What Are GARP Stocks & Why Focus on them Now?

- Our last missive on Advisor Perspectives explained why swapping out SMID Growth for SMID Value could help build a margin of safety into client portfolios

- This post explains why we believe GARP Investing may be another powerful way to protect and grow capital amid a speculative frenzy that appears to be on its way out

- We believe buying cheap, high-quality stocks that are growing profits faster than the index has never been more appealing than it is today

For the purposes of this paper, we will use KCR’s GARP Portfolio for illustrative purposes. We believe the opportunity vs. the benchmark is so vast that almost any GARP methodology will produce solid risk-adjusted returns. If you would like us to run another firm’s portfolio through our scoring system to check for factor exposure, let us know. We make no claims to a monopoly on great investment processes.

GARP strategies have almost been forgotten. Our team of veteran managers would happily recommend other proven GARP managers with track records longer than our own.

Our Growth at A Reasonable Price portfolio focuses on mispriced growth stocks and has been in production since 2012. With high concentration and low turnover, the portfolio underperformed the Russell 2500 Growth Index from 2018 - 2020. As documented extensively in our research, the period from 2017 - 2020 represented a speculative excess that eclipsed the dot.com mania.

The good news is our model portfolio - like almost any honest GARP strategy - has experienced a significant rebound. This paper offers a brief review of why we believe the model’s recent success is likely to continue and why investors should be focusing on putting money to work in mispriced growth now.

