The first quarter was a turbulent one. Persistently high inflation prodded the Fed to get much more hawkish on monetary policy and the invasion of Ukraine by Russia threw commodities markets into turmoil.

It was also a punishing quarter for many investors. Stocks swooned and rebounded but still ended down for the quarter. Bonds were brutalized with one of the worst quarters ever. As such, it was also one of the few occasions for which balanced fund investors were not cushioned from the blows. The big question now is, was this just a blip or was it the beginning of a new and more hostile investment landscape?

Are we living in a dream world?

Despite all of the turmoil in the quarter, the S&P 500 finished down just 6% from its all-time high, though it had been almost 14% at one point. Such resilience in light of fairly substantial headwinds cast a surreal complexion over the landscape. Robert Armstrong captured the contradictions in the FT's "Unhedged" newsletter:

Inflation is scalding, and the Fed is vigilant. We are flirting with an inverted yield curve. And yet markets, judging by the Fed funds futures curve, stock prices, and other indicators, are saying we will glide through the next few years without the US central bank needing to raise rates to even 3 per cent, and without falling into recession.

He wonders, “Are we living in a dream world?” and then goes on to describe, “It is a weird form of cognitive dissonance: to talk as though you recognise the headwinds and not price them in. Hoping, perhaps, that they will not, after all, materialise.”

A similar weird form of cognitive dissonance occurred last fall. With CPI prints coming in at high single digit levels and the Fed refusing to even tap on the monetary brakes, long-term interest rates nonetheless remained relatively insulated from such concerns, hovering around 1.5%. I addressed this issue in a market review in January. In hindsight, bond investors really were living in a dream world.

The weird form of cognitive dissonance also infected the geopolitical realm. Few people expected Putin to actually invade Ukraine, including many with business relations in Ukraine and Russia. With so many people so substantially failing to adequately account for identifiable risks, it begs the question, "Why?"

The great risk recalculation

Edward Alden's thesis, which he expressed at Foreign Policy, amounts to "a great risk recalculation". His report quotes Barry Lynn, executive director of the Open Markets Institute, who described, "corporations have built the most efficient system of production the world has ever seen, perfectly calibrated to a world in which nothing bad ever happens.”

In short, bad things are starting to happen and corporations need to recalibrate. Alden concludes, “A sober calculation of risks and rewards is just what is needed now.” We are in an environment with greater uncertainty and therefore we need to plan accordingly.

Of course, it is not just corporations to whom this new reality applies, but also to investors and everyone else. Investors, in particular, have long relied on central banks to make sure "nothing bad ever happens". For the vast majority of the last thirteen years, that has been true.

Now, with persistently high inflation and supply shortages exacerbated by the war in Ukraine, central banks no longer have the luxury of serving as the market's protector. As a result, investors need to plan for the possibility of bad things happening like they have not been doing for many years.

Breakdown

An excellent example to which to apply this insight is the yield curve. Short rates started increasing around the beginning of the new year and re-accelerated after Jerome Powell testified to Congress in early March. With long rates not moving nearly as much, the yield curve flattened substantially.

The common interpretation of an inverted yield curve is that a recession is on the way. Higher rates on the short end tighten financial conditions - which slows down business activity. Relatively low rates on the long end confirm growth will remain weak.

Negative economic growth isn't the only bad thing that can happen though. Jim Bianco provides a more generalized assessment of the curve. As he mentioned on Twitter, flattening yield curves “are signaling the huge number of rate hikes will break something in markets, the economy, and/or the financial plumbing (repo)”. It could be the economy that breaks, but it could be something else too.

