economics” were all on board for a “trickle-down money supply.”

To be sure, it worked. QE plus low rates clearly juiced the stock market. Powell used the same playbook in 2020 to help the stock market reverse its free fall. I think that was actually legitimate, as well as QE1. The problem was continuing QE well past its sell-by date, and keeping rates at zero far too long. Powell created the conditions for the inflation that he is now fighting, aided by massive fiscal stimulus.

Since I believe the economy and American businesses can handle 2% interest rates, and it will take us some time to get there, I think the quantitative tightening is the tool to watch. Clearly QE juiced the stock market. What makes us think reversing it won’t have the opposite effect? This is a part of the future we will find out.

Gentle or Aggressive

Let’s start by reviewing what we know. We know inflation has been climbing to the highest level since the 1970s, and is really even higher since the benchmarks understate housing prices. The unemployment rate is almost back to its pre-COVID level. The economy has many more job openings than available workers, with strong wage growth as a result. These are the “flation” parts of stagflation.

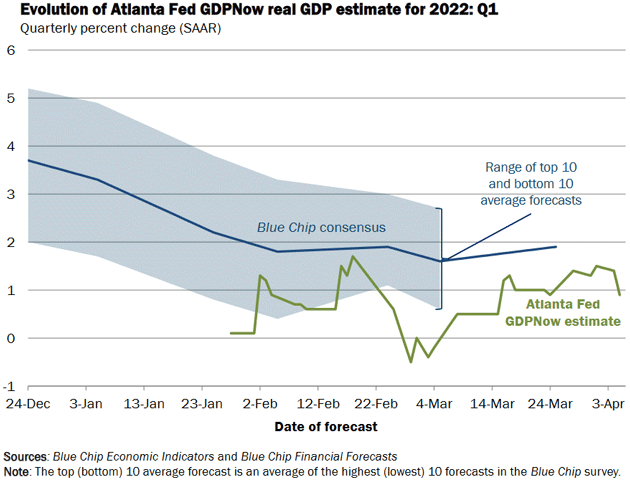

As for the stag, we’ll get the official estimate for Q1 GDP on April 28. The Atlanta Fed’s GDPNow model estimated (as of April 5) it will be 0.9%. The blue-chip consensus of human economists is closer to 2%. Anywhere in that range would be about average for the post-2008 era. So far, at least, we don’t see a giant hit to GDP growth.

Source: Atlanta Fed

Let’s note, however, the 1.5 to 2% range where GDP stayed for years after the 2008 recession wasn’t historically impressive. We saw much higher numbers after the COVID recession, but they now appear to be ending. If flat growth + high inflation = stagflation, then it looks like we’re almost there.

The optimistic scenario is the economy stabilizes in something like the current condition. Higher consumer prices will hurt, but people will have jobs and stay afloat. Inflation will gradually moderate as the Fed tightens and energy markets adapt to Russia sanctions.

Those two factors—the Fed and energy prices—are really the main variables, so let’s consider them more closely.

Interest rates are traditionally the Fed’s main inflation-fighting tool. It controls the overnight lending rates that dictate bank liquidity and lending. By raising them it can make borrowing more expensive, discouraging the economic activity that produces inflation. That’s the theory, at least. And it’s worked well in the past, though not quickly.

Further, we are starting from essentially 0%. I don’t think a 1% Fed funds rate will inhibit growth or discourage borrowing. The interest rate portion of their inflation-fighting toolbox is going to have to be a lot higher than 2%.

More recently, the Fed’s balance sheet has been an important tool. It uses excess bank reserves to buy and hold bonds, thereby reducing interest rates and, in theory, stimulating growth. It works the other way, too. When the Fed stops buying bonds or, God forbid (note sarcasm), actually sells some of its holdings, rates go up. This is happening right now as the Fed reduces its QE purchases. Lael Brainard said last week the Fed could begin “rapid” balance sheet reduction as soon as May.

We can see from the Fed minutes released this week that the “plan” is to sell $60 billion worth of government bonds along with $35 billion worth of mortgages. In talking with Barry Habib, he thinks the buying the Fed will do in mortgages from their run-off (they get interest, etc.) will just about balance their sales, so the mortgage market may not be as affected as one would think. That means that Federal Reserve economists are actually paying attention. That would also suggest that $35 billion is not a random number.

