Since the beginning of 2022, we have seen:

- Two European nations fighting a war for the first time in 80 years

- Inflation in most Western economies at levels we have not seen since the early 80s

- Unpredictable behavior by the government of one of the largest economies in the world

- The commencement of the first central bank rate hike cycle since 2015, and the first one reacting directly to inflation since the 1970s

One can argue that all these events are related, which begs the question: has the global investment environment which we have grown accustomed to over the past few decades fundamentally changed?

The current generation of investors have lived under a set of assumptions: Falling interest rates. Globalization. Declining tax rates. All these trends are deflationary. What if they all changed?

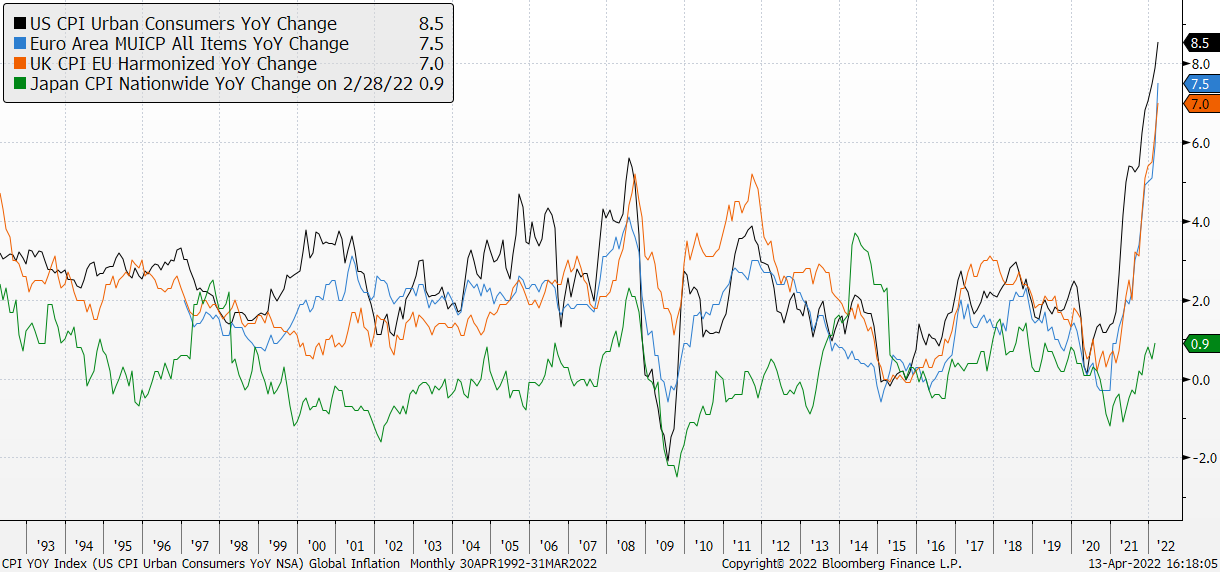

Inflation and Interest Rates

This chart represents annual inflation rates in the United States, Europe, the United Kingdom, and Japan over the past 30 years.

Causes of inflation vary across the world. In Europe, inflation is based in the rapid rise in food and energy prices. Western Europe has become dependent on Russian gas, and much of Europe and Africa depends on Russian and Ukrainian wheat. In the US, inflation is rooted in a combination of massive pandemic stimulus setting fire to the economy while the Federal Reserve stood by, unwilling to douse the flames. Globally, all economies are grappling with pandemic-related supply chain constraints.

Inflation at these levels or higher pushes interest rates higher. Through the end of April 10-year government yields rose in the US, the UK, and Europe by 1.42%, 0.93% and 1.11% respectively. Current forecasts have the Federal Reserve hiking rates seven or eight times by the end of the year. The European Central Bank is accelerating the end of its own asset purchase program, and the current outlook is for 10 rate hikes through the rest of 2022. The Bank of England leads everyone, following their December 25 basis point (bp) rate hike with further hikes in February, March, and May.