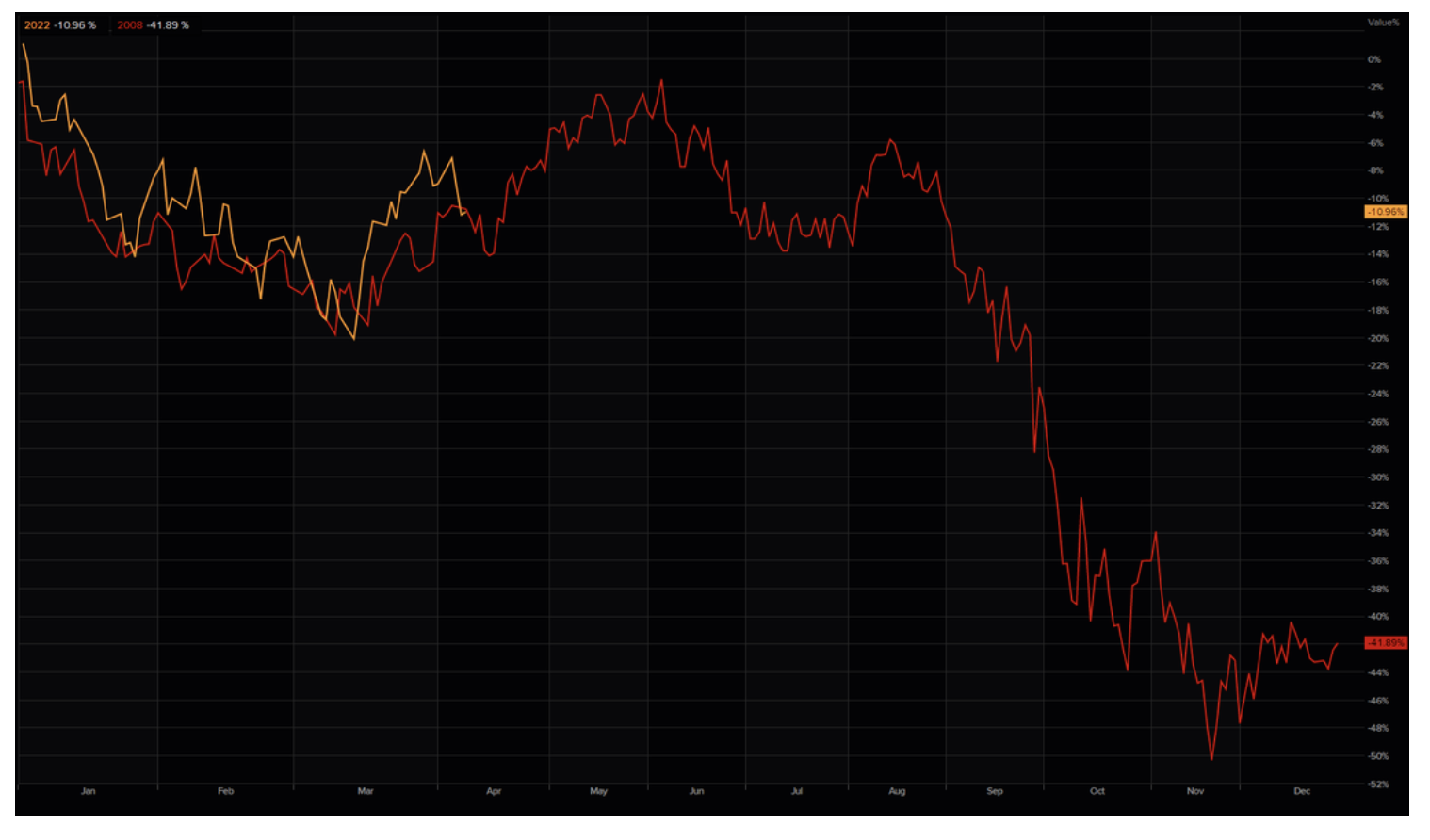

Insofar as a significant flattening portends trouble is on the way, it prompts exactly the kinds of "sober calculation of risks" that Alden endorses. To that point, one possible risk is a crash in the stock market. Given crashes in 2000, 2008 and 2020, these violent incidents are still very much in the minds of many investors. In addition, as The Market Ear (themarketear.com) shows, the analogy of the current market with that of 2008 is unsettlingly similar.

A big market crash like that of 2008 is not the only possibility, however. Significant, regular flows into stocks by way of target date and other passive funds provide a formidable bid for stocks regardless of price or fundamentals. These flows provide a meaningful obstacle to a big selloff. That doesn't mean one can't happen, but it would take a huge mass of discretionary outflows to overwhelm the automatic inflows to passive funds.