Mortgages won’t simply roll off the balance sheet like Treasury bonds. The Fed could actually face capital losses if it sells them outright. But in an economy where most major business decisions aren’t capital-constrained, their interest rate tools will have to focus on highly leveraged segments. Few are more leveraged than housing.

If I were on the FOMC, I would recognize we can’t do much about energy or food prices. Selling the Treasury holdings and raising interest rates will simply impose higher costs on government borrowing. I wouldn’t like having to suppress the housing sector because it accounts for a lot of jobs. But we have to stop inflation and these are the best knobs we can turn.

It matters whether they do this gently or aggressively, of course. I expect they’ll spend a few quarters trying to generate a soft landing. The Fed minutes suggested they are thinking of one or more 50-basis-point hikes. I would suggest that a 50-basis-point hike is not all that aggressive given the context of 8% inflation.

The Fed’s problem, though, is this drama has other characters who can work for or against the Fed’s goals. And if they give the Fed too much help, growth could fall a lot faster than most now think.

Energy Assumptions

We started out talking about risks to my forecast. There are basically three possible outcomes.

-

The Fed tightens just enough to squelch inflation and maintain GDP growth.

-

The Fed doesn’t do enough and inflation gets worse, or doesn’t come down as fast as the market or anyone else would like.

-

The Fed (eventually?) does too much and we swing from high inflation to recession. Remember, recessions are by definition deflationary. They are accompanied by demand destruction.

We can hope for #1, but it’s a (very) long shot.

I think #2 is most likely. Jerome Powell will act (and already is), but he isn’t Paul Volcker, nor does he need to be. The Powell Fed can go slower, hoping for that soft landing.

That leaves #3 as the main way I could be wrong. How would that work?

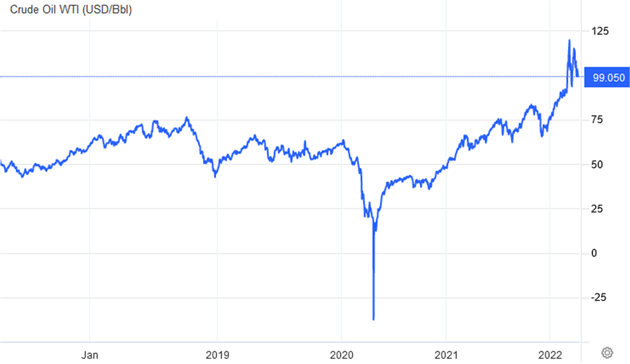

One way is if “something else” occurs to relieve inflation, on top of whatever the Fed does. The current inflation is largely (though not entirely) a function of supply chain problems and energy prices, plus housing prices. And not just the recent sanctions, but other events dating back to last summer and fall. Last fall crude oil broke out to its highest price since 2014, pushing CPI and other inflation benchmarks (which were already rising) up to scarier levels.

Source: Trading Economics

Other and better energy sources are coming, but prices over the next year or so are the immediate concern. Like everything else, energy prices are the intersection of supply and demand. Some combination of additional supply and lower demand could push them lower.

Frankly, the odds of significantly higher supply are quite low in the near term. Given the latest atrocities, the Russia sanctions aren’t going away. Loss of Western parts and expertise may further reduce Russian output as this drags on. OPEC shows no willingness to help.

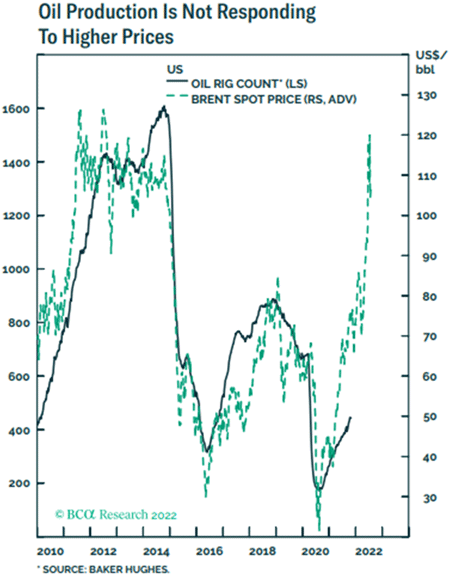

US oil and gas producers might be able to increase output, especially if they got some regulatory relief, but the Dallas Fed’s latest survey shows they don’t plan to do it. Having been burned by the boom/bust cycle too many times, shareholders don’t want more capex. They also cite serious shortages of the sand, pipes, and other materials needed for any new drilling. In fact, oil producers are not responding by putting drilling rigs to work. This chart from BCA suggests that the cavalry in the form of the US energy complex has not yet moved out of the fort to save us.

