Pressure Testing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn the depths of the COVID downturn and recovery, we made an effort to stop using the word “unprecedented.” While it was true that the economy had never seen such a tremendous contraction and bounce back, the word did not aid anyone’s understanding of how to deal with the crisis. Two years later, as we contemplate the growth outlook, we again are in unexplored territory: Recession fear continues to rise, but the markers of a classical recession are not yet evident.

Our primary source of confidence in growth is the strong state of the labor market. As long as people are working, economic activity will carry on and recession risk is mitigated. Inflation is a growing constraint, placing the expansion at risk. Our base case remains a growth slowdown, but not an outright recession.

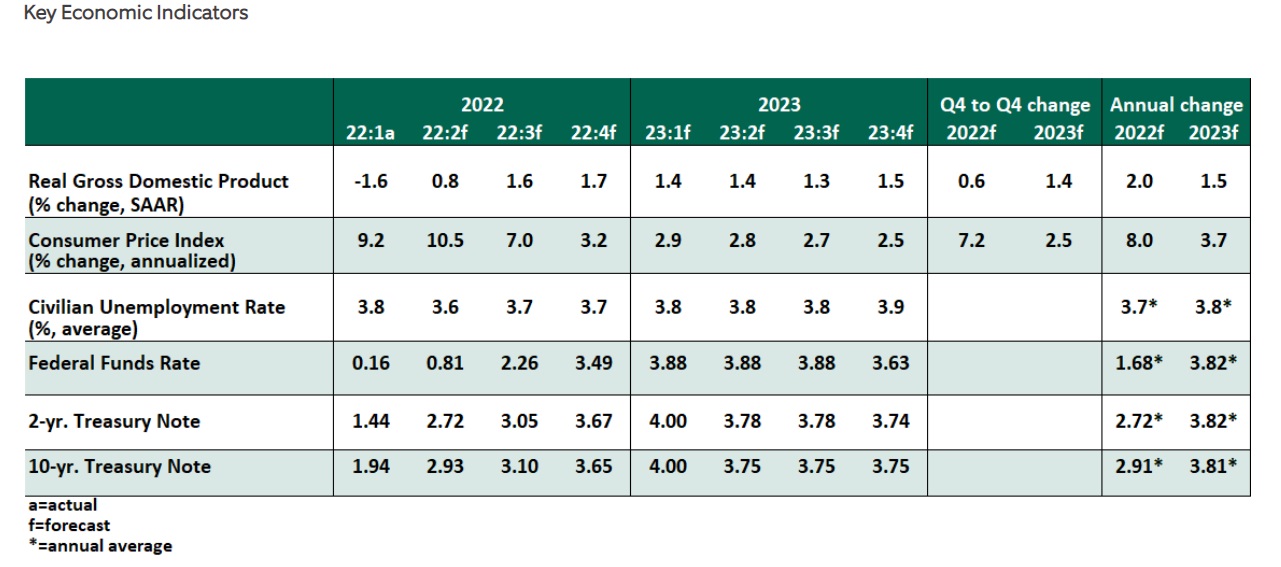

Influences on the Forecast

- Growth is at an inflection point. Gross domestic product (GDP) technically contracted in the first quarter due to slower inventory accumulation and a widening trade deficit. Ongoing supply constraints will weigh on the second quarter’s results, as well. However, the core of U.S. economic activity is consumer spending, which has not stopped but is dampened by inflation. For example, through June, nominal retail sales grew 8.4% year over year—an encouraging growth rate at first glance, but net negative when adjusted for inflation. We have revised down our growth forecast for the year ahead, but we expect the economy to avoid a recession.

- The consumer price index (CPI) report for June reflected persistently elevated inflation, with prices increasing 9.1% over the past year. While energy has been a primary source of pain, even core inflation (excluding food and energy) grew by 5.9%; the monthly changes to core prices show a troubling rise over the past four months.

- The runup in energy costs in the first half of the year appears to have abated, giving hope for lower readings to follow starting in July. Falling motor fuel prices, in particular, will ease some inflation worries, but their descent will be uncomfortably slow.

- Our outlook for inflation next year has been revised higher, as some of today’s inflation drivers are likely to linger. Rising shelter costs appear with a lag: rent measurements include all rents in force, but measures of asking rents on new leases are much higher than the 5.8% annual gain shown in the CPI tables. The cost of homeownership, shown as owners’ equivalent rent of 5.5%, also has much ground to recover to reflect actual house price appreciation over the past two years.

- The employment report for June continued an 18-month streak of job creation. Net of small downward revisions to prior months’ estimates, about 300,000 payrolls were added. The survey of households showed a minor decline in the labor force, which may forewarn a shift to slower hiring in the balance of the year. Employment remains about 500,000 workers shy of the February 2020 peak. Demand for labor is not abating, as surveys of job openings continue to show nearly two open positions for every unemployed worker.

- Wages grew by 5.1% over the past year, continuing a declining trend from a peak of 5.6% in March. Slower wage growth suggests that today’s inflation will not enter a dangerous wage-price spiral, but this cost will keep upward pressure on final prices.

- Every past recession has featured a significant decline in employment. As such, evidence of labor market strength is reassuring. We continue to watch weekly initial unemployment claims, which have risen from historic lows seen earlier in the year, but have settled into the range that was typical prior to COVID-19.

- At its June meeting, the Federal Open Market Committee raised the Federal Funds rate by a larger than expected 75 basis points, and signaled a willingness to continue moving in these large increments. With inflation staying high and labor markets still tight, we expect another increase of 75 basis points at the July 27 meeting, with steady hikes to follow, taking the overnight rate to a peak of 3.75-4.00% by the end of the year.

- Rapid increases to the overnight rate risk bringing the full Treasury yield curve into an inversion, a reliable recession signal. If long-end rates do not increase, or if any other signs of softening emerge, the Fed’s governors can downshift their tightening. For now, though, front-loaded hikes are in order.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All