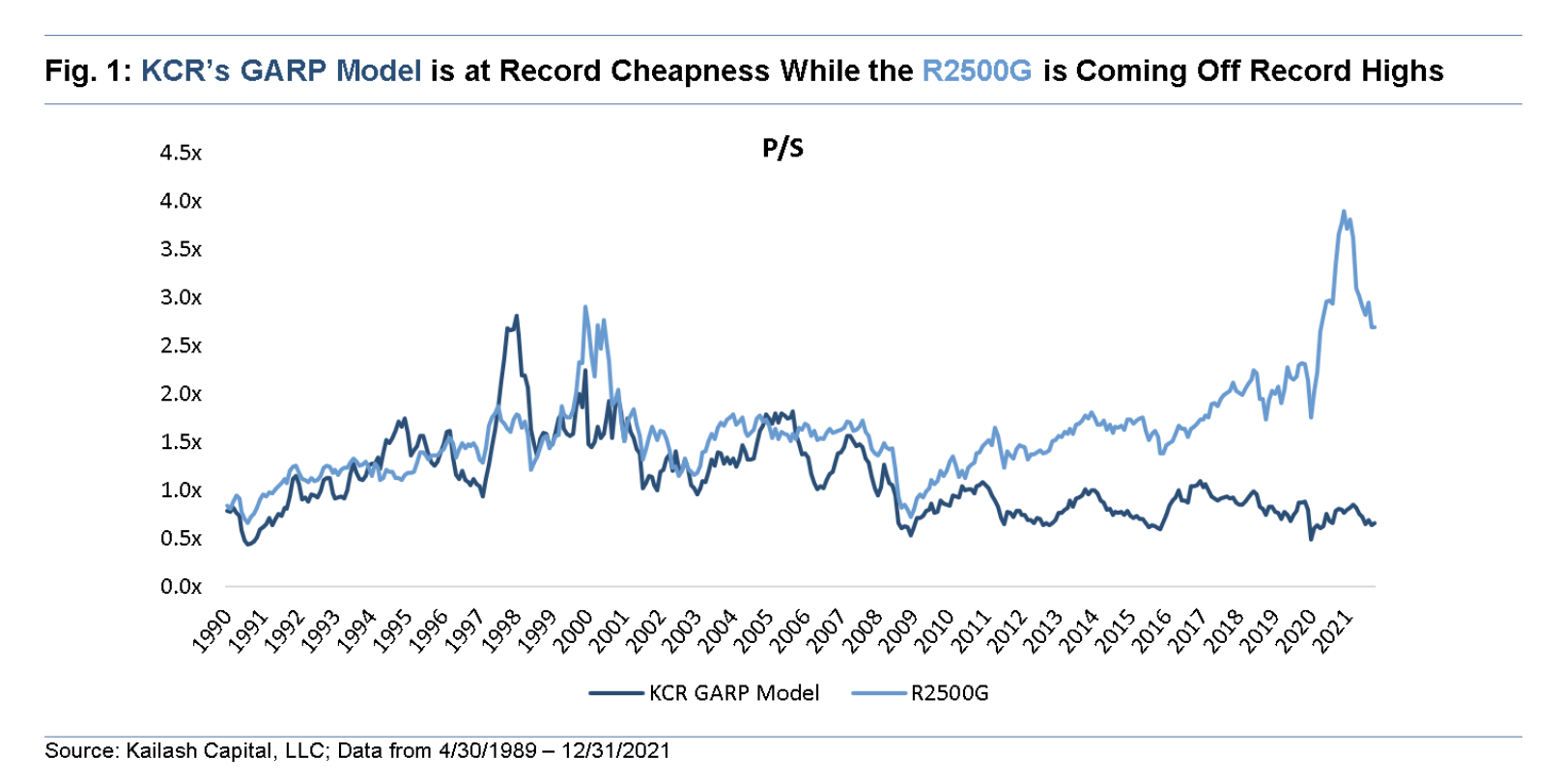

Figure 1 below shows the valuation of the Russell 2500G in light blue and KCR’s GARP Investment Portfolio in navy blue. We believe that the valuation spreads between the index and our GARP portfolio will continue to converge from never-before-seen spreads.