Source: BCA Research

All that sounds pretty bleak. How could it be wrong?

For one, we are making big assumptions about Russian exports. China, India, and some other large customers say they will keep buying. Putin is offering them discounts to do so. Oil is fungible, so this will have a (potentially) bearish effect on prices worldwide. How much, we don’t know. It could be more than presently expected.

On the demand side, high prices will have an effect. The question is how much. A lot of it is incremental: People adjust the thermostat a few degrees, drive a little less, etc. These small changes add up. In Europe the changes may be bigger and less optional, should more governments decide to stop importing Russian gas. A severe recession in Europe, while problematic, might reduce energy demand enough to affect prices globally. A US recession would likely trigger a global recession, reducing oil demand and prices.

Other things may happen. The point is that our base assumption of continued high energy prices could prove wrong. If so, and if that happens on top of Fed tightening and a housing downturn, inflation could drop farther and faster than presently anticipated.

Then what?

“The Outlook Is Deflationary”

Last week I mentioned Dave Rosenberg and a few others think we may be talking about deflation soon. That is so out-of-the-box right now, I feel I should explain more. I’ll do that by quoting Dave himself, from his March 31 letter.

“To little fanfare, the U.S. Federal Reserve lowered its estimates of the natural rate of interest and potential GDP growth in March. Those tweaks have significance, not because they reflect the true economic situation, but because of what they represent, namely a Fed trying to build a case for aggressive interest rate hikes to assuage political pressure. Potential real GDP growth is much higher than what the Fed is suggesting, meaning that there is more slack in the economy than what is being portrayed in Fed projections. For contrarian investors, that translates to preparing for a U.S. outlook that is deflationary rather than inflationary, and one that involves fewer rate hikes than what is being priced in by OIS markets—a strategy that will become more enticing as price-boosting impacts of supply chain bottlenecks and labor shortages fade…

“[T]he reality is that upcoming fiscal drag (which barely gets a mention from the Fed), the impact of declining real incomes on consumption, and an inverting yield curve, are all pointing to a sharp moderation in U.S. real GDP growth this year to below potential growth, which translates to diminishing price pressures ahead. In other words, a moderation of inflation is coming, regardless of Fed rate hikes.

“The Fed’s downgrades of the natural rate of interest and potential growth have to be taken with a grain of salt. Rather than reflecting reality, those tweaks were meant to paint a rosy picture of the economy (particularly the labor market) and to warrant aggressive interest rate increases to bring down inflation. Potential real GDP growth is in fact much higher than what the Fed is suggesting, meaning there’s more slack in the economy than what is being portrayed in its projections. In other words, the outlook is deflationary rather than inflationary, something that will become more apparent as supply chain problems and labor shortages that are now artificially boosting prices eventually fade.”

Unlike me, Dave has not turned in his Team Transitory t-shirt. He’s doggedly maintained the inflation, while real, will pass soon. The reason is because the “growth” we’ve seen wasn’t really growth; it came mainly from monetary policy and fiscal stimulus whose effects are fading quickly. Likewise, the present inflation comes from transitory supply chain and labor shortages.

If the economy has as much hidden slack as Dave thinks, it’s quite possible the combination of a tighter Fed and inflation expectations will bring down wages, raise unemployment, and tip the economy into a more traditional recession, instead of a stagflationary one. As Rosie said again this Friday morning:

“Inflation will come down, but that is because of what the Fed is going to do with demand, and a ‘soft landing’ is not going to be sufficient to deal with this sort of supply dynamic.

“Has anyone noticed that the peak in inflation invariably occurs in the context of an economic recession (or quickly heading into one)?”

Again, that’s not what I expect but Dave has been doing this a long time and is usually right. I take him seriously. You should, too, particularly if you’re buying inflation hedges. You may need to lift those hedges sooner than expected.

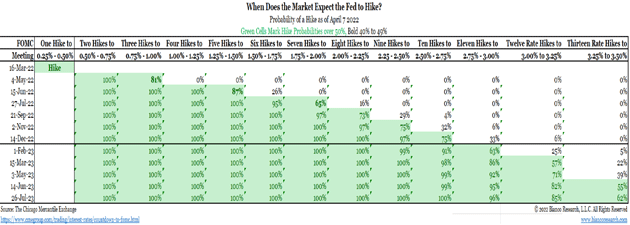

What Is the Market Fxpecting?