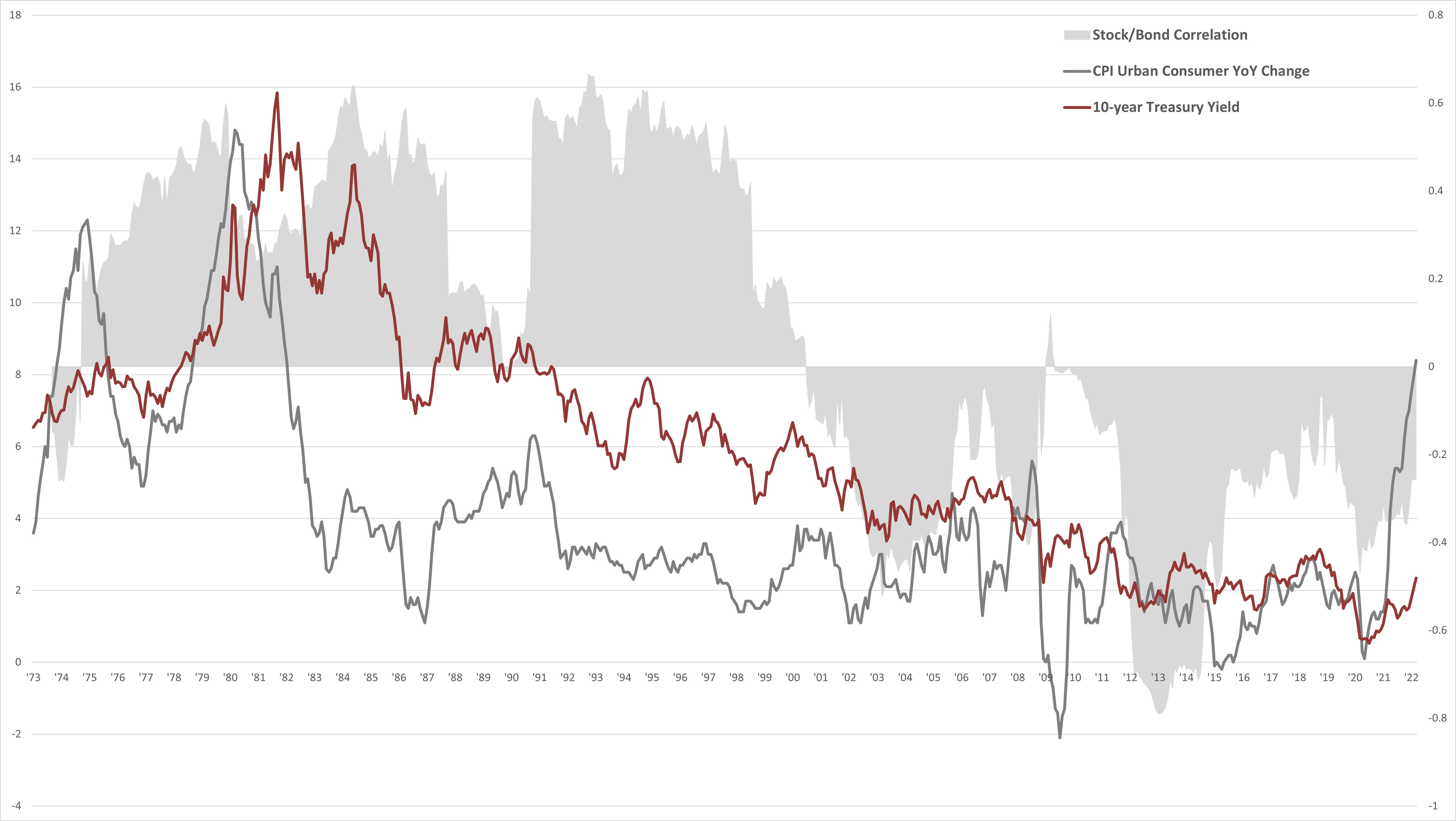

The following chart shows how these trends will affect the relationship between stocks and bonds. The red and black lines show the paths of the CPI and the 10-year treasury rate. The gray shaded area shows the correlation between returns for stocks and bonds. Since 2000, when 10-year Treasury rates fell comfortably and permanently below 5%, the correlation has been negative. Stock and bond returns have tended to move in opposite directions providing convenient diversification benefits. Before then, when rates and inflation were higher, the correlation was positive, and equity and bond returns moved in the same direction.

In the 20th century, investors’ primary macroeconomic focus was inflation, as the memories of the 1970s and Fed Chairman Paul Volker’s dramatic effort to squash inflation were still fresh. In the 21st century, prodded along by no less than two financial crises, global zero interest rate policies, and a pandemic, deflation became the investor’s greatest fear. The fading memory of inflation encouraged aggressive rate cutting and profligate government spending, ultimately hastening its return.

Negative correlation between stocks and bonds is the foundation of the 60/40 portfolio that provides the basis for contemporary asset allocation. A reversal in this relationship will force investors to find other options to diversify their returns.

And I Feel Fine…

The pieces are in place for regime change in financial markets. Geopolitically and economically, we are witnessing events unseen for 20, 30, even 40 years. If inflation proves to be more resilient, expect many of the trends of the past decades to reverse – bond returns, active manager underperformance (in large cap, at least), value versus growth, small caps versus large, international stocks versus US stocks -- the list is long.

While traditional foundations of inflation are in place – higher commodity prices, tight labor markets, central bank money printing -- keep in mind that the economy of the 2020s is not the economy of the 1970s. While globalization is on the wane, financialization is not. Flexible capital flows are quickly directed to choke points or areas of scarcity, rapidly mitigating sources of higher costs. The best cure for high prices is…high prices. History will be a guide for us in such times, but as Mark Twain said, it will only rhyme. Just as important is whether central banks and governments, especially the Federal Reserve, can successfully navigate this cycle without damaging economic growth. Their record is…mixed.

Derek Izuel is the chief investment officer at Shelton Capital Management.

© Shelton Capital Management

Read more commentaries by Shelton Capital Management