Index Investing & the Missing Margin of Safety in One Chart

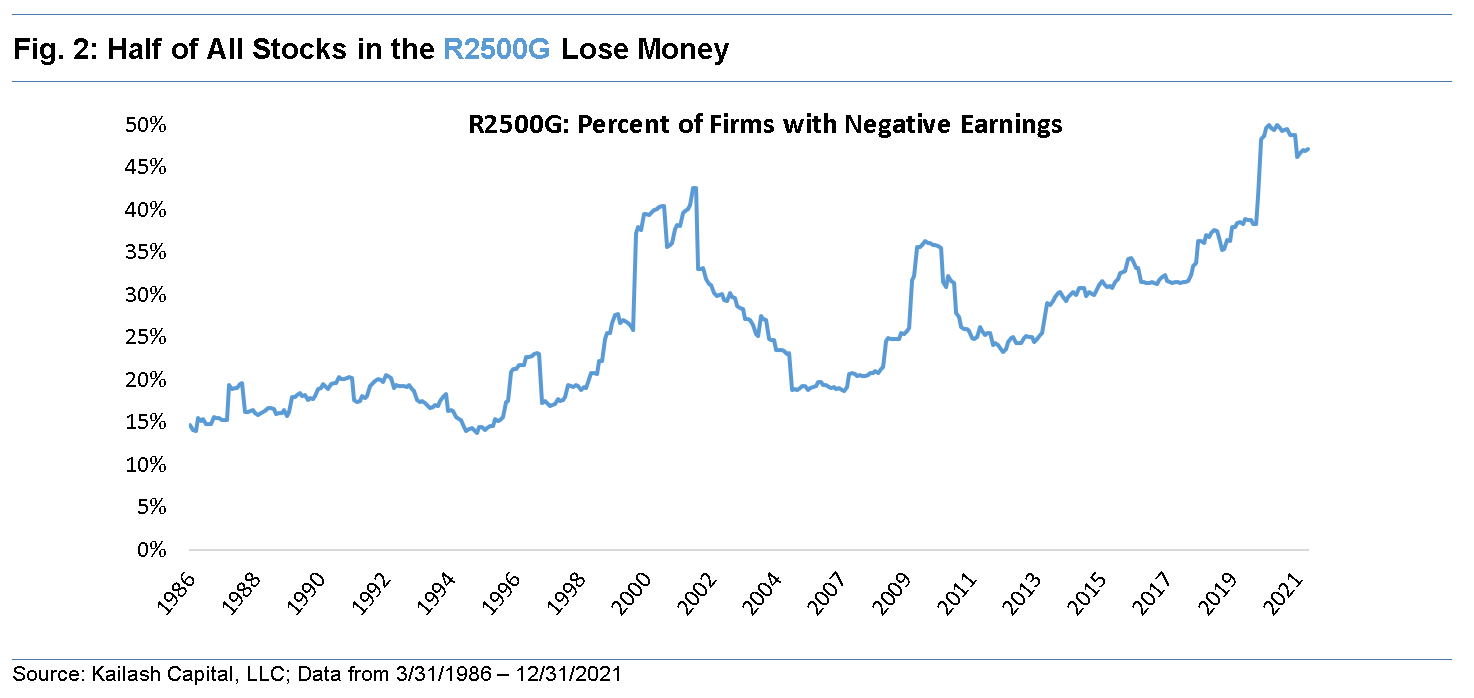

Figure 2 below offers one powerful and very simple reason to avoid indexing client money. In the Small & Midcap Growth universe, nearly 50% of the stocks in the index are losing money. Our site is filled with research explaining the horrible returns associated with stocks of loss-making firms compared to companies that make money.

This is as intuitive and as obvious as it seems. Indexing client money in the Small & Midcap space strikes us as needlessly hazardous behavior.