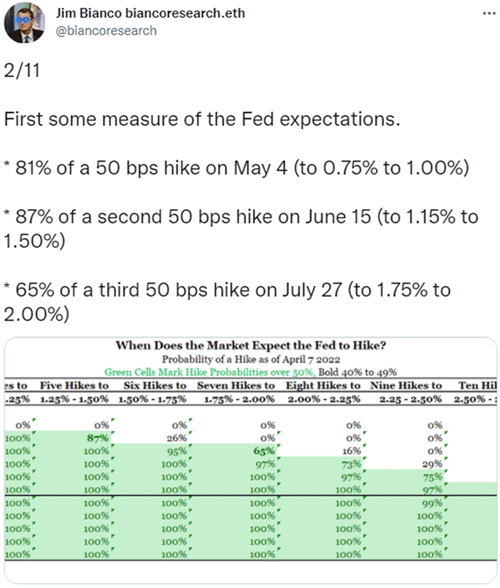

Jim Bianco creates some of the best threads on Twitter. I want to highlight this thread on market expectations as to what the Federal Reserve will do. (By the way, you should be following both Jim and me on Twitter.)

First, the bond market has priced in a 100% chance of a 0.25% increase and an 81% chance of a 0.5% increase. Oddly, as Jim notes, the market expects them to get more aggressive in June.

Source: Bianco Research

I have expanded his chart for you to explore at your leisure. The market is currently pricing in a 75% chance of nine rate hikes that would bring Fed Funds to somewhere between 2.5% and 2.75% by the end of the year!

Source: Bianco Research (Click to enlarge)

The idea that the Fed would hike 50 basis points at every meeting going forward was literally zero percent a month ago. Tough talk from Fed officials along with the March FOMC minutes changed everything. When Lael Brainard starts talking tough on inflation, you know things have changed.

Read their speeches. They are beginning to acknowledge that a tough stance will weaken growth. Quoting Jim: “Again, growth is no longer the priority, inflation is.”

Where the Wild Risks Are

Starting with Greenspan clearly boosting the housing market in the early part of the century, Bernanke/Yellen’s QE, compounded by Powell expanding QE and keeping 0% rates far too long, the Fed has created what Nassim Taleb would call a “fragile” market. By propping up financial institutions and asset prices, the Fed has pushed risk off into the future.

Note, they didn’t reduce risk; they simply moved it to a different place and let it compound. Rather than allow small, manageable fires, they have let fuel accumulate for a large fire. And then we will ask the arsonist to come in and put out the fire.

The coming volatile period is a direct result of Federal Reserve intervention in the workings of the market. They have now come to the place where they have to either let the fire of inflation (and a likely inflationary recession) or the fire of a recession and bear markets to erupt. Prior choices mean they have no good choices now.

I know there will be those who think current stock prices are the result of earnings growth and normal market forces, and the bull market will continue for a long time. I believe a correction in both the inflationary cycle and the market cycle is far more likely. I also believe this recession and bear market will give us an extraordinary generational buying opportunity. After the dust settles, the bull market can once again resume, hopefully without quantitative easing or other distortions. Technology, which is getting spanked almost every week, will once again become the darling of the 2020s. Stay tuned.

Power, Bird Flu, and the SIC

Still no travel planned until August and I am getting antsy. Not quite island fever, but getting there.

I can hear a low hum from diesel generators in our neighborhood. Puerto Rico’s grid went off this week due to a large fire at one of the power plants. It’s slowly coming back but not here yet.

You are beginning to get invitations for the Strategic Investment Conference. This year is going to be awesome. The faculty is the best we have ever had, with a mix of new and old faces. I have been listening to some of the experts on Ukraine and NATO we have lined up. What I hear is sobering, but it’s reality you need to hear. You really want to participate. With our virtual format you can watch the videos at your leisure, read the transcripts, or listen to podcasts. It will be every other day for five days beginning May 2. Don’t procrastinate. Sign up now.

Finally, in the when it rains, it pours category, bird flu has caused chicken farmers to have to put down over 23 million chickens so far, driving up the cost of chicken and eggs. Analysts note that bird flu season is normally kicked off by migrating ducks and geese, which has just started, so it is very likely to get worse. Sigh.

With that let me hit the send button. You have a great week and start looking for those bargains in the future! And follow me on Twitter!

Your ready for some bargain shopping analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All