Another reason why stocks might not crash is because the Fed might step in to prevent it. Just as the Fed has done many times in the past, it may quickly revert to turning the QE faucets back on at the first sign of "breakage". There is no stipulation, however, that the Fed react as quickly as it has in the past or as forcefully.

Indeed, it is quite fair to say the Fed's outward demeanor has changed given recent comments coming out of the Fed (namely by Lael Brainard and James Bullard). Based on those comments, it is also fair to assume its reaction function has changed. In short, if/when something breaks in the future, it is reasonable to expect the Fed to do something less than the "everything but the kitchen sink" policy it deployed in response to the pandemic.

It's not hard to imagine that a different playbook would be far more selective and more focused on whatever particular "breakage" transpires. It could be conditional - only lasting for a short period. It could be varied - perhaps involving some securities purchases to provide liquidity but maintaining the same interest rate policy. It may, or may not, include longer-term forecasts about policy. In short, there is a huge spectrum of possible remedial actions the Fed could take that fall far short of the post-pandemic QE program.

Let's try out yet another scenario for size. Imagine the Fed does what it says and keeps hiking rates and starts reducing its balance sheet. Treasury yields keep rising. The value of bonds keeps falling. Pension funds, which must allocate between stocks and bonds, must keep increasing allocations to bonds to maintain a fixed balance. Those funds must come from somewhere - so they come from stock sales. In a scenario like this, stocks don't come crashing down, but rather ratchet down as pension funds continually rebalance to maintain their targeted weight of bonds.

Yet another scenario has credit leading the way down. As Grant's Interest Rate Observer rightly observes, "Highly leveraged companies do best with low economic volatility". With higher rates and greater volatility, highly leveraged companies become less profitable and have a harder time rolling over debt. Perhaps the path for stocks is a slow, grinding game of economic attrition. Less dramatic, but just as effective.

Finally, stocks are not the only things that can break. As Zoltan Pozsar makes clear in a recent piece, currency systems matter - but so too do real, commodity systems. As highlighted by the war in Ukraine, conflict and sanctions can massively disrupt the logistics of delivering real commodities. Disruptions mean longer trade routes, greater financing needs, and more uncertainty in general. All these things add to commodity costs on top of higher prices caused by supply shortages. Pozsar deliberately highlights the potential for trouble in commodities markets by stating, "Sudden stops are about to get a new meaning".

Implications

So, the short answer to the question is "Yes", we are in a new and more hostile investment landscape. After being conditioned for years to ignore risk, the emergence of inflation and geopolitical conflict changes the game. No longer do central banks have the flexibility to save the day whenever something bad happens. We all need to recalibrate to this new environment and manage risk more actively.

Another point is that risk is not just a binary phenomenon. There isn't just no risk or big risk; this is too simple a characterization. Risk can come in the form of a single, big destabilizing event, but it can also come in the form of a long grind of tougher conditions. Risk mitigation efforts for these conditions are different and obviously also more costly if employed as a combined package.

More generally, the greatest risk is that of uncertainty - not even knowing what might happen, let alone knowing the probabilities. Earlier this year, not a lot of people had Russia invading Ukraine on their bingo card. A bewildering array of potential outcomes could spawn from that one event alone. Uncertainty, by its very nature, is hard to insure against. As a result, the most sensible response is to reduce exposure to risk altogether.

Conclusion

Investors have endured a number of bouts of turmoil since the financial crisis and each time it made the most sense to ride it out. It's no wonder that many attitudes toward risk are so dismissive.

This time, however, there are good reasons to believe that a risk recalculation is needed instead. There is also good evidence to support that view. While liquidity conditions are likely to be good for the next few weeks due to seasonal tax receipts, long-term investors should view that more as an opportunity to reduce risk than to add to it. Those who continue "living in a dream world" are likely to awaken to a nightmare.

© Arete Asset Management

Read more commentaries by Arete Asset Management