GARP Stocks: Getting Paid as Earnings Grow

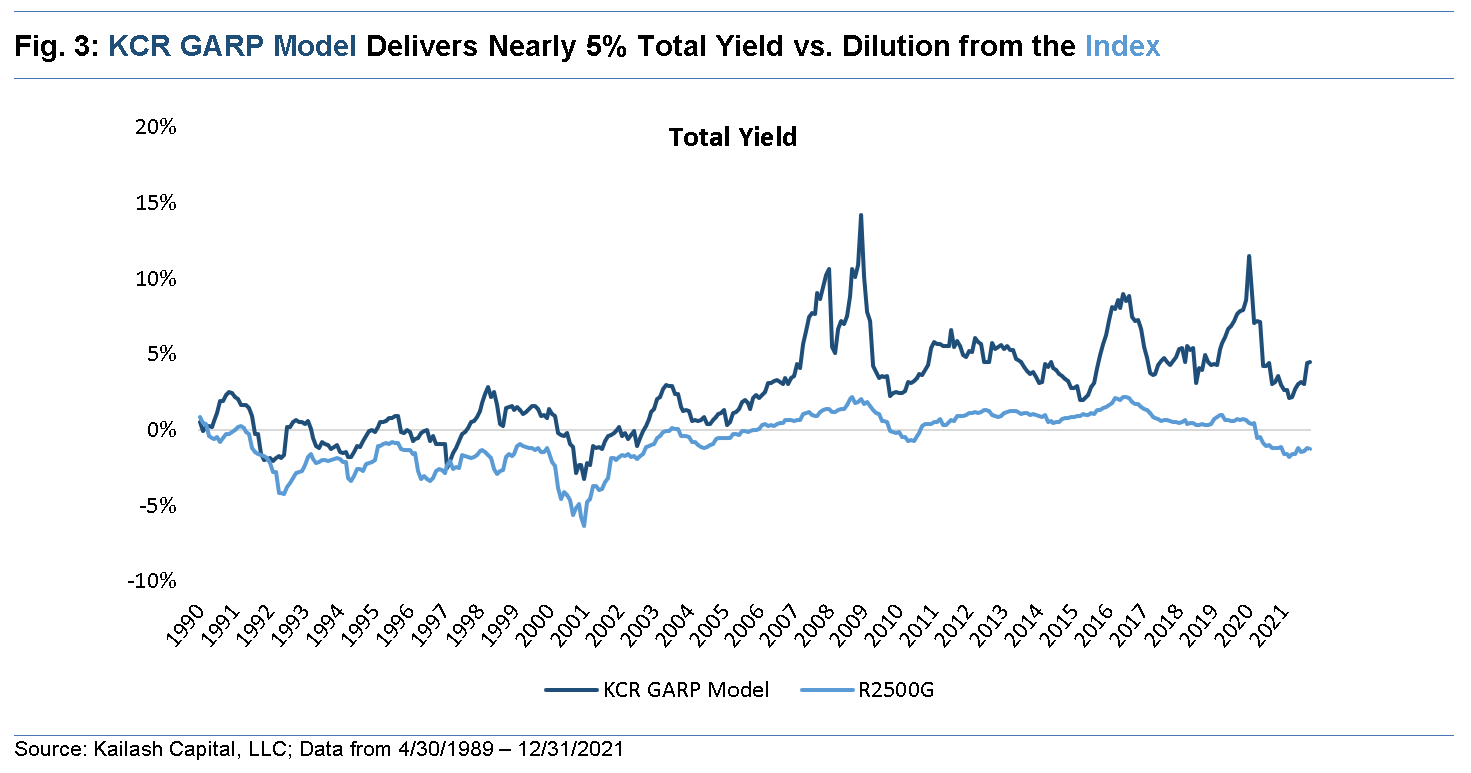

Figure 3 below shows the total yield of KCR’s GARP portfolio in navy blue vs. the Russell 2500G in light blue. We calculate total yield as: dividends + net repurchases. You can see that aside from growing profits far faster than the index, the GARP stocks in our portfolio offer you a 5% total yield - that is higher than the junk bond index.[1]

What strikes us, and we hope you, as alarming is that the Russell 2500 Growth Index has a negative yield. There are so many stocks in the index that are issuing equity to fund their operations that investors are actually being charged to own those stocks. Today, that dilution amounts to an incremental charge to investors of 1.3%. Our team believes this is a massive hidden charge for investors in index products.

[1] As represented by HYG which has a 4.45% yield and JNK which has a

In the three-year period between 2017 and 2020, investors in growth indexes were richly rewarded as speculation gripped markets. Starting in 2021, however, the valuations of speculative firms that came to dominate growth indexes exceeded any historical precedent and came under immense pressure. Our research indicates this reversion to the mean has much farther to go based on history.

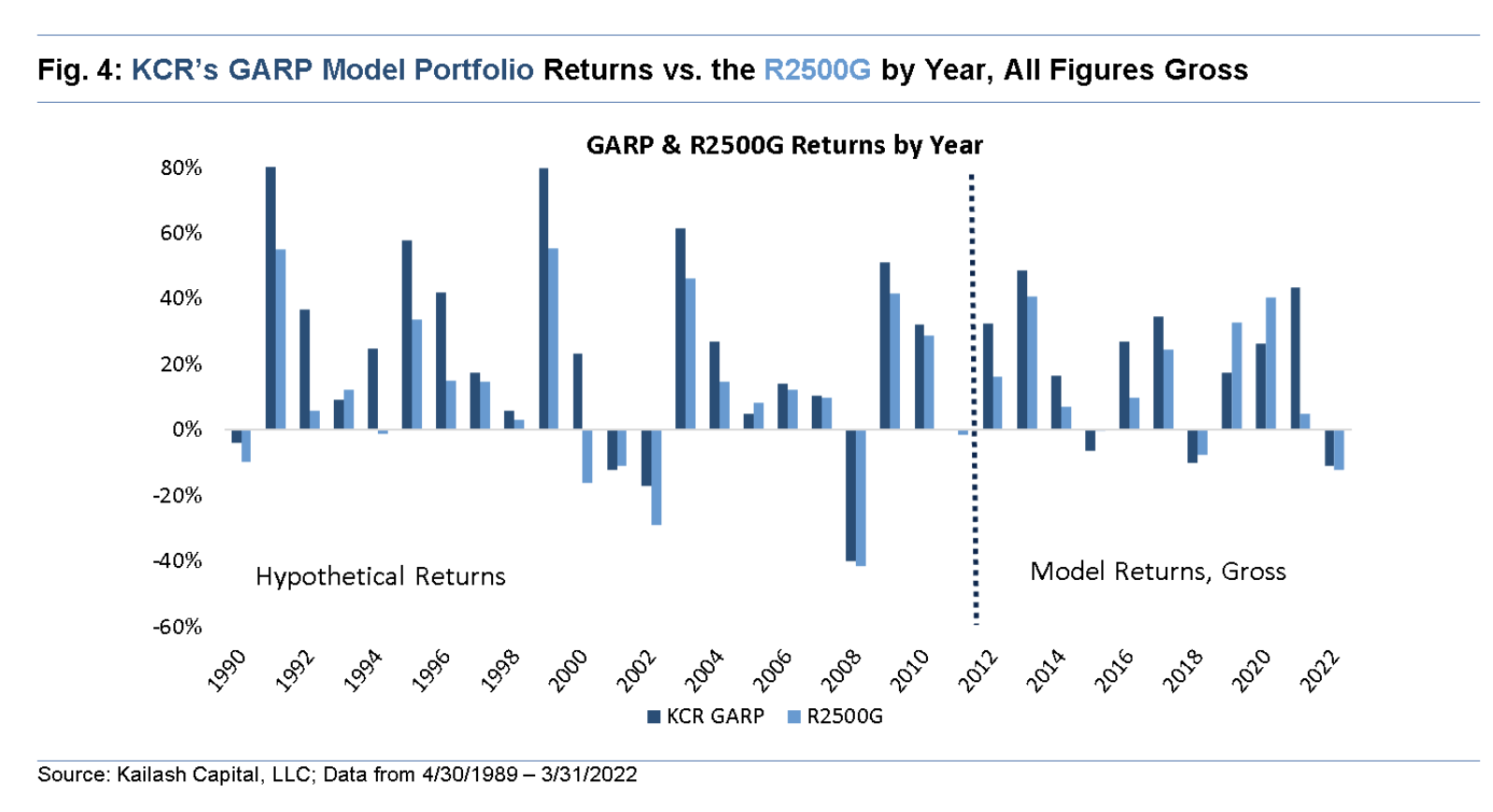

Figure 4 below shows the returns of our GARP Model Portfolio and the Russell 2500 Growth Index by year on a gross basis. You can see that our GARP portfolio has put up excellent results, excluding 2018, 2019, and 2020. In 2021 our model portfolio put up massive absolute and relative returns.

Conclusion: Getting Going on GARP Stocks

We believe the outlook for disciplined investors in GARP stocks has rarely been better than today. KCR is, first and foremost, a solutions provider. Our business model is predicated on the belief that helping people make better investing decisions is the first step in building the long-lasting relationships that our firm is known for.

Our powerful quantitative framework puts today’s markets in historical context to better identify pricing errors and investment opportunities. We hope to have triggered some thoughtful interest around investing in growth stocks trading at reasonable prices in this piece.

If you would like to learn more about KCR’s GARP model or hear our thoughts on some other GARP managers we believe are the best of breed please reach out to us. Our primary objective is to bring empirically robust and informed views to our clients and then help them locate the best solution for their specific needs. While our model portfolios are remarkably cost-efficient and scalable, we will happily point people to solutions outside our own business framework.

Kailash Capital’s sister company, L2 Asset Management, runs market neutral, long/short, and large-cap and mid-cap long-only portfolios with a value and quality bias. L2 employs a highly disciplined investment process characterized by moderate concentration, low turnover, high tax efficiency, and low fees. While nobody can predict the future, we believe the recent resurgence in risk-adjusted returns seen across all products are the beginning of what may be a long period where speculation is punished, and prudence and patience rewarded.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, © are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital, LLC and its affiliates (collectively, “Kailash Capital”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital. In preparing the information, data, analyses, and opinions presented herein, Kailash Capital has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital, however, does not perform an audit or seek independent verification of any of the data, statistics, and information it receives. Kailash Capital and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital, LLC shall have no obligation to recommend securities or investments in this publication as a result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

© 2022 Kailash Capital, LLC – All rights reserved.

© Kailash Concepts Research

Read more commentaries by Kailash Concepts Research